Contractor Liability Coverage: Essential Protections for Pros

One accident on a job site can cost you $50,000 or more in medical bills, legal fees, and property damage claims. Without contractor liability coverage, that bill comes straight out of your pocket and can shut down your business overnight.

At Direct Insurance Services, we’ve seen contractors lose everything because they skipped this protection. The right policy covers bodily injuries, property damage, and legal defense costs so a single claim doesn’t destroy what you’ve built.

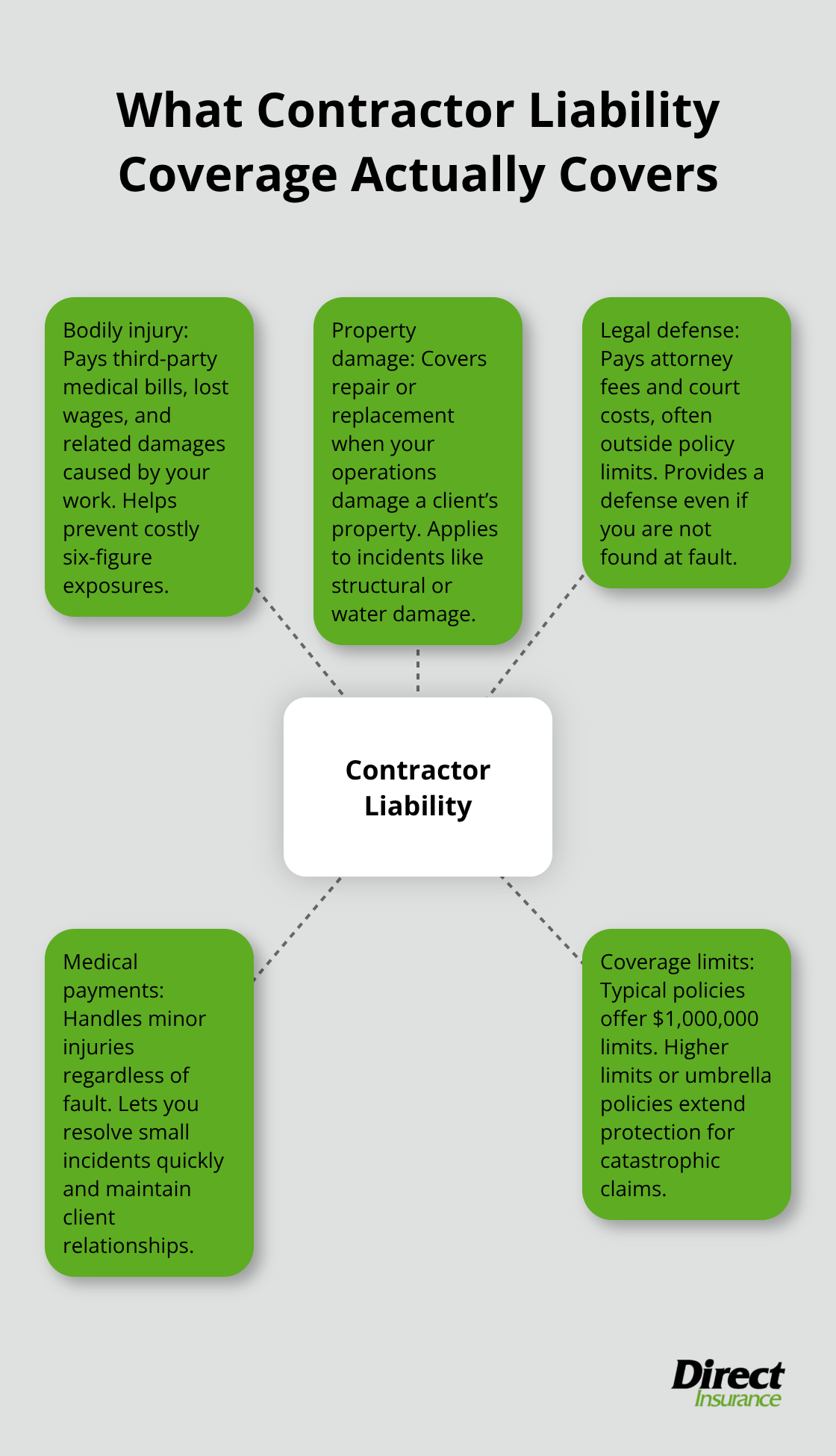

What Contractor Liability Coverage Actually Covers

Contractor liability coverage protects you from the financial fallout of accidents and damage that occur because of your work. When a homeowner trips over your equipment and breaks their arm, or your crew accidentally damages a client’s foundation during excavation, liability coverage pays for their medical bills, property repairs, and legal defense costs.

The Hartford reports that construction businesses pay an average of $1,351 per year for general liability insurance, or roughly $113 per month. That relatively modest expense stands between you and potential claims that can reach $50,000, $100,000, or more depending on the severity of the incident. Without this protection, you remain personally responsible for every penny of damages, settlements, and court costs.

Bodily Injury Claims Hit Hard and Fast

A single injury on your job site can escalate quickly into a six-figure liability claim. If a client’s employee gets hurt while you work on their property, they will file a claim against your liability policy rather than pay out of pocket. Medical expenses alone for serious injuries-surgery, hospitalization, physical therapy-routinely exceed $25,000 to $50,000. Add in lost wages for the injured person, pain and suffering damages, and legal fees to defend yourself, and the total climbs substantially higher. Research shows that bodily injury claims in construction average $27,000 per case, nearly double the per-case cost across all industries. Your liability coverage pays these costs up to your policy limits, which typically range from $1,000,000 in coverage. For a $1,000,000 liability limit, The Hartford reports you will pay approximately $824 per year. That investment protects your personal assets and business income from seizure to satisfy a judgment.

Property Damage Disputes Become Costly Fast

Property damage claims arise constantly in contracting work. You accidentally back a truck into a client’s fence, a water line breaks during foundation work and damages their landscaping, or your crew causes structural damage during a renovation. Clients rarely let these incidents slide, and they expect your insurance to cover repairs or replacement. Without liability coverage, you negotiate out-of-pocket settlements while your cash flow suffers. Legal disputes over property damage are common, and your liability policy covers not just the repair costs but also the attorney fees needed to defend your position if the client sues. This dual protection-covering both damages and defense-separates contractors who survive mistakes from those who don’t.

Medical Payments Coverage Stops Small Claims From Becoming Big Problems

Medical payments coverage (sometimes called med pay) handles minor injuries without requiring a formal liability claim. If a client or their employee sustains a small injury on your job site-a cut, minor burn, or minor fall-med pay covers their immediate medical treatment up to a set limit, typically $1,000 to $5,000 per incident. This coverage pays regardless of fault, which means you can resolve minor incidents quickly and maintain good client relationships. Without med pay, even a $500 emergency room visit becomes a negotiation that damages your reputation. The Hartford data shows that contractors with comprehensive coverage (including med pay) experience fewer disputes with clients over small incidents, allowing you to focus on completing projects rather than managing claims.

Legal Defense Costs Protect Your Bottom Line

Your liability policy covers attorney fees and court costs even if you ultimately win the case. A contractor facing a property damage lawsuit might spend $10,000 to $30,000 in legal fees before the case settles or concludes. Your insurance company assigns a defense attorney and covers those expenses separately from your policy limits in most cases. This means you don’t deplete your coverage amount just to defend yourself in court. Without this protection, you pay legal fees out of pocket while simultaneously facing potential damages if you lose. The combination of damage coverage and legal defense coverage makes liability insurance the single most important protection for your contracting business.

These protections form the foundation of what you need, but the specific types of policies and coverage limits vary based on your trade, the size of your operation, and the clients you serve.

Which Liability Policy Matches Your Contracting Business

General liability coverage forms the backbone of protection for nearly every contractor, but the specific policy structure and limits you need depend heavily on your trade, project scope, and client requirements. Most clients contractually require proof of coverage before you step on their property. The Hartford data shows construction businesses pay an average of $1,351 annually for general liability, making it an affordable baseline that protects against bodily injury, property damage, and legal defense costs. However, general liability alone leaves critical gaps for many contractors.

Trade-Specific Risks Demand Specialized Policies

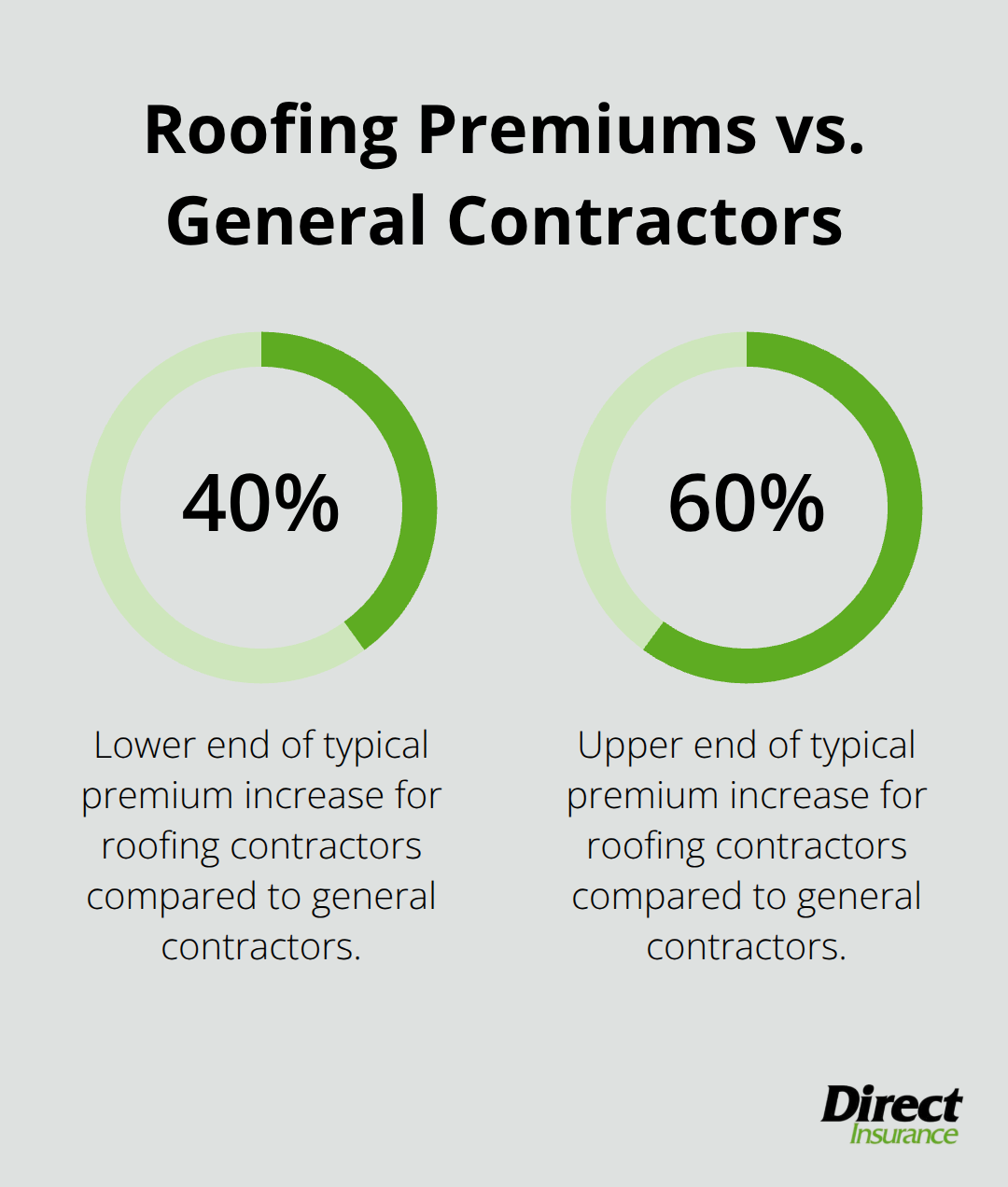

If you work in roofing, electrical work, or plumbing, your risk profile differs significantly from a carpenter or landscaper, and standard policies often exclude or limit coverage for high-risk activities. Roofers face higher injury claims due to fall hazards, so insurers typically charge 40 to 60 percent higher premiums for roofing contractors compared to general contractors. Electrical contractors face electrocution and fire risks that standard general liability policies may not adequately cover without endorsements.

Plumbers deal with water damage liability that can spiral into six-figure claims if a faulty installation floods a home. Rather than accept limited coverage under a standard policy, contractors in these trades should purchase trade-specific policies that account for their actual risk exposure.

Umbrella Policies Protect Against Catastrophic Claims

Umbrella policies provide an additional layer of protection once your underlying general liability limits are exhausted, and they become essential for contractors handling larger projects or working with commercial clients. A $1,000,000 general liability limit sounds substantial until a serious injury claim reaches $2,500,000 in damages. Your general liability policy covers the first $1,000,000, but you personally owe the remaining $1,500,000 without umbrella protection. Umbrella policies typically cost between $150 and $400 annually for $1,000,000 in additional coverage, making them remarkably affordable insurance against catastrophic exposure.

When Umbrella Coverage Becomes Non-Negotiable

Contractors working on commercial projects, large residential renovations, or handling multiple job sites simultaneously should carry umbrella coverage. The policy kicks in only after your primary liability limits are exhausted, so it supplements rather than replaces your general liability foundation. Many clients now require contractors to carry umbrella policies before bidding on projects exceeding $500,000 in value. If you serve commercial clients regularly, carrying umbrella protection demonstrates financial stability and reduces client hesitation about hiring your company. Without it, a single catastrophic claim can wipe out years of business profits and force you to liquidate personal assets to satisfy a judgment.

The coverage limits and policy types you select today directly impact which projects you can bid on tomorrow and how much financial exposure you carry on each job site.

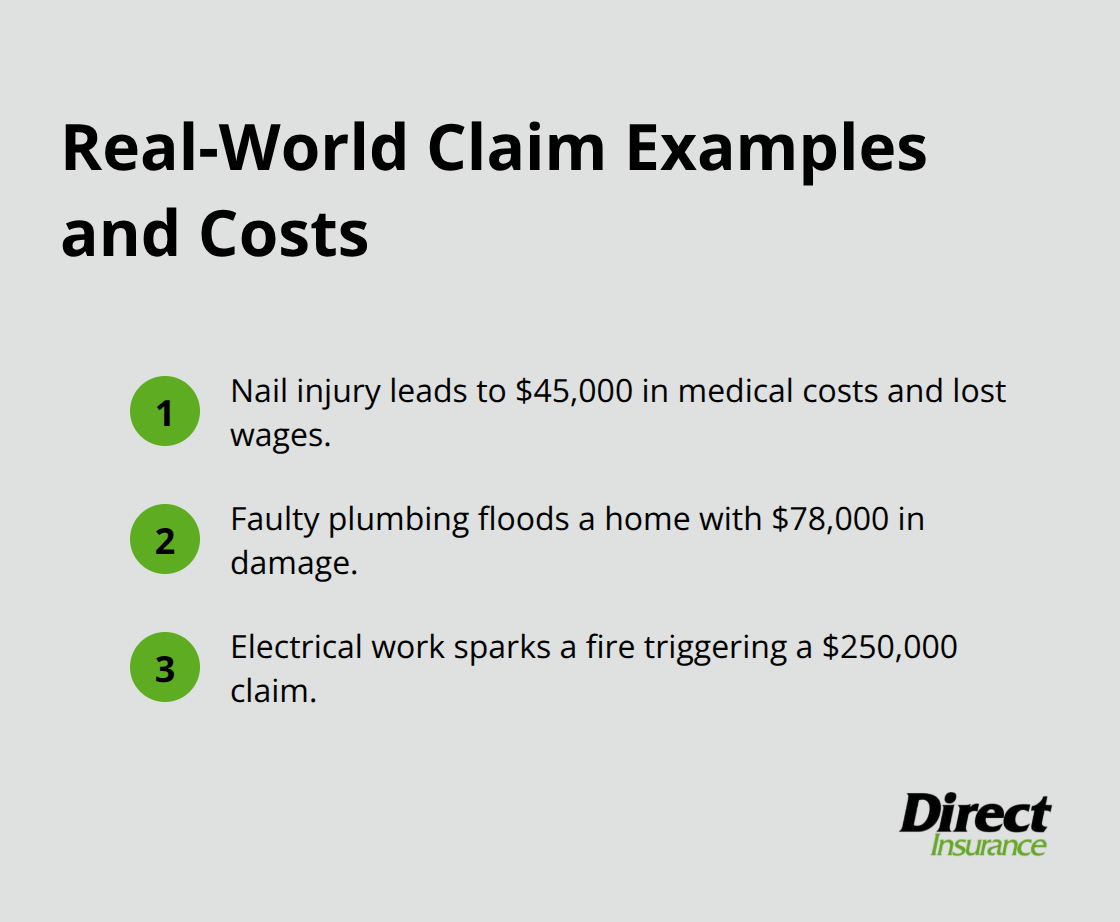

Real Claims That Destroy Contractors Without Coverage

A worker steps on a nail you left on a client’s deck and develops a serious infection requiring hospitalization and lost wages totaling $45,000. A plumber’s faulty installation floods a home, destroying hardwood floors and causing mold remediation costs that reach $78,000. An electrician’s work causes a fire that damages adjacent structures, triggering a $250,000 claim.

These incidents happen regularly in contracting work, and they devastate contractors without proper liability coverage. Bodily injury claims in construction average $90,043 per case, but serious incidents routinely exceed $100,000 when you factor in medical expenses, lost wages, and legal defense.

How Bodily Injury Claims Spiral Out of Control

A single injury on your job site escalates quickly into a six-figure liability claim. When a client’s employee gets hurt while you work on their property, they file a claim against your liability policy rather than pay out of pocket. Medical expenses alone for serious injuries-surgery, hospitalization, physical therapy-routinely exceed $25,000 to $50,000. Add in lost wages for the injured person, pain and suffering damages, and legal fees to defend yourself, and the total climbs substantially higher. Without liability coverage, you face a choice between paying out of pocket or refusing to pay and facing a lawsuit that costs $15,000 to $30,000 in legal fees alone.

Property Damage Disputes Force Expensive Settlements

You accidentally damage a client’s foundation wall during excavation, and they demand $35,000 in repairs. A roofing crew causes water damage to interior walls that wasn’t discovered for weeks, compounding repair costs and creating mold remediation expenses. Without liability coverage, you negotiate settlements while your cash flow suffers. Clients expect contractors to carry liability insurance, and they sue immediately when damage occurs because they know your policy should cover it. The legal defense costs alone can bankrupt a small operation before the claim ever settles.

Courts Award Damages That Exceed Initial Repair Costs

The financial exposure extends beyond the immediate claim amount. Courts award damages for pain and suffering, lost wages, and punitive damages in cases where negligence is clear. A contractor who caused a serious injury might face a $75,000 medical bill, $25,000 in lost wages for the injured person, $40,000 in pain and suffering damages, and $20,000 in legal fees-totaling $160,000 before any settlement negotiation begins. Without liability coverage, you personally owe every penny of that amount, and creditors can pursue your business assets, personal bank accounts, and even your home if the judgment is large enough.

Uninsured Contractors Lose Access to Profitable Work

Contractors working without coverage often turn to credit cards or personal loans to pay claims, starting a debt spiral that takes years to escape. The Hartford data shows that contractors with general liability coverage pay approximately $113 per month for protection that covers up to $1,000,000 in damages. That investment is so modest compared to the financial destruction of a single uninsured claim that operating without coverage represents reckless business management. Clients increasingly require certificates of insurance before allowing work to begin, which means you cannot bid on professional projects without coverage. You lose access to higher-paying commercial work, renovation contracts, and repeat clients who demand proof of insurance. The competitive disadvantage alone justifies carrying liability coverage, but the catastrophic financial risk of a single claim makes it non-negotiable for any contractor serious about protecting their livelihood.

Final Thoughts

Contractor liability coverage protects your business from financial ruin when accidents happen on job sites. A single claim can cost $50,000, $100,000, or more, and without insurance, that expense comes directly from your pocket and threatens everything you’ve built. The monthly cost of protection remains affordable compared to the catastrophic exposure you face operating uninsured.

Your specific trade and project scope determine the coverage limits and policy types you actually need. Most clients now require proof of insurance before allowing work to begin, which means contractor liability coverage functions as both financial protection and a business requirement that opens doors to professional projects and higher-paying commercial work. Contractors without coverage lose access to these opportunities and carry unlimited personal liability for every incident that occurs on their job sites.

We at Direct Insurance Services help contractors across Utah find tailored coverage that fits your specific risks and budget. Contact us today to discuss your contractor liability coverage needs and receive a customized quote that protects your livelihood. Our team provides clear guidance on coverage options and cost-saving strategies so you can focus on completing projects rather than worrying about financial catastrophe.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation