How Much Auto Insurance Coverage Do You Really Need?

Choosing the right auto insurance coverage can be overwhelming. Many drivers wonder, “How much coverage do I need for auto insurance?”

At Direct Insurance Services, we understand this challenge and want to help you make an informed decision.

This guide will break down the essential types of auto insurance coverage and provide practical advice on determining the right amount for your specific situation.

What Types of Auto Insurance Coverage Do You Need?

At Direct Insurance Services, we believe that understanding the different types of auto insurance coverage will help you make informed decisions about your policy. Let’s break down the essential coverage types you should consider:

Liability Coverage: Your Financial Safety Net

Liability coverage forms the foundation of any auto insurance policy. It protects you financially if you’re at fault in an accident. This coverage splits into two parts:

- Bodily Injury Liability: This covers medical expenses, lost wages, and legal fees if you injure someone in an accident.

- Property Damage Liability: This pays for damage you cause to other people’s property, including their vehicles.

The Insurance Information Institute reports that the average auto liability claim for bodily injury was $26,501 in 2023. This fact underscores the importance of adequate liability coverage. We recommend you carry limits higher than your state’s minimum requirements to fully protect your assets.

Collision and Comprehensive: Protecting Your Vehicle

Collision coverage pays for damage to your car from accidents with other vehicles or objects. Comprehensive coverage protects against non-collision incidents like theft, vandalism, or natural disasters.

While not legally required, these coverages often become mandatory if you have a car loan or lease. Even if you own your car outright, you should consider them. The National Highway Traffic Safety Administration reports over 5 million police-reported crashes in 2020 (highlighting the real risk of vehicle damage).

Personal Injury Protection and Medical Payments

Personal Injury Protection (PIP) and Medical Payments coverage help with medical expenses after an accident, regardless of fault. PIP can also cover lost wages and other related expenses.

The necessity of these coverages varies by state. For example, PIP becomes a requirement in no-fault states, while other states may offer it as an optional coverage. We can help you understand what’s required and recommended in Utah.

Uninsured/Underinsured Motorist Coverage

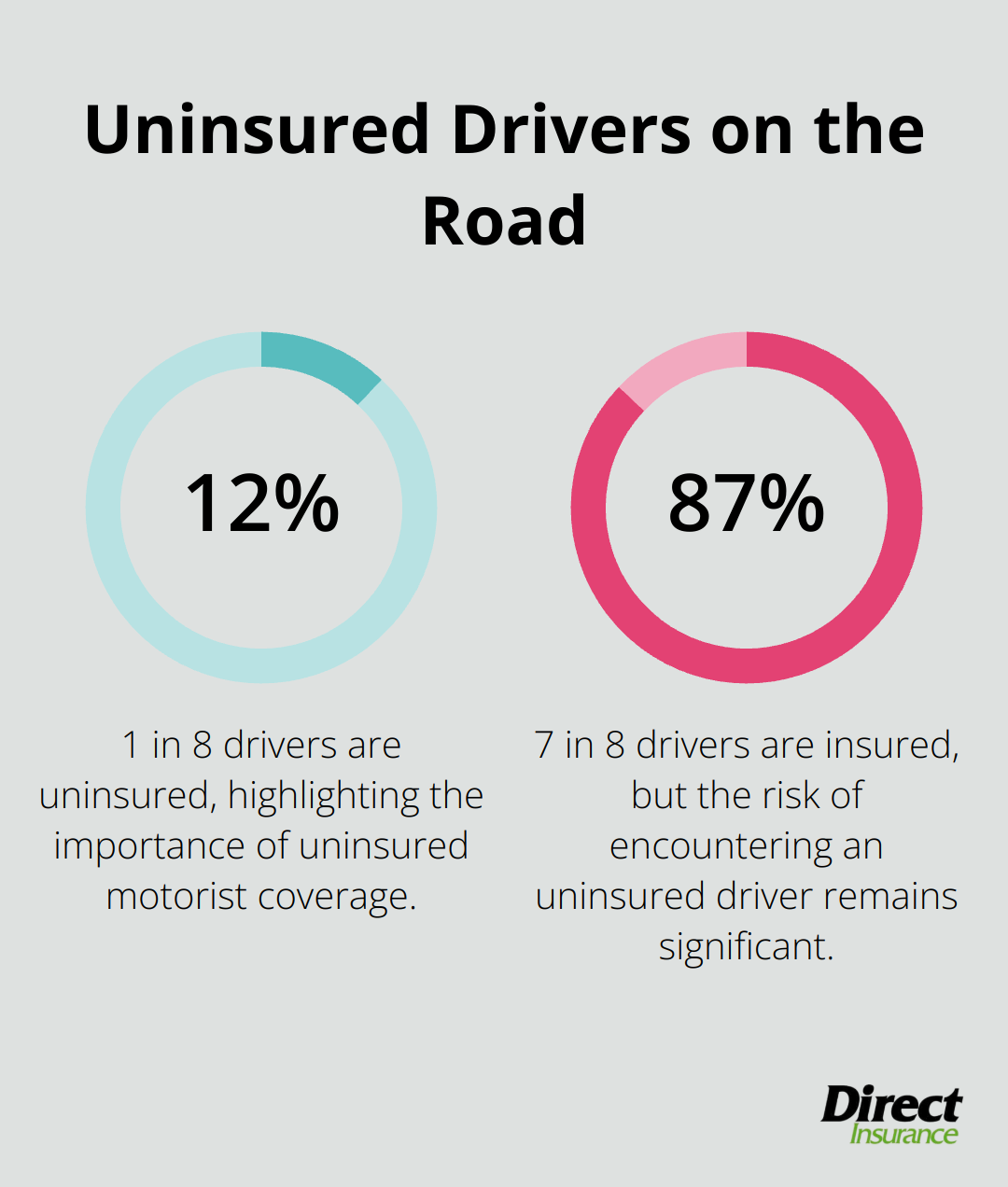

This coverage protects you if you’re in an accident with a driver who has insufficient or no insurance. The Insurance Research Council estimates that about 1 in 8 drivers are uninsured, making this coverage particularly important.

Tailoring Your Coverage

Choosing the right auto insurance coverage isn’t just about meeting legal requirements-it’s about protecting your financial well-being. At Direct Insurance Services, we commit to helping you find the right balance of coverage and cost. We’ll work with you to understand your specific needs and create a policy that gives you peace of mind on the road.

Now that we’ve covered the types of auto insurance coverage, let’s explore the factors that influence how much coverage you actually need.

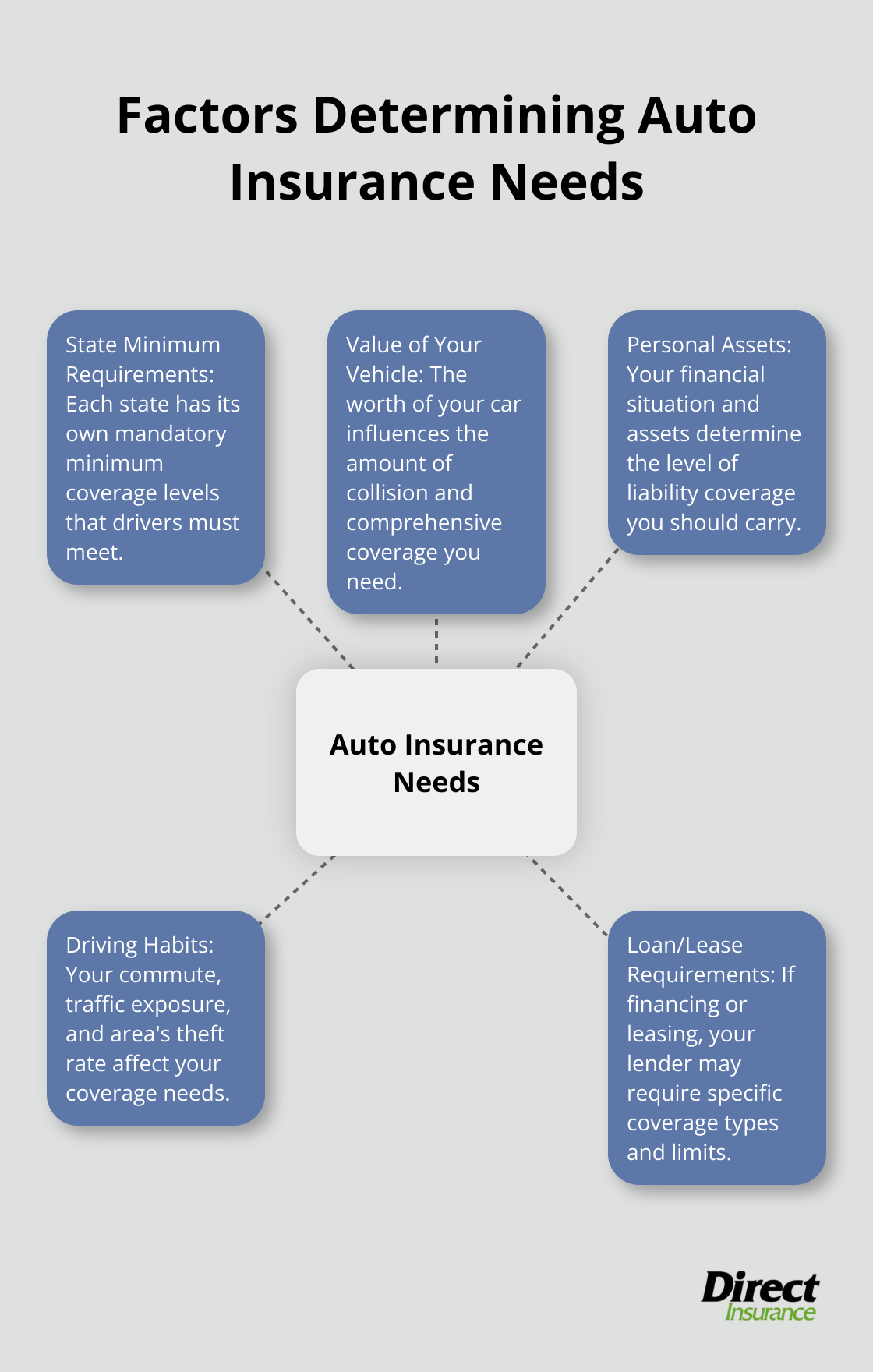

What Factors Determine Your Auto Insurance Needs?

At Direct Insurance Services, we understand that determining the right amount of auto insurance coverage isn’t a one-size-fits-all process. Several key factors influence how much coverage you need. Let’s explore these factors to help you make an informed decision about your auto insurance.

State Minimum Requirements

Every state has its own minimum auto insurance requirements. In Utah, drivers must carry at least $25,000 per person and $65,000 per accident for bodily injury liability, and $15,000 for property damage liability. However, these minimums often fail to provide full protection in the event of a serious accident. We recommend higher limits to ensure adequate protection.

The Value of Your Vehicle

Your car’s value plays a significant role in determining your coverage needs, particularly for collision and comprehensive coverage. If you own a newer or more expensive vehicle, you’ll want to ensure you have enough coverage to repair or replace it if it’s damaged or stolen. For an older car with a low market value, you might consider dropping these coverages to save on premiums.

Your Personal Assets and Financial Situation

Your personal assets and financial situation are important factors in determining your coverage needs. If you own a home, have significant savings, or other valuable assets, you’ll want higher liability limits to protect these assets in case of a lawsuit following an accident. The Insurance Information Institute suggests carrying at least $100,000 per person and $300,000 per accident in bodily injury liability coverage.

Driving Habits and Risk Factors

Your driving habits and personal risk factors also influence your coverage needs. If you have a long commute, frequently drive in heavy traffic, or live in an area with a high rate of auto theft, you might need more comprehensive coverage. Additionally, if you often drive with passengers, higher personal injury protection limits might be advisable.

Loan or Lease Requirements

If you’re financing or leasing your vehicle, your lender will likely require you to carry full coverage (collision and comprehensive coverage in addition to the state-mandated liability coverage). They may also specify minimum coverage limits to protect their investment in your vehicle.

Understanding these factors is just the first step in determining your auto insurance needs. Next, we’ll explore recommended coverage levels for different scenarios to help you make an informed decision about your policy.

How Much Coverage Do Different Drivers Need?

At Direct Insurance Services, we understand that every driver’s insurance needs are unique. Let’s explore recommended coverage levels for various scenarios to help you make an informed decision about your auto insurance.

New Car Owners

New vehicle owners should protect their investment with comprehensive coverage. We recommend full coverage, including collision and comprehensive, with limits that match or exceed your car’s value. For liability, consider limits of at least $100,000 per person and $300,000 per accident for bodily injury, and $100,000 for property damage.

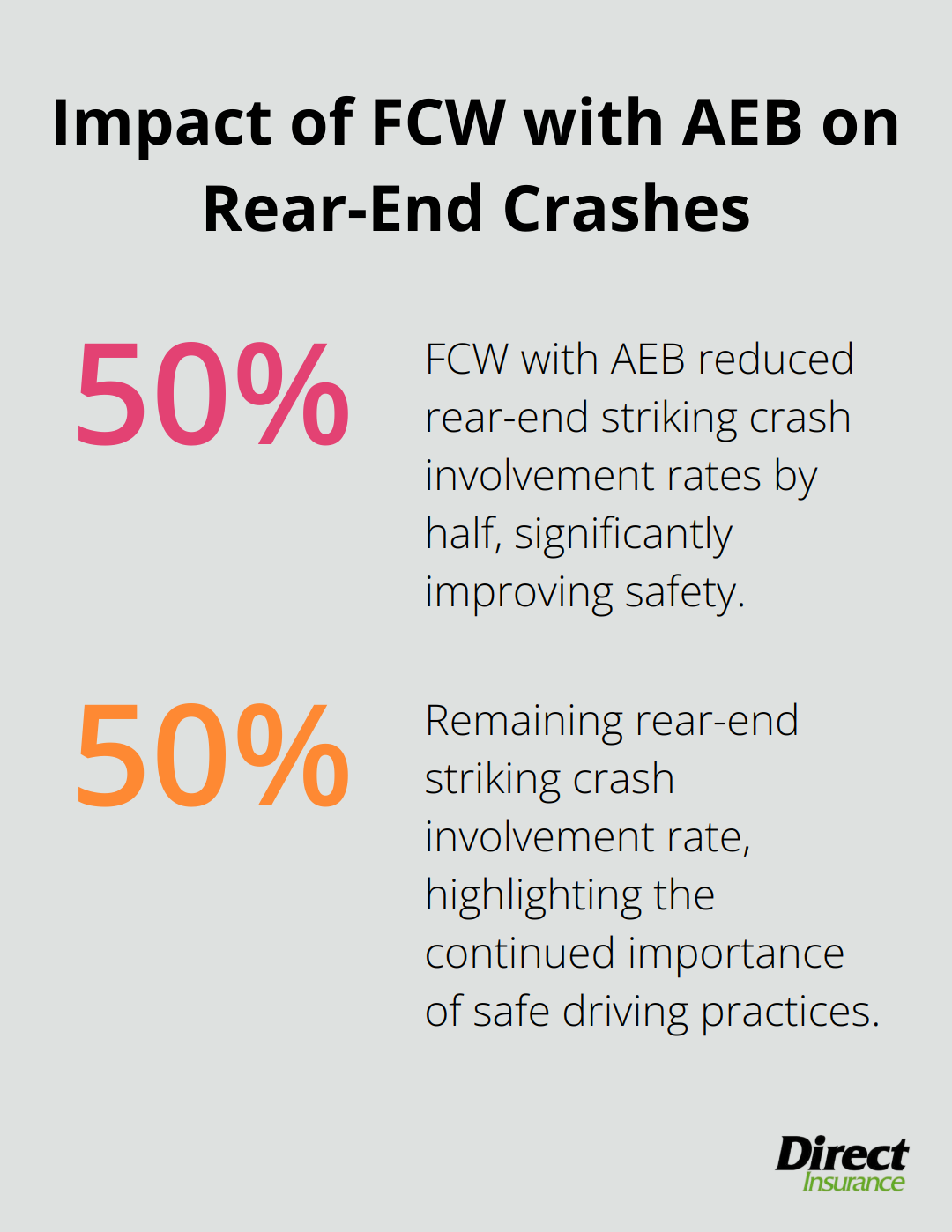

New cars often come with advanced safety features, which can lead to insurance discounts. The Insurance Institute for Highway Safety reports that FCW with AEB reduced rear-end striking crash involvement rates by 50%. Ask us about potential savings for these features.

Used Car Owners

Used car owners’ coverage needs depend on their vehicle’s value and financial situation. If your car is worth less than $4,000, you might consider dropping collision and comprehensive coverage to save on premiums. However, maintain high liability limits to protect your assets.

A study by Kelley Blue Book found that the average age of vehicles on U.S. roads is 12.2 years. If your car falls into this category, focus on robust liability coverage rather than full coverage.

High-Net-Worth Individuals

High-net-worth individuals need higher liability limits to protect their wealth. We often recommend liability limits of $250,000 per person and $500,000 per accident, or even higher. Consider an umbrella policy for additional protection.

According to a survey by Chubb, 40% of high-net-worth individuals are underinsured in key areas. Don’t fall into this trap – let us help you assess your true coverage needs.

Young Drivers or Students

Young drivers typically face higher premiums due to their lack of experience. Try to maintain good grades and a clean driving record to qualify for discounts. Consider higher deductibles to lower premiums, but ensure you can afford the out-of-pocket expense if needed.

The Centers for Disease Control and Prevention reports that the risk of motor vehicle crashes is higher among teens aged 16-19 than among any other age group. This underscores the importance of comprehensive coverage for young drivers.

Ride-Share Drivers

Ride-sharing drivers need specialized coverage. Your personal auto policy likely won’t cover you while you’re working. You need a specialized ride-share policy or endorsement. These policies typically offer coverage in three phases: when the app is on but you haven’t accepted a ride, when you’ve accepted a ride and are en route to pick up a passenger, and when you have a passenger in the car.

The National Association of Insurance Commissioners reports that many ride-share drivers are unaware of their coverage gaps. Don’t take this risk – let us help you find the right insurance solution for your needs.

Final Thoughts

Auto insurance coverage needs vary based on individual circumstances. We at Direct Insurance Services understand the importance of personalized coverage that protects you without unnecessary costs. Our team works closely with clients to create tailored insurance solutions that provide comprehensive protection.

Life changes often necessitate insurance adjustments. Major events like purchasing a new car, relocating, or experiencing financial shifts should prompt a coverage reassessment. We recommend erring on the side of caution when determining how much coverage you need for auto insurance.

Don’t leave your financial future to chance. Invest in the right auto insurance coverage today. We at Direct Insurance Services will guide you through this process to ensure you have the appropriate coverage for your needs and budget.