Can You Get Auto Insurance Without a Drivers License?

Getting auto insurance without a driver’s license might sound impossible, but it’s actually more common than you think. Many people face situations where they need coverage before obtaining their license or while their driving privileges are suspended.

At Direct Insurance Services, we help clients navigate these complex scenarios every day. Several legitimate options exist for securing coverage even when you can’t legally drive.

Are Insurance and License Requirements the Same?

Insurance mandates and driver’s license requirements operate under completely separate legal frameworks across all 50 states. Every state except New Hampshire requires vehicle owners to carry minimum liability insurance, while driver’s license requirements apply only to people who actually operate vehicles on public roads. This separation creates opportunities for unlicensed individuals to obtain coverage legally.

State Insurance Laws Override License Status

Most states require insurance coverage based on vehicle ownership, not the ability to drive. California mandates minimum liability coverage of $15,000 per person for bodily injury, regardless of the owner’s license status. Texas requires $30,000 per person in liability coverage for all vehicles that have registration. These laws focus on protection for other drivers and property, not validation of who can drive.

Vehicle registration systems in 48 states allow unlicensed owners to register cars with proper insurance documentation. The state treats insurance as a financial responsibility requirement separate from the privilege to drive.

License Requirements Target Road Safety

Driver’s license laws address competency and safety standards for road operation. States like Florida require vision tests, written exams, and road skills demonstrations before they issue licenses. However, these requirements don’t affect insurance eligibility in any way.

The Insurance Information Institute reports that 15.4 percent of drivers nationwide lack proper insurance coverage (this statistic includes both licensed and unlicensed individuals). License status has no direct correlation with insurance availability or requirements.

Different Enforcement Creates Coverage Gaps

Law enforcement handles license violations and insurance violations through separate processes. Police can issue citations for operation without a license independently from insurance status checks. Courts may require SR-22 filings for license reinstatement, which actually mandates insurance coverage for unlicensed drivers who seek to restore their privileges.

This enforcement separation allows unlicensed vehicle owners to maintain legal compliance through insurance alone. The next consideration involves specific situations where people commonly need insurance coverage without holding a valid license.

When Do You Need Insurance Without a License

Three distinct scenarios create legitimate needs for auto insurance coverage without a valid driver’s license, and each situation requires a different approach to secure proper protection.

Vehicle Purchase Before License Completion

Young adults frequently buy their first car months before they complete driver education requirements or pass road tests. The National Highway Traffic Safety Administration reports that 16-year-olds represent the highest crash risk group, which prompts many families to secure vehicles early while teens complete supervised hours behind the wheel.

Most auto lenders require full coverage insurance before they approve loans, regardless of the buyer’s license status. Credit unions like Navy Federal allow unlicensed buyers to finance vehicles with proof of insurance and a co-signer who holds a valid license. The most effective strategy involves listing a licensed family member as the primary driver while adding the unlicensed owner as a named insured on the policy.

Vehicle Storage and Seasonal Use Cases

Classic car collectors, military personnel who face deployment, and seasonal residents often own vehicles they cannot currently operate. Comprehensive coverage protects stored vehicles from theft, vandalism, and weather damage even when parked long-term.

The Insurance Information Institute data shows that comprehensive claims cost an average of $2,306 per incident, which makes coverage worthwhile for valuable vehicles. Storage facilities frequently require proof of insurance before they accept vehicles (this creates mandatory coverage needs for unlicensed owners).

License Suspension Situations

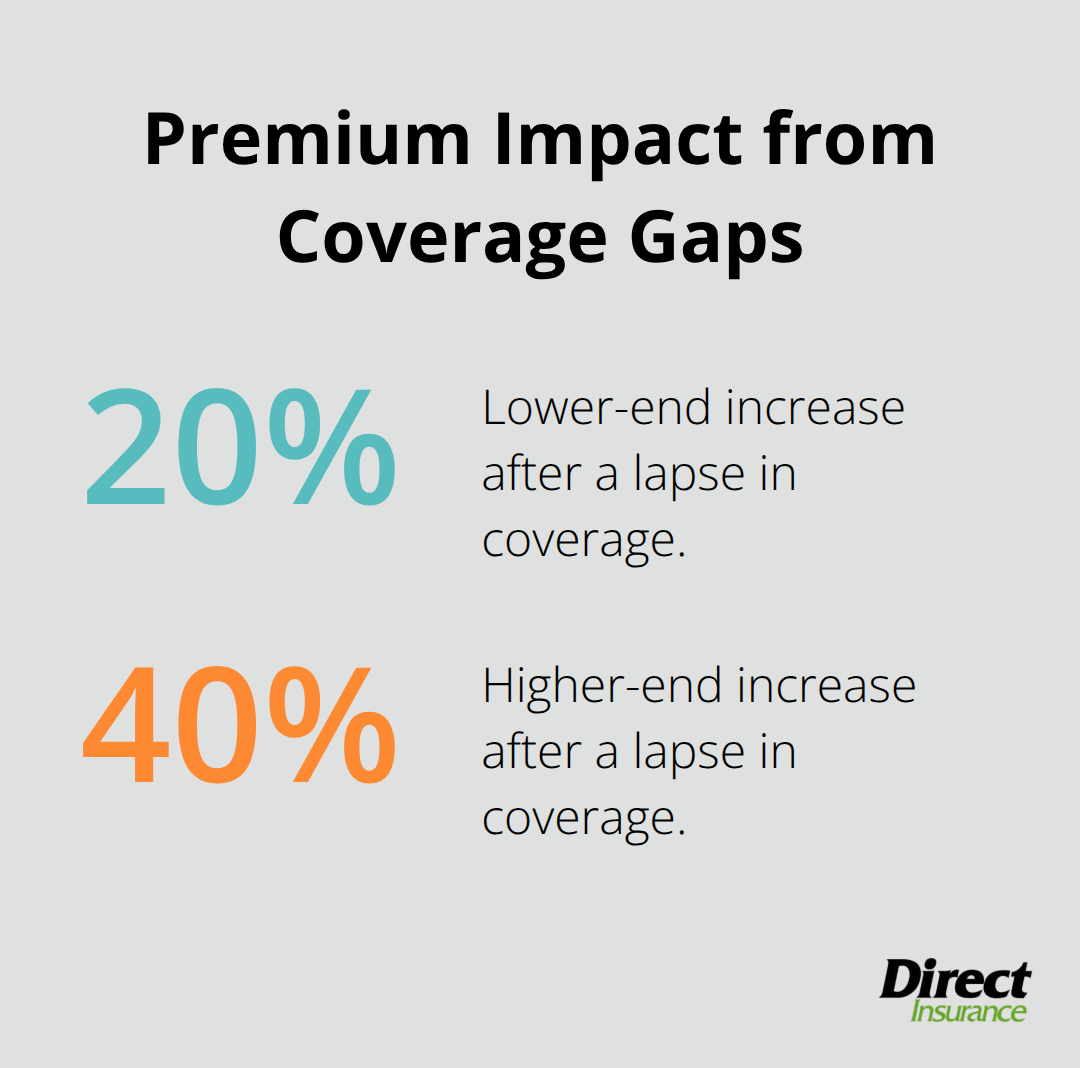

Suspended license holders must maintain continuous coverage to avoid gaps that increase future premiums by 20 to 40 percent according to industry data. Courts often require SR-22 filings for license reinstatement, which actually mandates insurance coverage for unlicensed drivers who seek to restore their privileges.

The smartest approach involves purchasing parked car policies that eliminate liability coverage while they maintain comprehensive and collision protection for the stored vehicle. These specialized policies cost significantly less than full coverage but still satisfy legal requirements for vehicle ownership.

Understanding these common scenarios helps identify the right coverage approach, but the next step involves exploring specific insurance options available to unlicensed drivers.

What Insurance Options Work for Unlicensed Drivers

Three practical strategies provide reliable coverage for unlicensed drivers, but success depends on the right approach for your specific situation. Independent agents consistently deliver the best results because they access multiple carriers and understand which companies accept unlicensed applicants.

Add Yourself to a Licensed Driver’s Policy

The most effective strategy involves addition to a family member’s existing auto insurance policy as a named insured while they serve as the primary driver. State Farm and Allstate regularly approve these arrangements when the licensed driver uses the vehicle most frequently.

This approach reduces premiums compared to standalone policies because insurers view shared family policies as lower risk. Progressive requires the primary driver to live at the same address as the unlicensed owner, while Geico allows different addresses within the same state. The licensed driver’s record directly impacts your rates, so choose someone with a clean history to minimize costs.

Secure Parked Car Coverage for Stored Vehicles

Parked car policies eliminate liability coverage while they maintain comprehensive and collision protection for vehicles that stay off public roads. These specialized policies cost significantly less than full coverage because they remove the highest-risk component from your premium calculation.

Farmers Insurance offers comprehensive-only policies for vehicles that remain parked. The coverage protects against theft, vandalism, fire, and weather damage while the vehicle remains parked (most insurers require proof that the vehicle stays in a secure location like a garage or storage facility). This option works perfectly for classic cars, seasonal vehicles, or cars owned during license suspension periods.

Work with Independent Agents for Specialized Coverage

Independent insurance agents maintain relationships with specialty carriers that standard companies often overlook. These agents know which insurers accept unlicensed drivers and can secure coverage when direct applications fail.

Independent agents typically increase approval rates compared to online applications because they present cases directly to underwriters. They also identify regional carriers that major companies miss, often with lower premiums as a result. The agent handles all paperwork and communicates directly with insurance companies, which saves time and reduces application errors that lead to denials.

Final Thoughts

Auto insurance without a driver’s license requires you to understand your state’s specific requirements and choose the right coverage strategy. You can join a licensed family member’s policy as a named insured, secure parked car coverage for stored vehicles, or work with independent agents who specialize in these situations. State laws separate insurance requirements from license requirements, which creates legitimate opportunities for unlicensed vehicle owners to obtain coverage.

Whether you buy your first car before you complete driver education, store a classic vehicle, or maintain coverage during license suspension, proper insurance protects your investment and keeps you compliant with state laws. Independent insurance agents consistently deliver the best results because they understand which carriers accept unlicensed applicants and can navigate complex underwriting requirements. These professionals know how to present your case effectively to underwriters who might otherwise reject direct applications.

At Direct Insurance Services, we work with top-rated carriers to help Utah residents find tailored auto insurance solutions that fit their unique situations (including scenarios where you need coverage without a valid license). Success depends on working with experienced professionals who understand these specialized coverage needs. The right agent can match you with the appropriate carrier for your specific circumstances and help you secure the protection you need.