What Is a Deductible in Auto Insurance Coverage?

Auto insurance deductibles directly impact how much you pay out-of-pocket when filing a claim. Understanding what is deductible in auto insurance helps you make informed coverage decisions.

At Direct Insurance Services, we see drivers struggle with choosing the right deductible amount. This guide breaks down everything you need to know about auto insurance deductibles and their role in your coverage.

What Is an Auto Insurance Deductible

An auto insurance deductible represents the specific dollar amount you pay out-of-pocket before your insurance company covers the remaining costs of a claim. According to the Insurance Information Institute, the countrywide average auto insurance expenditure increased 6.1 percent to $1,127 in 2022 from $1,062 in 2021. Your deductible applies each time you file a claim, not annually like health insurance deductibles.

Definition and Basic Concept

Auto insurance deductibles function as your financial responsibility threshold in the claims process. When damage occurs to your vehicle, you pay the deductible amount first, then your insurer handles the remaining costs. This system allows insurance companies to share risk with policyholders while keeping premium costs manageable. Most insurers offer deductible options from $250 to $2,500, though some provide amounts outside this range.

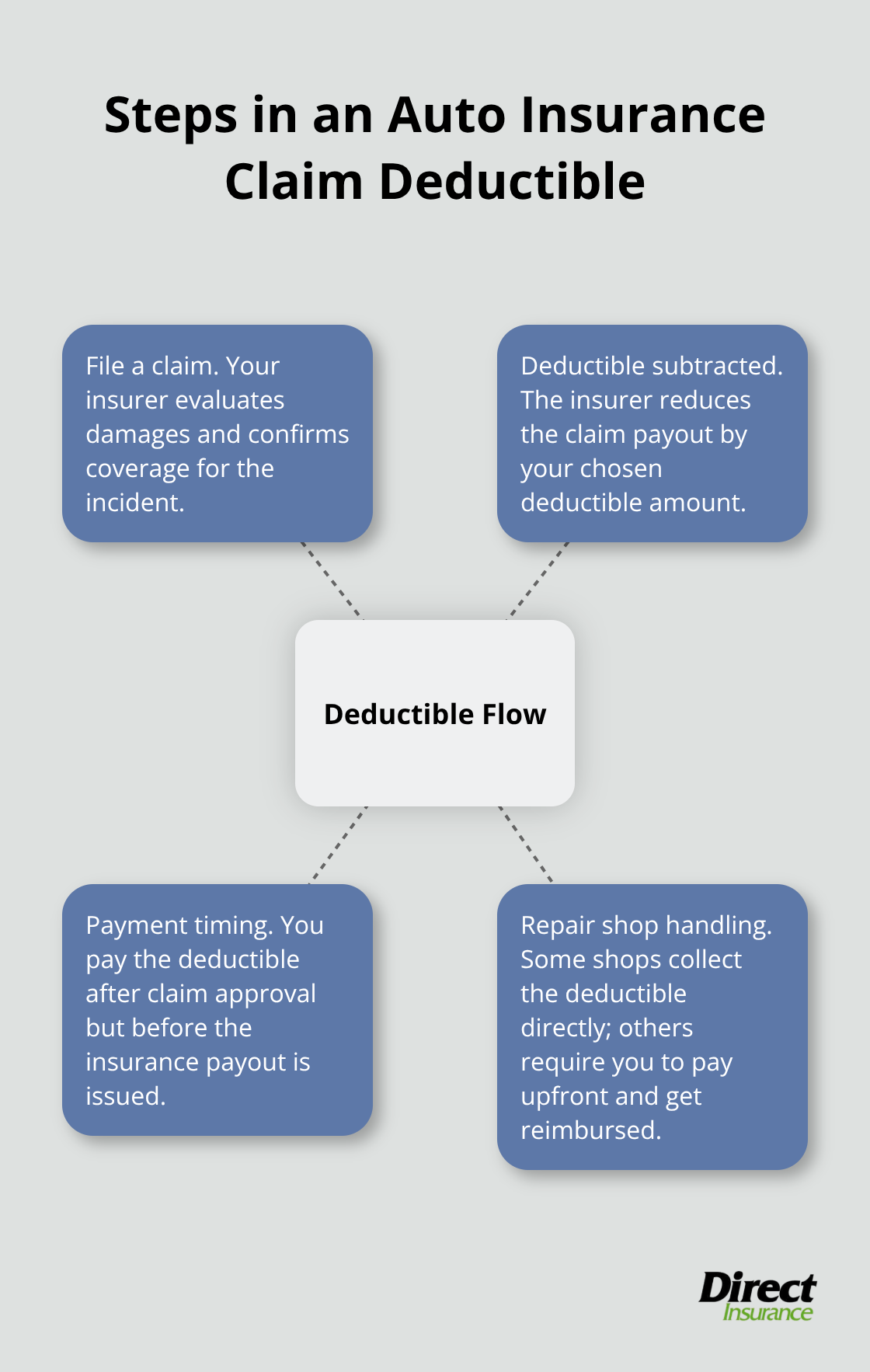

How Deductibles Work in Claims Process

When you file a claim, your insurer subtracts your deductible from the total repair cost before payment. If your car sustains $3,000 in damage and you carry a $500 deductible, your insurance company pays $2,500 while you cover the remaining $500. Payment timing matters: you must pay your deductible after claim approval but before your insurance payout arrives. Some repair shops collect the deductible directly, while others require upfront payment with later reimbursement.

Difference Between Deductible and Premium

Your deductible and premium serve opposite functions in your insurance policy. The premium represents your regular payment to maintain coverage, while the deductible becomes your financial responsibility during claims. Higher deductibles reduce monthly premiums by 10% to 20% (according to industry data) because you assume more financial risk. Lower deductibles increase premiums but reduce your out-of-pocket costs when accidents occur.

This relationship between deductibles and premiums leads directly to different types of coverage where deductibles apply, each with specific rules and considerations.

Types of Auto Insurance Deductibles

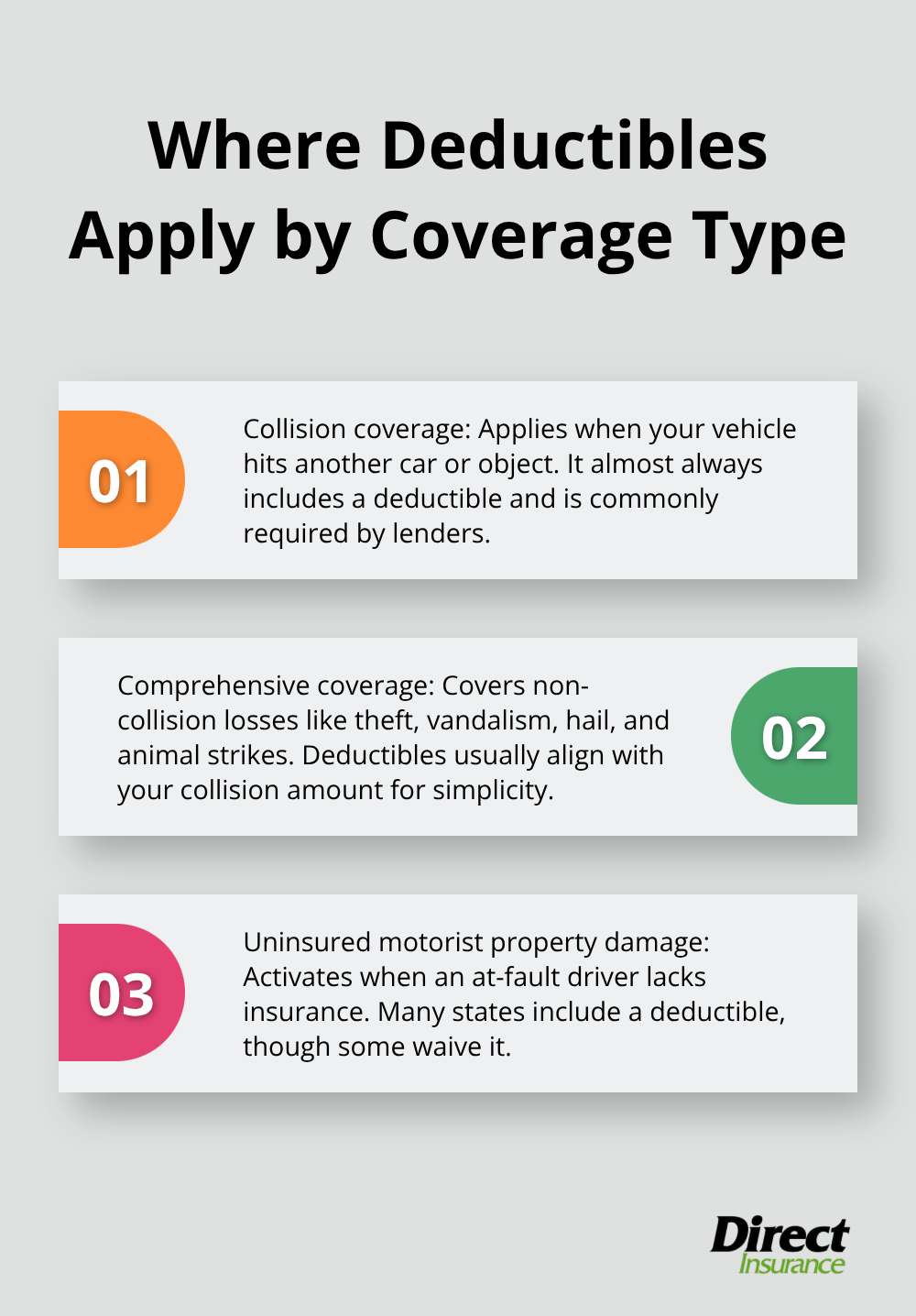

Not all auto insurance coverage types require deductibles, and you need to know which ones do to avoid unexpected out-of-pocket costs. Collision coverage protects your vehicle when accidents occur with other cars or objects, and this coverage always includes a deductible that typically ranges from $500 to $2,000. Comprehensive coverage handles non-collision incidents like theft, vandalism, hail damage, and animal strikes, with deductibles that usually match your collision amount for policy simplicity.

Collision Deductible Coverage

Collision deductibles apply every time your vehicle hits another car, guardrail, tree, or any stationary object. This coverage becomes mandatory when you finance or lease vehicles, with lenders typically requiring maximum $1,000 deductibles to protect their investment. Drivers with newer vehicles should stick closer to $500 to avoid large repair bills on expensive modern car technology.

Comprehensive Deductible Coverage

Comprehensive deductibles work differently than collision because incidents often involve total loss scenarios. Weather-related damage, theft, and vandalism claims frequently exceed vehicle values (which makes lower deductibles more valuable). States like Colorado and Texas see higher comprehensive claim frequencies due to hail storms, which makes $250 deductibles smart investments despite higher premiums.

Uninsured Motorist Property Damage Deductibles

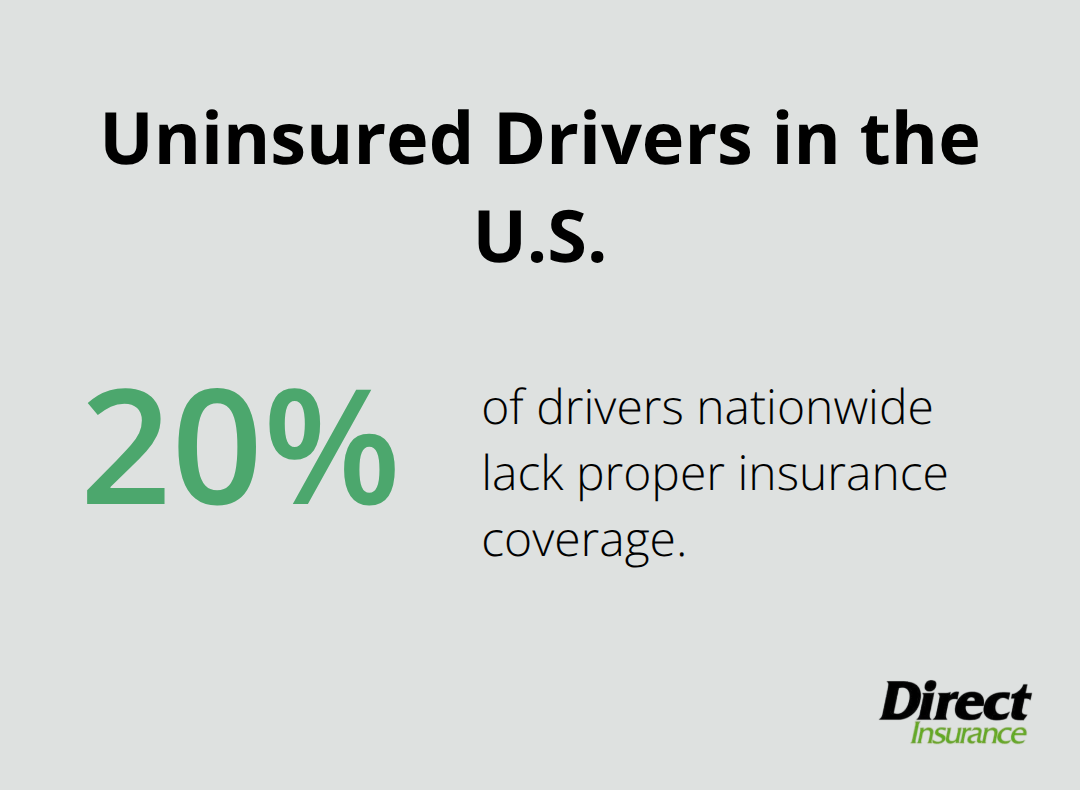

Uninsured motorist property damage coverage includes deductibles in most states, though some states waive this requirement entirely. This coverage activates when at-fault drivers lack insurance, and deductibles typically match your collision amount. Twenty percent of drivers nationwide lack proper insurance coverage, which makes this protection worthwhile despite the additional deductible exposure.

The specific deductible amounts you choose for these coverage types directly impact both your premium costs and financial exposure when claims occur.

How to Choose the Right Deductible Amount

Your deductible amount requires a calculated approach based on your financial situation and driving patterns. We at Direct Insurance Services recommend setting your deductible at the highest amount you can comfortably pay from your emergency savings without creating financial hardship. Most drivers select $500 deductibles because this amount strikes a reasonable balance between premium savings and out-of-pocket costs, but this one-size-fits-all approach often costs drivers money.

Factors to Consider When Setting Your Deductible

Your emergency fund size should directly dictate your maximum deductible amount. Financial advisors suggest keeping three to six months of expenses saved, and your deductible should never exceed 10 percent of this emergency fund. Drivers with $10,000 in savings can comfortably choose $1,000 deductibles and save $200 to $400 annually on premiums (according to Insurance Research Council data). Those with limited savings below $2,000 should stick with $250 to $500 deductibles to avoid financial strain during claims.

Impact of Deductible Amount on Premium Costs

Moving from a $500 to $1,000 deductible typically reduces premiums by 15 to 30 percent, while jumping to $2,000 can slash costs by 30 to 40 percent. However, these savings only benefit you if claims remain infrequent. Drivers who file claims every two to three years lose money with high deductibles despite lower premiums. Safe drivers with clean records for five years or more maximize savings with $1,500 to $2,000 deductibles.

Balancing Risk and Affordability

Your vehicle value also matters significantly: never select a deductible higher than 10 percent of your car’s current market value since total loss claims would leave you paying excessive amounts. Drivers with recent accidents should maintain lower amounts until their driving record improves (typically three to five years). Consider your daily commute distance and traffic conditions when making this decision, as higher-risk driving environments warrant lower deductibles for financial protection.

Final Thoughts

Auto insurance deductibles affect your premium costs and out-of-pocket expenses when you file claims. Smart deductible choices require honest assessment of your emergency savings, driving history, and risk tolerance. Drivers with substantial savings and clean records benefit from higher deductibles that reduce monthly premiums, while those with limited funds or frequent claims should prioritize lower deductibles for financial protection.

Your vehicle’s age and value also influence optimal deductible amounts, as older cars rarely justify high deductibles when repair costs approach the car’s worth. Regular policy reviews help maintain appropriate deductible levels as your financial situation and vehicle circumstances change over time. Understanding what is deductible in auto insurance empowers you to make financially sound coverage decisions that protect both your vehicle and your wallet.

We at Direct Insurance Services work with top-rated carriers to provide tailored auto insurance solutions that balance coverage needs with budget constraints (helping Utah families and businesses make confident insurance decisions). Our experienced team provides personalized guidance based on your unique situation. Contact us today to find the right deductible amount for your specific needs and circumstances.