How to Choose Auto Insurance with Liability Only Coverage

Auto insurance liability only coverage offers the most affordable protection for drivers who want to meet legal requirements without paying for comprehensive benefits.

At Direct Insurance Services, we see many customers choosing this option to reduce their monthly premiums while staying compliant with state laws.

This approach works best for specific financial situations and vehicle types, but requires careful consideration of your personal risk factors.

What Liability Only Coverage Actually Includes

Liability only coverage protects other drivers and passengers when you cause an accident, but stops there. Your policy pays for their medical bills, vehicle repairs, and legal fees if they sue you. The Insurance Information Institute reports that bodily injury liability covers hospital costs, rehabilitation, and lost wages for injured parties, while property damage liability handles repairs to their vehicles, fences, or buildings you damage. However, your own medical expenses, vehicle repairs, and replacement costs come directly from your pocket regardless of fault.

State Minimums Fall Short of Real-World Costs

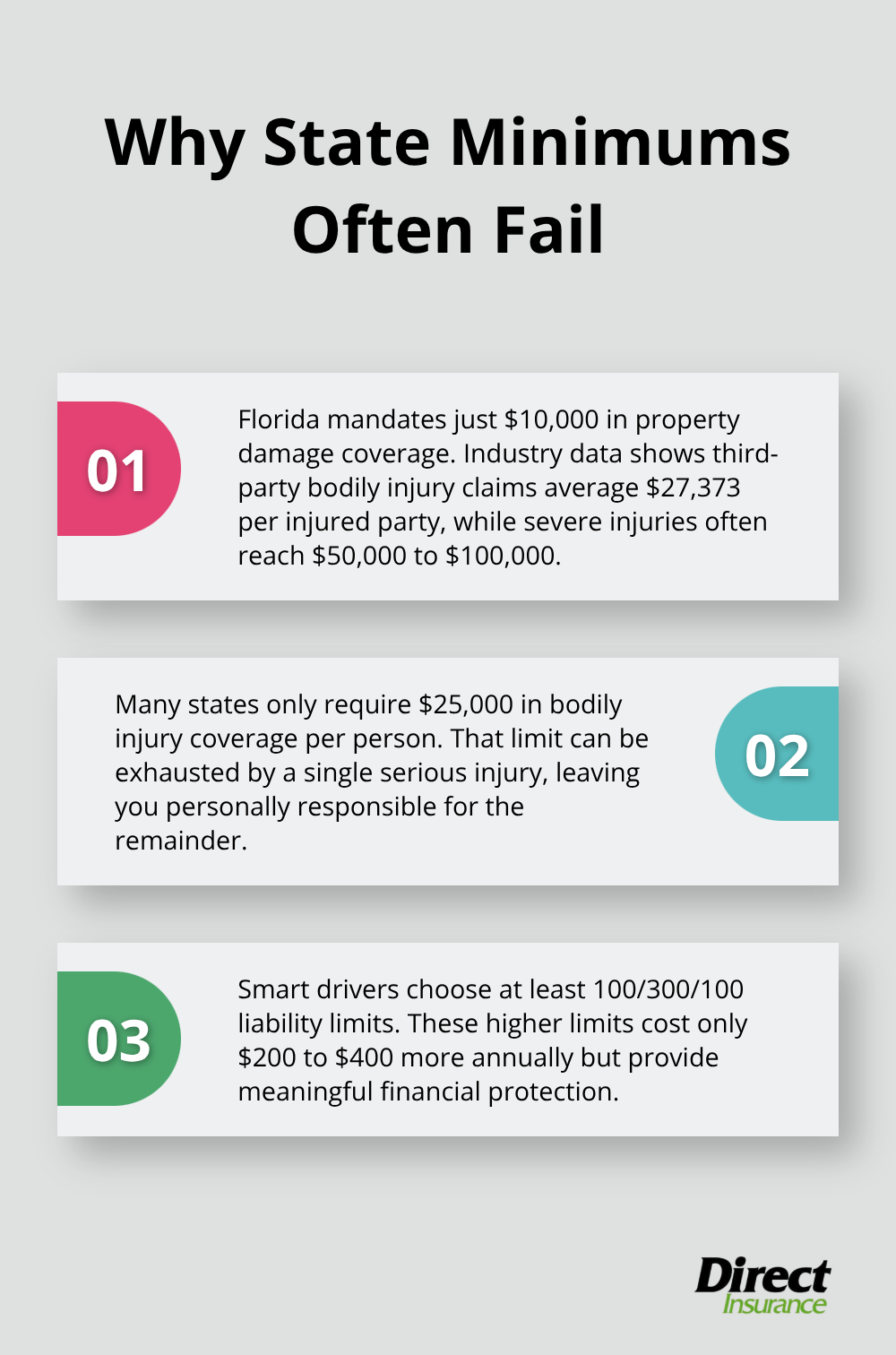

Most states require ridiculously low coverage amounts that won’t protect you in serious accidents. Florida mandates just $10,000 in property damage coverage, but third-party bodily injury claims average $27,373 per injured party according to 2024 industry data. Medical bills from severe injuries easily reach $50,000 to $100,000, yet many states only require $25,000 in bodily injury coverage per person. Smart drivers choose liability limits of at least $100,000 per person and $300,000 per accident for bodily injury, plus $100,000 for property damage. These higher limits cost only $200 to $400 more annually but provide genuine financial protection.

When Liability Only Makes Perfect Sense

Liability only coverage works best for older vehicles worth less than $4,000, since comprehensive and collision premiums often exceed the car’s actual value. If you drive a 2010 sedan worth $3,500 (and pay $800 yearly for full coverage), you waste money on unnecessary protection. Drivers with substantial emergency savings also benefit from liability only policies, as they can handle vehicle repairs without insurance payouts. However, avoid this approach if you cannot afford to replace your car immediately after an accident or if you still owe money on your vehicle loan.

The Hidden Gaps You Must Consider

Liability coverage leaves you exposed to significant financial risks beyond vehicle damage. Medical payments for your own injuries require separate coverage (personal injury protection or medical payments coverage), which most liability-only policies exclude. Property damage extends beyond vehicles-if you crash into someone’s fence, mailbox, or building, your liability coverage handles their repairs but not your legal defense costs in complex cases. These gaps become expensive problems when accidents involve multiple vehicles or serious injuries that exceed your coverage limits.

Should You Choose Liability Only Coverage?

Your Assets Determine Your Risk Exposure

Your net worth directly impacts whether liability only coverage makes financial sense. If you own a home worth $300,000, have $50,000 in savings, and earn $75,000 annually, you face serious exposure if your minimal state coverage fails to cover accident costs. The National Association of Insurance Commissioners reports that average bodily injury settlements reach $18,417, but severe accidents with multiple vehicles or permanent injuries can exceed $500,000. Drivers with significant assets should carry liability limits of at least $250,000 per person and $500,000 per accident to protect against lawsuits that could seize your home, savings, or future wages. However, if you rent your home, have minimal savings, and limited assets, higher liability limits provide less value since creditors cannot pursue what you don’t own.

Vehicle Age Creates Clear Coverage Decisions

Cars older than eight years rarely justify comprehensive and collision coverage costs. A 2015 Honda Accord worth $12,000 faces annual full coverage premiums around $1,400, while liability only costs approximately $600. Since comprehensive and collision coverage only pays actual cash value minus your deductible, you might receive just $10,500 after a $1,500 deductible for a totaled vehicle. This math becomes worse for vehicles worth under $5,000, where collision premiums often equal 20-30% of the car’s value annually. Financed vehicles require full coverage regardless of age, but once you own your car outright, switch to liability only when repair costs would exceed the vehicle’s market value.

Daily Habits Shape Your Risk Profile

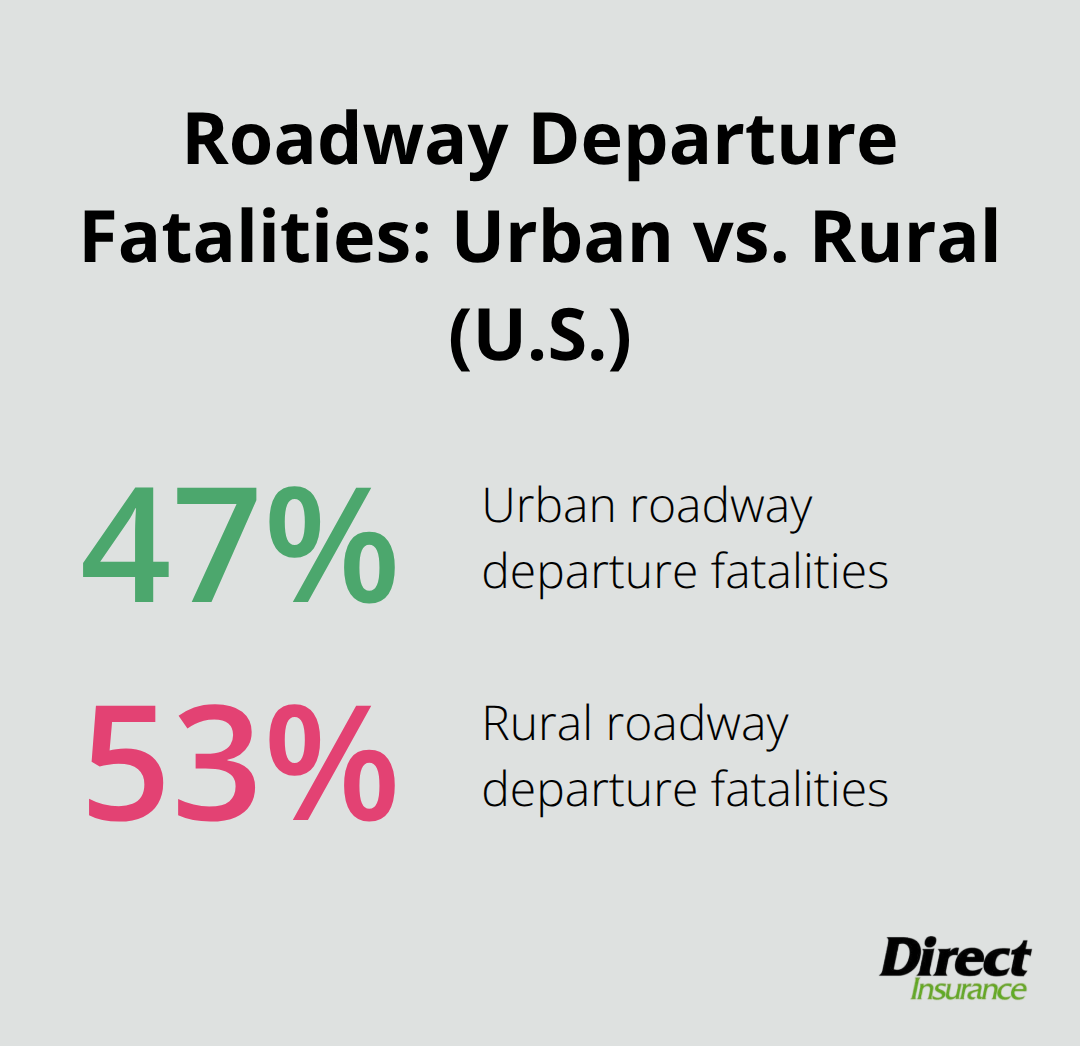

Urban drivers face higher accident risks than rural drivers, though roadway departure fatalities show 47 percent occur in urban areas versus 53 percent in rural areas. If you commute 40 miles daily through heavy traffic in Los Angeles or Chicago, your accident probability increases substantially compared to someone who drives 5,000 miles annually in rural areas. Drivers with poor records face even higher risks (one at-fault accident in the past three years increases your likelihood of future claims by 65%).

However, drivers over 50 with clean records who drive less than 10,000 miles annually represent the lowest risk category and benefit most from liability only policies.

Once you understand your personal risk factors, the next step involves comparison shopping to find the best rates and policy terms from multiple insurance carriers.

How to Find the Best Liability Coverage Deal

Insurance rates vary dramatically between carriers, with identical liability coverage differing significantly according to the National Association of Insurance Commissioners. GEICO might quote $450 annually for 50/100/50 liability limits while State Farm charges $720 for the same coverage in identical circumstances. Progressive, Allstate, and USAA each use different risk assessment models, which creates substantial price gaps even for drivers with clean records. We recommend that you obtain quotes from at least five carriers because the cheapest option changes based on your age, location, and history. Drivers under 25 often find the lowest rates with companies like GEICO or Progressive, while drivers over 50 typically save more with State Farm or Farmers. Online comparison tools provide quick estimates, but direct quotes from agents reveal additional discounts worth 10-25% that automated systems miss.

Policy Terms Hide Expensive Surprises

Standard liability policies contain exclusions that cost thousands during claims. Most carriers exclude coverage for commercial vehicle use, which means your Uber work or food delivery voids your personal policy entirely. Race activities, intentional damage, and impaired operation automatically void coverage, which leaves you personally liable for all accident costs. Per-occurrence limits create dangerous gaps in multi-vehicle accidents where your $100,000 property damage coverage splits between three damaged vehicles (just $33,333 each when repair costs exceed $50,000 per vehicle). Some carriers offer accident forgiveness for first-time claims, while others increase rates 20-40% immediately. Liberty Mutual and Nationwide typically provide more lenient claims processes compared to budget carriers that aggressively pursue premium increases after any claim.

Claims Response Time Separates Quality Carriers

Claims response time separates quality carriers from budget options during emergencies. State Farm processes 95% of liability claims within 30 days, while some discount carriers take 60-90 days for similar claims according to J.D. Power studies. Slow claims processes mean accident victims wait months for medical bill payments, which potentially leads to lawsuits against you personally. USAA consistently ranks highest for customer satisfaction but limits membership to military families. Progressive offers 24/7 claims reports and typically assigns adjusters within 24 hours, while Allstate provides local agents for face-to-face claim assistance.

Customer Complaint Ratios Reveal True Service Quality

Avoid carriers with complaint ratios above 1.5 per the National Association of Insurance Commissioners database, as these companies generate significantly more customer disputes and regulatory violations than industry averages. Companies with high complaint ratios often delay payments, deny valid claims, or provide poor customer service when you need help most. Check each carrier’s complaint ratio before you purchase coverage (this data appears on your state insurance department website). The best carriers maintain complaint ratios below 0.8, which indicates superior customer service and fair claims practices.

Final Thoughts

Auto insurance liability only coverage works best when your vehicle value falls below $4,000 and comprehensive premiums exceed potential payouts. Drivers with significant assets (homes worth $200,000+ or savings above $25,000) need higher liability limits to protect against lawsuits that could target their wealth. Your location and annual mileage directly affect accident probability, with urban drivers covering 15,000+ miles facing greater risks than rural drivers who travel 8,000 miles yearly.

Rate differences between carriers reach 30-60% for identical coverage, which makes comparison shopping essential for cost savings. Clean records over three years indicate lower future claims, but policy exclusions for ride-sharing or commercial use can void your protection entirely. Complaint ratios above 1.0 signal poor customer service when you need claims assistance most.

At Direct Insurance Services, we help drivers evaluate their specific circumstances to determine the right coverage balance. Our team provides personalized consultations without pressure tactics to match your protection needs with your budget. Contact our experienced agents to review your situation and find the most suitable auto insurance liability only option for your needs.