Most renters assume their landlord’s insurance covers their belongings. It doesn’t-and that gap leaves your possessions completely unprotected if theft, fire, or water damage strikes.

At Direct Insurance Services, we’ve seen renters lose thousands of dollars because they skipped this affordable protection. Home insurance for renters typically costs $15–30 monthly and covers your personal property, liability claims, and temporary housing if you’re displaced.

This guide walks you through what renters insurance actually covers and how to find a policy that fits your budget and needs.

What Renters Insurance Actually Protects

Personal Property Coverage Shields Your Belongings

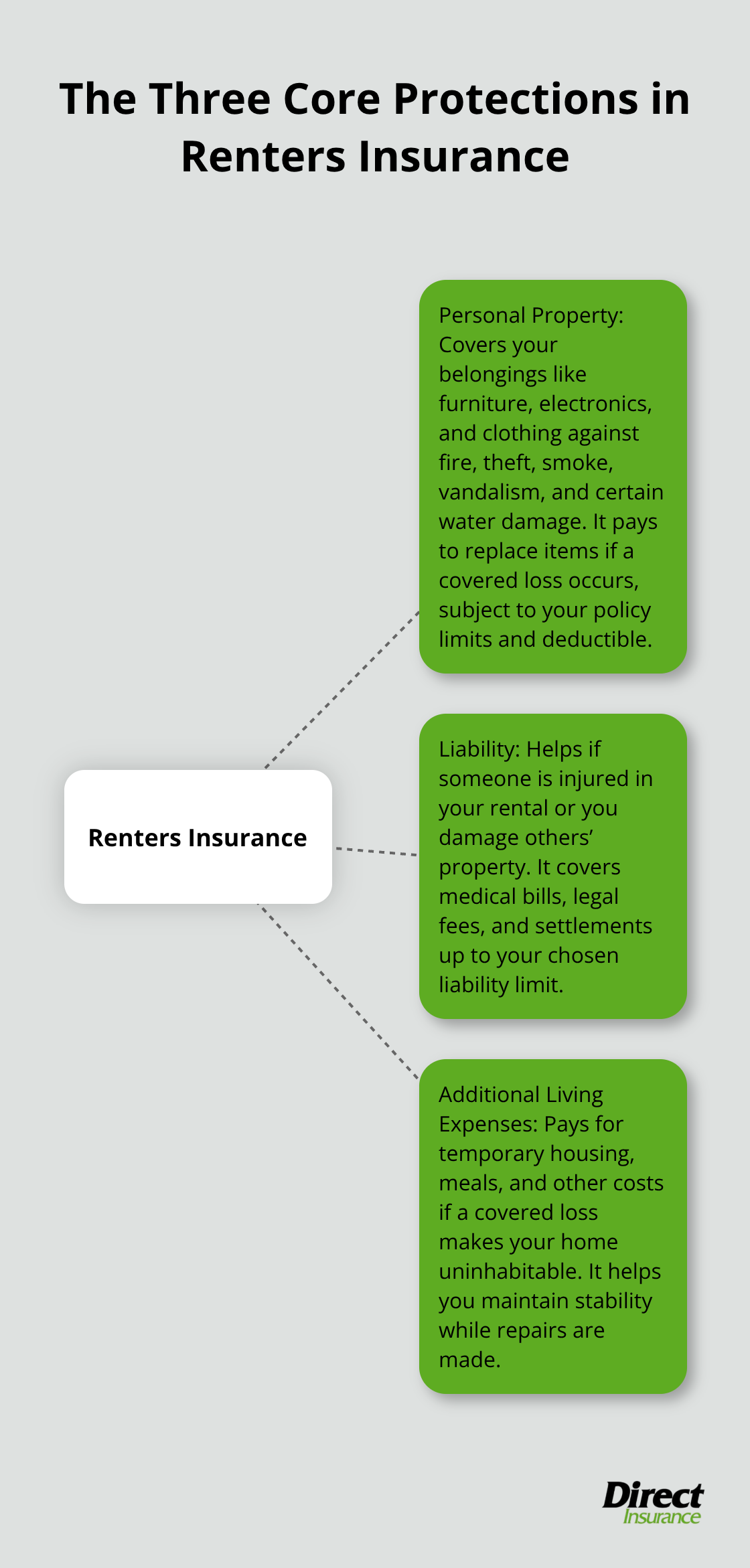

Renters insurance covers three distinct areas that directly impact your financial security as a tenant. Your personal belongings-furniture, electronics, clothing, and everything you own inside the rental-receive protection against fire, theft, smoke, vandalism, and certain water damage. According to the Insurance Information Institute, about one-third of renters face the risk of theft, property damage, or liability claims, making this coverage far from optional. If a kitchen fire destroys your laptop, couch, and wardrobe, renters insurance pays to replace those items. The Texas Department of Insurance notes that a typical policy costs around $20 monthly in Texas, with national averages between $15 and $30 per month depending on location and coverage limits. This affordability matters because most renters skip coverage entirely, assuming their landlord’s policy will protect them-a dangerous mistake that leaves thousands of dollars in personal property unprotected.

Liability Coverage Protects You from Financial Disaster

The second protection is liability coverage, which handles the financial fallout when someone gets injured at your rental or you accidentally damage someone else’s property. Standard policies include about $100,000 in personal liability coverage, though you can increase this to $300,000 or more if you have significant assets to protect. If a guest slips on your floor and requires surgery, or you accidentally flood your neighbor’s apartment, liability coverage pays their medical bills and legal fees. Medical payments coverage, typically $1,000–$5,000, covers minor injuries to guests without requiring you to prove fault. This distinction matters: liability coverage protects you from lawsuits, while medical payments coverage handles smaller injury costs immediately.

Additional Living Expenses Cover Temporary Displacement

The third component is additional living expenses-also called loss of use coverage-which reimburses temporary housing, meals, and other costs if a covered loss makes your rental uninhabitable. If a fire forces you to stay in a hotel for two months while repairs happen, this coverage covers those extra costs. The National Association of Insurance Commissioners confirms that renters policies include these three core protections, yet most tenants remain unaware of how much financial security they provide.

Understanding what you actually buy prevents costly gaps in protection and ensures you select appropriate coverage limits for your situation.

Understanding Your Coverage Limits and What Falls Outside

Personal Property Coverage Has Hidden Limits

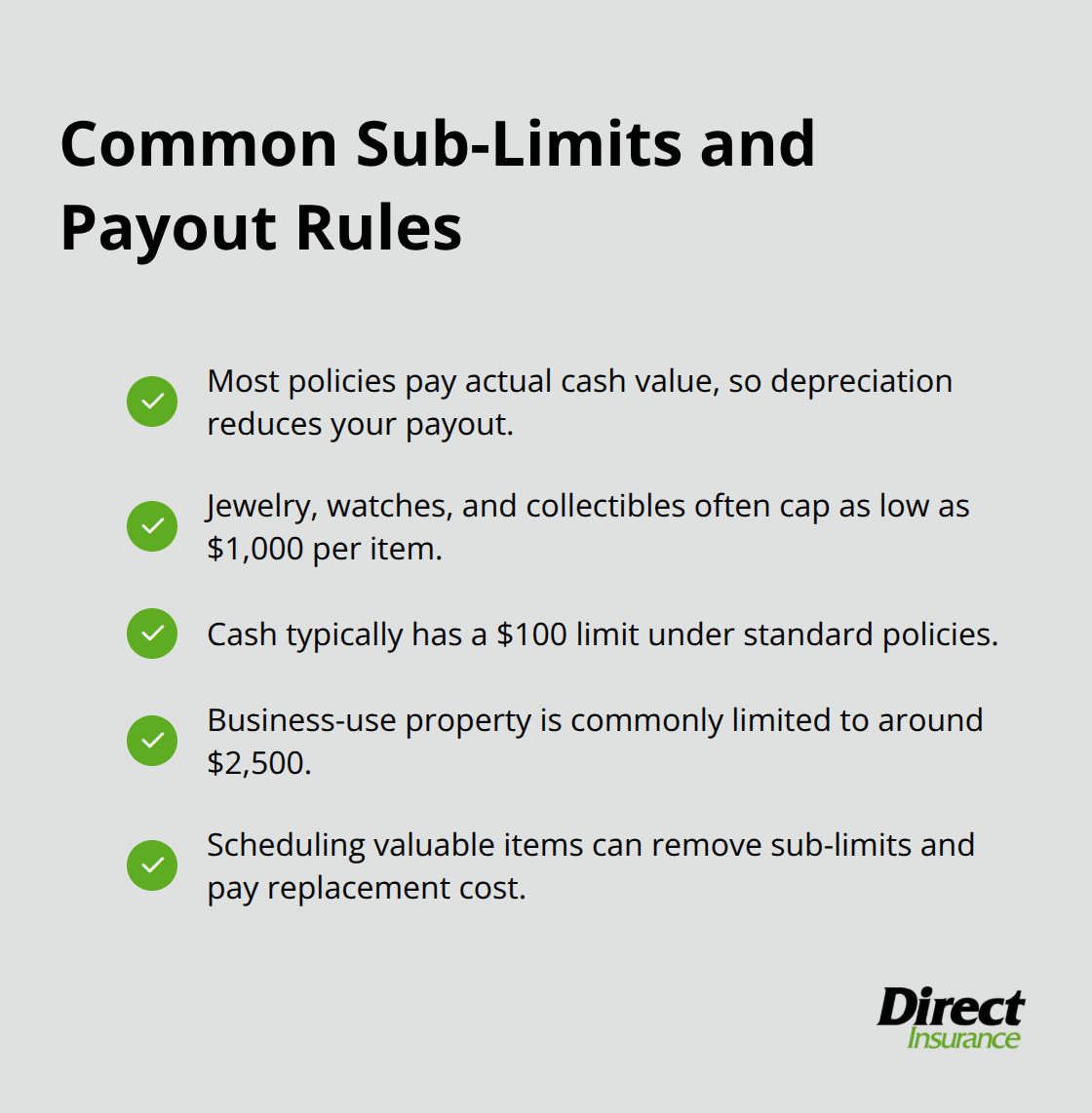

Personal property coverage sounds straightforward until you start filing a claim and discover sub-limits that cap protection for specific items. Standard renters policies typically cover your belongings at actual cash value, meaning depreciation reduces what you receive. A five-year-old laptop worth $800 new might only pay $300 at actual cash value. The Texas Department of Insurance warns that jewelry, watches, and collectibles often hit sub-limits as low as $1,000 per item. Cash has a notorious $100 cap, and business-use items max out around $2,500.

If you own expensive items, you need a scheduled personal property endorsement that lists valuables individually with their replacement cost. This endorsement eliminates depreciation and sub-limits entirely. High-value items like cameras, art, or musical instruments deserve this protection because standard policies leave them dramatically underinsured.

Create an Inventory Before You Need It

A detailed home inventory with photos, receipts, and serial numbers stored in cloud storage accelerates claims and prevents disputes over item values. This single step matters more than most renters realize. The Insurance Information Institute emphasizes that most renters wait until after a loss to discover coverage gaps, which is far too late. You’ll want to update your inventory every six months as you acquire new belongings or replace old ones.

Evaluate Liability and Loss-of-Use Coverage Separately

Liability coverage and loss-of-use coverage protect against different financial threats, so you need different evaluation strategies for each. Liability coverage starting at $100,000 sounds adequate until you consider that a single serious injury lawsuit can exceed that amount, especially if permanent disability results. Medical payments coverage, typically $1,000–$5,000, handles minor injuries immediately without requiring fault determination, but it covers only guests, not you.

Loss-of-use coverage reimburses actual temporary housing and meal costs if a fire or other covered loss displaces you. This coverage only applies if your personal property loss is also covered under the policy. The National Association of Insurance Commissioners notes that loss-of-use limits vary widely, so confirm your specific limit before you sign.

Deductibles and Exclusions Shape Your Real Protection

Your deductible choice directly impacts both your monthly premium and your out-of-pocket costs when you file a claim. A $500 deductible saves premium money monthly but means you’ll pay that amount out-of-pocket before coverage begins. The National Association of Insurance Commissioners notes that choosing a higher deductible can significantly reduce annual premiums, making coverage more affordable if you have emergency savings to cover the deductible.

Standard exclusions in renters policies include floods, earthquakes, mold, pest damage, and wear-and-tear. You must understand what your policy explicitly does not cover before signing. Floods require separate National Flood Insurance Program coverage, and earthquakes need dedicated earthquake policies or riders in most states. These gaps matter most in high-risk areas where the excluded perils actually threaten your rental.

Understanding these limits and exclusions prevents costly surprises when you need your policy most. The next step involves comparing actual quotes from multiple insurers to see how coverage limits, deductibles, and exclusions vary in price and protection.

Picking the Right Policy Without Overpaying

Calculate What You Actually Own

Start by calculating what you actually own, not what you think you own. Walk through your apartment or rental house room by room and list items with approximate replacement costs. Your furniture, electronics, clothing, kitchen items, and everything else adds up faster than expected. Most renters underestimate their belongings because they forget about the small items that accumulate over years.

Take photos of each room and store them in cloud storage alongside your list. This inventory becomes your foundation for determining whether a $30,000 or $50,000 personal property limit makes sense for your situation. If you own expensive jewelry, cameras, art, or musical instruments, add those separately with their replacement costs noted. Calculate what you actually own by taking the item’s replacement cost and subtracting depreciation based on its age, condition, and wear and tear. Understanding your actual exposure helps you make better coverage decisions instead of guessing.

Compare Quotes from Multiple Carriers

Once you know what you’re protecting, get quotes from at least three different insurers to see how dramatically prices vary for identical coverage. A $50,000 personal property limit with a $500 deductible might cost $18 monthly from one carrier and $26 from another-that’s a $96 annual difference on the same protection. The National Association of Insurance Commissioners notes that location, building age, and safety features like smoke alarms or deadbolts heavily influence pricing, so comparing quotes from your specific rental address matters more than national averages.

When you compare, hold the coverage limits and deductible constant across quotes so you’re actually comparing apples to apples. Pay special attention to how each insurer handles claims-check their complaint ratios and customer reviews on independent sites rather than trusting marketing claims. A $2 monthly savings means nothing if the insurer denies your claim or takes six months to process it.

Select a Deductible You Can Actually Afford

Your deductible choice directly affects both your premium and your claim experience. A $250 deductible costs less monthly but requires you to pay that amount out-of-pocket before coverage begins, while a $1,000 deductible significantly reduces your monthly payment if you have emergency savings to cover it. The Insurance Information Institute confirms that choosing a higher deductible is the most effective way to lower premiums without reducing coverage limits, but only select a deductible you can actually afford to pay.

Review Exclusions and Coverage Gaps

Finally, review the specific exclusions in each quote-floods, earthquakes, and mold vary by policy, and understanding these gaps prevents nasty surprises when you file a claim. Some renters in flood-prone areas need National Flood Insurance Program coverage alongside their standard renters policy, which requires separate shopping and typically carries a 30-day waiting period before protection begins. These exclusions matter most in high-risk locations where the excluded perils actually threaten your rental.

Final Thoughts

Renters insurance protects your personal belongings against fire, theft, and water damage while shielding you from liability claims and covering temporary housing costs if a covered loss displaces you. The math works in your favor-home insurance for renters costs $15–30 monthly while protecting thousands of dollars in possessions and preventing financial devastation from liability claims. Most renters skip this protection because they mistakenly believe their landlord’s policy covers their belongings, a dangerous assumption that leaves them completely exposed.

Calculate what you actually own, then obtain quotes from at least three carriers to compare how prices vary for identical coverage. Pay attention to deductible options, coverage limits for high-value items, and specific exclusions like floods or earthquakes that might affect your rental location. Review each insurer’s complaint history and claims-handling reputation rather than selecting based on price alone-a $5 monthly savings disappears instantly if your claim gets denied or delayed.

We at Direct Insurance Services work with top-rated carriers to help you find coverage that matches your belongings, liability exposure, and budget without unnecessary add-ons or gaps. Our team provides personalized guidance that puts your needs first, not pressure to buy more than you need. Contact Direct Insurance Services to discuss how renters insurance fits into your overall protection plan and get a quote that reflects your actual situation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation