RV insurance costs vary widely depending on your vehicle type, coverage choices, and driving history. At Direct Insurance Services, we’ve seen premiums range from a few hundred to several thousand dollars annually, and understanding what drives these prices helps you make smarter decisions.

This guide breaks down the real factors affecting your rates and shows you practical ways to reduce what you pay.

What Drives Your RV Insurance Costs

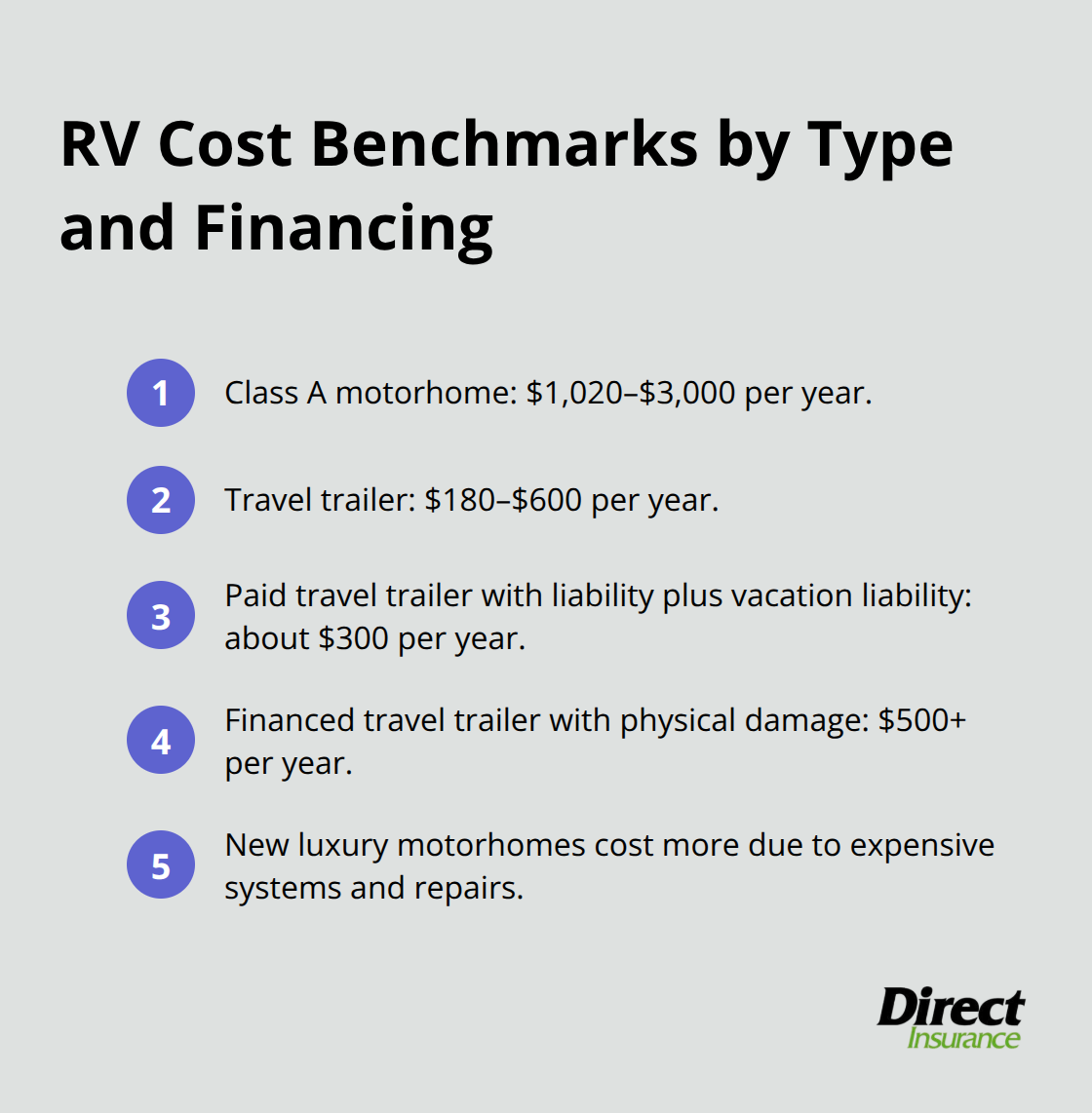

Your RV insurance premium isn’t a mystery-it’s built on concrete factors that insurers measure every day. The type of RV you own matters most. A Class A motorhome costs $1,020 to $3,000 annually and substantially outpaces a travel trailer at $180 to $600 per year, according to real market data. This gap exists because Class A motorhomes are larger, more expensive to replace, and carry higher liability exposure. If you finance your RV, lenders require comprehensive and collision coverage on top of liability, which automatically increases your annual cost.

A fully paid travel trailer might cost $300 per year with just liability and vacation liability coverage, while the same trailer financed could jump to $500 or more once physical damage protection enters the equation. New luxury motorhomes push premiums even higher due to advanced systems like integrated solar panels, smart technology, and high-end generators-repairs for these features run into thousands of dollars when something breaks.

How Your Driving History Shapes Your Rate

Your personal driving record is one of the few factors you can control. Drivers with clean records pay noticeably less than those with accidents or violations. A single at-fault accident raises your premium by 10-20% or more, while a speeding ticket might add 5-10%. Full-time RVers are seeing premiums rising approximately 22% over the previous year, partly because higher usage means more exposure to claims. Your age and experience matter too-veteran RV operators qualify for lower rates than new drivers. If you complete an RV safety program, many insurers offer discounts that offset the course cost within a year. Your claims history follows you; filing a claim in the past three years signals higher risk to underwriters, even if the claim was minor. Storage location and security measures directly impact your rate as well. An RV parked in a garage or covered facility with an alarm system qualifies for lower comprehensive premiums than one left exposed in a driveway or high-theft area.

Coverage Choices Set Your Price

The coverage limits and deductibles you select determine what you actually pay each month. A liability-only baseline policy starts around $125 per year for minimal protection, while full coverage with comprehensive, collision, and optional add-ons can exceed $4,000 annually. Raising your deductible from $250 to $500 or $1,000 directly lowers your premium-sometimes by 15-30%-but increases what you pay out-of-pocket if you file a claim. Optional coverages like roadside assistance, total loss replacement, personal effects protection, and emergency expense coverage each add to your premium (typically $50-150 per year per add-on). The choice between actual cash value and agreed value settlement also affects cost; agreed value guarantees a preset payout if your RV is totaled, while actual cash value pays depreciated value and often leaves owners with shortfalls. Your location within the country shifts your premium significantly-Michigan motorhome owners face rates up to $4,500 annually due to weather and theft risk, while Oregon averages around $1,100 or less.

Full-Time Living Requires Different Coverage

Full-time RVers who live in their vehicle 150 or more nights per year need hybrid auto and homeowners protections that include personal liability, medical payments for guests, and loss assessment coverage. This comprehensive approach naturally costs $1,500-$4,000 annually compared to $300-$800 for recreational users. The difference reflects the reality that full-time residents face exposure similar to homeowners-guests visit, property sits in one place longer, and liability risks multiply. Seasonal storage in certain areas (such as Upstate New York) with storage-only policies can reduce premiums while still covering fire, theft, or vandalism. Understanding whether you’ll use your RV full-time or seasonally shapes not just your premium but the entire coverage structure you need.

What You Actually Pay for Each Coverage Type

Liability coverage forms the foundation of any RV policy, and it’s the only protection legally required for motorized RVs in most states. A baseline liability-only policy starts around $125 per year, making it the cheapest entry point for RV owners. However, this bare-minimum coverage leaves you exposed to catastrophic financial risk if you cause injury or property damage. Try liability limits of at least $100,000 per person and $300,000 per accident, which typically runs $300–$600 annually depending on your RV type and driving record.

Liability Coverage Gaps You Need to Address

Travel trailer owners often overlook a critical gap: their tow vehicle’s liability policy may not fully cover incidents that occur while the trailer sits parked at a campground or when someone is injured on the property. Vacation liability coverage specifically addresses this exposure and costs roughly $50–$100 extra per year, but it protects you if a guest is injured while visiting your RV. Motorhome owners face higher liability premiums than trailer owners because the vehicle itself is motorized and presents active driving risk; a Class A motorhome with solid liability limits costs $400–$800 annually just for this coverage.

Collision and Comprehensive: Where Costs Spike

Collision and comprehensive protection cover damage to your RV itself, and these costs escalate dramatically based on your vehicle’s value and age. Comprehensive coverage (fire, theft, vandalism, weather) typically costs $200–$500 annually for a travel trailer but can exceed $1,200 for a new luxury Class A motorhome. Collision coverage (damage from accidents) adds another $250–$800 depending on your deductible choice. A $500 deductible costs substantially more than a $1,000 deductible-sometimes 20–30% more-so selecting the right deductible is critical to managing your total premium.

Full-Time Living Multiplies Your Costs

Full-time RVers who live in their vehicle year-round face annual premiums of $1,500–$4,000 because insurers view continuous occupancy as higher risk and require homeowners-like protections including personal liability, medical payments for guests, and loss assessment coverage. These full-time policies often bundle auto and homeowners elements, which explains the dramatic cost jump from recreational use. A part-time RV user who travels weekends might pay $300–$800 annually for the same motorhome model that costs a full-timer $2,500–$3,500, illustrating how usage patterns directly control what you pay.

The coverage you select and how you use your RV determine whether you’re paying a few hundred dollars or several thousand annually. Understanding these price drivers positions you to make informed choices about what protection actually makes sense for your situation-and that’s where shopping for quotes from multiple carriers becomes your most powerful tool.

Cut Your RV Insurance Costs Without Cutting Coverage

Bundle Your Policies for Maximum Savings

The most effective way to lower your RV insurance premium is consolidating your auto, home, and RV policies with a single carrier. Insurers reward this loyalty aggressively-bundling typically saves 15–25% on your total insurance spend. If you currently insure your tow vehicle and home separately, consolidating everything under one policy can drop your RV premium by $100–300 annually. A homeowner paying $1,200 for auto and home coverage might add RV insurance for $400 instead of $600 when bundled. As an independent agency, Direct Insurance Services works with top-rated carriers to help you find bundling options that fit your specific needs and budget.

Control What You Can: Your Driving Record and Safety Choices

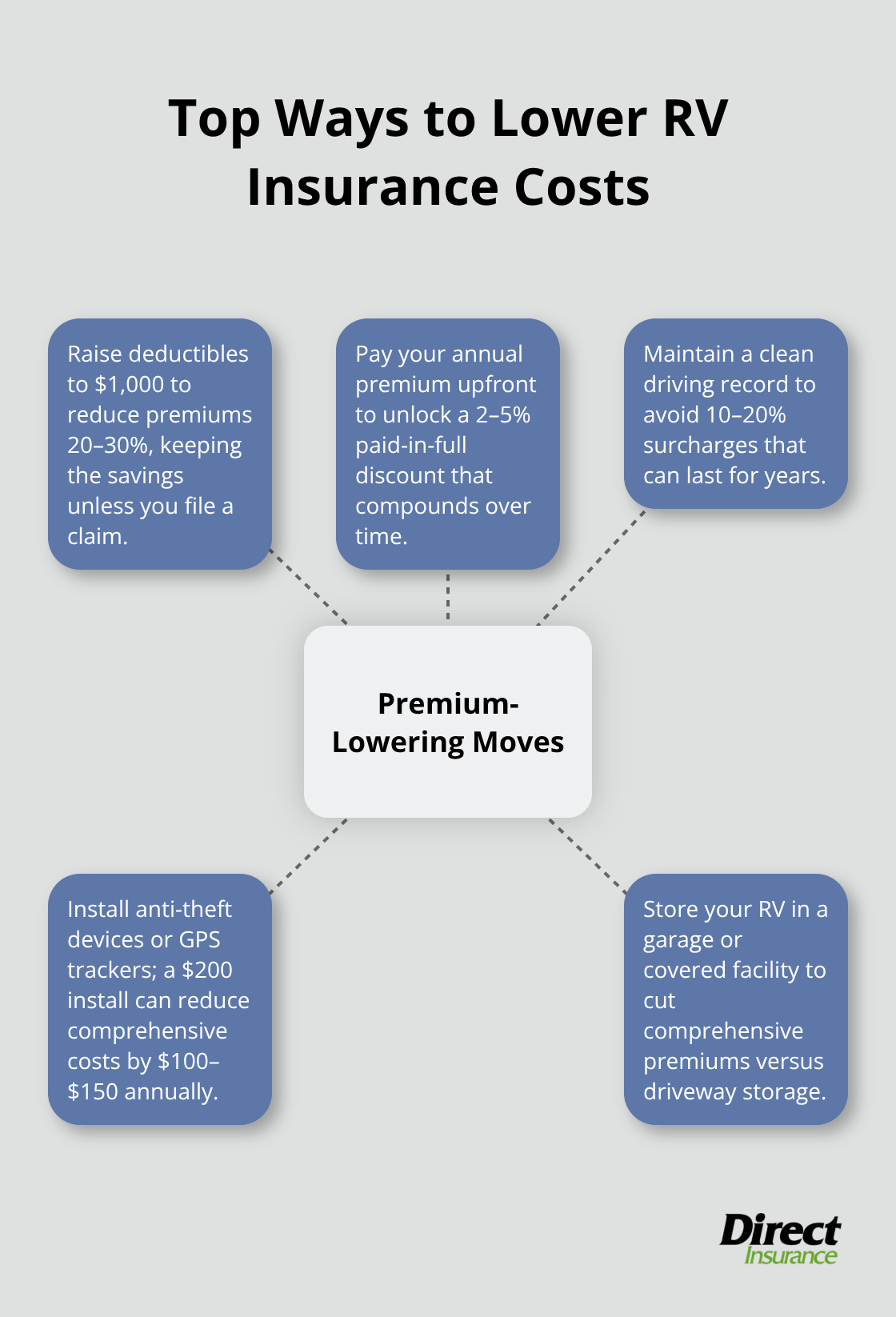

Your driving record remains the single most controllable lever you have. One accident or violation raises your premium 10–20% for three to five years, so avoiding claims is worth far more than any discount you could negotiate. Completing an RV safety course through organizations like the RV Industry Association qualifies you for discounts at most carriers and costs $50–150 for the course-a breakeven within months. Anti-theft devices and GPS trackers installed on your RV directly lower comprehensive premiums because insurers view them as loss prevention tools; a $200 installation can reduce your annual comprehensive cost by $100–150. Storing your RV in a garage or covered facility rather than leaving it exposed in a driveway or parking lot cuts comprehensive premiums noticeably because theft and weather damage risk drops substantially.

Optimize Your Deductible and Payment Strategy

The deductible you choose is where most people leave money on the table. Raising your collision and comprehensive deductible from $250 to $1,000 typically reduces your premium 20–30%, and unless you file a claim, you pocket that entire savings. A travel trailer owner paying $450 annually with a $250 deductible might drop to $315 with a $1,000 deductible-$135 saved every year with zero added risk if you drive carefully. Paying your annual premium upfront instead of monthly sometimes qualifies you for a 2–5% paid-in-full discount that compounds year after year.

Maintaining continuous coverage without lapses signals stability to underwriters and unlocks claim-free renewal discounts, which can reach 10–15% after three years of no claims.

Shop Multiple Carriers and Leverage Your Location

Shopping quotes across at least three to five different insurers is non-negotiable because pricing varies wildly for identical coverage. One first-time RV buyer received a quote of $92 monthly from one carrier for a 33-foot travel trailer, then switched to another insurer at $40 monthly for the same vehicle and coverage-a 57% price reduction that amounts to $624 annually. Independent insurance agents can access quotes from roughly 24 different carriers simultaneously, eliminating the tedious process of contacting each company individually. Your zip code and storage location matter more than most people realize because coastal areas and high-theft regions carry premiums 20–40% higher than rural or low-risk zones.

If you store your RV seasonally and don’t use it during winter months, ask about storage-only policies that reduce your premium while maintaining fire, theft, and vandalism protection. Discounts for RV club membership, military service, or professional affiliations vary by carrier but typically range from 5–10% and stack on top of other discounts you’ve already earned.

Final Thoughts

RV insurance costs depend on factors you control and factors you don’t, but understanding them gives you real leverage to reduce your premiums without sacrificing protection. Your RV type, coverage selections, driving record, and usage patterns determine what you pay annually-whether that’s $300 for seasonal travel or $4,000 for full-time living. Shopping around directly impacts your wallet because pricing varies dramatically for identical coverage, with some buyers finding 57% price differences between insurers for the same vehicle.

Start by requesting quotes from multiple carriers and bundling your auto, home, and RV policies with one carrier to unlock 15–25% savings across your entire insurance portfolio. Raise your deductible to $1,000 if you can absorb that out-of-pocket cost, since this single move typically cuts your premium 20–30%. Install anti-theft devices, store your RV in a garage or covered facility, and complete an RV safety course to qualify for additional discounts that pay for themselves within months.

Your driving record matters most because one accident or violation raises rates 10–20% for years, while maintaining continuous coverage without lapses and avoiding claims unlocks claim-free renewal discounts that reach 10–15% after three years. Ask about storage-only policies if you don’t use your RV during winter months, and explore discounts for RV club membership or military service. Contact Direct Insurance Services today to get personalized quotes and discover how much you can actually save on your RV insurance.