An empty house sits differently than an occupied one. Pipes freeze, roofs leak, and security becomes a real concern-yet standard homeowners insurance often won’t cover these risks.

Vacant home insurance fills that gap. At Direct Insurance Services, we help Utah property owners protect investment homes, seasonal properties, and houses between tenants with coverage designed specifically for empty buildings.

What Vacant Home Insurance Actually Covers

Vacant home insurance protects the structure and liability exposure of a property sitting empty for extended periods. Standard homeowners policies typically include a vacancy clause that voids or severely limits coverage after 30 to 60 days of non-occupancy. The National Association of Insurance Commissioners defines vacancy as unoccupied for 60 or more days-the threshold where most insurers stop covering fire, theft, vandalism, and water damage. This gap exists because empty properties face higher risk: pipes burst without heat, squatters move in, and fires spread unchecked without early detection.

Core Coverage Types

Vacant home insurance fills this void with several key protections. Fire and smoke damage coverage protects against structural loss from flames or smoke. Weather-related losses like wind and hail damage are included, along with theft and vandalism protection. Water intrusion from burst pipes or failed systems receives coverage, and personal liability protection applies if someone is injured on the property. The coverage you select depends on the property’s condition and how long it will sit empty. A basic form typically includes vandalism protection, while a special form offers broader coverage but requires the structure to be under 40 years old or fully gutted and renovated within the past 30 years. If you add an active central alarm system monitoring for fire and burglary, you can extend theft coverage to the special form.

Multi-Property and Liability Options

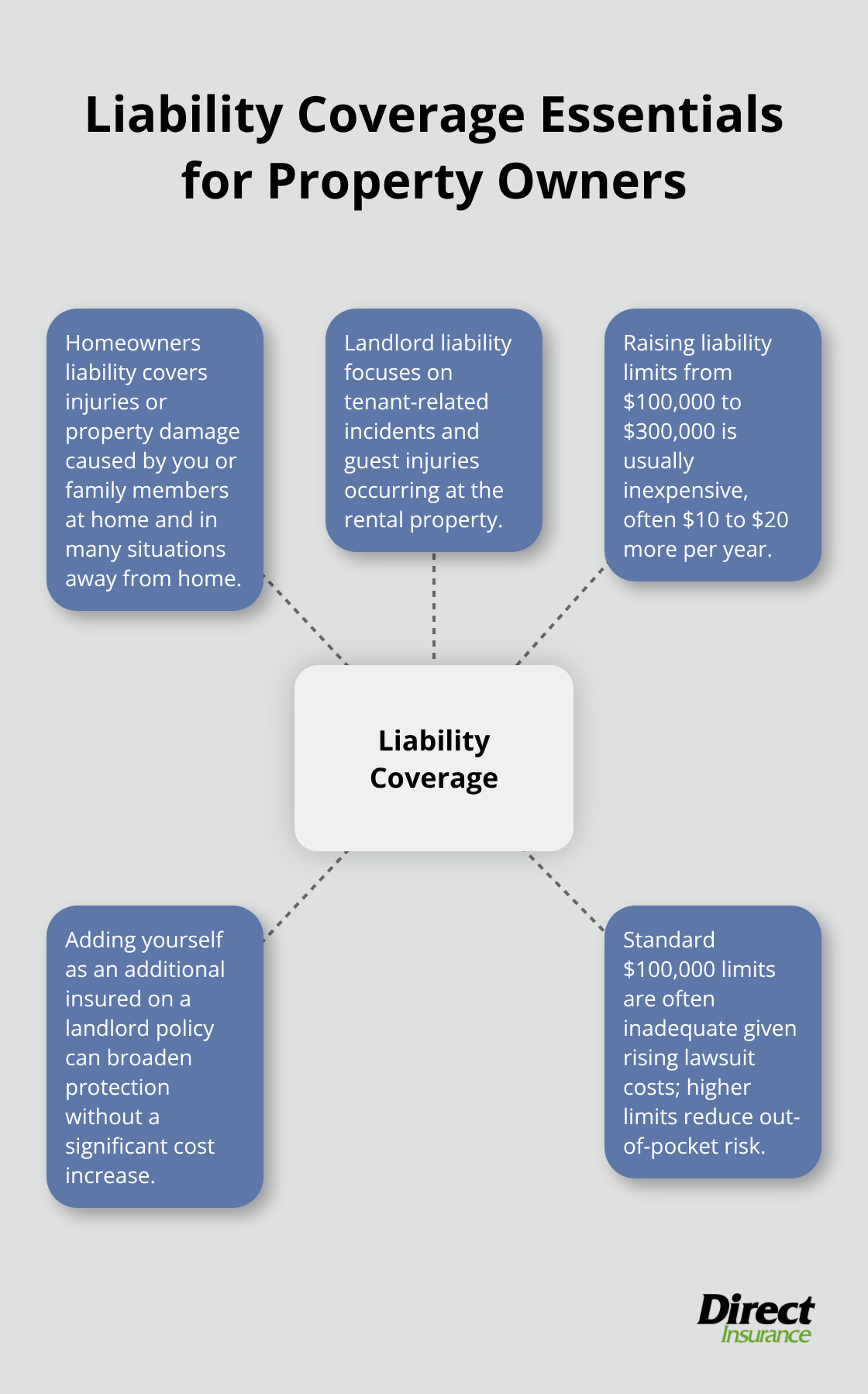

Some policies allow you to insure multiple vacant properties on one policy with limits up to 5 million dollars in total property coverage and up to 1 million in general liability. This approach simplifies administration for investors managing several properties at once. Liability coverage becomes especially important when vacant homes sit on properties with hazards-ponds, pools, or trampolines may disqualify a property from coverage or require additional underwriting review.

Who Actually Needs This Coverage

Landlords between tenants, homeowners selling after moving out, and house flippers are the primary buyers of vacant home insurance in Utah. If you own a seasonal property left empty for months, or if you inherited a home and need time to decide what to do with it, you need this coverage. Properties under renovation where you won’t sleep on-site fall into this category too.

Many insurers consider on-site sleeping 3 to 4 nights per week as maintaining occupancy status, but regular daytime visits do not qualify as occupancy.

Premium Costs and What Drives Them

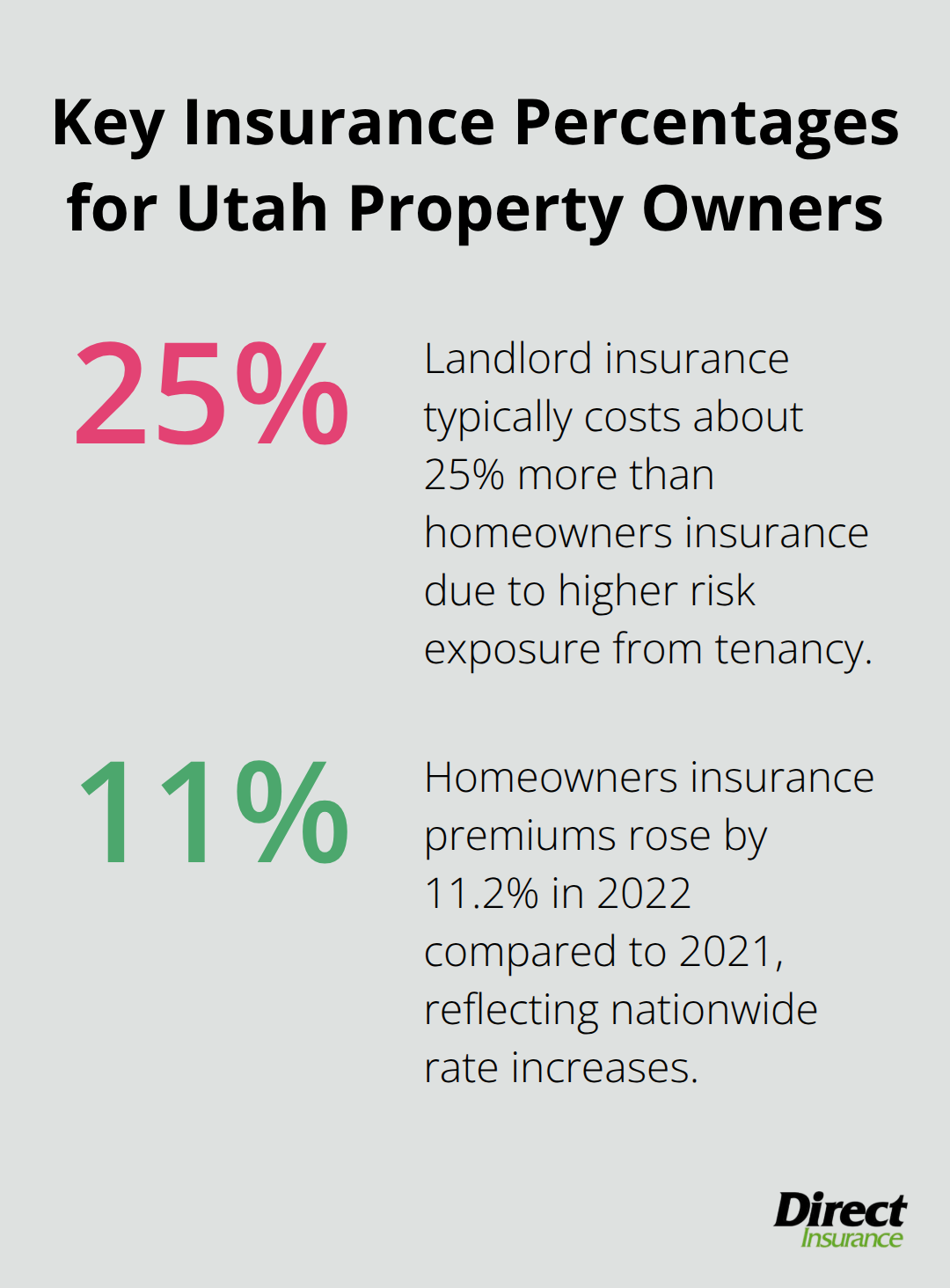

The cost difference matters significantly. Vacant home insurance typically runs 25 to 50 percent higher than standard homeowners insurance, with national average premiums around 3,410 dollars or more annually depending on location, property condition, and security measures. Location risk drives much of this cost-properties in high-crime areas or wildfire zones pay substantially more. Well-maintained properties with security upgrades like alarm systems, cameras, or smart water-leak sensors command lower premiums because they reduce loss exposure. Lenders often require vacant home insurance if you have a mortgage, and even without one, the protection is worth the expense given the financial exposure from potential theft, vandalism, or unattended water damage that could cost tens of thousands to repair.

Understanding what vacant home insurance covers helps you determine the right protection level for your situation. The next step involves comparing coverage options and finding the right policy for your specific property and timeline.

What Each Coverage Type Actually Protects

Vacant home insurance divides into distinct protection layers, and understanding what each covers matters more than the policy’s price tag. Property damage protection covers fire, smoke, lightning, wind, hail, and water damage from burst pipes or failed sprinkler systems-the exact perils that threaten empty houses. Theft and vandalism coverage applies when properties sit unattended, though basic forms automatically include vandalism while special forms require an active central alarm system monitoring for fire and burglary before theft protection activates. This distinction matters because a house under renovation without an alarm system cannot claim theft coverage on a special form policy, which means you either install monitoring or accept that risk.

Water Damage: The Silent Threat

Water damage stands out as the costliest exposure in vacant properties. Frozen pipes are one of the most common and costly causes of winter property damage, making this coverage non-negotiable for properties in freeze-prone climates where the thermostat cannot maintain 55 degrees Fahrenheit consistently. Properties in cold regions face particular risk because no one occupies the space to detect leaks early or respond to temperature drops. You must address this exposure directly when you select your policy limits and coverage options.

Liability Protection and Property Hazards

Liability coverage protects you when someone enters the vacant property and suffers an injury, though eligibility varies significantly by insurer and property hazards. Policies typically offer up to 1 million dollars in general liability coverage, but properties with hazards like pools, trampolines, ponds, or hot tubs face disqualification or stricter underwriting requirements because these features attract trespassers and increase injury risk. This creates a practical problem: if your vacant property has a pool, you must disclose it upfront and expect either denial or a substantially higher premium.

Additional Riders and Multi-Property Solutions

Additional riders address specific needs-you can add coverage for detached structures like garages or sheds, extend protection to personal property such as lawn equipment left on-site, or purchase endorsements that extend vacancy protection beyond standard timeframes. For investors managing multiple properties, multi-location policies consolidate coverage across several vacant buildings under one policy with limits up to 5 million dollars in total property coverage, reducing administrative overhead and simplifying claims management when issues arise across your portfolio. These options allow you to tailor protection to match your actual exposure rather than accept a one-size-fits-all approach.

The specific coverage you select depends on your property’s condition, location, and how long it will remain empty. Once you understand what protections exist, the next step involves identifying which coverage options make financial sense for your situation and how to find affordable rates in Utah’s insurance market.

Cost Factors and How to Find Affordable Vacant Home Insurance

Location Risk Sets Your Premium Foundation

Location risk determines your premium more than any other factor. Properties in high-crime areas or wildfire zones pay substantially more because theft, vandalism, and fire represent genuine exposure. A home in a flood-prone region will cost more to insure vacant than one on higher ground. Property condition matters equally-a well-maintained structure with a sound roof and functional heating system costs less to insure than a deteriorating building where pipes freeze easily or weather damage spreads rapidly.

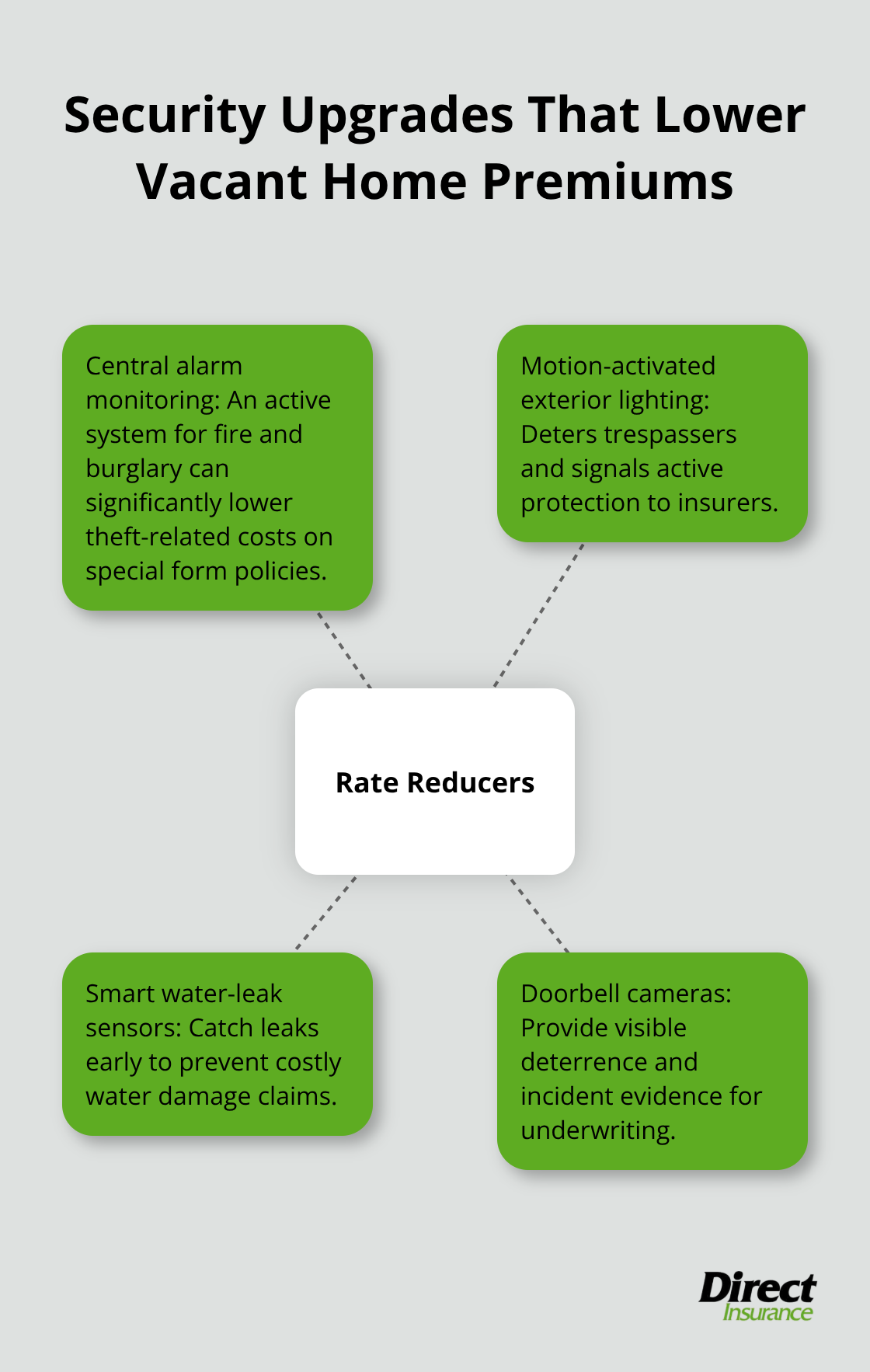

Security Measures Lower Your Rates

Security measures create the most direct path to lower premiums. An active central alarm system monitoring for fire and burglary reduces theft coverage costs significantly on special form policies. Motion-activated exterior lighting, smart water-leak sensors, and doorbell cameras signal active protection to insurers and can lower your rate by 10 to 20 percent. These upgrades work because they reduce loss exposure and demonstrate that you take property protection seriously.

Vacancy Duration and Policy Terms Affect Pricing

Vacancy duration affects pricing too-a property empty for three months costs less than one vacant for a year. The longer you expect the property to sit empty, the higher your annual premium climbs because exposure extends over a longer period. Request quotes for different policy terms (3-month, 6-month, and 12-month options) because shorter terms sometimes cost proportionally less if you only need temporary coverage while selling or renovating.

Shopping Strategy for Utah Homeowners

Utah homeowners shopping for vacant home insurance should start by contacting their current homeowners insurer about endorsements before purchasing a separate policy. Many carriers allow you to add vacancy coverage to your existing policy rather than purchase standalone protection, which often costs less and simplifies administration. When you contact insurers for quotes, specify whether the property is vacant, unoccupied, or under renovation-these distinctions affect underwriting and pricing.

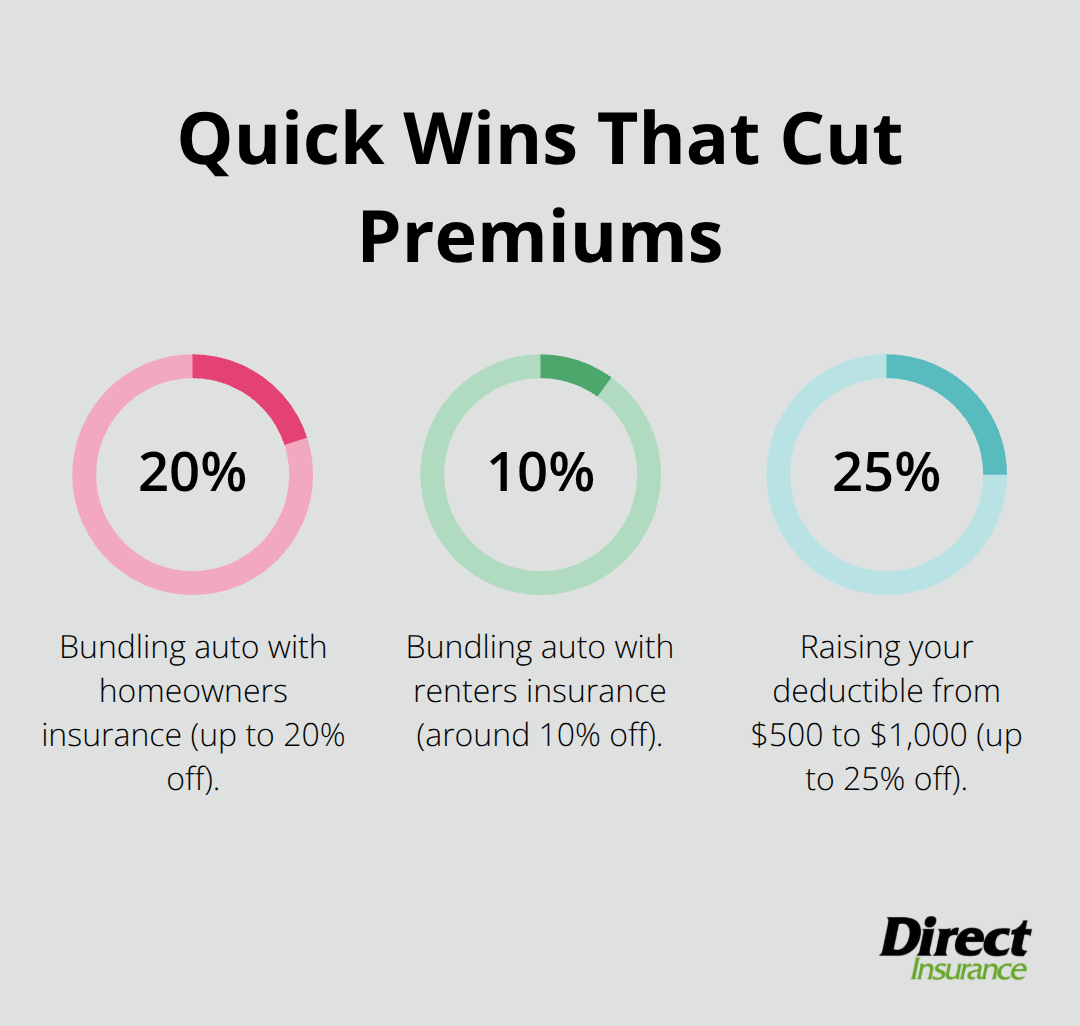

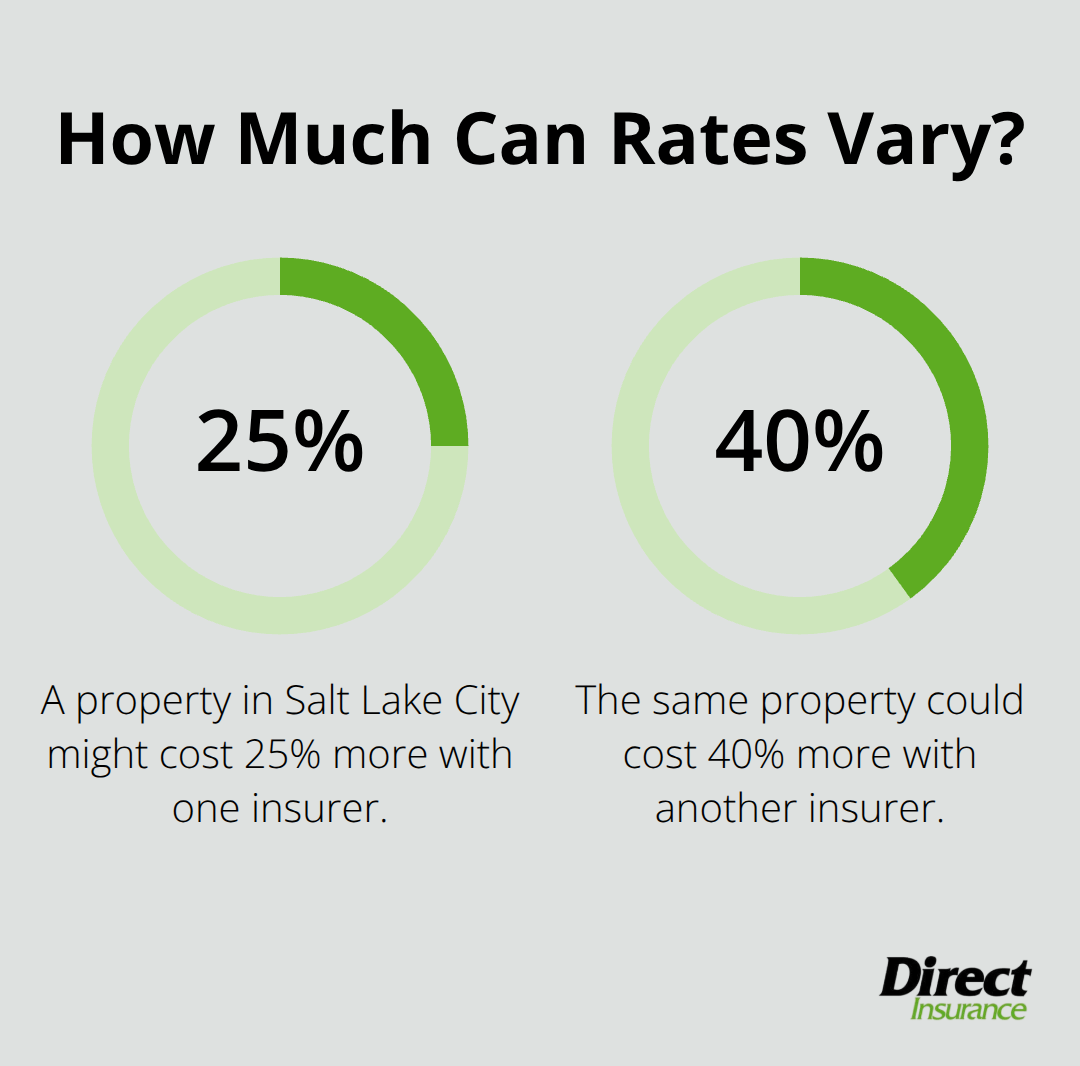

Compare at least three carriers because rates vary dramatically for identical coverage. A property in Salt Lake City might cost 25 percent more with one insurer and 40 percent more with another depending on how they weight local risk factors. Ask each insurer about discounts for multiple policies, paid-in-full annual premiums, and claims-free history.

Some carriers offer 10 to 15 percent discounts when you bundle vacant home coverage with auto or business insurance.

Review what each policy excludes because hazards like pools, hot tubs, or trampolines may disqualify your property entirely or require separate underwriting. Direct Insurance Services works with multiple carriers to match Utah properties with the right coverage at competitive rates, helping you avoid both gaps in protection and unnecessary expense.

Final Thoughts

Vacant home insurance protects your financial investment when a property sits empty for extended periods. Standard homeowners policies stop covering your structure after 30 to 60 days of vacancy, leaving you exposed to fire, theft, vandalism, water damage, and liability claims. A dedicated vacant home insurance policy fills that gap with coverage designed specifically for unoccupied properties, whether you’re selling, renovating, managing rental transitions, or holding a seasonal property.

The cost of vacant home insurance typically runs 25 to 50 percent higher than standard coverage, but this expense is justified by the real risks empty properties face. Location, property condition, and security measures directly influence your premium, meaning you can lower costs by installing alarm systems, motion-activated lighting, or water-leak sensors. Shopping multiple carriers matters because rates vary dramatically for identical coverage in Utah’s market, and requesting quotes for different policy terms sometimes reveals that a three-month policy costs proportionally less than annual coverage if you only need temporary protection.

Start by contacting your current homeowners insurer about adding a vacancy endorsement before purchasing a separate policy. When you request quotes, specify whether your property is vacant, unoccupied, or under renovation because these distinctions affect underwriting and pricing. Direct Insurance Services works with multiple carriers to match Utah properties with the right coverage at competitive rates and helps you avoid both gaps in protection and unnecessary expense.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation