Choosing the Right Deductible for Your Auto Insurance

Picking what deductible for auto insurance can save you hundreds of dollars annually or cost you thousands when accidents happen. Most drivers choose their deductible without understanding the real financial impact.

We at Direct Insurance Services see clients struggle with this decision daily. The right deductible balances your monthly budget with your ability to handle unexpected repair costs.

How Auto Insurance Deductibles Actually Work

Your auto insurance deductible represents the amount you pay before your insurance company covers the remaining repair costs after an accident. When you file a claim for $3,000 in damage and carry a $500 deductible, you pay $500 and your insurer pays $2,500. The Insurance Information Institute reports that 80% of drivers have comprehensive coverage, with average auto insurance expenditure reaching $1,127 in 2022.

Coverage Types That Include Deductibles

Deductibles apply to collision coverage when you hit another vehicle or object, and comprehensive coverage for theft, vandalism, or weather damage. Your liability coverage never includes a deductible because it pays for damage you cause to others. Some states require deductibles for uninsured motorist property damage and personal injury protection (PIP). Progressive and other major insurers offer identical deductible amounts across both collision and comprehensive coverage, though you can select different amounts for each type.

Premium Impact of Deductible Changes

When you raise your deductible from $500 to $1,000, you typically reduce your collision and comprehensive premiums by 10% to 30% according to industry data. A driver who pays $1,200 annually could save $120 to $360 per year with this change. However, you must pay the higher deductible every single time you file a claim that qualifies. NerdWallet research shows that drivers who increase their deductible to $1,000 break even after they file one claim every three to four years, which makes higher deductibles profitable for safe drivers.

How Claims Work With Your Deductible

Insurance companies deduct your deductible amount from the total claim payout after they approve your claim. You either pay the repair shop directly for your deductible portion, or your insurer handles all payments after you settle your deductible with them. Each claim you file under comprehensive or collision coverage requires you to meet your deductible again (there’s no annual limit like health insurance). Your choice of deductible amount directly affects both your monthly costs and your financial exposure when accidents occur.

What Makes the Right Deductible Choice

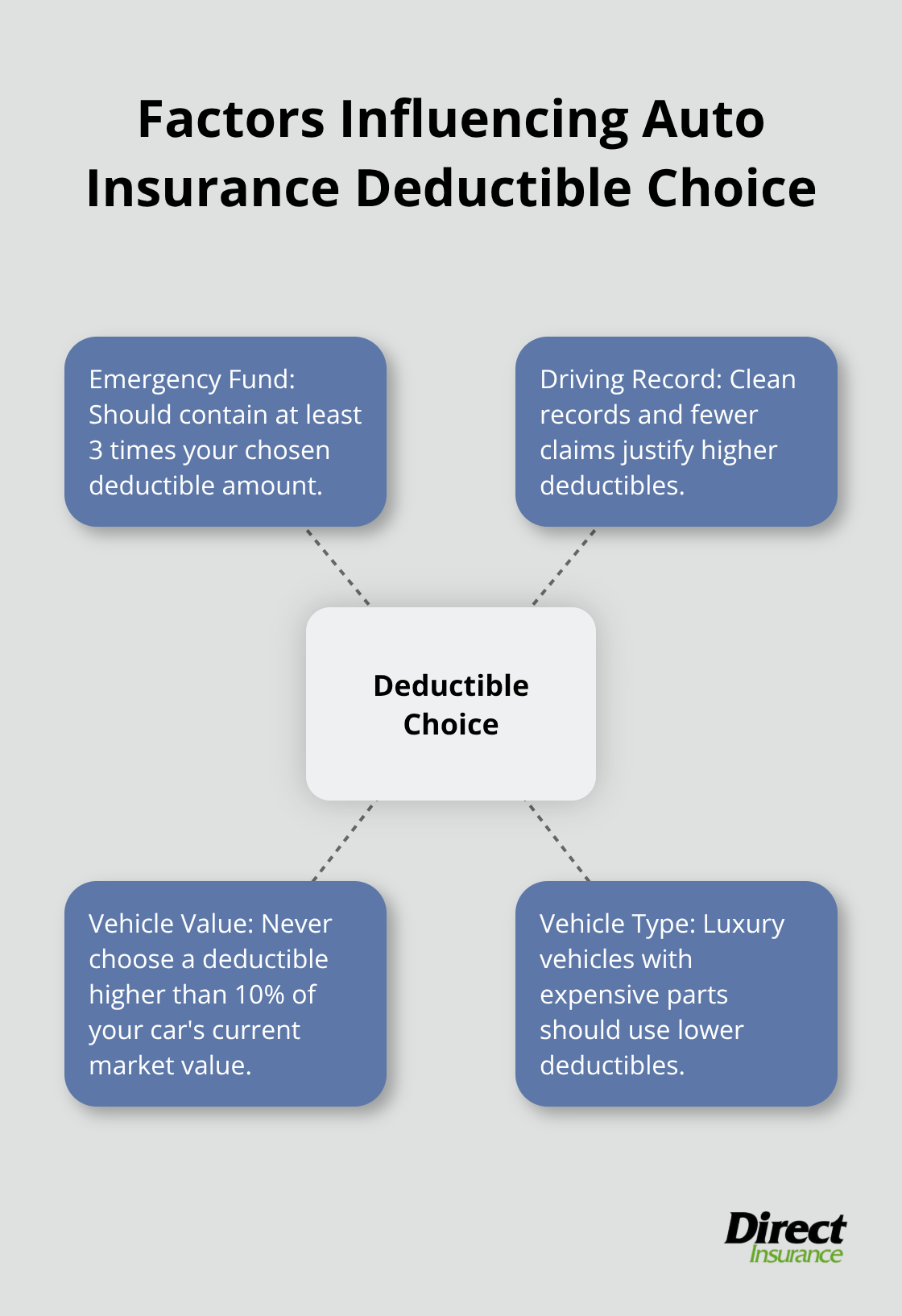

Your emergency fund should contain at least three times your chosen deductible amount before you consider anything above $500. The National Association of Insurance Commissioners found that 29% of Americans cannot cover a $400 emergency expense, which means these drivers should stick with $250 or $500 deductibles regardless of premium savings. Financial advisors recommend you keep your deductible at an amount you can pay immediately without borrowing money or using credit cards. If you have $3,000 in emergency savings, a $1,000 deductible becomes reasonable, but anything higher puts you at financial risk.

Your Driving Record Determines Your Risk Level

Drivers with clean records who haven’t filed a claim in five years should choose higher deductibles because they statistically won’t need them. Insurance Research Council data shows that drivers over 50 with no recent violations file 60% fewer claims than younger drivers with tickets. If you’ve had two or more at-fault accidents in three years, select the lowest deductible available because you’re likely to file future claims. Urban drivers face higher accident rates than rural drivers (city dwellers experience 2.3 times more fender-benders according to Highway Loss Data Institute research).

Vehicle Value Changes Everything

Never choose a deductible higher than 10% of your car’s current market value because you’ll lose money on total loss claims. A 2015 Honda Civic worth $12,000 shouldn’t have a deductible above $1,200, while a 2023 BMW worth $45,000 can handle a $2,000 deductible without problems. Cars older than eight years depreciate rapidly, which makes high deductibles counterproductive when repair costs approach the vehicle’s actual cash value.

Luxury vs Economy Vehicle Considerations

Luxury vehicles with expensive parts should use lower deductibles because even minor repairs often exceed $2,000. Basic economy cars can justify higher deductibles due to affordable replacement parts and lower repair costs. Mercedes-Benz and BMW owners typically pay 40% more for parts than Honda or Toyota owners (according to automotive repair industry data). This cost difference affects how you should structure your deductible choice based on your specific vehicle make and model.

The most common deductible amounts range from $100 to $2,000, and each option creates different financial scenarios that you need to understand before making your final decision.

What Do Different Deductible Amounts Actually Cost?

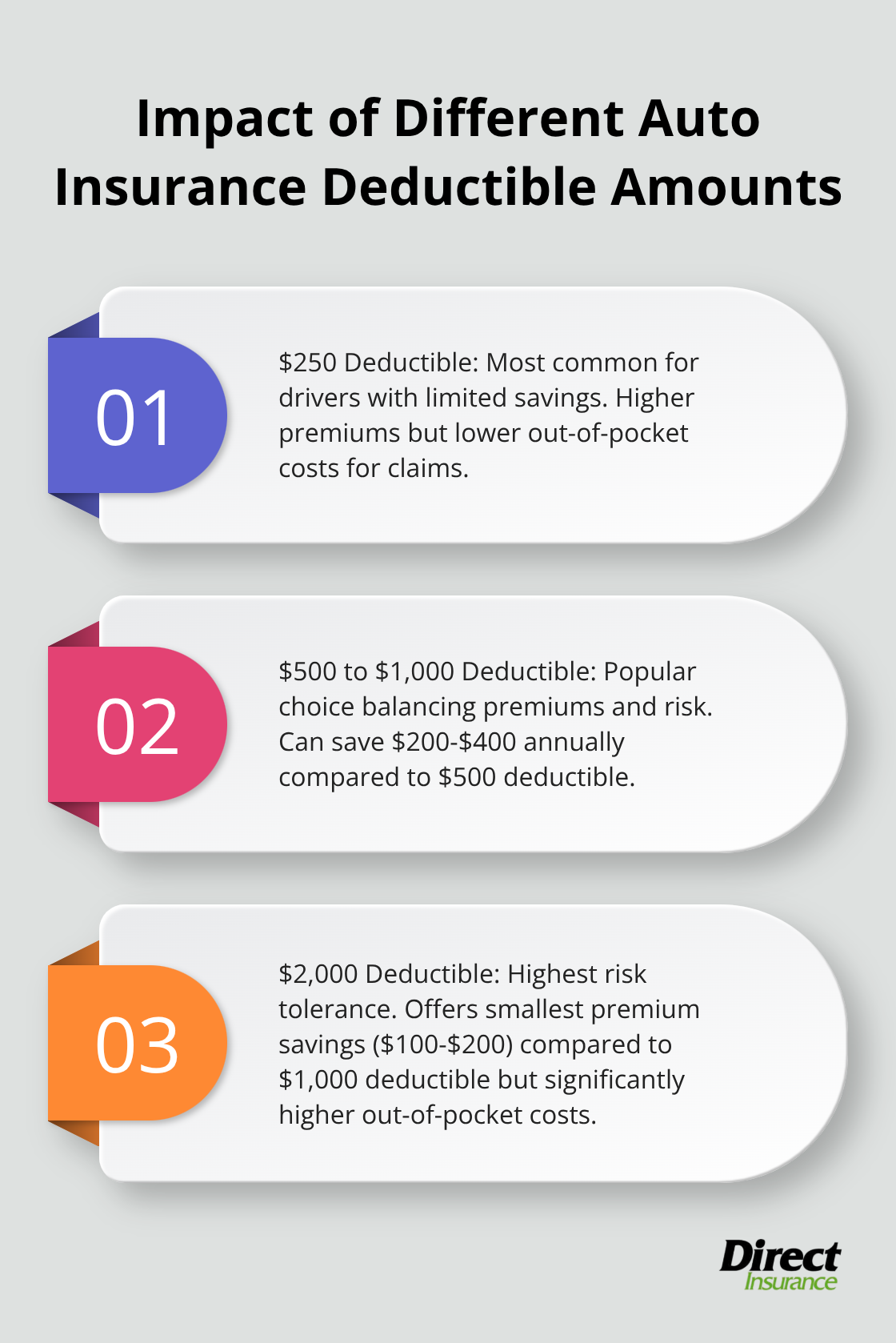

Most insurers offer standard deductible amounts of $250, $500, $1,000, and $2,000, with $500 being the most popular choice among drivers nationwide. The Insurance Information Institute reports that drivers who switch from a $250 to $1,000 deductible can reduce their collision and comprehensive premiums by up to 40% annually. A driver who pays $800 per year for full coverage could save $320 annually with this change, but would pay $750 more out-of-pocket when they file a claim.

Premium Savings Break Down by Amount

When you raise your deductible from $500 to $1,000, you typically save $200 to $400 per year (depending on your location and record). The jump from $1,000 to $2,000 produces smaller savings of $100 to $200 annually because insurers view both amounts as high-risk tolerance levels. Progressive data shows that drivers who choose a higher deductible save an average of $600 annually compared to $250 deductibles, but this choice only makes financial sense if you avoid claims for more than three years.

Urban vs Rural Driver Differences

Rural drivers in low-traffic areas benefit most from high deductibles because they experience crash deaths at a rate of 1.65 per 100 million miles traveled compared to 1.07 in urban areas according to 2023 data. City drivers face more fender-benders and parking lot incidents, which makes lower deductibles more practical despite higher premiums. The frequency of minor claims in urban areas often outweighs the premium savings from higher deductibles.

Real Cost Scenarios Show the Truth

A driver with a $250 deductible who files one claim every two years pays $400 more in premiums annually but only $250 per claim, which creates a net loss of $150 yearly compared to a $1,000 deductible option. Accident-prone drivers who file claims annually should choose $250 deductibles because they’ll pay $750 less per incident despite higher premiums. The math changes completely for luxury vehicle owners where repair costs often exceed $5,000, which makes the difference between a $500 and $2,000 deductible relatively small compared to total claim amounts.

Final Thoughts

You must balance your monthly budget against potential out-of-pocket costs when you decide what deductible for auto insurance works best. The optimal choice exists where your premium savings justify the financial risk you accept. Drivers with strong emergency funds and clean records benefit from higher deductibles, while those with limited savings or frequent claims need lower amounts.

You should review your deductible annually when your policy renews, especially after major life changes like job loss, salary increases, or vehicle purchases. Your financial situation and risk tolerance change over time, which means your optimal deductible amount shifts too. Market conditions and insurance rates fluctuate, which creates opportunities to adjust your coverage for better value.

We at Direct Insurance Services help you find deductible options that match your specific circumstances and budget constraints (through our independent agency network). Our approach means we compare rates across different insurers to identify the best combination of premium costs and deductible amounts for your situation. Professional guidance helps you avoid costly mistakes when you select coverage that protects both your vehicle and your financial stability.