Can Landlords Legally Require Tenants to Have Pet Insurance?

Pet ownership in rental properties creates complex legal questions that affect millions of tenants nationwide. Can a landlord require pet insurance as a condition of your lease agreement?

We at Direct Insurance Services see these disputes regularly, and the answer varies significantly by state and local jurisdiction. Understanding your rights and obligations helps both landlords and tenants navigate this evolving area of rental law.

What Laws Actually Allow Pet Insurance Requirements?

State Law Variations Create Uneven Protection

Most states grant landlords broad authority to set lease terms, including pet insurance requirements. Oklahoma allows landlords to charge pet rent, though tenants with emotional support animals are exempt from pet fees or deposits under state ESA laws. Virginia represents the majority approach and allows landlords to include pet insurance clauses as standard contractual conditions. This state-by-state patchwork means your rights depend entirely on your zip code.

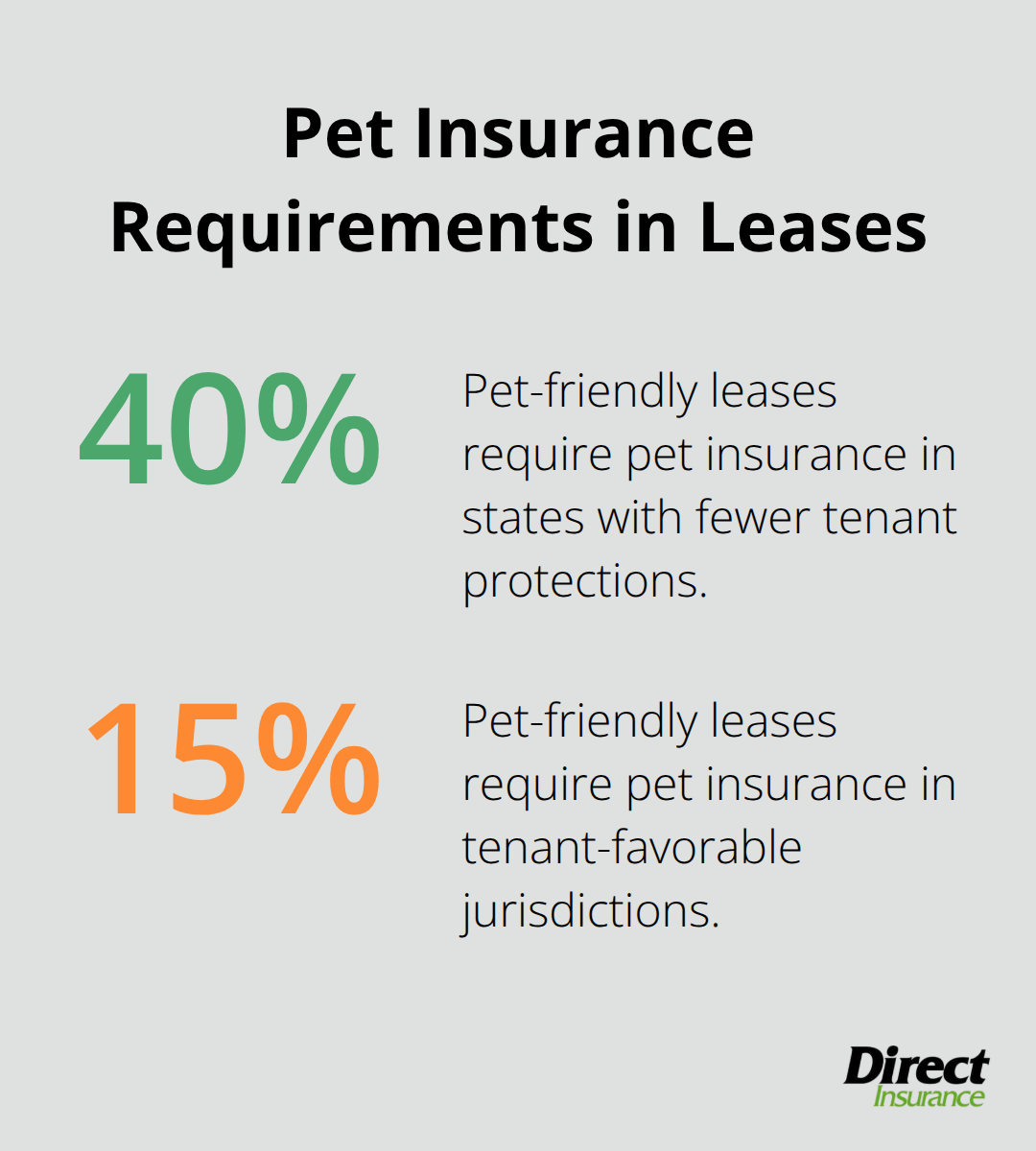

Cities with rent control like San Francisco and New York impose additional restrictions on insurance-related fees, though landlords can still require coverage itself. Research from landlord associations shows that states with fewer tenant protections see pet insurance requirements in approximately 40% of pet-friendly leases, compared to just 15% in tenant-favorable jurisdictions.

Fair Housing Laws Protect Service Animals

The Fair Housing Act creates a clear distinction between pets and service animals that landlords frequently misunderstand. Service animals and emotional support animals cannot be subject to pet insurance requirements, pet deposits, or pet fees under federal law. Landlords who attempt to impose these requirements on disability-related animals face significant legal liability.

Pet ownership itself receives no Fair Housing protection, which means landlords can legally deny applications based solely on pet ownership. This fundamental difference explains why landlords maintain extensive breed restriction lists while simultaneously being required to accommodate service animals regardless of breed.

Contract Enforceability Depends on Local Standards

Lease agreements function as contracts, which makes pet insurance clauses generally enforceable if properly written. Courts consistently uphold these requirements when they specify coverage amounts, acceptable insurance providers, and clear consequences for non-compliance. The average required liability coverage ranges from $100,000 to $300,000, with some high-value properties demanding $500,000 or more.

Vague language weakens enforceability significantly. Clauses that state tenants must maintain adequate pet coverage without defining specific amounts or requirements face challenges in court. Insurance professionals recommend landlords specify exact coverage types, minimum limits, and require tenants to name the landlord as an additional insured party for maximum legal protection.

Implementation Varies by Property Type

Single-family rental homes typically see different pet insurance requirements than large apartment complexes. Individual landlords often accept basic renters insurance with pet liability coverage (around $100,000), while corporate property management companies frequently demand higher limits and specific policy features. Luxury properties commonly require umbrella policies that extend coverage beyond standard limits.

The practical implementation of these requirements affects how landlords monitor compliance and what happens when tenants fail to maintain coverage.

What Pet Insurance Do Landlords Actually Require?

Landlords typically demand standard renters insurance with pet liability coverage rather than standalone pet insurance policies. The distinction matters significantly for cost and coverage scope. Renters insurance with pet liability averages $15 to $20 monthly and includes $100,000 to $300,000 in liability protection, while separate pet insurance focuses solely on veterinary expenses and provides no property damage coverage. The Insurance Information Institute reports that dog bite claims cost homeowners insurers $1,570 million in 2024, which makes liability coverage the primary concern for property owners.

Coverage Amounts Reflect Property Values

Most landlords require liability limits between $100,000 and $300,000, though luxury properties often demand $500,000 or umbrella policies that extend beyond standard limits. Corporate property management companies frequently specify that tenants name the landlord as an additional insured party (which costs nothing extra but provides direct claim notification). High-value properties may require separate animal liability insurance for restricted breeds like Pit Bulls or Rottweilers that standard policies exclude.

Pet Deposits Remain the Preferred Alternative

Pet deposits and monthly pet rent generate immediate revenue without insurance complications. Monthly pet fees typically range from $25 to $75 per pet, while deposits average $200 to $500. These alternatives appeal to landlords who want guaranteed compensation rather than reliance on insurance claims processes. However, non-refundable pet fees face prohibition in many states, which makes refundable deposits tied to actual damages the legally safer option for property owners who seek predictable pet-related income.

Policy Exclusions Create Coverage Gaps

Standard renters insurance excludes certain dog breeds and exotic pets from liability coverage. Companies like Progressive and State Farm maintain breed restriction lists that exclude Pit Bulls, Rottweilers, and Doberman Pinschers from standard policies. Tenants with restricted breeds must purchase separate animal liability insurance or seek coverage from companies without breed restrictions (such as Auto-Owners, Chubb, or USAA). These exclusions force landlords to either accept higher risk or require additional specialized coverage that costs tenants significantly more.

The complexity of these insurance requirements creates practical challenges for both landlords and tenants that extend far beyond simple policy selection.

Who Really Benefits From Pet Insurance Requirements

Landlord Protection Shows Measurable Results

Landlords who require pet insurance gain concrete protection against expensive liability claims. The Insurance Information Institute data shows dog bite claims averaged $64,555 in 2023, with thousands of total claims nationwide. Property damage from pets extends beyond bite incidents to include scratched hardwood floors, chewed trim, and carpet damage that security deposits rarely cover completely.

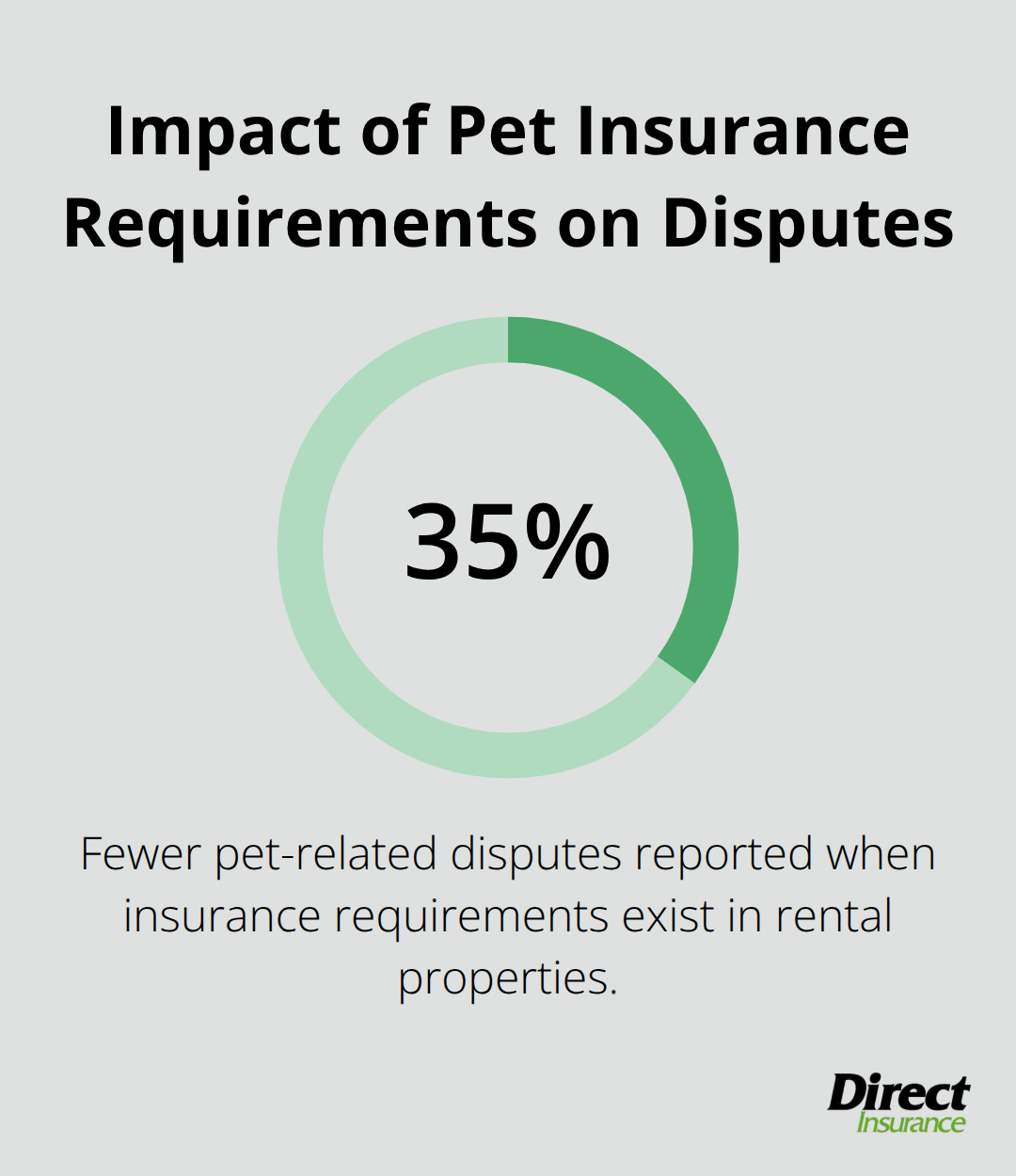

Corporate property management companies report 35% fewer pet-related disputes when insurance requirements exist, according to landlord association surveys. The insurance requirement creates accountability that reduces problematic pet behavior, as tenants with coverage maintain better control over their animals. Properties with mandatory pet insurance also see higher tenant retention rates among pet owners, who view the requirement as a sign of professional property management rather than an unreasonable restriction.

Tenant Costs Create Housing Barriers

Pet insurance requirements add $180-240 annually to rental costs, which represents a significant burden for lower-income tenants. Tenants with restricted dog breeds face even higher expenses, as specialized animal liability policies cost $300-500 yearly compared to standard renters insurance. These additional costs effectively price out responsible pet owners who cannot afford both rent increases and insurance premiums (particularly in tight rental markets where pet-friendly properties command premium rents).

Coverage limitations create frustration for tenants who discover their policies exclude specific situations. Standard renters insurance covers guest injuries from pet incidents but excludes damage to the tenant’s own property or injuries to household members. Noise complaints from barking dogs typically fall outside coverage scope, which leaves tenants vulnerable to lease violations despite maintaining required insurance.

Market Impact Reduces Pet-Friendly Options

Insurance requirements effectively reduce the supply of truly accessible pet-friendly housing. Landlords who implement these policies often combine them with breed restrictions, monthly pet fees, and higher security deposits (creating multiple financial barriers). This layered approach pushes pet owners toward a shrinking pool of properties willing to accept animals without extensive requirements.

The concentration of pet owners in fewer properties drives up rents in the remaining pet-friendly segment by 15-20% above comparable non-pet properties. Many responsible pet owners find themselves forced to choose between their animals and affordable housing, particularly in markets where landlords maintain strict insurance requirements alongside other pet-related fees.

Final Thoughts

The question “can a landlord require pet insurance” has no universal answer due to state laws and local regulations that vary significantly. Most states allow these requirements as standard lease conditions, while places like Oklahoma and rent-controlled cities impose specific limitations. Courts consistently uphold properly written clauses that specify coverage amounts and policy requirements, which clearly favors landlord authority in most jurisdictions.

Smart landlords focus on liability coverage rather than veterinary pet insurance and typically require $100,000 to $300,000 in renters insurance with pet liability protection. This approach provides meaningful protection against the average $64,555 dog bite claim while tenants can afford the monthly premiums. Successful implementation requires clear lease language, specific coverage amounts, and landlords must be named as additional insured parties.

Tenants should understand that service animals remain exempt from all pet-related fees and insurance requirements under federal law. The rental market continues to evolve toward more sophisticated pet policies that balance landlord protection with housing accessibility. We at Direct Insurance Services help property owners and tenants navigate these complex insurance requirements through personalized coverage solutions that protect both parties.