Most landlords focus on protecting their property through their own insurance policies, but they often overlook a powerful ally: their tenants’ renters insurance.

How does renters insurance protect the landlord? It creates an additional layer of financial protection that can save property owners thousands in unexpected costs. We at Direct Insurance Services see landlords reduce their risk exposure significantly when tenants carry proper coverage.

What Property Damage Does Renters Insurance Actually Cover?

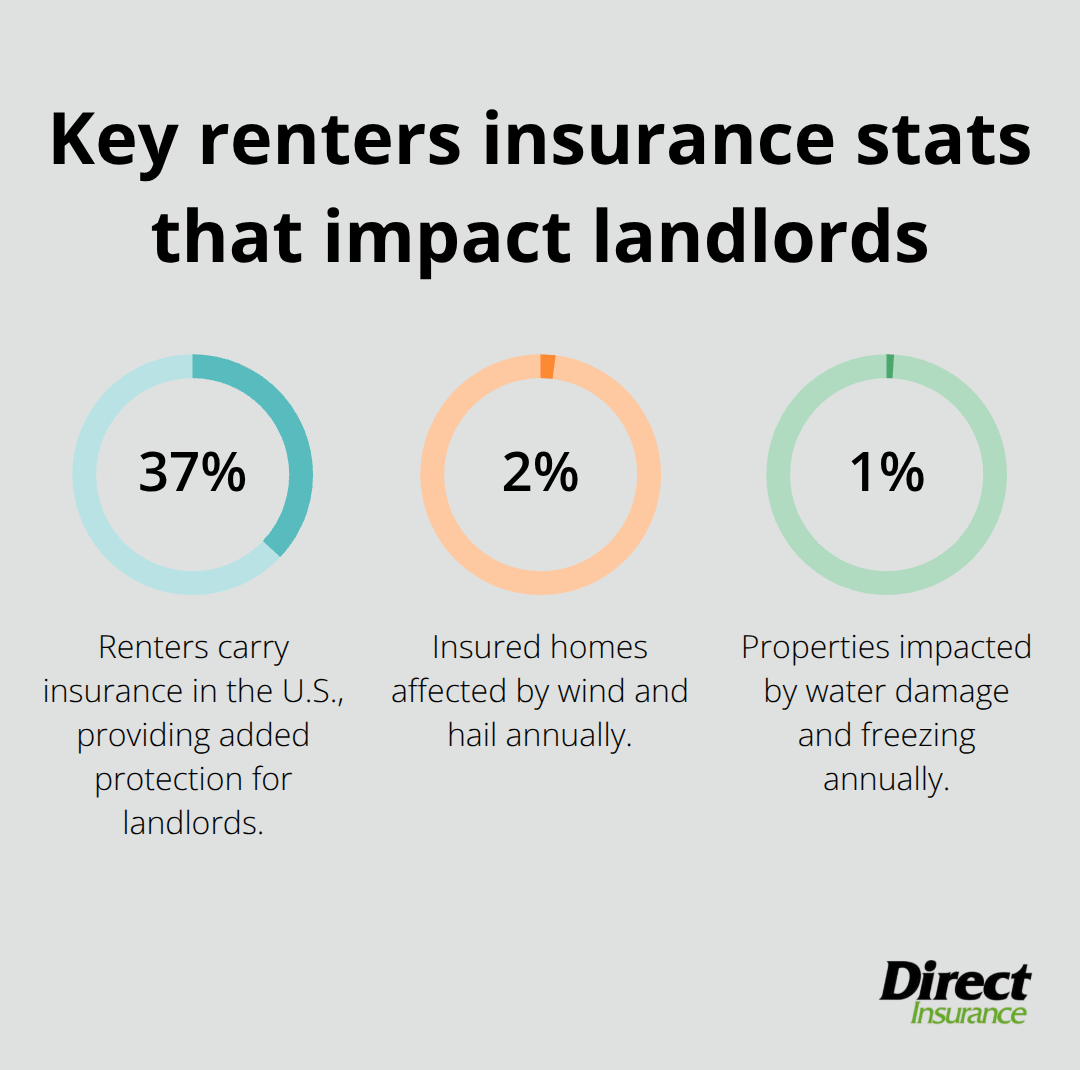

Renters insurance transforms tenant-caused damage from a landlord’s nightmare into a manageable situation. The Insurance Information Institute reports that 37% of renters carry insurance, but those who do provide landlords with substantial protection beyond basic security deposits. When a tenant’s kitchen fire spreads to neighboring units, their renters insurance liability coverage typically handles repair costs that can reach $50,000 or more. Security deposits rarely exceed two months’ rent, which makes them insufficient for major damage incidents.

Tenant Negligence Claims Get Redirected

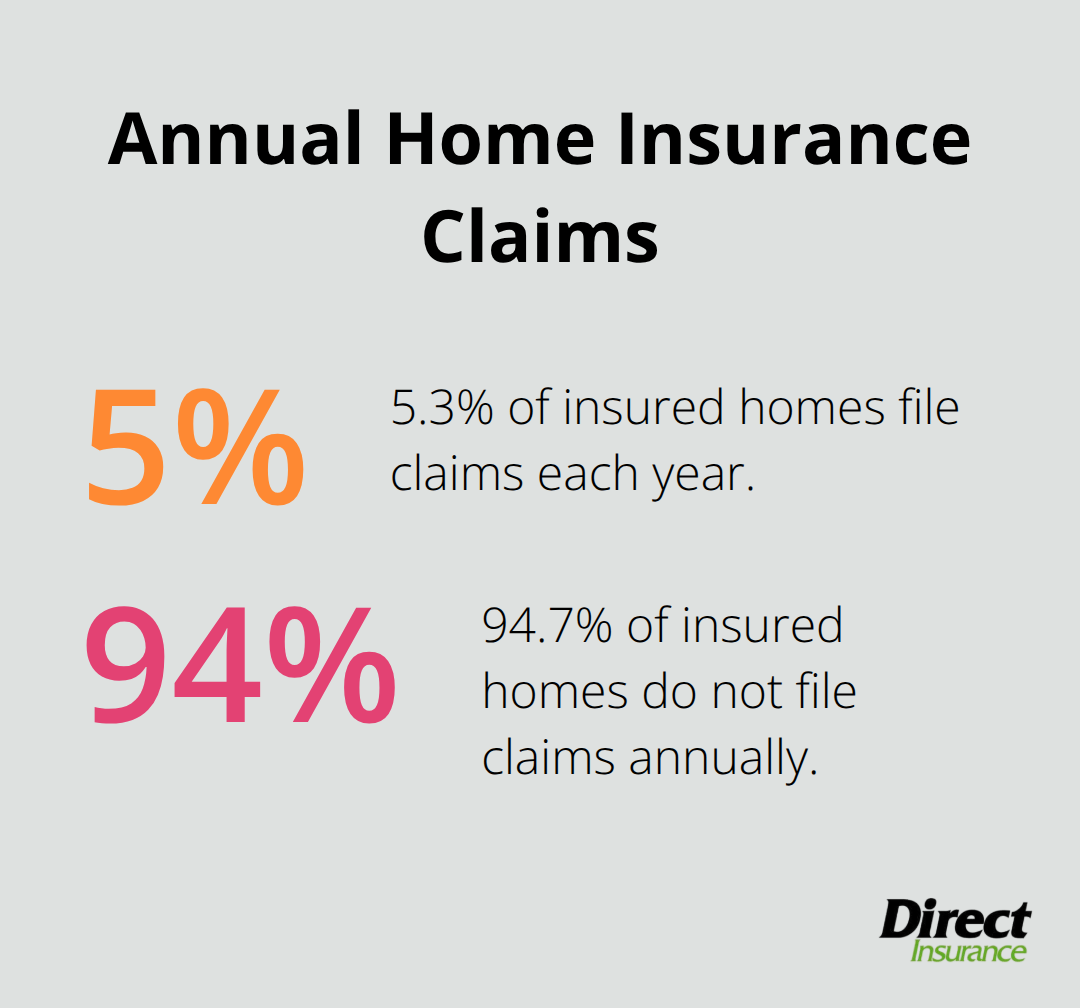

Water damage from bathtubs that overflow, grease fires from unattended stoves, and broken windows from parties represent common tenant negligence scenarios. Wind and hail account for the largest share of property claims, affecting 2.8% of insured homes, while water damage and freezing impact 1.5% of properties annually. The National Multifamily Housing Council found that properties that require renters insurance report 10-20% fewer tenant-related claims against landlord policies. When tenants carry liability coverage, these incidents become their insurance company’s responsibility rather than the landlord’s financial burden. Property managers consistently report smoother claim processes when both parties have proper coverage in place.

Pet and Guest Liability Protection

Renters insurance liability coverage extends to tenant guests and pets, areas where landlords face significant exposure. Dog bite incidents can cost landlords $18,000 on average (according to State Farm data), but tenant liability coverage handles these claims directly. Guest injuries that occur at tenant parties also fall under renters insurance protection, which removes potential lawsuit risks from property owners. Properties that allow pets while they require renters insurance see dramatically reduced liability claims compared to those without coverage requirements.

Beyond Basic Security Deposits

Standard security deposits cannot match the comprehensive protection that renters insurance provides. Most deposits cover only minor wear and tear or small damages (typically $1,000-$3,000), but major incidents like fires or floods can cost tens of thousands in repairs. Tenant liability coverage fills this gap and protects landlords from catastrophic financial losses that security deposits never could handle.

The next financial advantage landlords gain extends far beyond individual damage claims and affects their overall insurance costs and long-term profitability.

How Much Money Can Landlords Save?

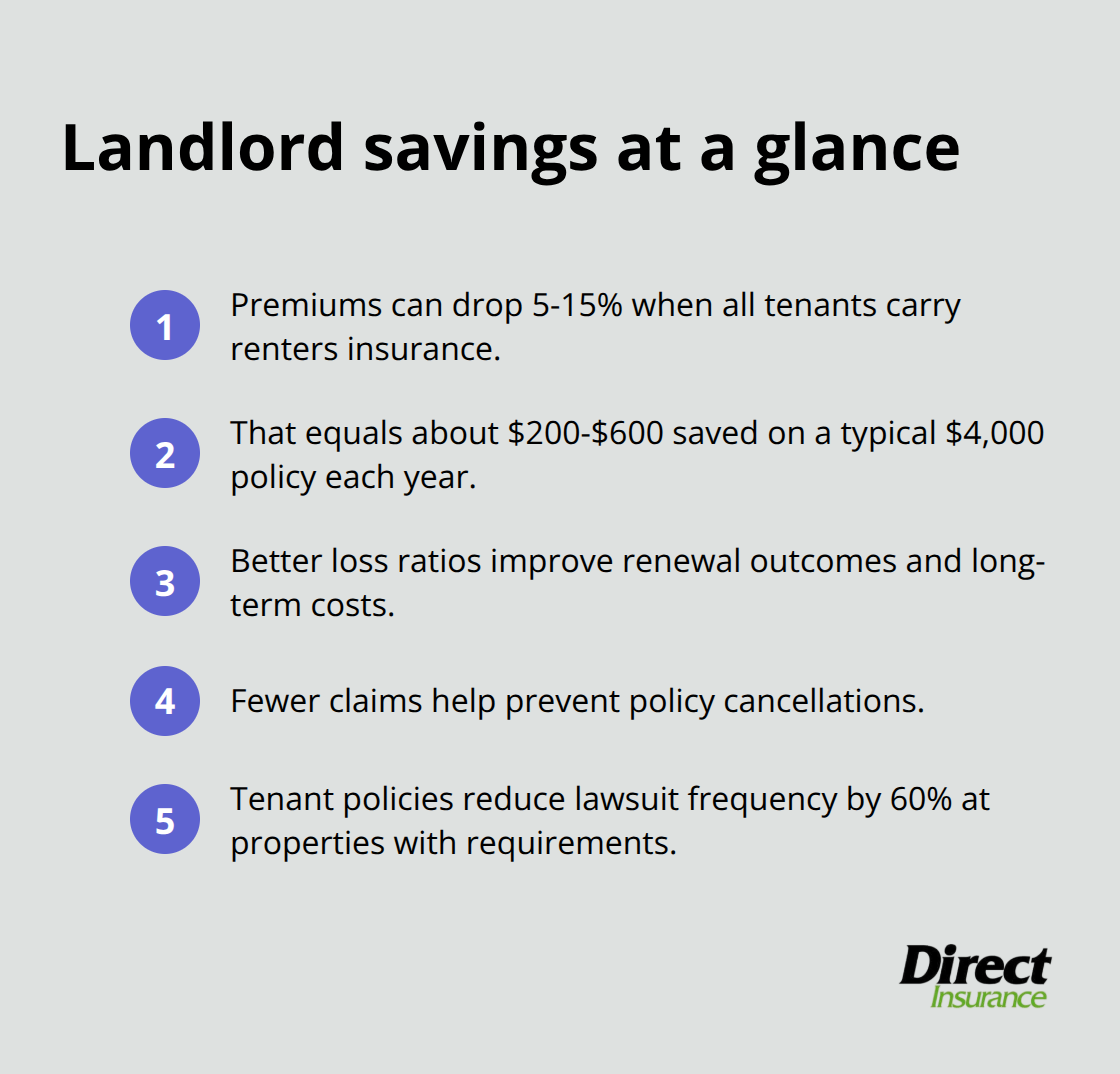

Landlords who require renters insurance see immediate financial benefits that compound over time. Insurance companies reward reduced risk exposure with lower premiums on landlord policies. The National Association of Insurance Commissioners reports that landlords can reduce their property insurance costs by 5-15% when all tenants carry renters insurance. This translates to $200-$600 annual savings on a typical $4,000 landlord policy. Properties with fewer claims maintain better loss ratios, which insurance companies factor into renewal decisions.

Premium Reductions Through Risk Transfer

Smart landlords understand that tenant insurance creates a barrier between their policy and costly claims. When tenant negligence causes damage, renters insurance handles the expense rather than triggers a claim against the landlord’s policy. Fewer claims mean lower premiums and reduced risk of policy cancellation. Insurance companies report that increased risks due to severe weather are the main factor contributing to premium hikes, which makes tenant insurance requirements a critical cost control strategy.

Direct Cost Savings on Repairs and Legal Defense

Tenant-caused damage without insurance coverage forces landlords to pay repair costs upfront, then pursue reimbursement through lengthy legal processes. Renters insurance eliminates this cash flow problem and handles claims directly. Legal disputes over tenant damage cost landlords an average of $3,000-$8,000 in attorney fees (according to the American Rental Property Owners Association). When tenants have liability coverage, their insurance company provides legal defense and removes this expense burden from property owners. Properties that enforce renters insurance requirements report 60% fewer tenant-related lawsuits compared to those without coverage mandates.

Long-Term Portfolio Protection

The financial advantages extend beyond individual incidents to protect entire rental portfolios. Landlords with consistent renters insurance requirements across all properties maintain cleaner claim histories, which insurance companies reward with preferred rates and better coverage terms. This protection becomes particularly valuable as property portfolios grow and risk exposure multiplies.

These direct financial benefits create the foundation for successful tenant relationships, but implementation requires strategic approaches that encourage compliance while maintaining positive landlord-tenant dynamics.

How Do You Get Tenants to Buy Renters Insurance

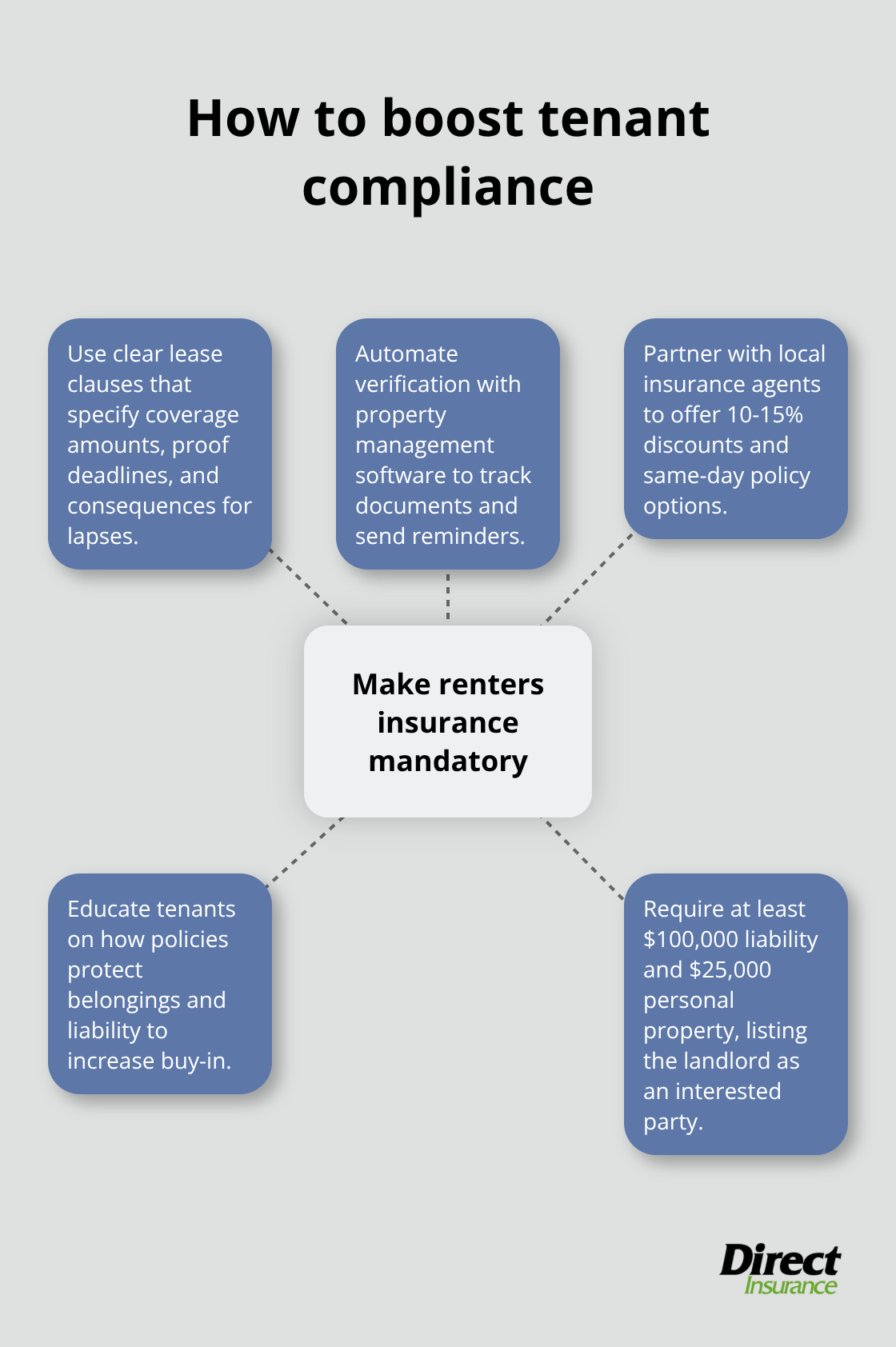

Landlords must take a strategic approach to make renters insurance mandatory through clear lease requirements and tenant education. Successful property owners write specific insurance requirements directly into lease agreements, state minimum coverage amounts, and require proof of insurance before move-in. The lease should specify $100,000 minimum liability coverage and $25,000 personal property protection, with the landlord listed as an interested party on the policy. This approach works because tenants understand the requirement before they sign, creating clear expectations from the start.

Write Clear Lease Language That Works

Effective lease clauses specify exact coverage amounts, renewal requirements, and consequences for coverage lapses. Smart landlords require tenants to provide declaration pages within 30 days of lease execution and annually thereafter. The lease should state that failure to maintain coverage constitutes a lease violation subject to immediate cure or quit notices. Property management software can automate insurance verification and send renewal reminders, which reduces administrative burden while maintaining compliance. Automated systems significantly improve tenant compliance rates compared to manual tracking methods.

Partner with Local Insurance Agents for Tenant Discounts

Direct partnerships with insurance agencies create win-win situations for landlords and tenants. Many insurance companies offer 10-15% discounts when landlords refer multiple tenants, which brings monthly costs down to $15-$20 per policy. These partnerships also streamline the application process and provide tenants with immediate coverage options. Some agencies offer same-day policy issuance, which eliminates delays in lease execution. Landlords who establish these relationships see faster tenant placement and reduced vacancy periods because insurance requirements become less of a barrier to rental approval.

Educate Tenants on Personal Benefits

Tenant education transforms insurance requirements from obstacles into valuable protections. Most renters don’t realize that landlord insurance covers only the building structure, not their personal belongings. A simple fact sheet that explains how renters insurance protects their furniture, electronics, and clothing helps tenants understand the personal value. Properties that provide educational materials see higher voluntary compliance rates before lease requirements take effect.

Final Thoughts

How does renters insurance protect the landlord? The evidence shows clear financial advantages that extend far beyond basic property protection. Landlords who require tenant coverage reduce their insurance premiums by 5-15% annually while they transfer liability risks worth thousands of dollars per incident. Properties with mandatory renters insurance report 10-20% fewer claims and 60% fewer tenant-related lawsuits compared to those without coverage requirements.

The long-term financial benefits compound over time through cleaner claim histories, preferred insurance rates, and reduced legal expenses. Smart property owners implement these requirements through clear lease language, insurance partnerships, and tenant education programs that transform coverage from an obstacle into a valuable protection. These strategies create win-win situations where tenants receive comprehensive protection while landlords reduce their risk exposure significantly.

We at Direct Insurance Services help landlords and tenants navigate these insurance requirements with personalized coverage solutions that protect both parties. Our independent agency works with top-rated carriers to provide affordable renters insurance options that meet lease requirements while they deliver comprehensive protection. The investment in proper tenant insurance requirements pays dividends through reduced risk exposure and improved property management outcomes (particularly for multi-unit properties).