Landlords Insurance for Rentals: Protecting Your Investment

Rental properties can generate steady income, but they also expose you to significant financial risks. Landlords insurance for rentals protects your investment by covering property damage, liability claims, and lost rental income when tenants can’t pay.

At Direct Insurance Services, we’ve seen too many landlords operate without adequate coverage-and regret it when disaster strikes. This guide walks you through the essential protections you need.

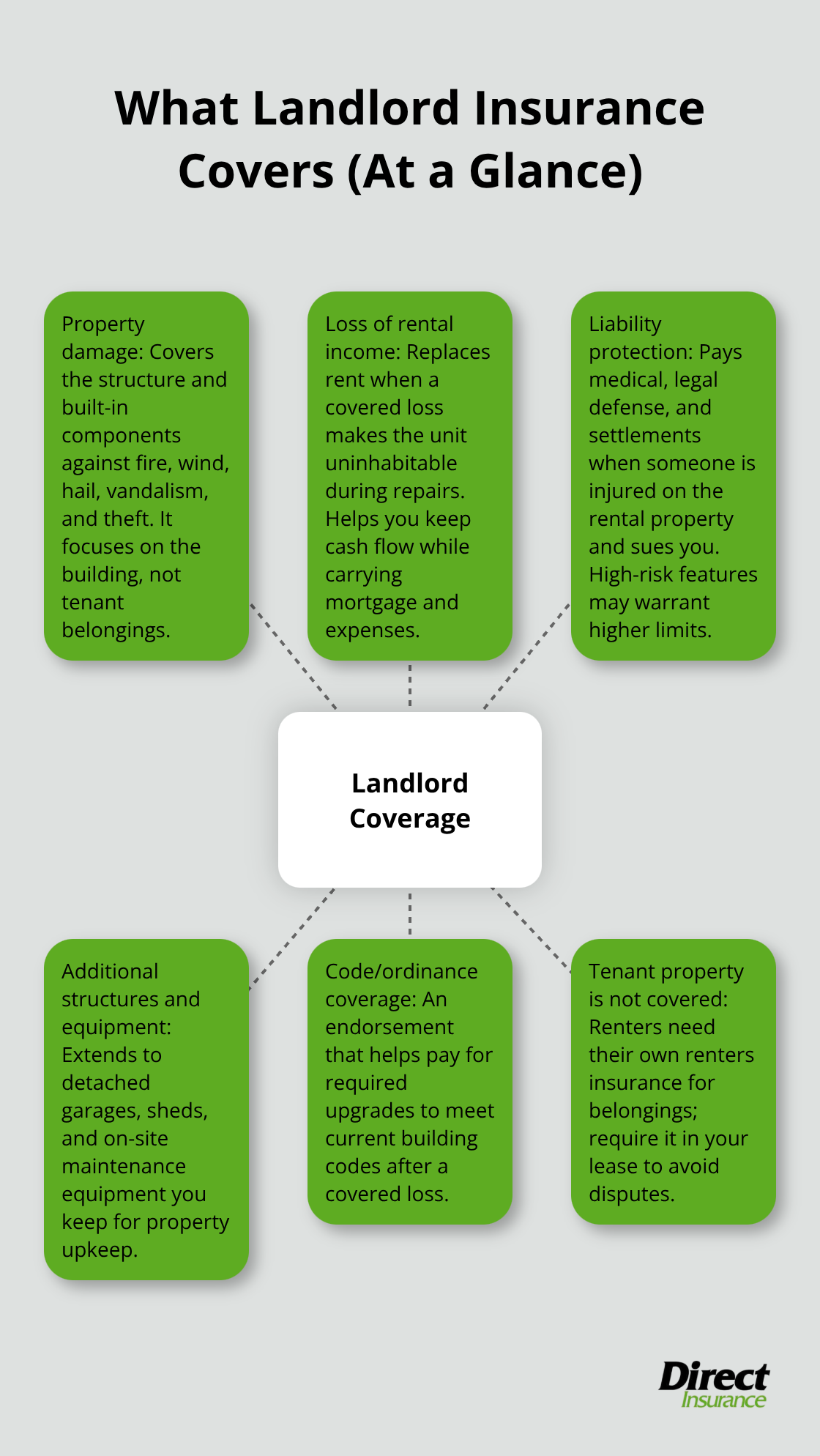

What Landlord Insurance Actually Covers

Landlord insurance fills a gap that standard homeowners policies leave wide open. If you convert your home to a rental or own investment property, your homeowners policy either excludes rental activity entirely or provides inadequate protection. Many landlords learn this gap exists only after a loss occurs-and by then it’s too late. A landlord policy protects the structure itself, including walls, roof, fixtures, and built-in appliances, from fire, windstorms, hail, vandalism, and theft. It does not cover your tenants’ belongings; that’s their responsibility through renters insurance, which you should require in your lease. What matters most is understanding what actually happens when damage occurs. If a pipe bursts and floods the unit, your policy covers the structural repair. If a tenant’s furniture is destroyed in that same flood, their renters insurance covers it, not yours.

This distinction matters because landlord policies cost less than homeowners policies precisely because they don’t cover tenant property.

When Income Loss Protection Becomes Critical

Loss of rental income coverage is the feature most landlords overlook until they need it desperately. When a fire, severe weather, or other covered event makes the property uninhabitable, this coverage reimburses the rent you would have collected while repairs happen. To calculate how much coverage you need, multiply your monthly rental income by the estimated months it would take to repair or rebuild the property after a major loss. If your property takes three months to repair and you lose $3,000 monthly in rent, that’s $9,000 in income you won’t recover without this coverage. Standard policies typically cover up to 12 months of lost rent, though extended rehab situations can exceed that window. The cost to add this coverage is modest compared to the financial devastation of losing months of income while you carry a mortgage, property taxes, and maintenance costs.

Liability Coverage Protects You From Tenant and Visitor Claims

Someone gets injured on your property-a tenant slips on ice you didn’t treat, a visitor falls down poorly maintained stairs, or a guest suffers an injury in the common area. Your personal homeowners liability won’t cover these claims because they arise from rental activity. Landlord liability coverage pays medical expenses, legal defense costs, and settlements when someone is injured on the rental property and sues you. Liability limits typically range from $300,000 to $2 million depending on your property type and risk profile. Properties with pools, decks, or outdoor stairs warrant higher limits because they present greater injury risk. If you own multiple units or have furnished rentals with more foot traffic, you absorb more liability exposure and should consider umbrella coverage that sits above your primary policy limits. This extra layer of protection costs far less than defending a single serious injury lawsuit.

What Landlord Policies Don’t Cover

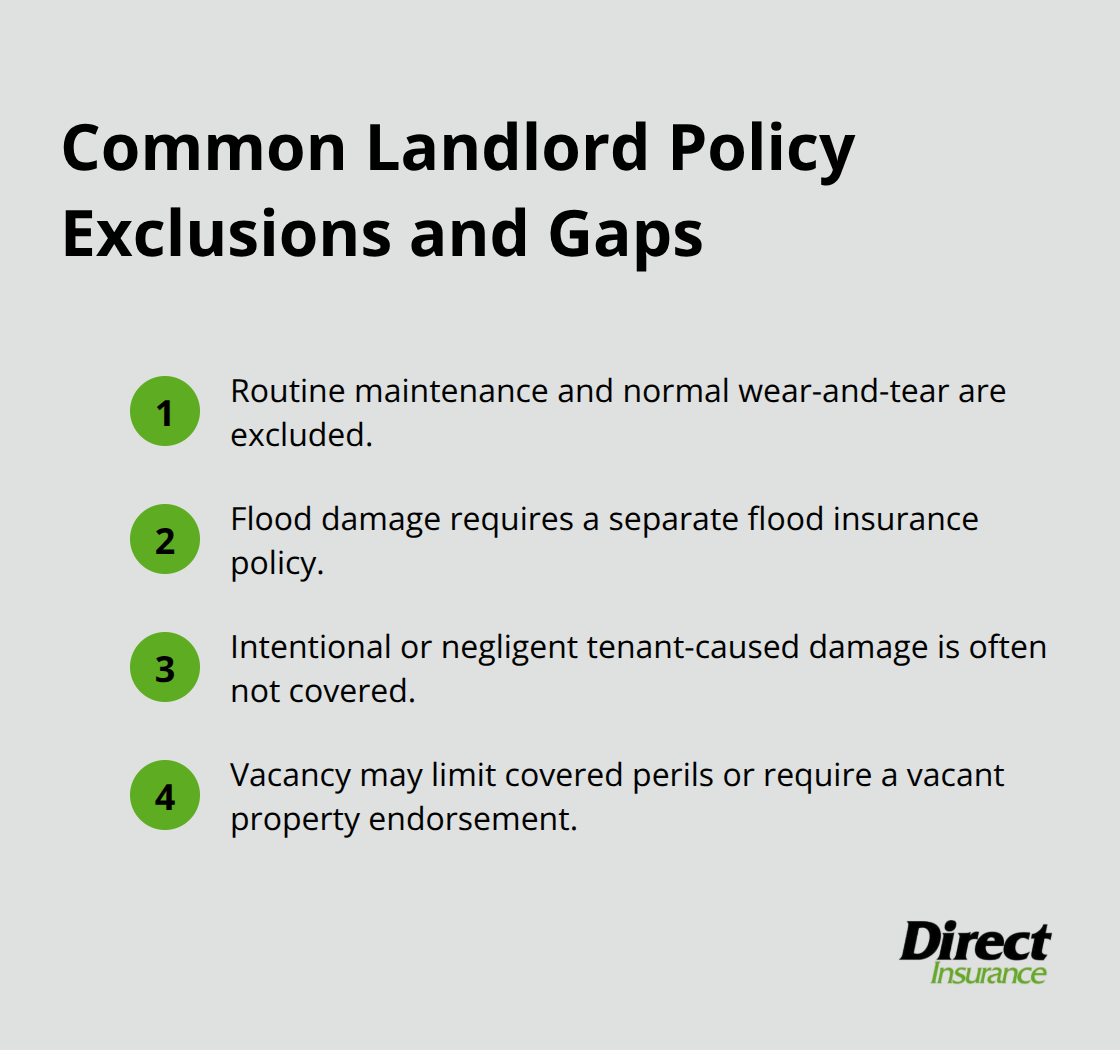

Understanding exclusions matters as much as understanding what your policy covers. Landlord insurance does not cover routine maintenance, repairs, or wear-and-tear damage-those costs fall on you as the property owner. Flood damage also falls outside standard coverage; you need a separate flood insurance policy for that protection.

Tenant-caused damage beyond normal wear-and-tear may be covered, but intentional damage or damage from tenant negligence often requires you to pursue the tenant directly rather than file an insurance claim. Vacant properties present another coverage challenge. If your rental sits empty for an extended period, your standard landlord policy may not cover certain perils or may require a vacant property endorsement. These gaps expose you to significant financial risk, which is why reviewing your specific policy terms with an agent matters before you face a loss.

Building Coverage for Your Rental Structure

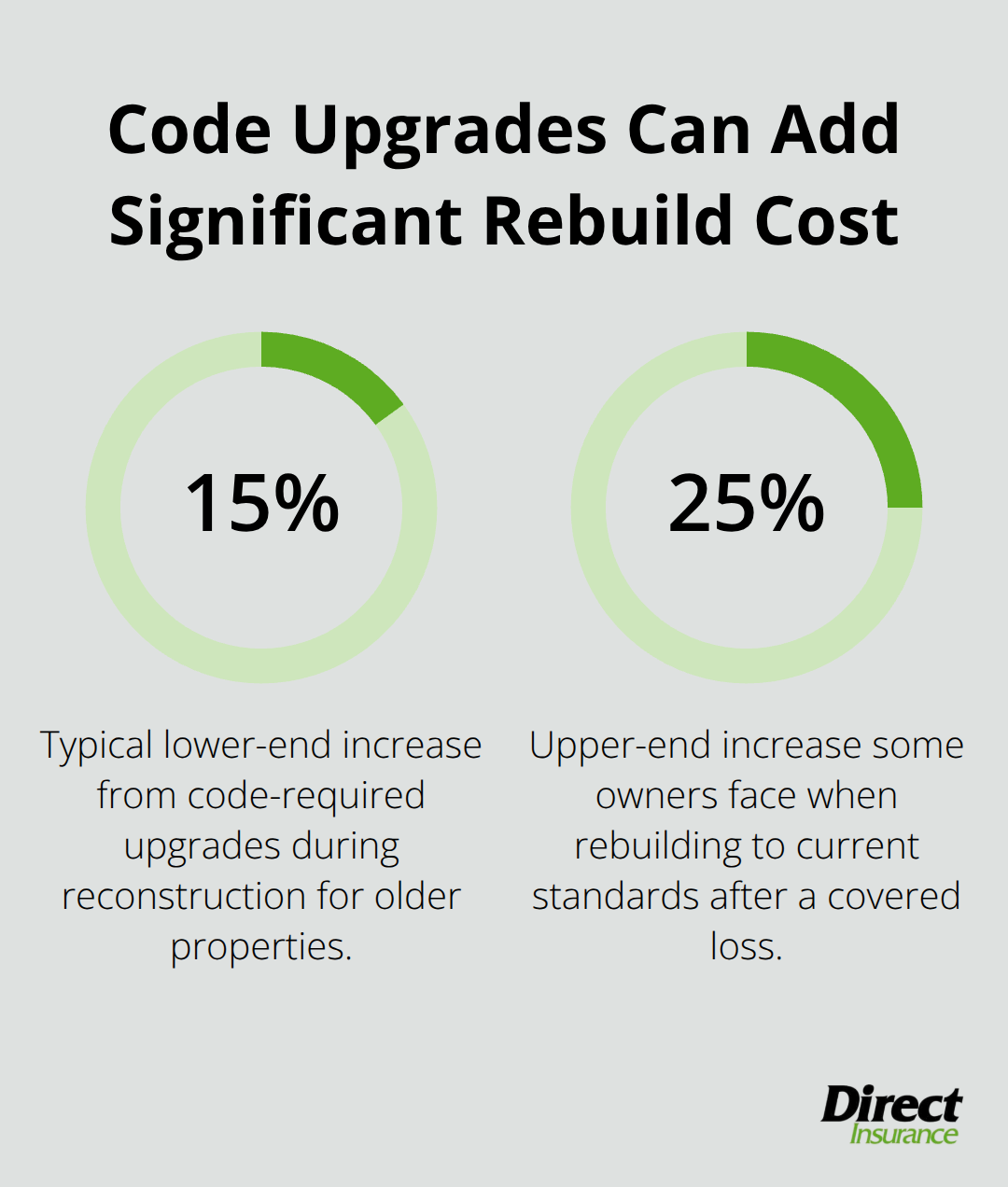

The foundation of any landlord policy is building coverage, which protects the structure and its permanent fixtures. This includes the walls, roof, flooring, built-in cabinets, and permanently installed appliances like ovens or dishwashers. Coverage limits typically range from $100,000 to $500,000, though replacement costs are rising and leaving many landlords underinsured. You should calculate the actual cost to rebuild your property from the ground up, not just the current market value, because that’s what you’ll need to restore it after a total loss. Building code coverage is an endorsement worth considering, especially for older properties. When you rebuild after a loss, current building codes may require upgrades that exceed the original construction cost. This endorsement covers those additional expenses, protecting you from unexpected out-of-pocket costs during reconstruction.

Additional Structures and On-Site Equipment

Your rental property likely includes structures beyond the main building-a detached garage, shed, or storage building. Landlord policies cover these additional structures, though you can adjust the coverage limits to match your situation. On-site maintenance equipment also receives protection under most policies. Lawn mowers, snow blowers, and other equipment you keep on the property for maintenance purposes are covered, which matters if you maintain the grounds yourself rather than hiring a service. These coverages prevent small assets from creating big financial gaps when damage or theft occurs.

Coverage That Matches Your Landlord Risk

Calculate Your True Rebuild Cost

Building coverage forms the foundation of landlord protection, but many property owners stop there and miss critical gaps. You need to choose limits based on what it actually costs to rebuild, not what you paid for the property. A home worth $400,000 on the market might cost $550,000 to rebuild from the ground up because replacement includes new materials, current labor rates, and modern building standards. Underestimating by even $100,000 leaves you paying out of pocket for repairs after a major loss. A professional rebuild cost estimate protects you from guesswork that costs thousands later.

Older properties require special attention because building code upgrades during reconstruction can add 15 to 25 percent to rebuild costs. An endorsement for code compliance coverage protects you from these surprise expenses when you must rebuild to current standards.

This small addition to your policy prevents major financial surprises after a loss.

Protect Furnishings and Personal Property

Personal property coverage inside the rental becomes critical if you furnish the unit or store your own belongings there for maintenance purposes. Standard landlord policies exclude personal property, so if you own the washer and dryer, the furniture, or equipment stored in the garage, those items sit unprotected without this endorsement. Furnished rentals command higher monthly rents, but that premium income disappears if fire destroys your furnishings and you lack coverage. Calculate what you own inside the property and match your coverage limit to that value.

Liability Protection Demands Aggressive Coverage

Liability protection deserves the most aggressive stance possible because injury lawsuits destroy rental businesses. A single slip-and-fall claim can exceed $500,000 when medical bills, legal defense, and settlement costs combine. Standard landlord liability limits of $300,000 sound adequate until you face a catastrophic injury case where a jury awards damages beyond that amount. You pay the excess from your personal assets.

Properties with higher injury risk-those with pools, decks, hot tubs, or multiple units with common areas-need minimum liability limits of $1 million, not $300,000. Umbrella policies sitting above your primary landlord coverage cost surprisingly little, often $150 to $300 annually for $1 million in extra protection. The math is simple: umbrella coverage is cheap insurance against losing everything you own.

Short-Term Rentals Require Explicit Coverage

Short-term rentals like Airbnbs create elevated liability exposure because you host strangers with higher injury risk and potential for property damage claims. Standard landlord policies often exclude or limit short-term rental coverage, so you need explicit coverage for that rental model. Insurance costs rise for short-term rentals compared to traditional long-term leases, but the liability protection justifies that expense.

If you own multiple rental properties or furnish units with significant foot traffic, umbrella coverage moves from optional to non-negotiable. An agent can evaluate your specific property type and rental model to recommend liability limits that actually match your exposure rather than settling for whatever feels standard. The next section examines the coverage gaps that catch landlords off guard and how to avoid them.

Where Landlord Policies Actually Fall Short

Landlord insurance protects your investment, but coverage gaps catch property owners off guard. Tenant damage exclusions top the list of surprises. Your policy covers damage from fire or weather, but damage a tenant causes through negligence or intentional destruction often falls outside coverage unless you pursue the tenant directly for damages. This means you absorb the cost of a tenant who deliberately punches through drywall, breaks fixtures, or causes water damage through careless behavior.

Two steps address this exposure. First, document the property condition with photos before tenants move in and require them to carry renters insurance naming you as interested party. Second, understand your specific policy’s tenant damage language because coverage varies significantly between carriers. Standard landlord policies exclude flood damage entirely, which matters because many property owners assume coverage extends to all water damage.

Natural Disasters and Flood Exposure

If you own property near rivers, in low-lying areas, or in regions with heavy rainfall, separate flood insurance is non-negotiable. Earthquake and water backup coverage also require separate endorsements in most states. These gaps expose you to catastrophic losses that your primary policy won’t cover.

Vacant Property Coverage Gaps

Vacant properties create the most problematic gap of all. When a rental sits empty during turnover, renovation, or market slowdowns, your standard policy may deny claims for certain perils or require a vacant property endorsement that costs extra. Insurance companies view vacant properties as higher risk for theft, vandalism, and weather damage, so they restrict coverage or require specific endorsements.

This exposure catches investors off guard because they assume coverage continues while the unit sits empty. If you anticipate extended vacancy, contact your agent before the property becomes empty and add the appropriate coverage rather than discovering the gap when a break-in occurs. The timing of this conversation matters because carriers impose restrictions once a property sits vacant, making it harder to add protection retroactively.

Final Thoughts

Landlord insurance for rentals protects your investment in ways that standard homeowners policies simply cannot. The coverage you’ve learned about-property damage protection, liability coverage, loss of rental income, and specialized endorsements-works together to shield you from financial devastation. Without adequate coverage, a single fire, injury claim, or extended vacancy wipes out years of rental income and forces you to pay repairs from personal savings.

The gap between what you think you’re covered for and what your policy actually covers is where landlords lose money. Reviewing your current coverage means examining your rebuild cost estimates, liability limits, and whether your policy addresses your specific rental model (furnished units, short-term rentals, or flood-prone areas all demand different protection). Most landlords discover these gaps only after a loss occurs, which is too late.

We at Direct Insurance Services understand that landlord insurance decisions affect your financial security. Our team works with top-rated carriers to build coverage that matches your specific rental situation rather than settling for generic policies. Contact Direct Insurance Services today for a quote that reflects your real exposure and your budget.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation