Home Insurance Flood Coverage: Protecting Your Home From Sudden Floods

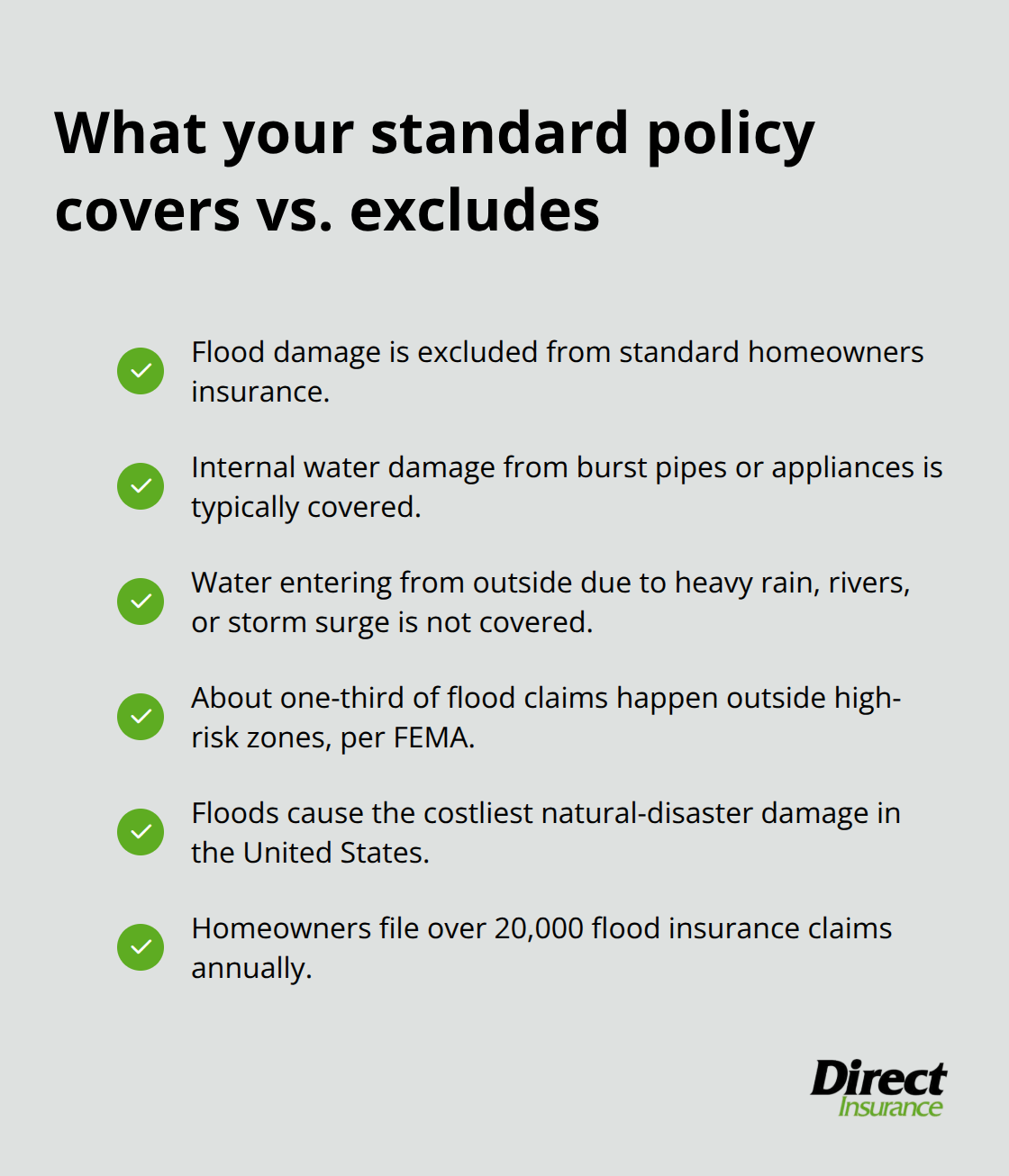

Floods cause more property damage than any other natural disaster in the United States, with homeowners filing over 20,000 flood insurance claims annually. Standard homeowners insurance policies don’t cover flood damage, leaving most property owners exposed to significant financial risk.

At Direct Insurance Services, we help Utah homeowners understand why home insurance flood coverage requires a separate policy and how to protect their properties effectively. This guide walks you through what’s covered, how to assess your risk, and the steps to add flood protection to your insurance plan.

What Your Standard Policy Actually Covers

The Flood Coverage Gap in Standard Homeowners Insurance

Your standard homeowners insurance policy has a significant blind spot: it completely excludes flood damage. This isn’t a minor limitation or something buried in fine print-it’s a fundamental exclusion that applies regardless of whether you live in a flood zone or not. According to FEMA, about one-third of flood insurance claims occur outside designated high-risk areas, which means countless homeowners think they’re protected when they’re actually exposed.

Standard policies cover water damage from burst pipes, appliance malfunctions, or roof leaks caused by storms, but the moment water comes from outside your home due to heavy rain, overflowing rivers, or storm surge, your coverage stops. This distinction matters enormously because flood damage represents the costliest natural disaster in the United States, with homeowners filing over 20,000 flood insurance claims annually. A single flooding event can result in tens of thousands of dollars in repairs that your standard policy won’t touch.

Why Insurance Companies Exclude Flood Risk

Insurance companies exclude flood coverage because flood risk is unpredictable, widespread, and catastrophically expensive. Unlike fire or theft, which affect individual properties sporadically, flooding can damage thousands of homes simultaneously in a single weather event. Standard homeowners policies are structured around manageable risk levels-companies cannot profitably insure against events that could simultaneously impact entire neighborhoods or regions. This is why the federal government stepped in to create the National Flood Insurance Program, which FEMA administers through about 47 private insurers. The NFIP now provides nearly $1.3 trillion in flood coverage to approximately 4.7 million policyholders nationwide, making it the largest single-line insurance program in the United States.

What This Means for Your Mortgage and Your Home

If you have a mortgage in a high-risk flood zone, your lender will require you to purchase flood insurance separately before approving your loan. This requirement protects both you and the lender from catastrophic financial loss. Understanding this gap between what your standard policy covers and what it doesn’t is the first step toward comprehensive protection. The next section explores how to assess whether your property faces flood risk and what coverage options exist to fill this critical protection gap.

Know Your Flood Risk Before It’s Too Late

Check Your Flood Zone, But Look Beyond the Map

Your property’s flood risk extends far beyond what official flood zone designations reveal. FEMA publishes flood maps that identify Special Flood Hazard Areas-the highest-risk zones where lenders mandate flood insurance for mortgaged properties. However, FEMA data shows that roughly one-third of all flood insurance claims occur outside these designated high-risk areas. This gap between official risk zones and actual flood damage means living in a low-risk zone provides no guarantee of safety.

Start by checking your property’s flood zone using FEMA’s flood map tool, but treat this as your starting point, not your final answer. Contact your local city or county planning department to access historical flooding records in your area. These records reveal patterns that FEMA maps don’t always capture, including flooding from heavy rainfall, overflowing storm drains, and localized drainage problems that affect properties well outside official flood zones.

Evaluate Your Property’s Specific Vulnerability Factors

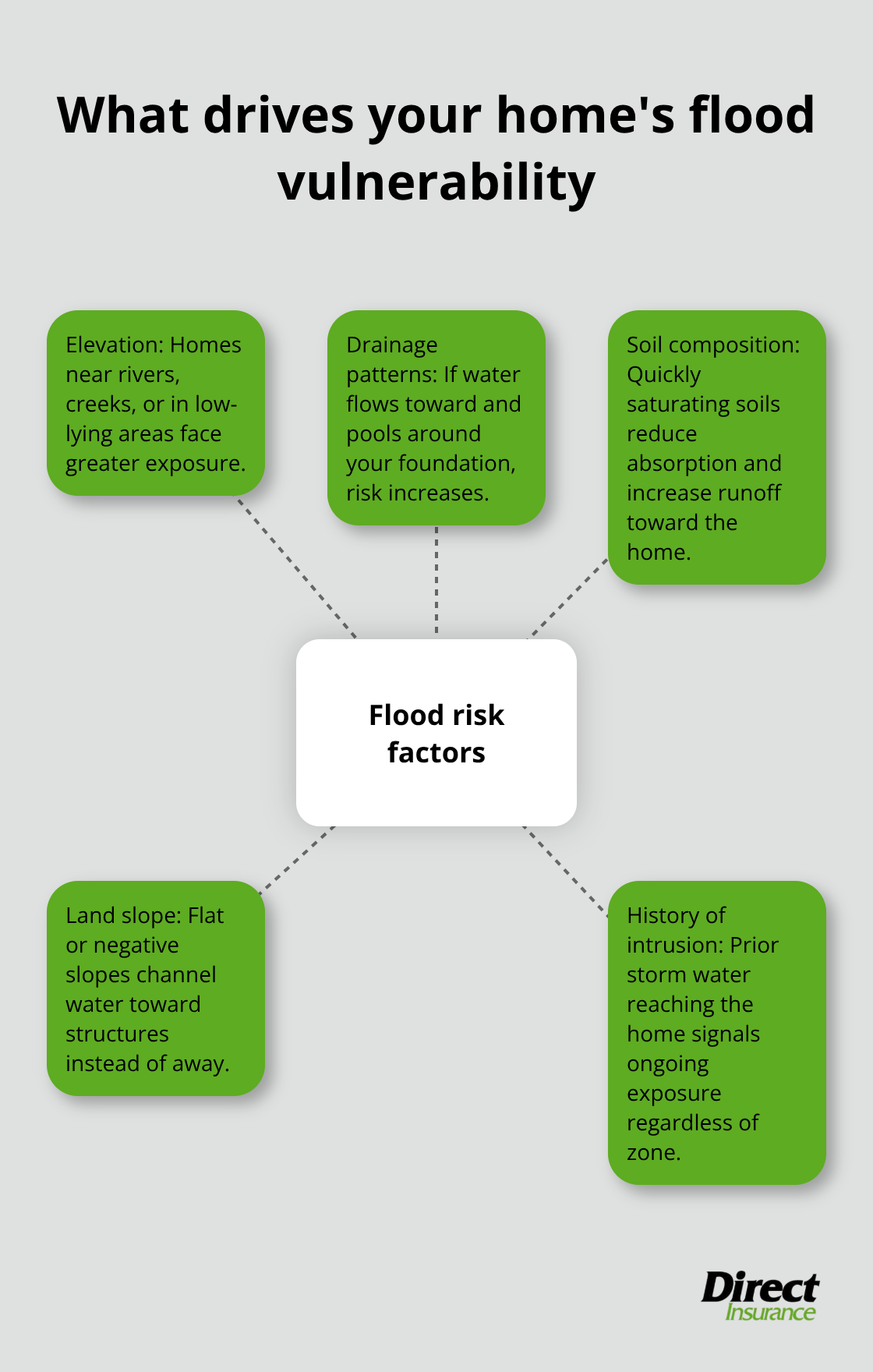

Your home’s actual flood exposure depends on multiple physical characteristics that determine how water moves across and around your property. Elevation relative to nearby water sources matters significantly-properties near rivers, creeks, or in low-lying areas face substantially higher risk. Local drainage patterns determine whether water flows away from your foundation or pools around it. Soil composition affects how quickly water saturates the ground, and the steepness of the land slope away from your foundation influences whether water drains naturally or accumulates.

If your property has experienced water intrusion during heavy storms, flood insurance isn’t optional regardless of what your flood zone designation says. These past incidents indicate that your home sits in a location where water reaches it during significant precipitation events. The combination of proximity to water sources, poor drainage, and historical water problems creates genuine flood exposure that standard homeowners insurance won’t cover.

How Extreme Weather Patterns Increase Your Risk

Climate patterns are making flood risk worse across Utah and the nation. Extreme precipitation events have increased significantly over recent decades, with the intensity of heavy rainfall now exceeding historical norms that older drainage systems were designed to handle. Infrastructure built decades ago cannot manage today’s storm intensity, leaving communities vulnerable even in areas that rarely flooded before.

This shift means that historical flood data becomes less reliable for predicting future risk. A neighborhood that experienced minimal flooding over the past fifty years may face substantial exposure under current weather patterns. Your assessment of flood risk must account for this changing reality rather than relying solely on outdated historical information.

Take Action to Assess Your Actual Exposure

Your best action is to assess your specific property risk by consulting with an insurance professional who understands local conditions rather than relying solely on flood zone maps. An experienced agent can evaluate how your home’s location, elevation, drainage characteristics, and local infrastructure interact to create actual flood exposure. This assessment gives you the information needed to determine whether flood insurance makes financial sense for your situation and what coverage limits appropriately protect your investment.

Getting this evaluation done now, before a flooding event occurs, gives you time to secure coverage and implement mitigation measures that can reduce both your risk and your insurance costs. With your flood risk clearly understood, the next step involves exploring how to add flood coverage to your insurance protection and what policy options exist to fill the gap that standard homeowners insurance leaves open.

How to Add Flood Coverage to Your Home Insurance

Understanding NFIP Policies and How They Work

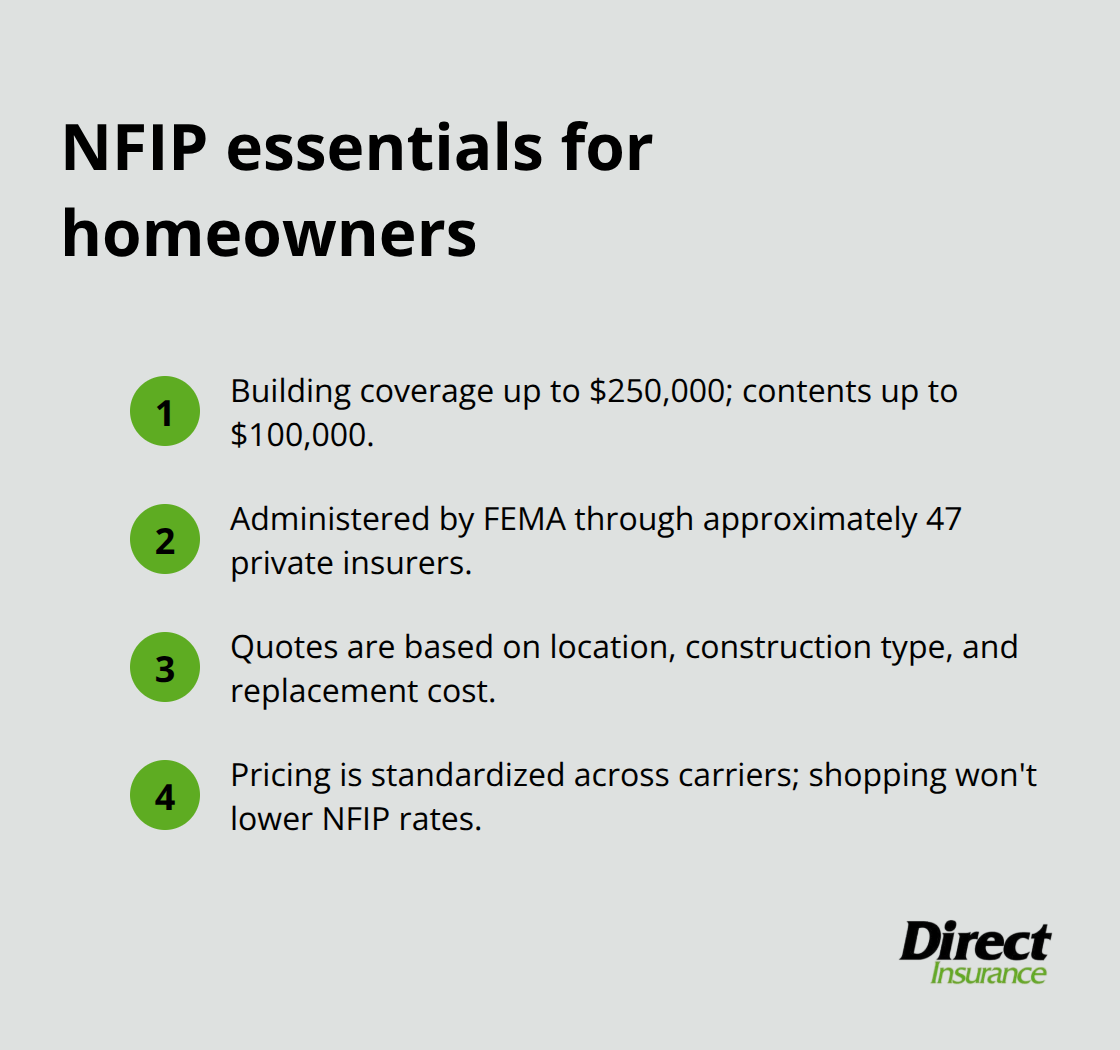

Flood insurance through the National Flood Insurance Program operates differently from standard homeowners coverage, and understanding how to purchase it prevents costly delays. The NFIP, administered by FEMA and delivered through approximately 47 private insurers, covers buildings up to $250,000 and contents up to $100,000 for homeowners. When you contact an agent to purchase an NFIP policy, you’ll receive a personalized quote based on your property’s specific location, construction type, and replacement cost. The NFIP uses standardized pricing across all carriers, meaning you won’t find lower rates by shopping between insurers-all partners use identical pricing formulas.

The 30-Day Waiting Period and Coverage Activation

A critical detail changes everything: NFIP policies typically include a 30-day waiting period before coverage activates. This waiting period disappears only in specific situations, such as when a mortgage lender mandates the policy or when your property enters a newly designated high-risk flood zone. If you need immediate coverage, some private flood insurers and surplus-line carriers can start protection sooner, though their premiums may differ from NFIP rates. Getting your policy in place well before severe weather season matters enormously because that 30-day gap leaves you completely unprotected if flooding occurs before your coverage begins.

Selecting Deductibles and Coverage Limits That Match Your Needs

Your deductible selection and coverage limits directly determine how much protection your flood policy actually provides when water damage strikes. Most NFIP policies offer deductible options starting at $1,000, $2,000, $5,000, or higher-choosing a higher deductible reduces your premium but increases your out-of-pocket costs when you file a claim. Building coverage protects your home’s structure including electrical systems, plumbing, furnaces, water heaters, and permanently installed carpeting, while contents coverage protects movable property like furniture, clothing, and electronics.

Many homeowners underestimate how much contents coverage they actually need; a detailed home inventory revealing the replacement cost of your belongings often surprises people who initially thought lower limits would suffice. If standard NFIP limits feel insufficient for your property’s replacement value, excess flood coverage through private insurers can supplement NFIP protection and reach higher limits.

Comparing Your Coverage Options

An experienced agent can help you evaluate whether your current coverage limits match your actual exposure and recommend appropriate deductibles based on your financial situation and risk tolerance. Direct Insurance Services can guide you through these decisions by comparing what NFIP policies offer against private flood insurance options available in Utah, ensuring you understand exactly what protection you’re purchasing and what gaps might remain.

Final Thoughts

Flood damage represents a genuine financial threat to Utah homeowners, and standard homeowners insurance simply won’t protect you when water strikes. The gap between what your policy covers and what actually happens during a flooding event can cost tens of thousands of dollars in repairs and replacements. Home insurance flood coverage through the National Flood Insurance Program fills this protection gap, offering building coverage up to $250,000 and contents coverage up to $100,000 at standardized rates across all carriers.

Your next step is straightforward: assess your actual flood risk by reviewing FEMA flood maps, checking local flooding history, and evaluating your property’s specific vulnerability factors. Then contact an insurance professional to discuss whether flood insurance makes sense for your situation and what coverage limits appropriately protect your home and belongings. Getting this done before severe weather season arrives matters enormously because NFIP policies include a 30-day waiting period before coverage activates.

We at Direct Insurance Services understand Utah’s unique flood risks and can guide you through the process of adding flood coverage to your insurance protection. We work with top-rated carriers to help you compare NFIP policies against private flood insurance options, ensuring you understand exactly what protection you’re purchasing. Contact Direct Insurance Services today to discuss your flood coverage options and take control of your home’s protection.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation