Is Landlord Insurance Cheaper Than Homeowners Coverage?

At Direct Insurance Services, we often get asked: Is landlord insurance cheaper than homeowners coverage? It’s a common question for property owners considering renting out their homes.

The answer isn’t always straightforward, as several factors influence the cost of both types of insurance. In this post, we’ll break down the key differences between landlord and homeowners insurance, and explore the various elements that affect their pricing.

What Is Landlord Insurance?

Property Protection and Liability Coverage

Landlord insurance protects property owners who rent out their homes, apartments, or commercial spaces. This specialized insurance includes two main components: property protection and liability coverage. Property protection safeguards the physical structure of your rental against damages from fire, storms, or vandalism. Liability coverage protects you if a tenant or visitor sustains an injury on your property due to your negligence.

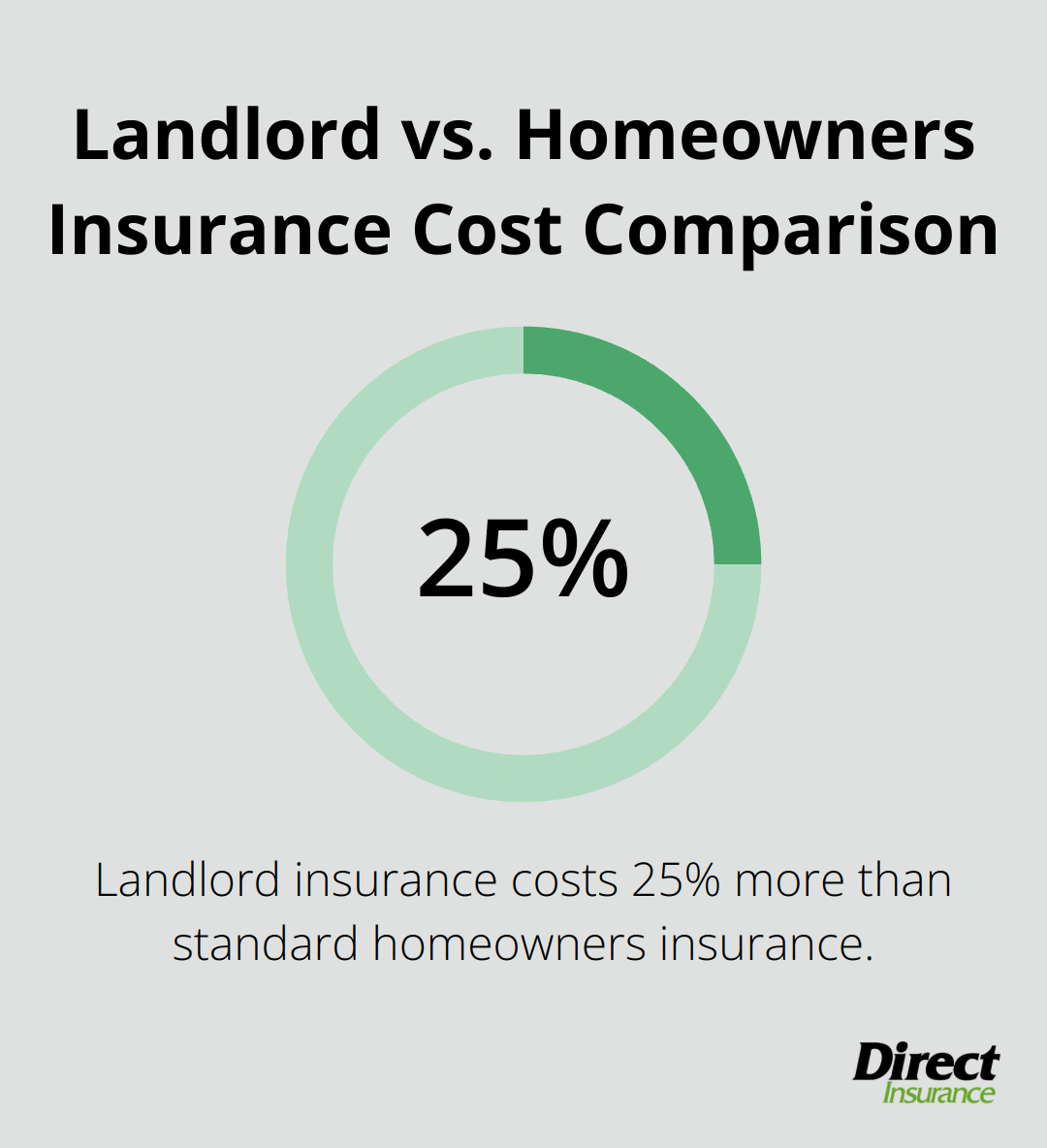

Landlord policies generally cost about 25 percent more than a standard homeowners policy to pay for increased protections. This higher cost reflects the increased risks associated with rental properties (such as more frequent claims and potential property damage from tenants).

Additional Coverages for Landlords

Landlord insurance offers coverage options not found in typical homeowners policies. Loss of rental income protection can provide financial security if your property becomes uninhabitable due to a covered event. This feature ensures you continue to receive rental income while repairs take place.

Many landlord policies also cover tenant-caused damage, which homeowners insurance typically excludes. The National Association of Realtors reports an increase in rental property ownership in recent years, which highlights the importance of these additional protections.

Key Differences from Homeowners Insurance

Landlord and homeowners insurance both protect property, but significant differences exist. Homeowners insurance covers personal belongings and provides additional living expenses if you must leave your home. Landlord insurance focuses on the structure and potential liability issues related to tenants.

Homeowners insurance may become void if you rent out your property without informing your insurer. This fact underscores the importance of obtaining the right type of coverage for your specific situation.

Importance of Regular Policy Reviews

Landlords should review their policies regularly to ensure adequate coverage. As the rental market evolves and property values change, your insurance needs may shift. A proactive approach helps protect your investment and minimizes potential financial risks associated with being a landlord.

The next chapter will explore the various factors that affect insurance costs for both landlord and homeowners policies. Understanding these elements will help you make informed decisions about your coverage needs.

What Impacts Insurance Costs?

At Direct Insurance Services, we understand that various factors influence the cost of both landlord and homeowners insurance. Let’s explore the key elements that affect your premiums.

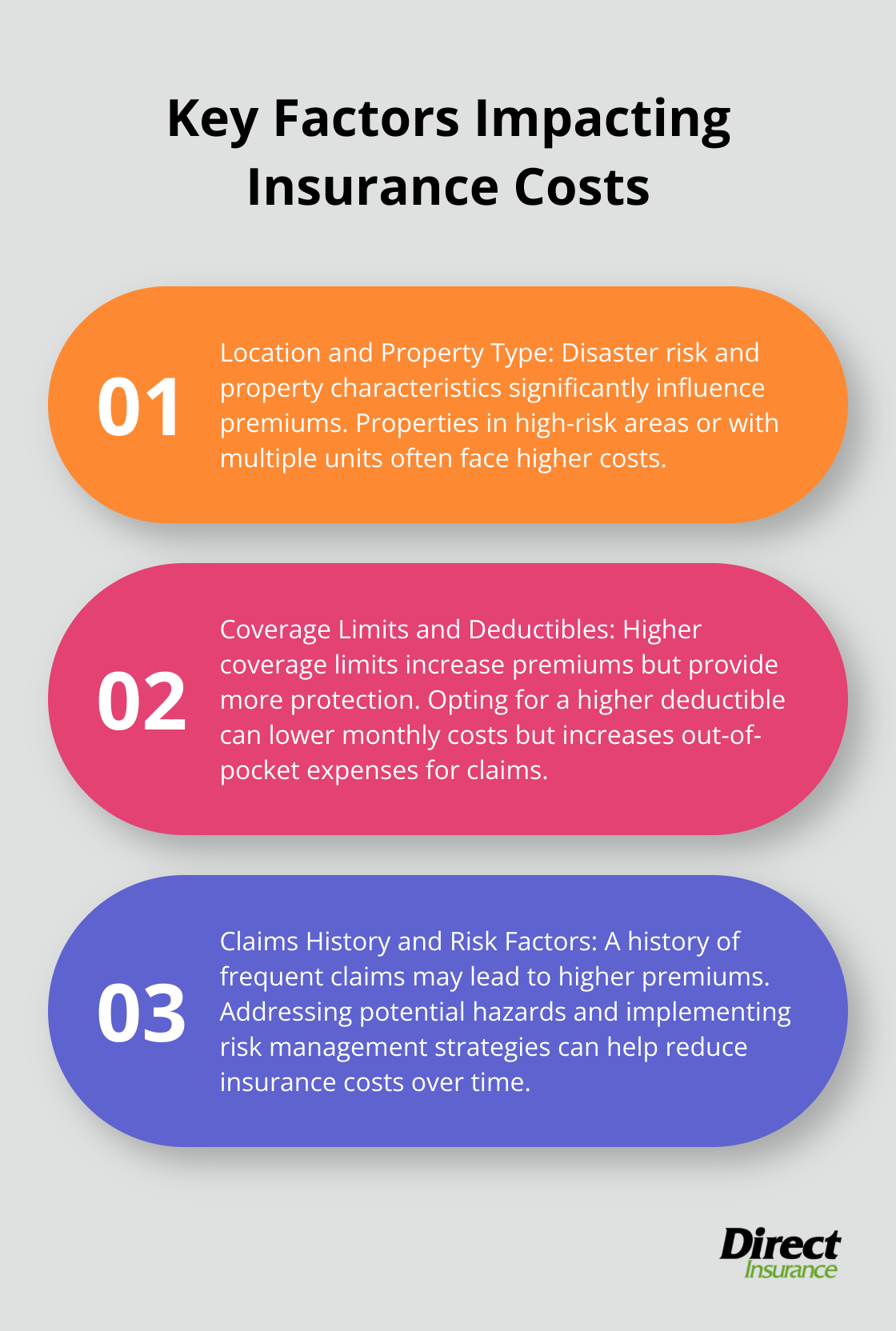

Location and Property Type

Your property’s location significantly impacts insurance costs. Disaster risk and premiums have become more strongly correlated over time, with premiums being higher in riskier locations. For example, a rental property in a flood-prone area may require additional flood insurance, increasing overall costs.

The type of property also plays a key role. Multi-unit buildings often have higher premiums than single-family homes due to increased risks and potential for multiple claims. Older properties may face higher costs due to outdated systems or materials that pose greater risks.

Rental Income and Occupancy

For landlords, rental income and occupancy rates can affect insurance costs. Properties with higher rental incomes may require more coverage, potentially leading to higher premiums. However, consistently high occupancy rates might demonstrate stability to insurers, possibly resulting in more favorable rates.

Seasonal rentals or properties with frequent tenant turnover may face higher premiums due to increased risks associated with vacant periods and changing occupants.

Coverage Limits and Deductibles

The coverage limits you choose directly impact your premiums. Higher limits provide more protection but come with increased costs. It’s important to balance adequate coverage with affordable premiums.

Deductibles also play a significant role. Opting for a higher deductible can lower your monthly premiums, but it means you’ll pay more out-of-pocket if you need to file a claim. Try to find the right balance for your financial situation.

Claims History and Risk Factors

Your claims history is a critical factor in determining insurance costs. A history of frequent claims may lead to higher premiums (or even difficulty obtaining coverage). Maintaining your property well and addressing potential hazards can help minimize claims and keep costs down.

Risk factors specific to your property, such as outdated electrical systems or the presence of attractive nuisances like swimming pools, can increase premiums. Addressing these factors through renovations or additional safety measures may help reduce insurance costs over time.

The Insurance Information Institute reports that implementing effective risk management strategies can lead to significant savings on insurance premiums. This might include installing security systems, updating old plumbing or electrical systems, or reinforcing your property against natural disasters common in your area.

Now that we’ve covered the factors that impact insurance costs, let’s compare the specific costs between landlord and homeowners insurance policies in the next section.

How Much More Does Landlord Insurance Cost?

At Direct Insurance Services, we have observed that landlord insurance typically costs more than homeowners insurance. The average homeowners insurance premium rose by 7.6 percent in 2021 from 2020, according to a December 2023 study by the National Association of Insurance. This price difference reflects the increased risks associated with rental properties.

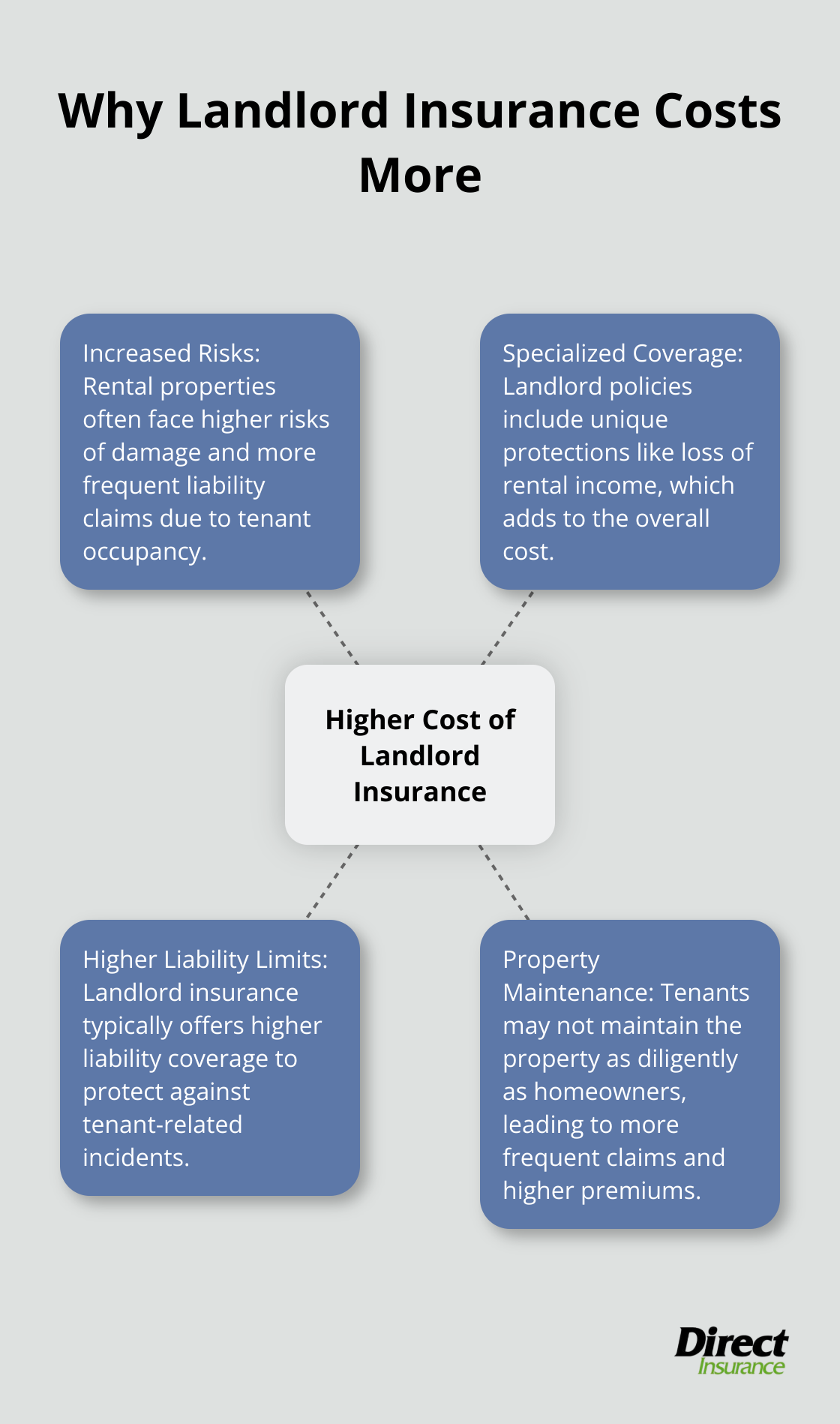

Higher Risks, Higher Premiums

Landlord insurance costs more due to several factors. Rental properties often face higher risks of damage and liability claims. Tenants may not maintain the property as diligently as homeowners, which leads to more frequent claims. Additionally, landlord policies usually offer higher liability limits to protect against tenant-related incidents.

Specialized Coverage Increases Costs

Landlord policies include coverages not found in standard homeowners insurance. Loss of rental income protection serves as a prime example. This coverage ensures you don’t lose income if your property becomes uninhabitable due to a covered event. While this adds to the policy cost, it provides essential financial protection for landlords.

Long-Term Financial Benefits

While landlord insurance costs more upfront, it often proves more cost-effective in the long run. The specialized coverage can save property owners from significant out-of-pocket expenses in the event of major property damage or liability claims. For instance, if a tenant’s guest sustains an injury on your property, the higher liability limits in a landlord policy could prevent a financially devastating lawsuit.

Tax Advantages for Property Owners

One advantage of landlord insurance is its tax-deductible status. Unlike homeowners insurance premiums, landlord insurance premiums typically qualify as a business expense (always consult with a tax professional to understand how this applies to your specific situation). This deduction can help offset the higher cost of coverage.

The National Association of Realtors notes that rental property ownership has increased in recent years. This trend underscores the importance of proper insurance coverage for landlords. The comprehensive protection offered by landlord insurance proves essential for protecting your investment and financial well-being, despite the higher cost.

Final Thoughts

Landlord insurance typically costs more than homeowners insurance due to the unique risks associated with rental properties. This increased cost reflects specialized coverage, such as loss of rental income and higher liability limits. Property owners must weigh these additional expenses against the comprehensive protection and potential tax benefits landlord insurance offers.

We at Direct Insurance Services understand the complexities of insurance for both homeowners and landlords. Our team of experienced professionals can help you navigate your options and find the right coverage to protect your property and financial interests. We provide personalized guidance and support tailored to your unique needs.

For expert advice on whether landlord insurance is cheaper than homeowners coverage for your specific situation, contact us today. Our team will work with you to ensure you have the appropriate coverage to safeguard your investment and financial well-being. Don’t leave your property’s protection to chance – let us help you make an informed decision.