Is Renters Insurance Required by Landlords?

Can a landlord make you get renters insurance? The answer varies by state and lease terms, but most landlords can legally require tenants to carry coverage.

We at Direct Insurance Services see this question frequently from both renters and property owners. Understanding these requirements protects everyone involved and prevents costly disputes down the road.

What Can Landlords Legally Require?

State Laws Set the Framework

No state law mandates renters insurance, but landlords possess broad authority to include coverage requirements in lease agreements. The RentRedi and BiggerPockets study reveals that many landlords still fail to capitalize on this legal right, with approximately 50% not verifying coverage and less than 50% including requirements in leases. This represents a missed opportunity, as tenant screening becomes more effective when insurance demonstrates financial responsibility and preparedness.

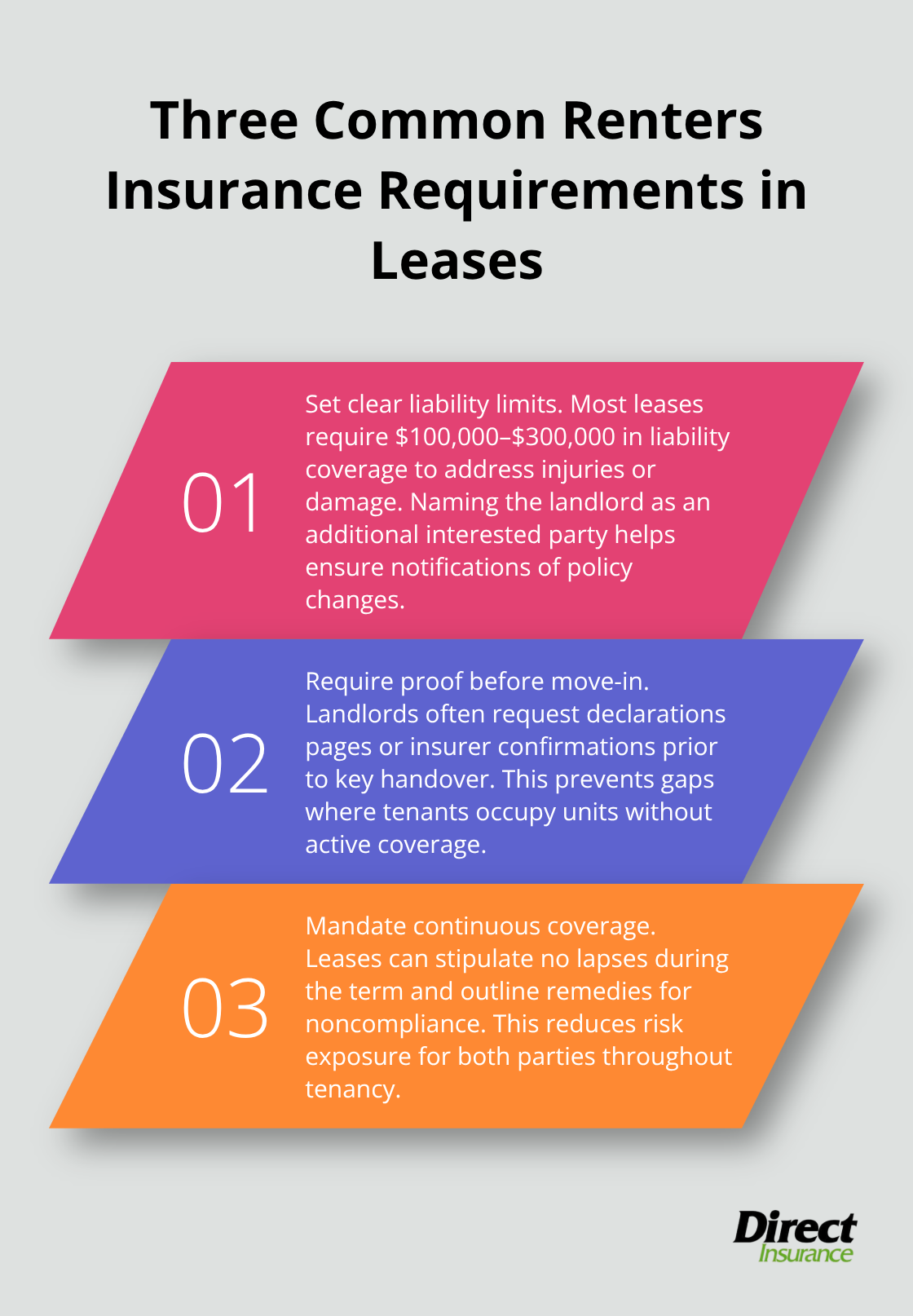

Standard Lease Requirements

Property owners typically require liability coverage between $100,000 and $300,000, with the landlord named as an additional interested party on the policy. Smart landlords specify minimum coverage amounts, require proof of active policies before move-in, and mandate continuous coverage throughout the lease term.

The Insurance Information Institute reports that only 48.2% of renters carry coverage voluntarily, which makes lease requirements the primary driver for tenant compliance.

Enforcement Varies by Portfolio Size

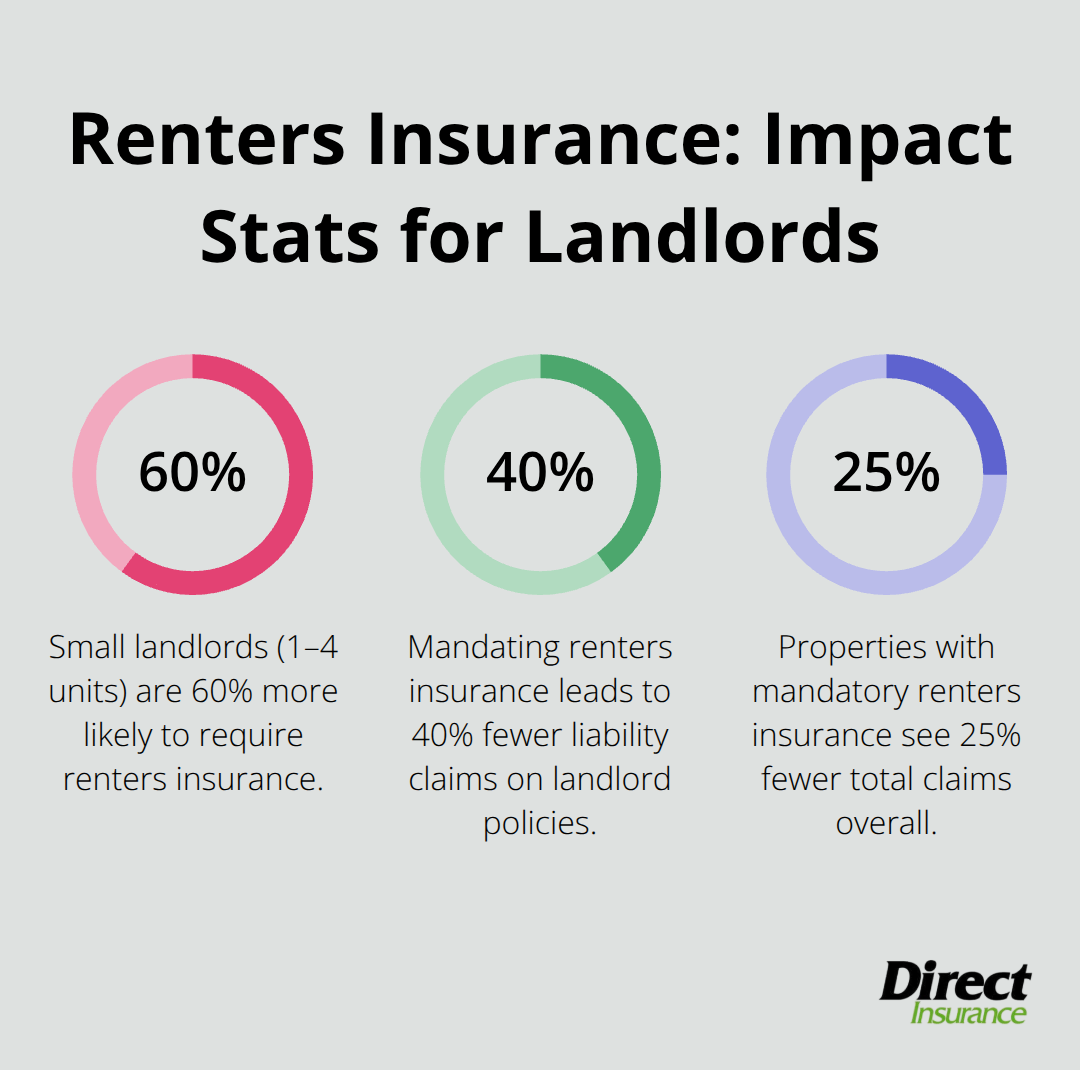

Smaller landlords who own 1-4 units are 60% more likely to require renters insurance compared to larger property owners. This trend reflects the personal investment smaller landlords have in their properties and their direct relationship with tenants. Larger portfolios often lack systematic enforcement and miss opportunities to reduce liability exposure through comprehensive tenant requirements.

Technology Solutions Bridge the Gap

Property management software now automates renters insurance verification (eliminating manual tracking headaches). Many landlords utilize these tools to streamline the process, though less than half take full advantage of available technology. The survey data shows that landlords who actively verify insurance better protect their assets and reduce potential liability claims.

These legal frameworks and enforcement patterns directly impact how landlords structure their tenant protection strategies and what coverage benefits they can expect from their requirements. Landlord insurance provides additional property protection beyond tenant requirements.

Why Renters Insurance Benefits Tenants More Than Landlords Realize

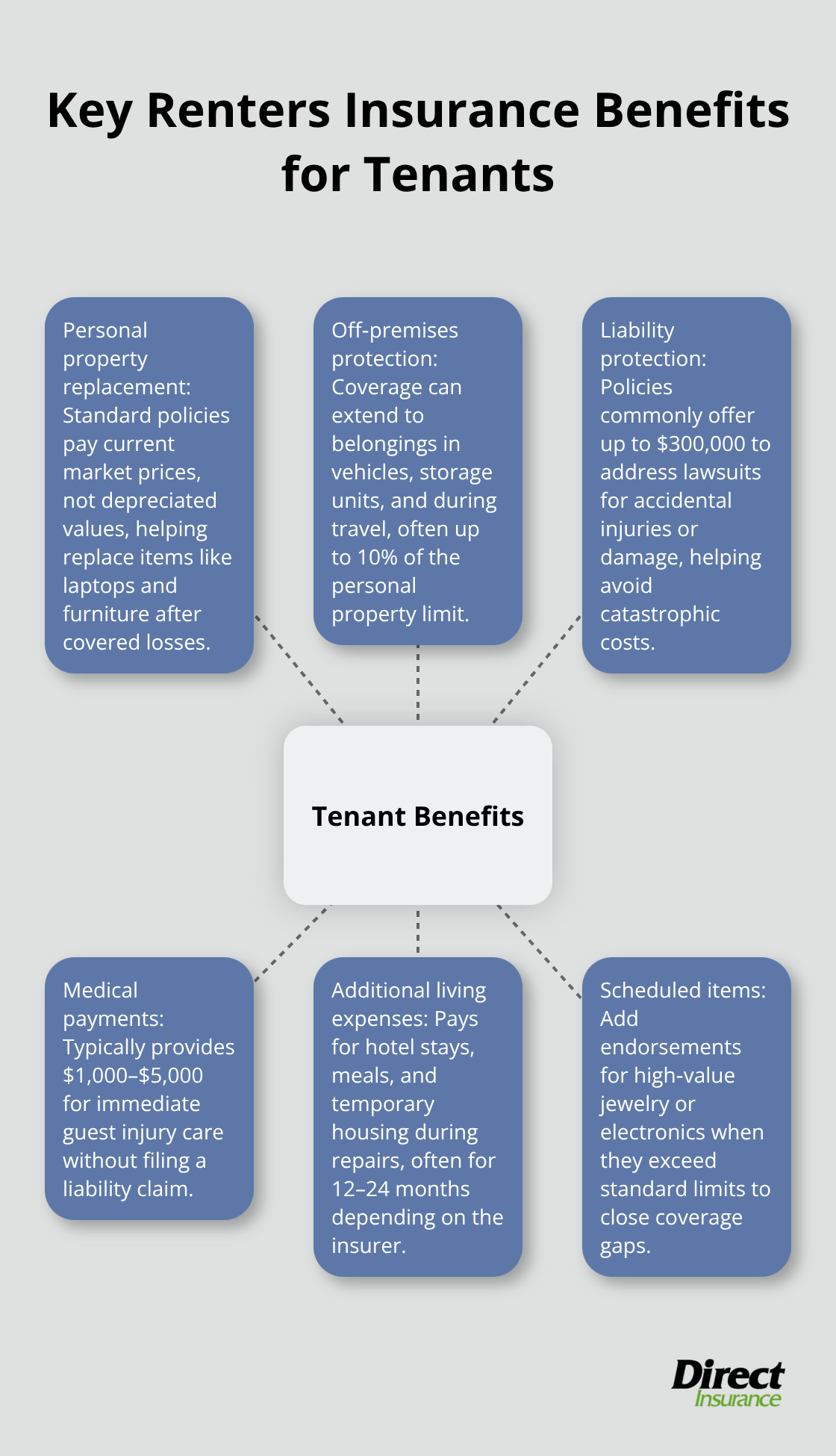

Tenants receive substantial financial protection through renters insurance that extends far beyond basic property coverage. Personal belongings receive replacement cost protection that averages $20,000 to $40,000 per policy, which covers electronics, furniture, clothing, and appliances damaged by fire, theft, or water damage. The National Association of Insurance Commissioners data shows liability coverage protects tenants against lawsuits up to $300,000 when guests suffer injuries in rental units, which prevents devastating financial consequences from medical bills and legal fees. Additional living expenses coverage pays for hotel stays, restaurant meals, and temporary housing when apartments become uninhabitable due to covered disasters (with most policies providing 12 months of alternative accommodation costs).

Personal Property Receives Full Replacement Value

Standard policies replace stolen or damaged items at current market prices rather than depreciated values, which means a three-year-old laptop receives full replacement funds instead of reduced compensation. Coverage extends beyond the rental unit to protect belongings in vehicles, storage units, and during travel, with most insurers covering up to 10% of total personal property limits for off-premises incidents. Tenants with valuable collections, jewelry, or electronics should add scheduled personal property endorsements for items that exceed standard coverage limits (typically $2,500 for jewelry and $5,000 for electronics per occurrence).

Liability Protection Prevents Financial Catastrophe

Medical payments coverage handles minor guest injuries without liability claims, which typically provides $1,000 to $5,000 for immediate medical expenses like emergency room visits or urgent care treatments. Personal liability coverage activates when tenants face lawsuits for accidental injuries or property damage, which includes incidents where cooking fires spread to neighboring units or water damage affects multiple apartments. Dog bite incidents represent the most expensive liability claims, with average settlements that exceed $50,000 according to Insurance Information Institute data, which makes pet liability coverage particularly valuable for animal owners.

Additional Living Expenses Cover Displacement Costs

Temporary housing benefits activate when covered perils make rental units uninhabitable, which covers hotel costs, increased food expenses, and storage fees for personal belongings. Most policies provide coverage for 12 to 24 months of additional living expenses, though some insurers limit benefits to 20% of personal property coverage amounts. These benefits prove invaluable during extended repairs from fire or water damage, when tenants face months of displacement and substantial out-of-pocket expenses.

Property owners who understand these tenant benefits can better appreciate why renters insurance requirements protect both parties and reduce overall liability exposure across their rental portfolios.

How Renters Insurance Protects Landlords

Tenant Negligence Claims Transfer to Renters Policies

Landlords face reduced liability exposure when tenants carry adequate renters insurance coverage because liability claims shift from landlord policies to tenant policies in many scenarios. Water damage from overflowing bathtubs, kitchen fires from unattended cooking, and electrical fires from overloaded circuits become the tenant’s insurance responsibility rather than the landlord’s burden.

The RentRedi study shows that landlords who require renters insurance see 40% fewer liability claims on their property policies compared to those who don’t mandate coverage. This protection proves particularly valuable for smaller landlords who own 1-4 units and maintain direct relationships with tenants, as personal injury lawsuits from guest accidents can exceed $100,000 in medical expenses and legal fees.

Property Damage Recovery Becomes Tenant Responsibility

Renters insurance policies cover tenant-caused damages that exceed security deposit amounts, which means landlords can recover full repair costs for incidents like carpet damage from pet accidents, wall damage from furniture movement, and appliance damage from misuse. Standard renters policies provide $20,000 to $40,000 in personal property coverage that extends to damage liability, though landlords should require minimum liability limits of $300,000 to handle major incidents like apartment fires that spread to neighboring units. Property owners who verify active coverage throughout lease terms protect themselves against situations where tenants cause thousands in damage but lack financial resources for repairs.

Insurance Premium Reductions Follow Risk Mitigation

Landlord insurance carriers often provide premium discounts for properties where all tenants maintain renters insurance because the risk profile improves significantly when tenant-caused damages transfer to separate policies. Some insurers reduce landlord policy premiums by 5% to 15% when comprehensive tenant insurance requirements exist (though these discounts vary by carrier and property type). The Insurance Information Institute data indicates that properties with mandatory renters insurance experience 25% fewer total claims, which creates long-term premium stability for landlords who enforce consistent coverage requirements across their rental portfolios.

Final Thoughts

Can a landlord make you get renters insurance? Most landlords possess this legal authority, yet many fail to exercise it effectively. Only 48.2% of renters carry coverage voluntarily, while approximately 50% of landlords don’t verify insurance requirements. This gap creates unnecessary risk for both parties.

Tenants benefit from comprehensive protection that averages $20,000 to $40,000 in personal property coverage, plus liability protection up to $300,000. Additional living expenses coverage provides financial support during displacement, while medical payments handle minor guest injuries without major claims. Landlords who require renters insurance see 40% fewer liability claims and potential premium reductions of 5% to 15% (with properties experiencing 25% fewer total claims overall).

We at Direct Insurance Services recommend that landlords include specific coverage requirements in lease agreements and verify active policies throughout tenancy. Tenants should secure coverage regardless of requirements, as the financial protection far exceeds the average monthly cost of $15. Direct Insurance Services helps Utah residents navigate renters insurance options with personalized service and competitive rates from top-rated carriers.