How to Find the Most Affordable Auto and Home Insurance

Finding the most affordable auto and home insurance requires more than just picking the lowest price. Smart shoppers compare multiple factors beyond premium costs.

We at Direct Insurance Services see clients save hundreds of dollars annually by using proven strategies. The right approach can cut your insurance expenses by 20-40% without sacrificing coverage quality.

What Really Drives Your Insurance Costs

Your Personal Risk Profile Sets the Foundation

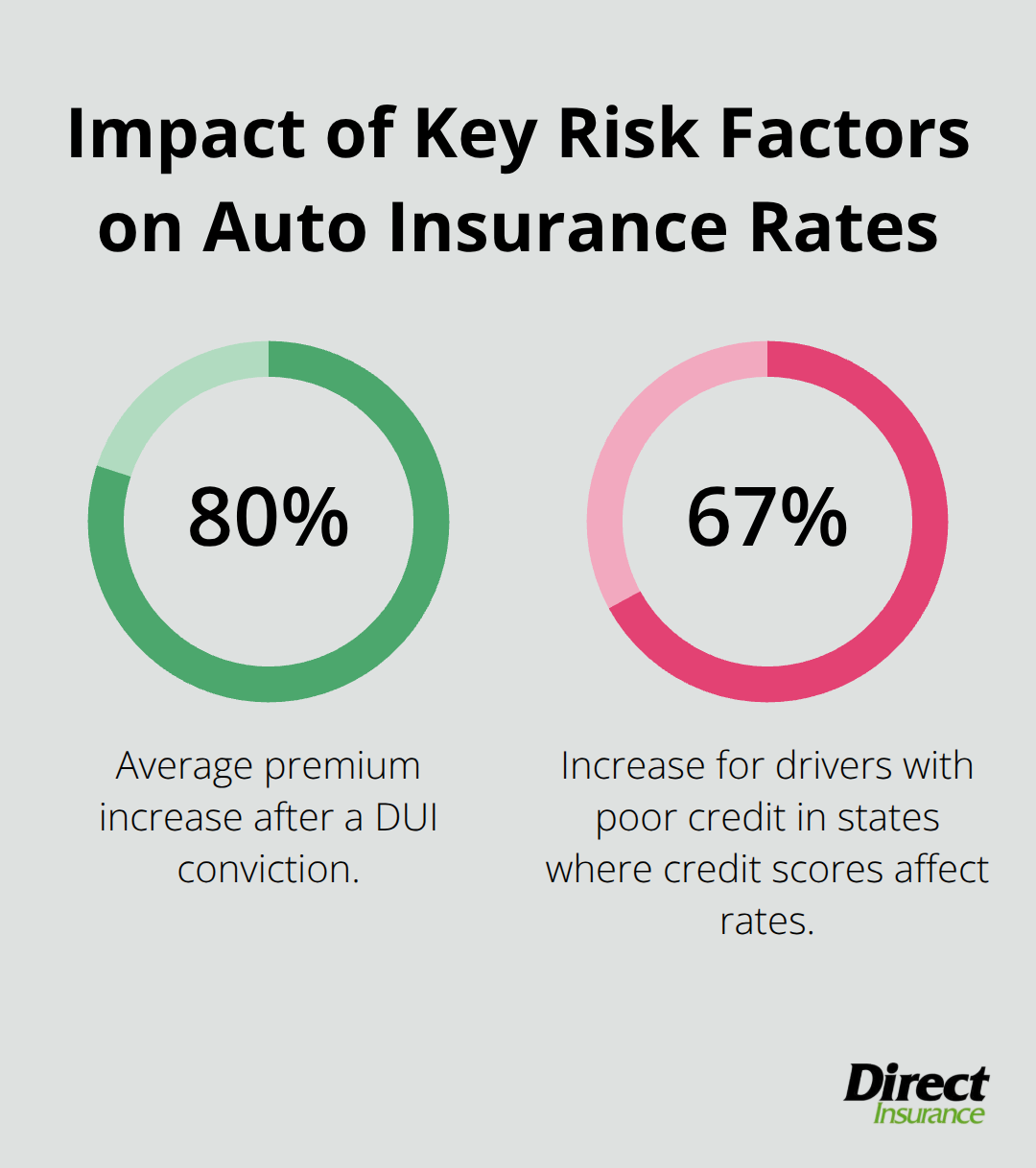

Insurance companies analyze over 200 data points to calculate your premiums. Your auto coverage depends most heavily on your record behind the wheel. A single speeding ticket increases your rates by 13-15% according to Insurance.com data, while a DUI conviction raises premiums by an average of 80%.

Credit scores play an equally significant role – drivers with poor credit pay 67% more than those with excellent credit in states where credit scores affect rates.

Home insurance calculations focus heavily on your property’s location and construction details. Homes within 1,000 feet of fire stations receive discounts of 5-10%, while properties in high-crime zip codes face surcharges of 15-25%. The age of your roof matters tremendously – roofs over 20 years old trigger premium increases of 10-20% or coverage restrictions.

Geographic Location Trumps Individual Factors

Your zip code determines roughly 60% of your insurance costs before companies even consider your personal information. Michigan drivers pay an average of $2,878 annually for full coverage auto insurance, while Maine residents pay just $1,175 – a 150% difference driven purely by state regulations and claim frequencies. Weather patterns create similar disparities for homeowners insurance (Oklahoma residents pay triple the national average due to severe storm frequency).

Most People Misunderstand Deductible Mathematics

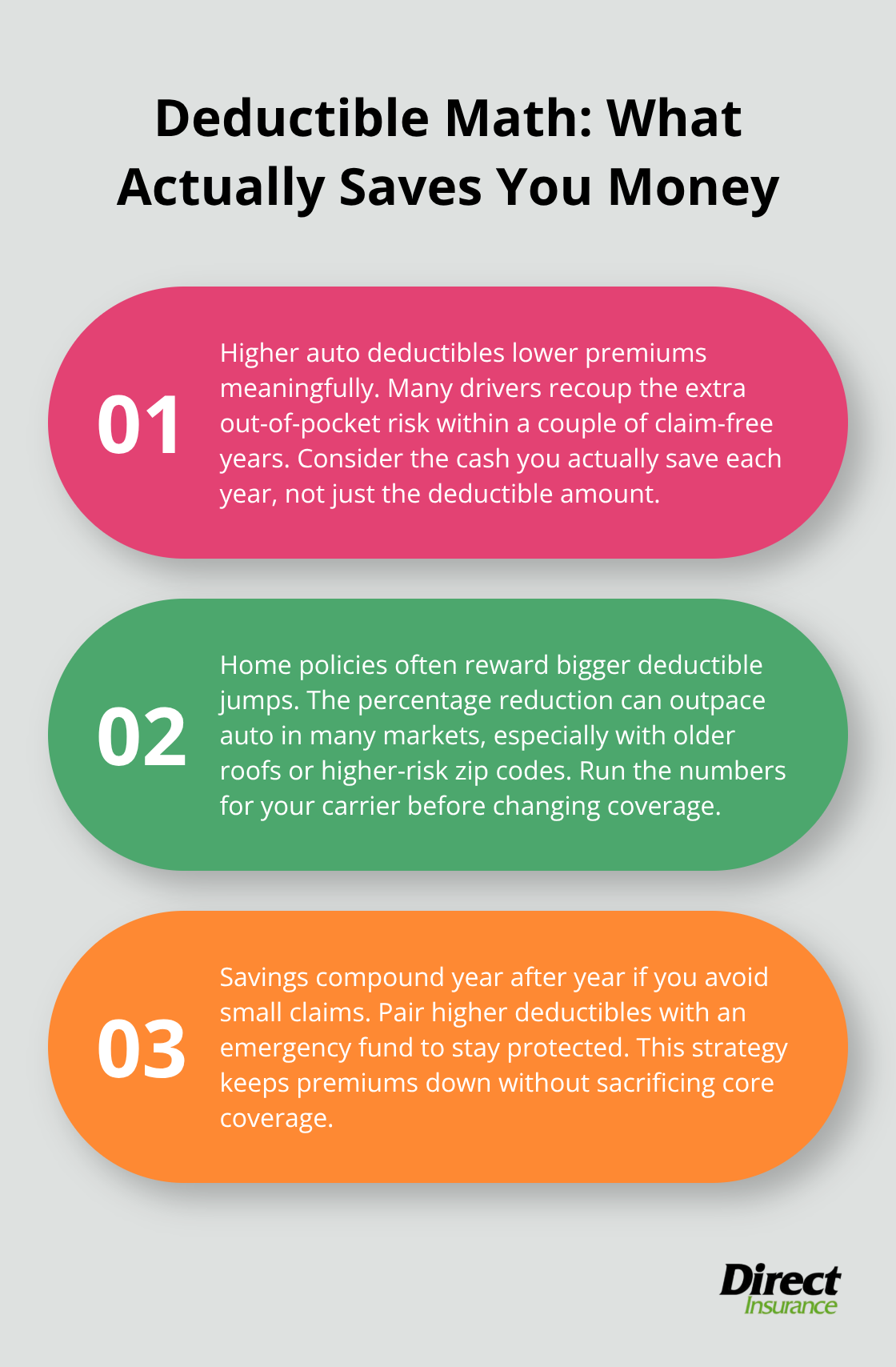

The biggest misconception involves deductible selection. Drivers who raise their auto deductible from $500 to $1,000 typically reduce premiums by 25-30%, which saves most people $200-400 annually. This means you recover the higher deductible cost in just 1-2 years of claims-free operation. Home insurance shows even greater savings – homeowners who increase deductibles from $1,000 to $2,500 can cut premiums by 12-25% depending on their insurer.

These cost factors create the foundation for smart comparison tactics that can dramatically reduce your annual insurance expenses.

How Can You Cut Premiums Without Losing Protection

Multi-Policy Bundling Delivers Immediate Savings

Carriers automatically apply discounts of 5-25% when you combine auto and home insurance policies. Progressive offers up to 12% savings, while State Farm provides discounts that reach 17% for bundled customers. Insurers reward customer loyalty and reduce their administrative costs through these arrangements.

A family that pays $1,200 annually for auto coverage and $800 for homeowners insurance saves $240-400 per year through bundling alone. The math becomes even more compelling when you add umbrella policies (which cost just $150-300 annually but provide $1-2 million in additional liability protection).

Strategic Deductible Increases Generate Long-Term Value

Auto premiums drop by 16 percent when you raise your deductible from $250 to $1,000. Homeowners coverage shows similar patterns – deductibles that increase from $500 to $2,500 reduce annual costs by 12-40% depending on your location and carrier.

A homeowner who pays $1,500 annually and raises their deductible to $2,500 typically saves $300-600 per year. The higher out-of-pocket cost pays for itself within 2-4 years if you avoid claims, and most homeowners file claims less than once every 10 years.

Discount Categories Most Customers Never Request

Insurance companies offer 50+ discount categories that remain unused by most policyholders. Safe driver discounts reduce auto premiums by 10-23%, while defensive courses provide additional 5-10% savings that last three years. Home security systems generate 5-20% discounts, and newer homes with updated electrical, plumbing, and roof systems qualify for construction-related savings of 8-15%.

Military service, professional associations, and alumni groups often provide exclusive discounts of 5-12%. Ask your agent to review every available discount annually, as qualification requirements and discount amounts change frequently.

These proven cost-reduction strategies work best when combined with smart comparison tactics that identify the carriers offering the most competitive rates for your specific situation.

Where Should You Shop for Insurance Quotes

Quotes from at least five different carriers reveal price differences of 30-50% for identical coverage. NerdWallet research shows auto insurance rates vary by $1,200-2,000 annually between the highest and lowest quotes for the same driver profile. Home insurance disparities reach even greater extremes – identical properties receive quotes that differ by $800-1,500 per year.

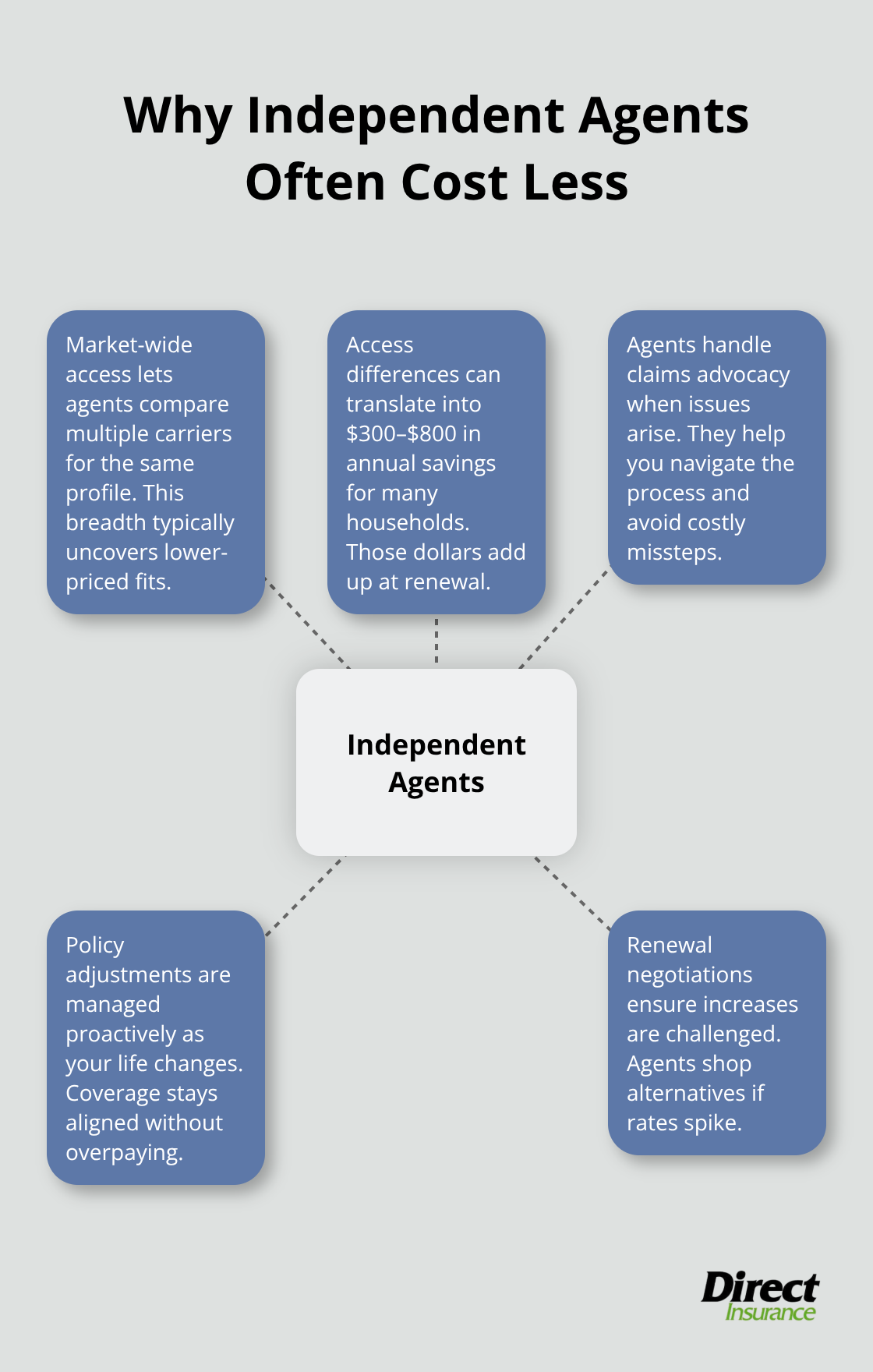

Direct Carrier Websites Miss Critical Discount Opportunities

Major insurers like Geico and Progressive push online quotes, but their automated systems miss 40-60% of available discounts. These platforms cannot evaluate complex scenarios like multi-vehicle households, home business operations, or specialty vehicle coverage. Independent agents access wholesale rates that direct carriers reserve for broker channels, often with premiums 8-15% lower than published online rates.

Independent Agents Provide Market-Wide Access

There are two types of insurance agents: captive agents and independent agents. While both roles have certain similarities, there are also major differences. Independent agents represent multiple carriers simultaneously, while captive agents sell only one company’s products. This access difference translates to savings of $300-800 annually for most households. Independent agents also handle claims advocacy, policy adjustments, and renewal negotiations that online platforms ignore completely.

Annual Reviews Capture Rate Changes and Life Updates

Insurance companies adjust their rates quarterly, which creates fluctuations of 5-20% that affect different customer segments unpredictably. Customers who skip annual reviews miss these market shifts and overpay by $200-600 per year on average. Life changes like marriage, new vehicles, home improvements, or job relocations trigger rate adjustments that require immediate policy updates to maintain optimal rates and coverage adequacy (these updates often take just one phone call to complete).

Market conditions shift constantly, and carriers modify their appetite for different risk profiles throughout the year. What made one company competitive last year may no longer apply to your current situation.

Final Thoughts

Customers who compare quotes across multiple carriers and adjust their policies strategically save $400-1,200 annually on the most affordable auto and home insurance. The data proves that bundled policies, higher deductibles, and annual reviews deliver consistent savings compared to accepting initial quotes. Smart shoppers who work with independent agents access wholesale rates that direct carriers reserve for broker channels.

Independent agents provide ongoing value through claims advocacy and market monitoring as your circumstances evolve. These professionals track quarterly rate adjustments and carrier appetite changes that affect your premiums throughout the year. We at Direct Insurance Services help Utah families navigate carrier options and maximize available discounts through our independent agency model.

The insurance market shifts constantly, with carriers modifying rates and risk preferences every quarter (annual reviews capture these changes before they impact your budget). Customers who maintain active relationships with their agents avoid the gradual premium increases that affect set-and-forget policies. Professional guidance transforms adequate coverage into optimal protection at competitive rates.