How to Choose Between Landlord and Home Insurance

Property owners often struggle with understanding the difference between landlord and home insurance policies. These two coverage types serve distinct purposes and protect different aspects of your investment.

We at Direct Insurance Services see this confusion regularly among Utah property owners. The wrong choice can leave you financially exposed when claims arise.

What Makes These Insurance Types So Different?

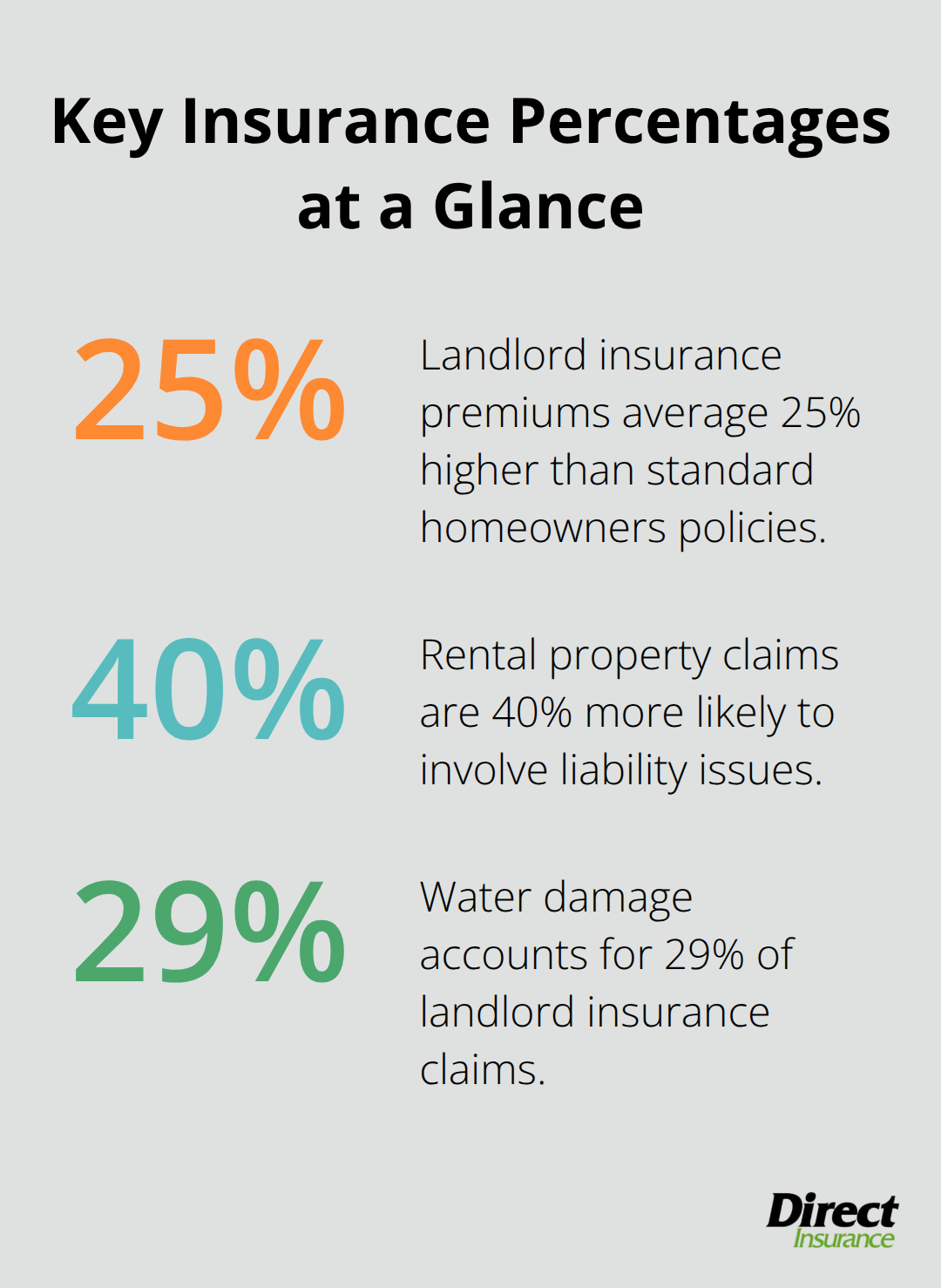

The fundamental distinction lies in property occupancy and risk exposure. Home insurance protects owner-occupied residences where you live full-time, while landlord insurance covers rental properties where tenants reside. According to the Insurance Information Institute, landlord insurance premiums average 25% higher than standard homeowners policies due to increased liability risks and vacancy periods.

Home insurance covers your personal belongings, temporary living expenses during repairs, and liability for family activities. Landlord insurance excludes tenant belongings but includes rental income protection when property damage forces vacancy.

Liability Coverage Gaps You Cannot Ignore

Tenant-related injuries create massive liability exposure that home insurance policies simply do not address adequately. Landlord insurance provides specialized liability protection for slip-and-fall accidents, property maintenance issues, and tenant guest injuries.

The Insurance Information Institute reports that homeowners insurance premiums rose by 11.2 percent in 2022 from 2021. Standard home insurance liability limits ($100,000-$300,000) prove insufficient for rental scenarios where injury settlements often exceed $500,000.

The Real Cost Breakdown

Landlord insurance costs significantly more because insurers factor in tenant turnover, property vacancy periods, and increased wear from multiple occupants. Utah rental properties face average annual premiums of $1,750-$2,400 compared to $1,200-$1,600 for homeowners insurance.

However, landlord insurance premiums qualify as tax-deductible business expenses against rental income, while homeowners insurance offers no tax benefits. Water damage claims cost landlords an average of $8,500 according to recent industry data (making comprehensive coverage essential for rental income protection).

These cost differences become even more significant when you consider specific rental scenarios that demand landlord coverage.

When Should You Choose Landlord Insurance

You need landlord insurance the moment you collect your first rent payment from a tenant. The National Association of Insurance Commissioners reports that rental property claims are 40% more likely to involve liability issues compared to owner-occupied homes. Your standard homeowners policy becomes invalid the instant you rent out your property. This leaves you completely exposed to tenant injuries, property damage, and lost rental income.

Investment Properties Demand Specialized Protection

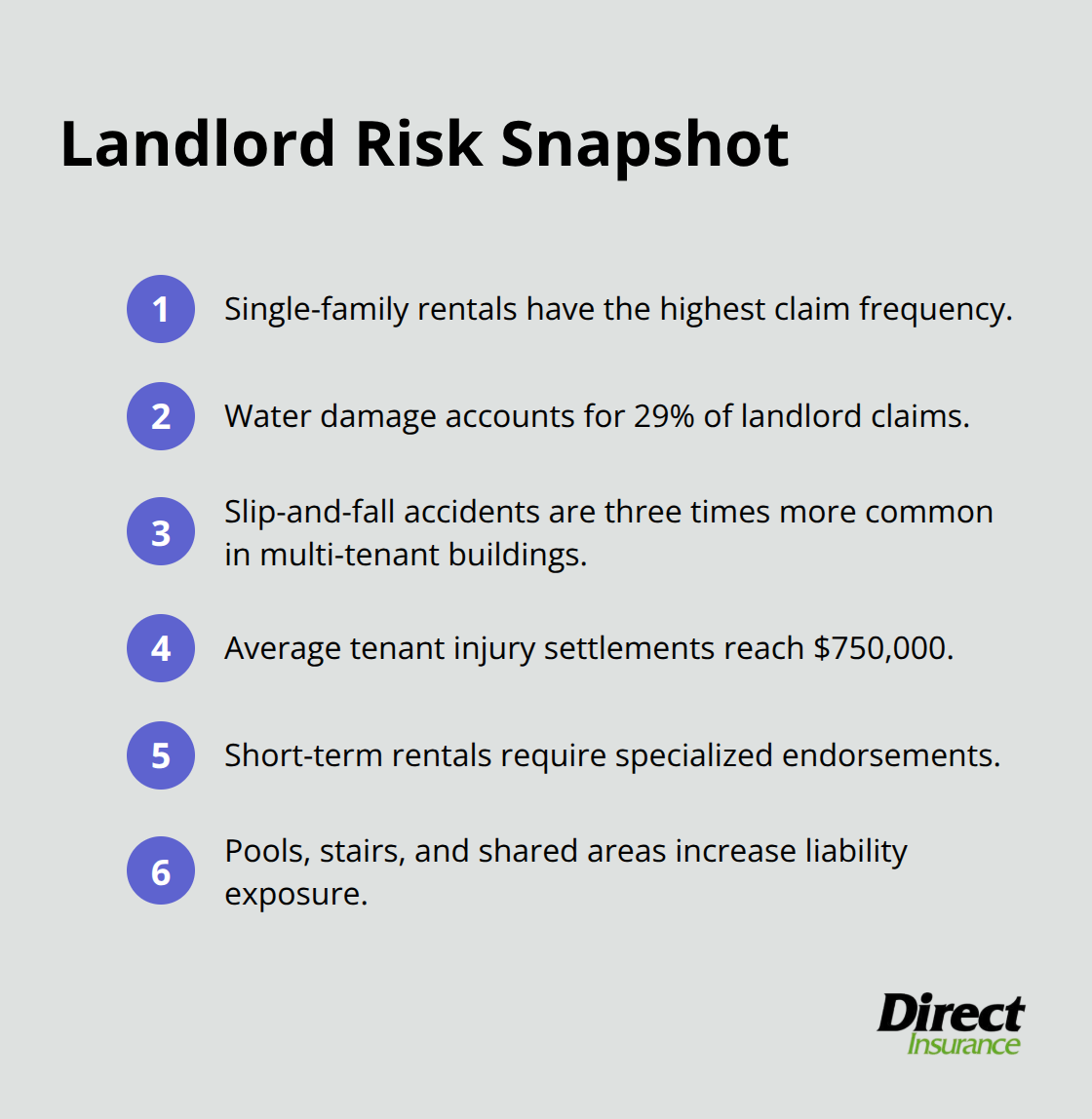

Single-family rental properties generate the highest claim frequency among landlords, with water damage accounting for 29% of all claims according to the Insurance Research Council. Multi-unit properties face even greater exposure, with slip-and-fall accidents occurring three times more often in buildings with multiple tenants.

Vacation rental properties that use Airbnb or VRBO platforms require specialized short-term rental endorsements that standard policies never cover. The average liability settlement for tenant injuries reaches $750,000, far exceeding typical homeowners liability limits of $300,000. Properties with pools, stairs, or shared common areas create massive liability gaps that only landlord insurance addresses properly.

Investment properties generally cover things like damage to the structures and can be customized to cover damage to systems, furnishings and appliances within those structures.

Tenant Turnover Creates Unavoidable Risks

Vacant rental properties face 43% higher burglary rates than occupied homes (making vacancy protection coverage absolutely necessary for landlords). Tenant-caused damage averages $2,100 per incident beyond normal security deposits, while malicious damage can reach $15,000 or more.

Properties rented to college students show 67% higher claim rates due to parties and negligent behavior. Month-to-month tenancies increase your risk profile significantly compared to long-term lease agreements. Smart landlords require tenant renters insurance, but this only covers tenant belongings and never protects your property investment or rental income streams.

When Standard Coverage Falls Short

Standard homeowners policies exclude coverage for business activities, which includes rental income generation. Insurance companies view rental properties as commercial ventures that require specialized protection. The moment you advertise your property for rent, your homeowners policy exclusions take effect (even before you sign a lease agreement).

However, certain property ownership situations call for traditional homeowners coverage instead of landlord insurance.

When Does Home Insurance Make Sense

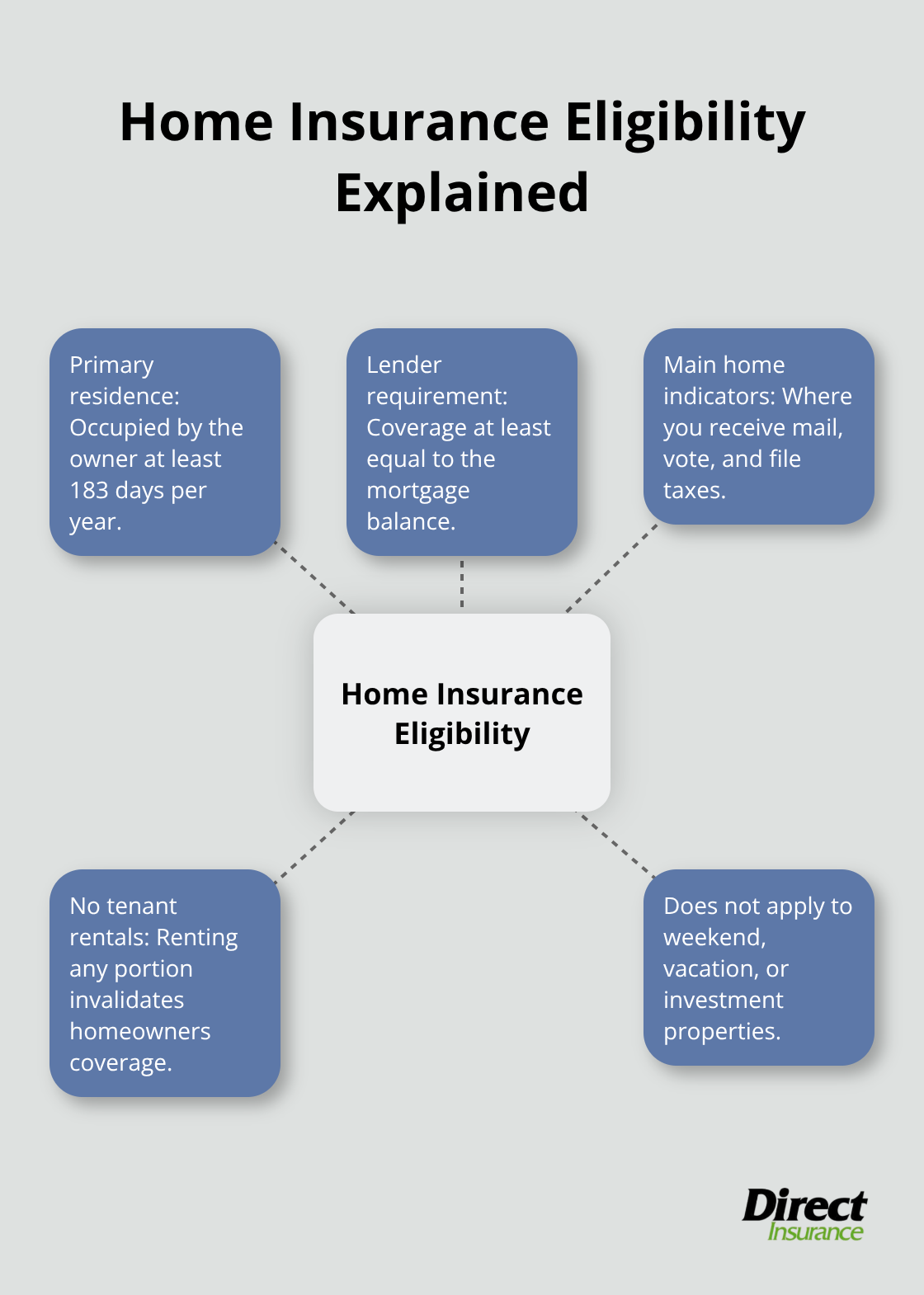

Home insurance protects owner-occupied properties where you live as your primary residence full-time. The National Association of Insurance Commissioners defines primary residence as a property occupied at least 183 days per year by the owner. This coverage becomes invalid the moment you rent out any portion of your home to tenants, even temporarily.

Primary Residence Protection Requirements

Your mortgage lender requires homeowners insurance for occupied primary residences, with minimum coverage equal to your loan balance. The Federal Housing Finance Agency reports that 64% of American households own their primary residence (which makes homeowners insurance the most common property coverage type). Properties must serve as your main home where you receive mail, register to vote, and file tax returns. Weekend homes, vacation properties, or investment properties never qualify for homeowners coverage regardless of how often you visit them.

Personal Property Coverage Limits

Homeowners insurance covers personal items up to 50-70% of your home coverage amount, with average limits that range from $150,000 to $300,000 according to the Insurance Information Institute. High-value items like jewelry, art, or collectibles require separate endorsements with individual item limits typically capped at $2,500. Standard policies exclude business equipment, inventory, or rental property items completely. The Insurance Research Council reports that regulatory delays and disparities challenge the homeowners insurance market, which creates coverage gaps when total loss claims occur.

Occupancy Rules That Cannot Be Broken

Insurance companies monitor occupancy patterns through claims investigations and property inspections. You void your homeowners policy immediately when you rent out rooms, basement apartments, or entire homes, and coverage becomes invalid retroactively. Even occasional short-term rentals through Airbnb trigger policy cancellation, with insurers who deny claims and potentially pursue fraud charges. Property owners face significant financial losses when they confuse homeowners and landlord insurance, with 5.3 percent of insured homes filing claims annually. Properties left vacant for more than 30 consecutive days require special vacant home endorsements with significantly higher premiums and reduced coverage.

Final Thoughts

The difference between landlord and home insurance centers on property occupancy and risk exposure. Property owners who live in their homes need homeowners insurance, while those who collect rent require landlord coverage. This decision affects your financial protection, premium costs, and legal compliance with mortgage requirements.

Utah property owners face significant consequences when they choose incorrectly. Homeowners policies become void the moment you rent out your property (which leaves you exposed to tenant injuries and property damage claims). Landlord insurance costs 25% more but provides rental income protection and higher liability limits that rental properties demand.

Your mortgage lender, tax situation, and intended property use determine which coverage type you need. Investment properties, vacation rentals, and tenant-occupied homes require landlord insurance without exception. We at Direct Insurance Services help Utah property owners navigate these complex insurance decisions, and our independent agency works with top-rated carriers to find coverage that fits your specific situation and budget. Contact Direct Insurance Services today to review your property insurance needs and protect your investment properly.