Do You Need Both Homeowners and Landlord Insurance?

Property owners often ask: “Do I need both homeowners insurance and landlord insurance?” The answer depends on how you use your property.

We at Direct Insurance Services see many clients who own multiple properties or transition between living in and renting out their homes. Understanding when dual coverage makes financial sense can save you thousands in potential losses.

What Makes These Insurance Types Different

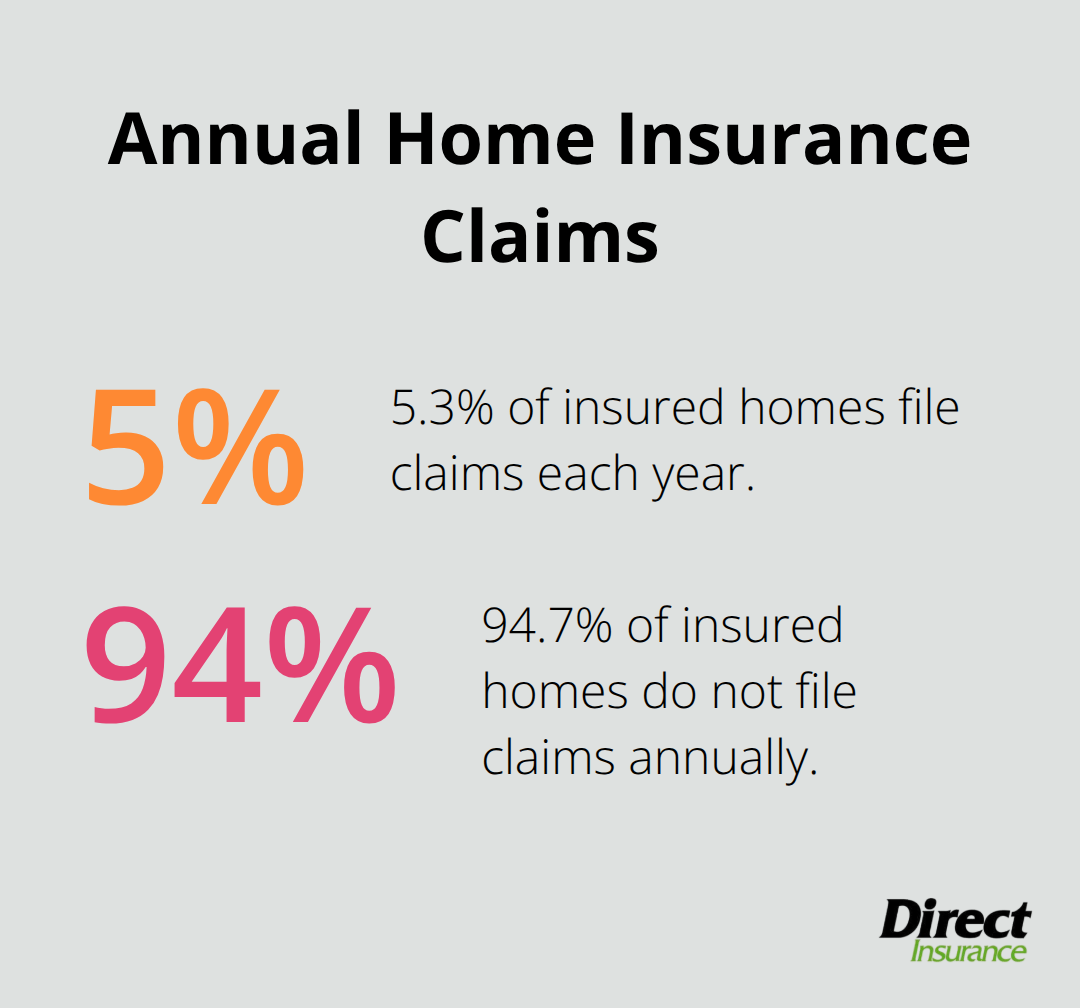

Property owners face significant financial losses when they confuse homeowners and landlord insurance, with 5.3 percent of insured homes filing claims annually. These two insurance types serve completely different purposes and protect against distinct risks.

Homeowners insurance protects owner-occupied properties where you live full-time. This coverage includes your personal belongings, liability for guest injuries, and additional expenses if you need temporary housing. The policy assumes you maintain the property regularly and control who enters your home.

The moment you rent out your property-even to family members-homeowners insurance becomes invalid. Insurance companies deny claims on rental properties covered under homeowners policies because the risk profile changes completely.

Owner-Occupied Property Protection

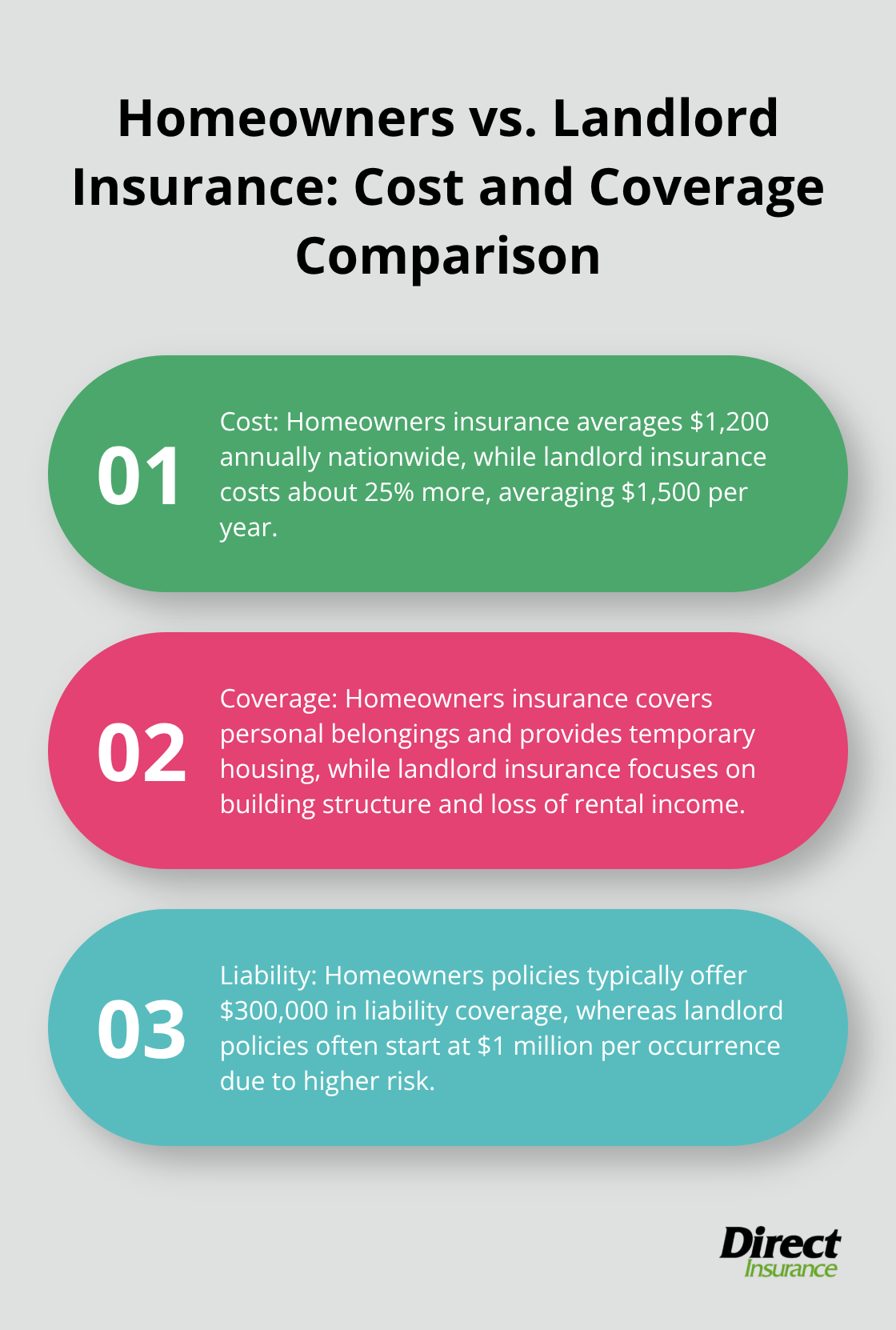

Homeowners insurance covers structural damage from fire, storms, and theft, plus your personal belongings up to policy limits. The average homeowners policy provides $300,000 in liability coverage and costs $1,200 annually nationwide.

Personal property coverage extends to furniture, electronics, and clothing. Replacement cost coverage adds roughly 10% to your premium but pays current replacement value rather than depreciated worth. Medical payments coverage handles small injuries to guests without lawsuits, typically providing $1,000 to $5,000 per incident.

Standard homeowners policies also cover additional expenses if you must live elsewhere temporarily after covered damage (like hotel costs while repairs happen).

Rental Property Requirements

Landlord insurance costs 25% more than homeowners insurance but addresses entirely different risks. This policy protects the building structure, provides liability coverage for tenant and visitor injuries, and includes loss of rental income when properties become uninhabitable.

Personal property coverage applies only to items you provide-appliances, lawn equipment, or furnished rental items. Tenant belongings require separate renters insurance that tenants must purchase themselves.

Most landlord policies exclude normal wear and tear but cover sudden damage from tenant negligence. Typical liability limits start at $1 million per occurrence, reflecting the higher lawsuit risk from rental properties.

These fundamental differences mean you cannot substitute one policy type for another. Each property type requires its specific insurance approach to avoid dangerous coverage gaps.

When You Need Both Insurance Types

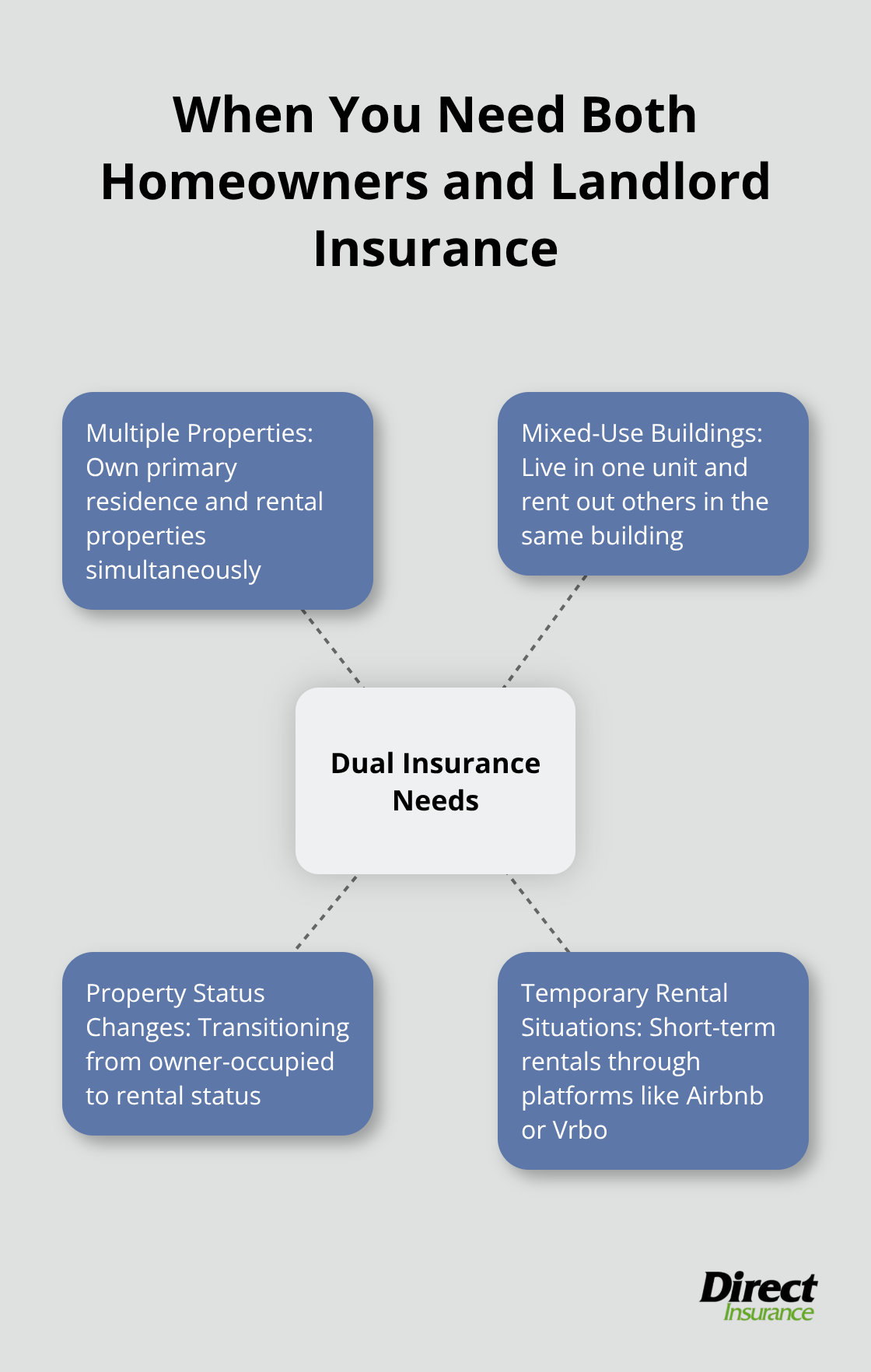

Property owners need both homeowners and landlord insurance when they own multiple properties with different occupancy statuses or operate mixed-use buildings. The National Association of Insurance Commissioners reports that 23% of property owners maintain dual policies to protect varied property uses.

You need homeowners insurance for your primary residence and landlord insurance for any rental properties you own simultaneously. This dual approach prevents coverage gaps that could cost tens of thousands in unprotected losses.

Mixed-Use and Multi-Unit Buildings

Mixed-use properties require both insurance types because different sections serve different purposes. If you live in one unit of a duplex and rent the other, you need homeowners coverage for your residence and landlord coverage for the rental unit.

The Insurance Information Institute confirms that single policies cannot adequately cover both scenarios. Multi-unit buildings where you occupy one unit follow the same rule – your unit needs homeowners insurance while rental units require landlord policies.

Property owners who ignore this distinction face claim denials when incidents occur in improperly covered areas.

Property Status Changes

Property owners must change insurance immediately when they transition from owner-occupied to rental status. Homeowners insurance becomes invalid the moment you move out and begin to rent, even if the transition takes months.

Smart property owners maintain both policies during transition periods to avoid coverage gaps. Dual coverage provides wise protection during property status changes.

Insurance companies typically allow 30-day grace periods for transitions, but they void your protection completely if you extend beyond this timeframe without proper landlord coverage.

Temporary Rental Situations

Short-term rental hosts face unique insurance challenges that standard homeowners policies don’t address. Properties rented through platforms like Airbnb or Vrbo require specialized coverage that bridges the gap between homeowners and landlord insurance.

Regular short-term hosts may need commercial insurance policies instead of standard residential coverage. The frequency of rental activity determines whether you need occasional rental endorsements or full commercial protection.

Understanding these premium differences and coverage requirements helps you make informed decisions about your insurance investment strategy.

Cost Analysis and Coverage Gaps

Landlord insurance premiums run 25% higher than homeowners policies, with the average landlord policy costing $1,500 annually compared to $1,200 for homeowners coverage. This $300 difference reflects the elevated risks that rental properties face from tenant-related damage, higher liability exposure, and increased vacancy periods.

Property location drives the biggest cost variations. Landlord policies in high-risk areas like coastal Florida can reach $4,000 annually while rural Midwest properties may cost only $800. The amount you choose for coverage, deductible level, and liability limits directly impact your premium (with $1 million liability coverage adding roughly $150 to your annual cost).

Coverage Gaps Cost More Than Premium Differences

Property owners who switch from homeowners to landlord insurance face dangerous coverage gaps that create expensive blind spots. Standard homeowners policies immediately void coverage when you start to rent, which leaves a window where you have zero protection during the transition period.

Personal property coverage drops significantly. Your homeowners policy might cover $150,000 in belongings while landlord insurance typically covers only $10,000 in landlord-owned items like appliances. Loss of use coverage changes completely too, shifting from additional expenses for you to lost rental income protection.

The biggest gap involves liability claims, as homeowners policies exclude rental-related incidents entirely. This potentially leaves you exposed to six-figure lawsuit settlements.

Premium Factors That Drive Costs

Insurance companies calculate landlord premiums based on specific risk factors that differ from homeowner calculations. Property age affects rates significantly – buildings over 30 years old face 15-20% higher premiums due to outdated electrical and plumbing systems.

Tenant demographics influence costs too. Properties in college towns or high-turnover areas command higher rates because frequent tenant changes increase damage risks. The number of units you own also matters (multi-property owners often qualify for portfolio discounts of 10-25%).

Smart Insurance Strategies

Purchase landlord insurance before your first tenant moves in, not after problems arise. Insurance companies require 30-60 days processing time for new policies, and gaps in coverage void your protection completely.

Bundle multiple rental properties with the same insurer to secure 10-15% multi-policy discounts. Maintain your homeowners policy with the same company for additional savings. Set appropriate coverage limits by calculating your property value plus one year of rental income – underinsurance saves money upfront but costs exponentially more during claims.

Review coverage annually because property values and rental rates change, which affects your insurance needs and potential savings opportunities.

Final Thoughts

The question “Do I need both homeowners insurance and landlord insurance?” has a straightforward answer: yes, when you own both your primary residence and rental properties. Each property type demands its specific coverage to protect against distinct risks and liability exposures. Property owners who attempt to save money with incorrect insurance types face devastating financial consequences.

Homeowners policies become void the moment you rent out a property, while landlord insurance cannot adequately protect your personal residence. Independent insurance agents understand the nuances between policy types and help you avoid costly coverage gaps during property transitions. They provide access to multiple carriers and create tailored solutions for complex property portfolios.

The cost difference between proper coverage and inadequate protection remains minimal compared to potential losses from uninsured claims (often reaching six figures for major incidents). We at Direct Insurance Services help property owners navigate these insurance complexities with experienced guidance. Contact us today to protect your property investments with the right insurance strategy.