Low-Cost Auto Insurance Options for New Drivers

New drivers face insurance premiums that average $3,000-$6,000 annually, making affordable coverage a top priority. Finding low cost auto insurance for new drivers requires understanding rate factors and available discounts.

We at Direct Insurance Services help new drivers navigate these challenges with proven strategies that can reduce premiums by 20-40%. Smart coverage choices make quality protection accessible.

What Drives Your Insurance Costs as a New Driver

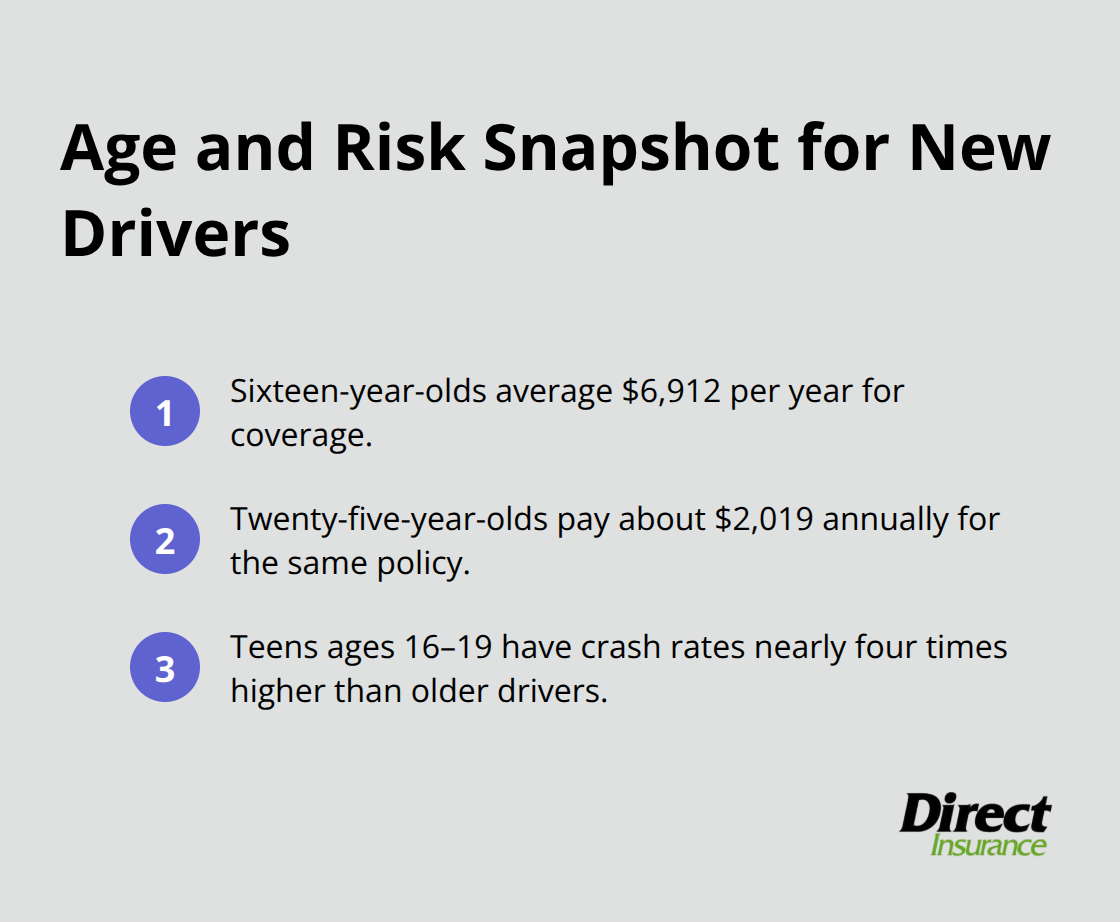

New drivers pay steep premiums because insurers calculate risk based on hard data. The Insurance Institute for Highway Safety reports that drivers aged 16-19 have crash rates nearly four times higher than older drivers, with over 2,883 teens dying in motor vehicle accidents in 2022 alone. This statistical reality drives pricing decisions that hit new drivers hard.

Age Determines Your Base Rate

Age stands as the primary cost factor in insurance calculations. Sixteen-year-olds pay an average of $6,912 annually while 25-year-olds pay just $2,019 for identical coverage (according to MarketWatch data). Insurance companies track accident patterns religiously, and the numbers paint a clear picture about risk levels across age groups.

Experience Matters More Than Time

Most insurers consider drivers new until they accumulate three years of experience behind the wheel. A 17-year-old female driver averages $6,410 in annual premiums, while males pay $7,377 due to higher accident rates. These costs drop dramatically as drivers gain experience – 25-year-old females pay $2,387 and males $2,526 annually.

Location and Credit Shape Your Premium

Credit scores heavily influence premium calculations, with higher scores yielding lower rates across all age groups. Urban drivers face steeper costs than rural counterparts due to higher theft rates, accident frequency, and repair costs. States amplify these differences significantly, with Texas teens paying $5,397 versus Ohio teens at $4,008.

Vehicle Choice Impacts Your Bill

California new drivers can expect full coverage rates reaching $567 monthly, while Hawaii offers some of the lowest teen rates at $43 for minimum coverage. Your choice of car significantly impacts your insurance costs, with sports cars and luxury vehicles costing more to insure than older, safer vehicles. Alaska averages $158 for teen minimum coverage, showing how geography impacts rates.

These cost factors create the foundation for your premium, but smart discount strategies can significantly reduce what you actually pay.

Money-Saving Strategies and Discounts

Smart discounts slash new driver premiums by thousands annually. Good student discounts reward academic performance with savings of 10-25% for students who maintain B averages or better. The Insurance Information Institute confirms that bundled auto with renters or homeowners insurance delivers significant savings. Driver education course completion earns additional discounts for drivers under 21, with some insurers offering up to 15% reductions for qualified programs.

Family Plans Beat Individual Policies

New drivers who join existing family policies cost far less than individual coverage. Teen drivers on parent policies typically save 40-60% compared to standalone insurance. Multi-vehicle discounts apply when families insure multiple cars under one policy, which creates compound savings opportunities.

Parents can add teens to their existing coverage without the massive rate increases that come with separate policies. This strategy works particularly well when parents already maintain good credit scores and clean records with their current insurer.

Technology-Based Savings Programs

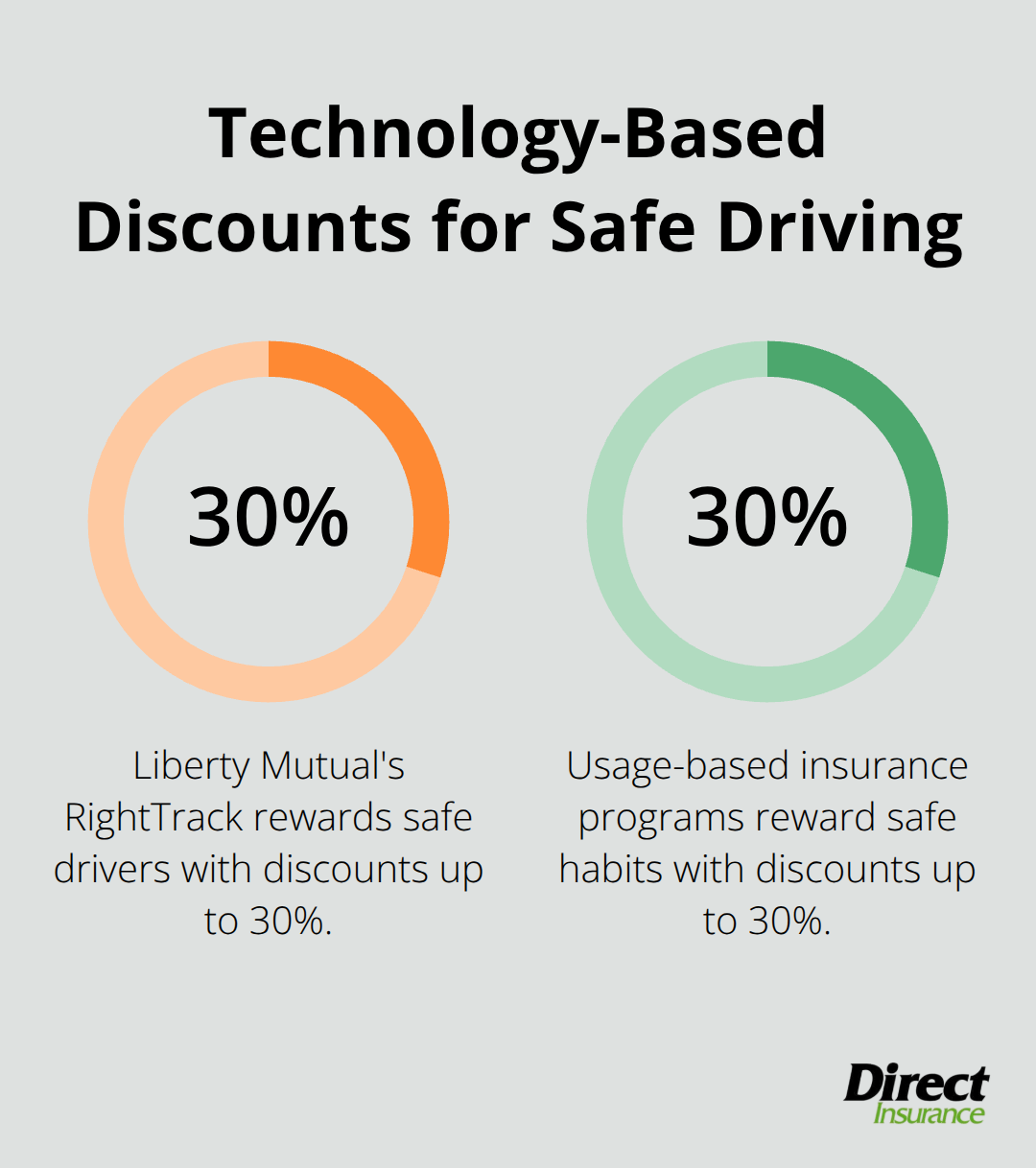

Modern insurance technology offers unprecedented savings opportunities for disciplined drivers. Liberty Mutual’s RightTrack program rewards safe drivers with discounts that reach 30%, while similar programs from major carriers track speed, braking patterns, and night frequency.

Usage-based insurance programs like telematics track actual habits and reward safe drivers with discounts up to 30%. Pay-per-mile options work exceptionally well for students who drive infrequently, with some programs that charge as little as 5 cents per mile.

Student and Low-Mileage Discounts

Student-away-at-school discounts apply when teens attend college without regular vehicle access (reducing premiums by 20-40%). Low-mileage discounts activate automatically for drivers who log fewer than 7,500 miles annually, which makes them perfect for college students or urban drivers who rely primarily on public transportation.

These programs require consistent safe habits but deliver substantial long-term savings that compound as drivers mature and maintain clean records. The key lies in understanding which coverage levels provide adequate protection without unnecessary costs.

How Much Coverage Do New Drivers Actually Need

State minimum requirements trap new drivers in a dangerous coverage gap that costs thousands when accidents happen. Most states require liability-only coverage from $15,000 to $50,000 per person, but the National Safety Council reports that motor-vehicle crashes cost $11,490,000 per death when including all crash types. New drivers who choose minimum coverage face devastating financial exposure that can destroy their future income potential.

Full Coverage Protects Your Financial Future

Full coverage with comprehensive and collision protection costs new drivers an additional $200-400 monthly but prevents catastrophic losses. Comprehensive coverage handles theft, vandalism, and weather damage while collision pays for accident repairs regardless of fault. New drivers who operate financed or leased vehicles must carry full coverage anyway, which makes the decision automatic.

Even drivers with older paid-off vehicles benefit from collision coverage when repair costs exceed $3,000-5,000. This happens frequently with modern vehicle complexity and parts costs that continue to rise across all vehicle categories.

Strategic Deductible Choices Slash Monthly Premiums

Higher deductibles reduce monthly premiums by 15-30% but require careful financial planning. New drivers should choose the highest deductible they can afford to pay immediately in case of an accident. A $1,000 deductible instead of $250 typically saves $600-1,200 annually in premium costs (depending on coverage levels and location).

Smart new drivers set aside their deductible amount in a separate savings account and treat it as part of their insurance strategy. This approach works particularly well for drivers with emergency funds who want to minimize their monthly insurance expenses while they maintain comprehensive protection.

Essential Coverage Types New Drivers Need

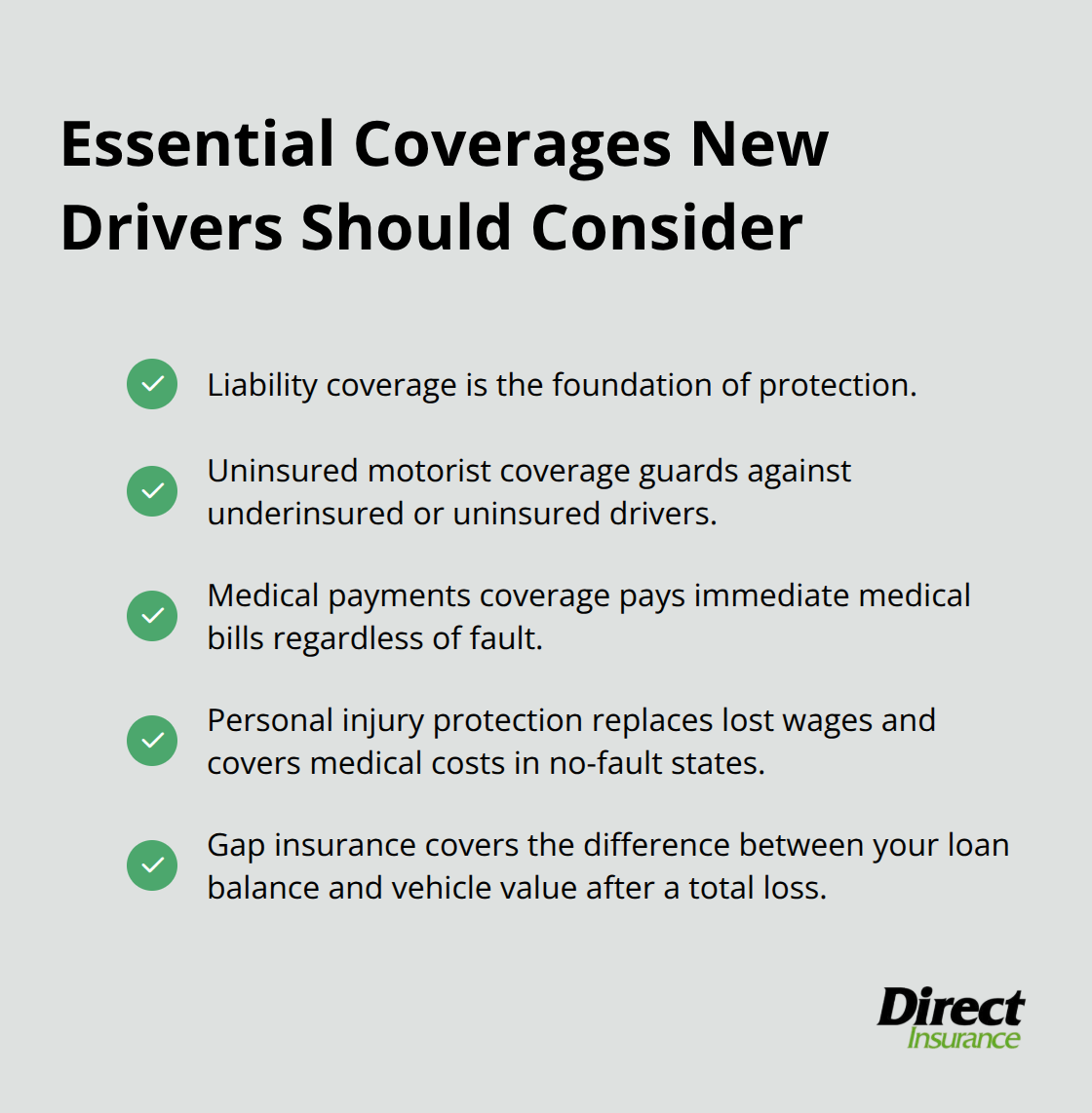

Liability coverage forms the foundation but falls short of complete protection. Uninsured motorist coverage protects against drivers who carry no insurance or insufficient limits. Medical payments coverage handles immediate medical expenses regardless of fault, which proves valuable when health insurance has high deductibles.

Personal injury protection (available in no-fault states) covers lost wages and medical expenses beyond basic liability limits. Gap insurance becomes essential for drivers with auto loans, as it covers the difference between what you owe and what your car is worth after total loss accidents.

Final Thoughts

New drivers must compare quotes from at least five insurers to secure low cost auto insurance for new drivers, as rates differ dramatically between companies. USAA charges $1,292 annually while Geico offers identical coverage for $1,420, which proves comparison shopping saves hundreds each year. Smart drivers review their policies every six months to capture new discounts and adjust coverage as their experience grows.

Insurance companies reassess rates annually, and premiums drop as drivers gain experience and maintain clean records. Your coverage needs change as you build credit history and accumulate safe miles behind the wheel. Independent agents provide access to multiple carriers without the limitations of captive agents who represent single companies.

We at Direct Insurance Services connect new drivers with top-rated carriers that offer competitive rates and comprehensive coverage options. Our team helps Utah families navigate complex insurance decisions while securing protection that adapts to their changing circumstances. Quality auto insurance becomes accessible when you combine smart coverage choices with professional guidance from Direct Insurance Services.