Landlord vs Homeowners Insurance: What’s the Difference?

Navigating the world of property insurance can be confusing, especially when it comes to landlord insurance vs homeowners insurance. Many property owners struggle to understand the key differences between these two types of coverage.

At Direct Insurance Services, we often encounter clients who are unsure which policy best suits their needs. This guide will clarify the distinctions between homeowners and landlord insurance, helping you make an informed decision about protecting your property.

What Is Homeowners Insurance?

A Vital Safety Net for Property Owners

Homeowners insurance serves as an essential protection for property owners. This type of policy safeguards your home and belongings from unexpected events such as fires, storms, and theft. However, it extends beyond mere protection for your physical assets.

Financial Protection Beyond Your Four Walls

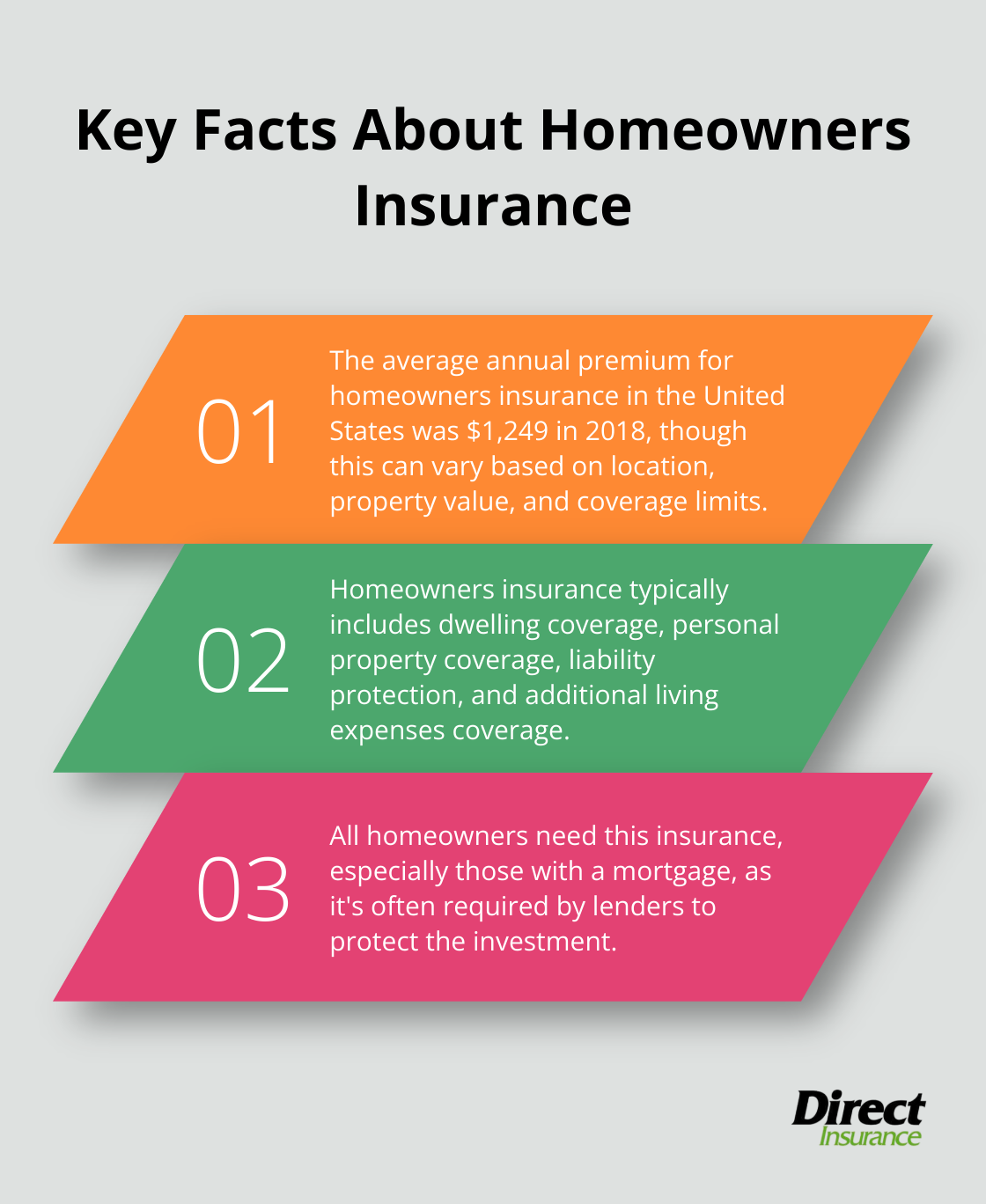

A standard homeowners insurance policy typically covers your dwelling, other structures on your property, personal belongings, and liability. The Insurance Information Institute reports that the average annual premium for homeowners insurance in the United States was $1,249 in 2018 (though this can vary significantly based on location, property value, and coverage limits).

Coverage Types You Need to Know

Most homeowners policies include several types of coverage:

- Dwelling coverage: This protects the structure of your home.

- Personal property coverage: This safeguards your belongings.

- Liability protection: This covers you if someone sustains an injury on your property.

- Additional living expenses: This helps with costs if you must temporarily relocate from your home.

Who Needs Homeowners Insurance?

If you own a home, you need homeowners insurance. It’s that straightforward. In fact, if you have a mortgage, your lender will likely require it. Even if you’ve paid off your home, maintaining coverage remains critical to protect your investment.

Real-World Impact of Proper Coverage

Proper coverage can make a significant difference in real-life situations. For instance, a homeowner recently faced substantial damage from a severe storm. Their comprehensive policy covered not only the repairs but also their temporary living expenses while the home was uninhabitable.

The right policy isn’t just about meeting lender requirements-it’s about protecting what matters most to you. Whether you’re a first-time homebuyer or want to review your current coverage, finding a policy that fits your unique needs and budget is essential.

Now that we’ve covered the basics of homeowners insurance, let’s explore how landlord insurance differs and why it’s necessary for property owners who rent out their homes.

What Is Landlord Insurance?

Specialized Protection for Rental Properties

Landlord insurance is a specialized type of property insurance. It protects property owners who rent out their homes, apartments, or other real estate investments. This insurance differs from homeowners insurance. It focuses on the unique risks associated with rental properties.

Key Components of Landlord Coverage

A typical landlord insurance policy includes several important components:

- Property Coverage: This protects the physical structure of your rental. It includes the building itself and other structures on the property (like garages or sheds). This coverage can help pay for repairs or rebuilding if your rental property suffers damage from covered events such as fire, wind, or hail.

- Liability Protection: This is a critical aspect of landlord insurance. It can help if a tenant or visitor sustains an injury on your property and you’re held responsible. For example, if someone slips on an icy walkway, your liability coverage could help cover their medical expenses and your legal fees if they decide to sue.

Income Protection: A Financial Safeguard

One of the most valuable features of landlord insurance is loss of rental income coverage. This protection can help replace the rent you would have received if your property becomes uninhabitable due to a covered loss. The National Association of REALTORS® provides the latest real estate research and statistics that affect the industry, including information on rental rates.

Who Needs Landlord Insurance?

You need landlord insurance if you rent out a property. This applies whether it’s a single-family home, a multi-unit building, or even a vacation property. Even if you only rent out a portion of your primary residence, your standard homeowners policy may not provide adequate coverage for your rental activities.

Many property owners mistakenly believe their homeowners insurance will cover their rental property. This can lead to significant gaps in coverage when they need to file a claim. If you earn rental income from a property, landlord insurance is essential.

The right insurance policy isn’t just about meeting legal requirements. It’s about protecting your investment and your financial future. Understanding and obtaining proper landlord insurance is a critical step in your journey as a landlord, whether you’re a seasoned property investor or considering renting out your home for the first time.

Now that we’ve explored the basics of both homeowners and landlord insurance, let’s examine the key differences between these two types of coverage in more detail.

How Do Homeowners and Landlord Insurance Differ?

Understanding the differences between homeowners and landlord insurance is essential for property owners. These policies serve distinct purposes and offer different types of protection. Let’s explore the key distinctions:

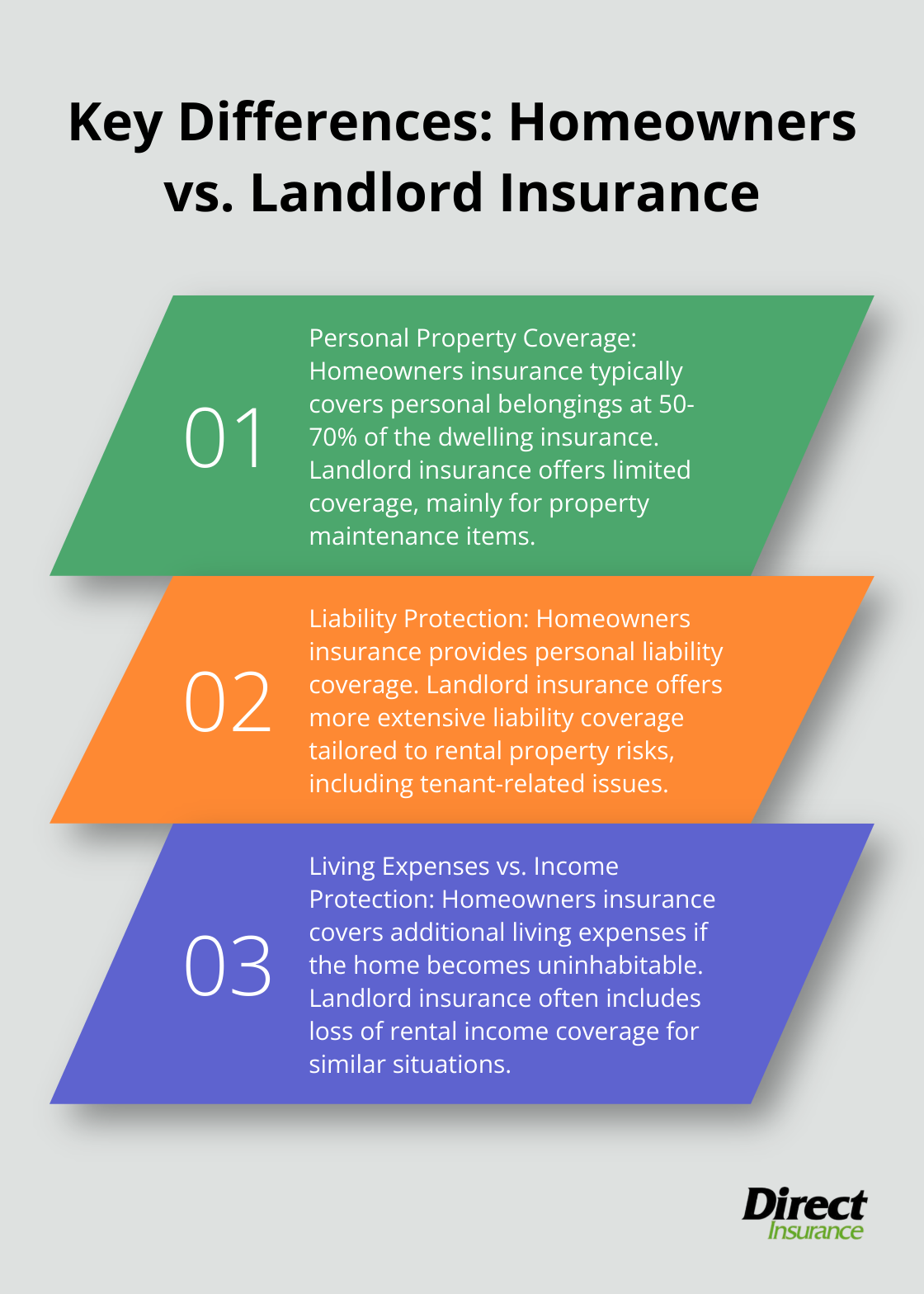

Personal Property Coverage: A Significant Difference

Home insurance provides extensive coverage for personal belongings. Standard homeowners policies usually cover personal property at about 50-70% of the insurance on the dwelling (according to the Insurance Information Institute).

Landlord insurance offers limited personal property coverage, if any. This coverage typically restricts itself to items used for property maintenance (such as lawnmowers or snow blowers). Tenants must insure their own belongings through renters insurance.

Liability Protection: Broader Scope for Landlords

Both policies offer liability protection, but the scope differs significantly:

- Homeowners insurance provides personal liability coverage. It protects you if someone sustains an injury on your property or if you accidentally damage someone else’s property.

- Landlord insurance offers more extensive liability coverage tailored to the risks of renting out property. This includes protection against lawsuits from tenants or their guests who sustain injuries on your property. It may also cover legal fees for tenant evictions.

Income Protection vs. Additional Living Expenses

These policies handle disruptions to your living situation or rental income differently:

- Homeowners insurance typically includes coverage for additional living expenses. This helps pay for temporary housing and other extra costs if your home becomes uninhabitable due to a covered loss.

- Landlord insurance often includes loss of rental income coverage. If your rental property becomes uninhabitable due to a covered event like fire or storms, this coverage can compensate you for lost rent during the repair period.

Cost Considerations

Landlord insurance typically costs more than homeowners insurance. This price difference reflects the increased risks associated with rental properties. Factors that influence the cost include:

- Property location

- Building age and condition

- Number of units

- Coverage limits

Claims Process and Frequency

The claims process and frequency often differ between these two types of insurance:

- Homeowners insurance claims typically involve the homeowner directly.

- Landlord insurance claims may involve tenants, potentially complicating the process.

Landlords may file claims more frequently due to tenant-related issues or property damage, which can affect premiums over time.

Final Thoughts

Homeowners insurance and landlord insurance serve different purposes for property owners. Homeowners insurance protects your primary residence and personal belongings, while landlord insurance addresses the specific risks of rental properties. The choice between these two types of coverage depends on how you use your property.

We at Direct Insurance Services understand the complexities of property insurance. Our team of experienced professionals helps you navigate these choices. We offer personalized insurance solutions tailored to your unique situation (whether you’re a homeowner or a landlord).

Don’t leave your property’s protection to chance. Contact Direct Insurance Services today to review your current coverage or explore new options. With our expertise, you can feel confident that your property and financial future are well-protected.