Renting property to family members creates a unique situation that many property owners face. The question “Do I need landlord insurance if renting to family?” comes up frequently, and the answer might surprise you.

At Direct Insurance Services, we see property owners assume family relationships eliminate the need for proper coverage. This assumption can lead to significant financial exposure when unexpected situations arise.

What Makes Landlord Insurance Different from Homeowners Coverage

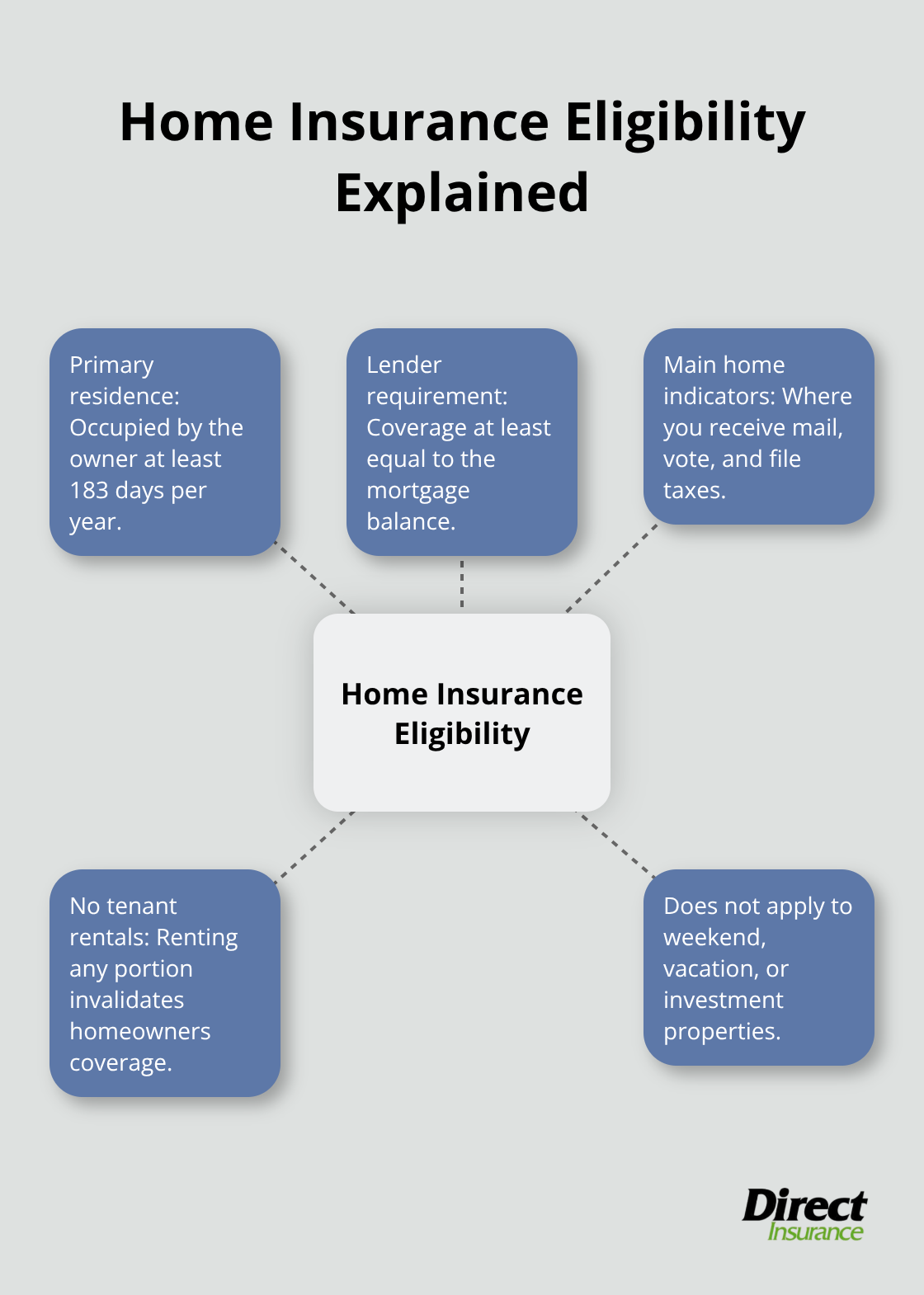

Homeowners insurance protects your primary residence and personal belongings, but it stops coverage the moment you collect rent from anyone. The Insurance Information Institute confirms that homeowners policies work exclusively for occupied residences, not rental activities. This fundamental difference means your standard policy will deny claims related to tenant damage, rental income loss, or liability issues that involve renters.

Property Coverage Gaps That Cost Money

Standard homeowners insurance covers typical residential risks like fire, theft, and weather damage. Landlord insurance goes further and protects against tenant-specific damages like intentional property destruction, excessive wear from multiple occupants, and vandalism after move-out.

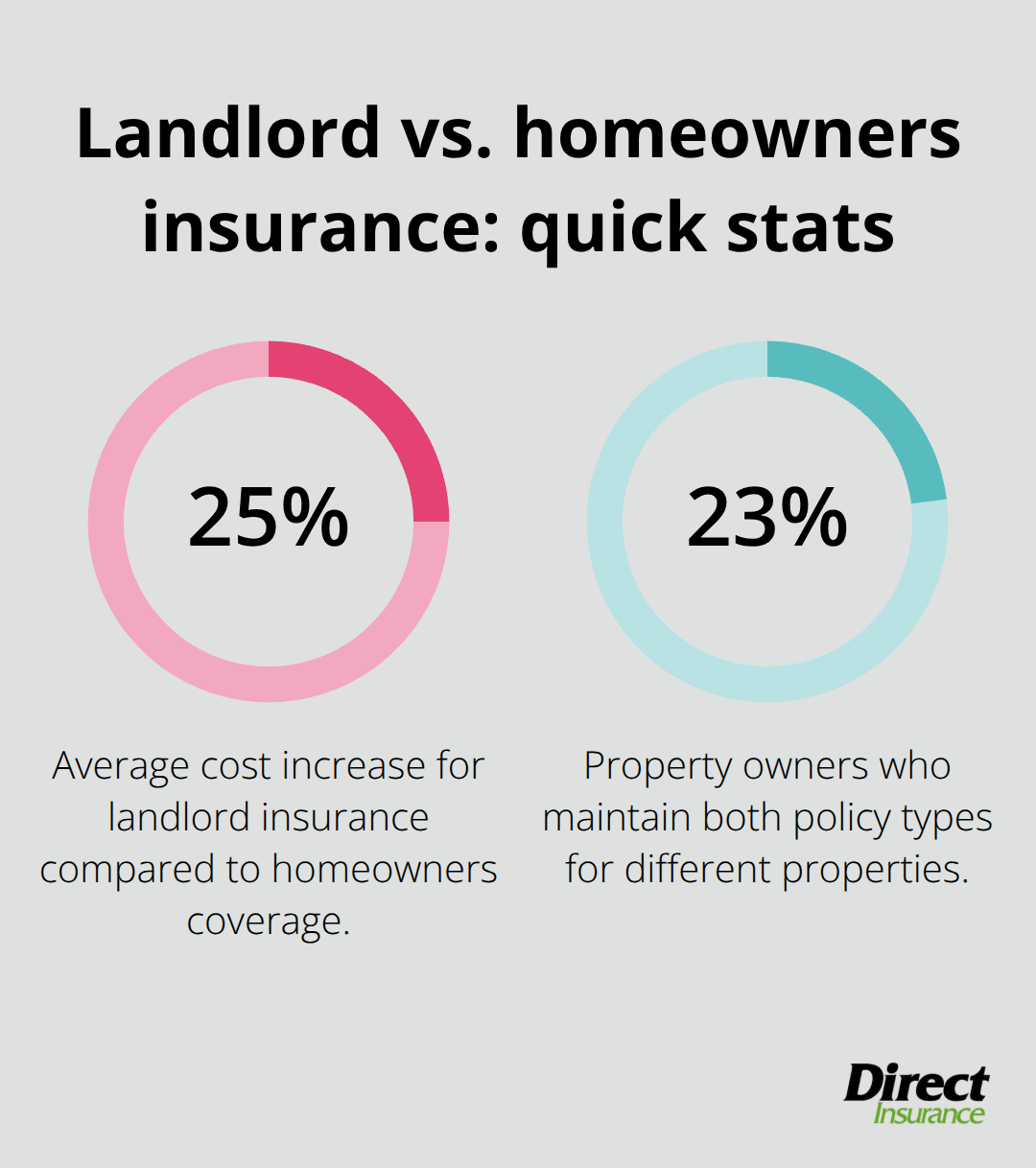

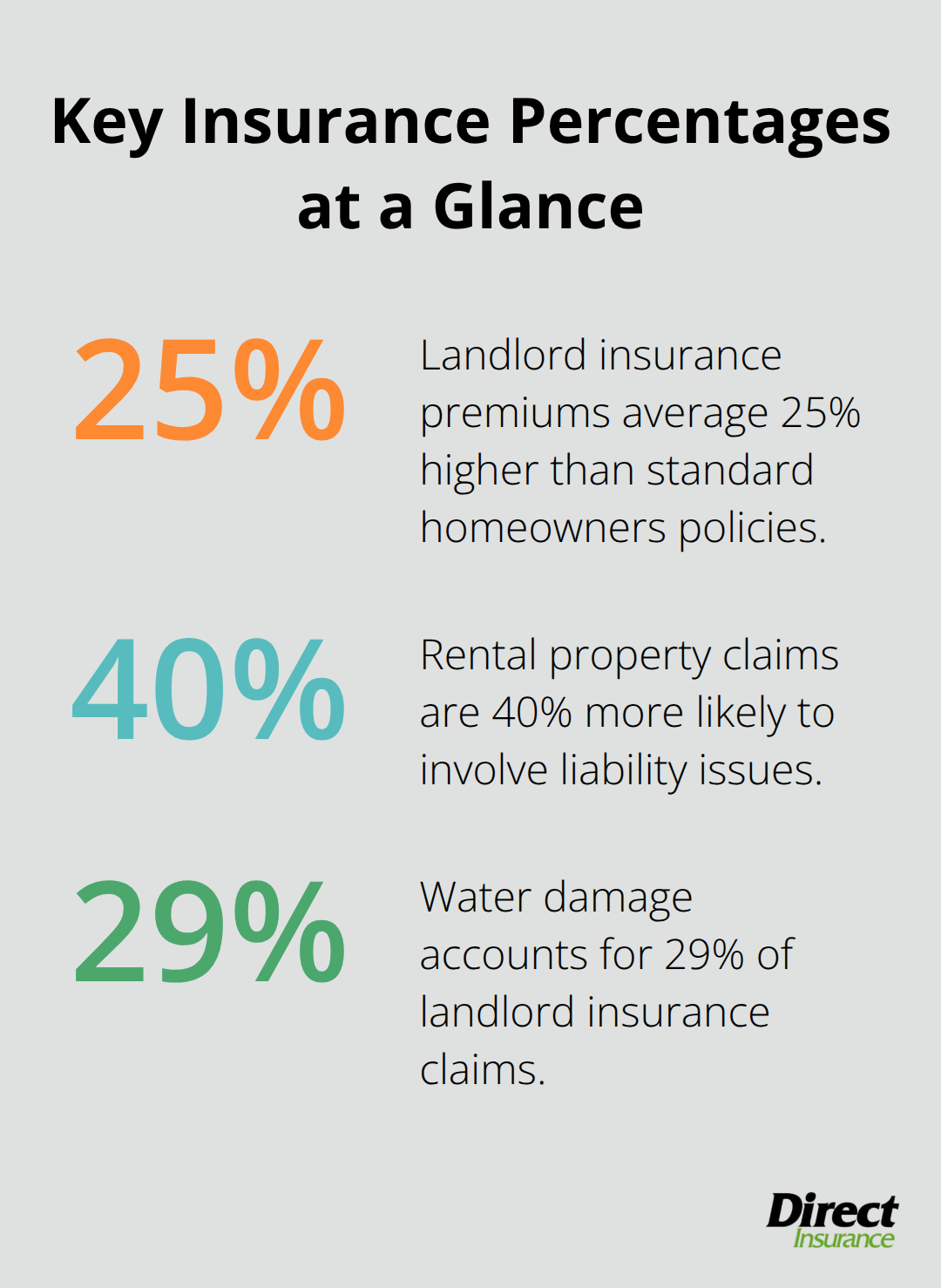

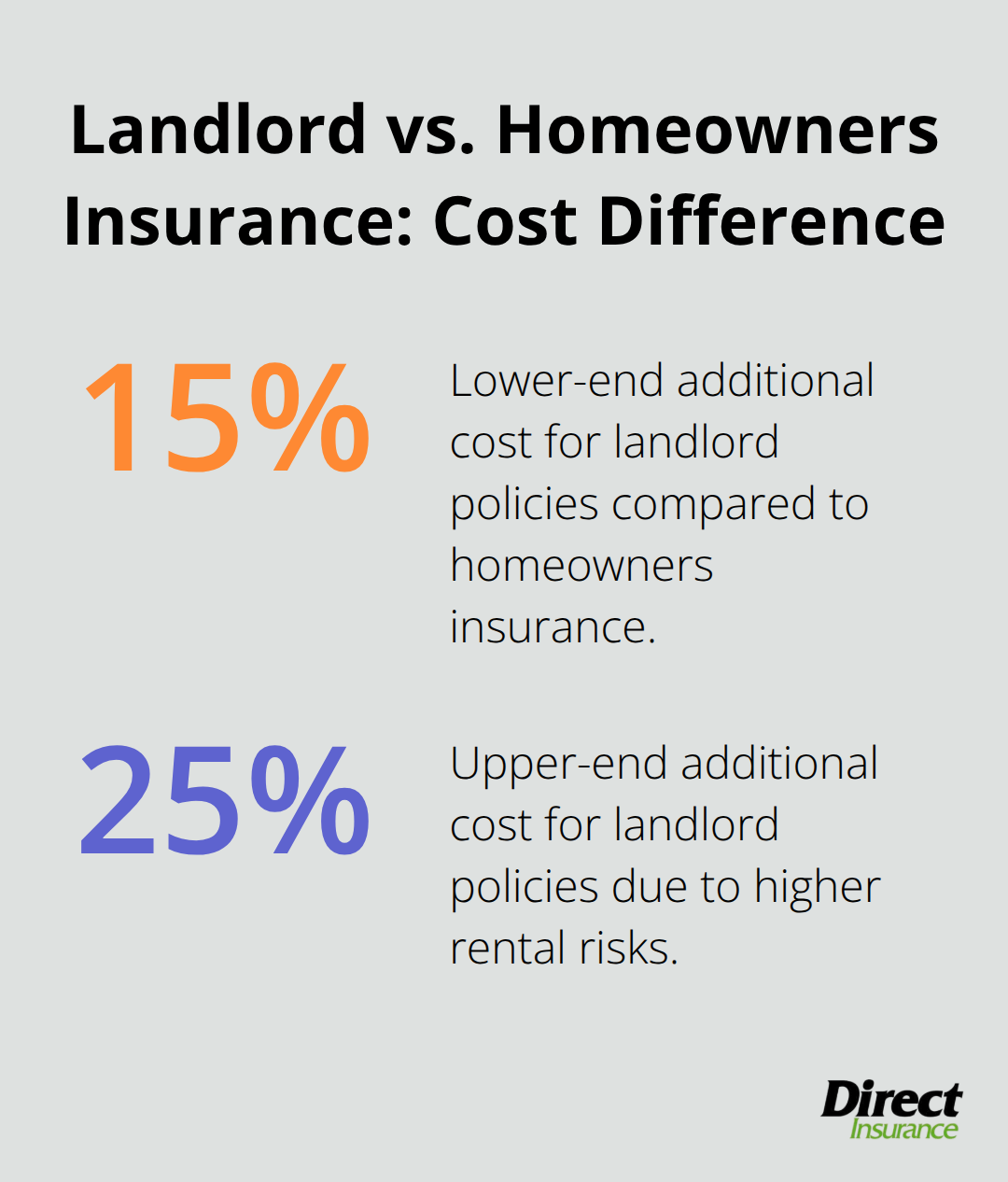

The National Association of Insurance Commissioners reports that landlord policies cost 15% to 25% more than homeowners insurance because rental properties face higher damage risks. Average landlord insurance premiums range from $73.58 monthly in Oregon to $207.00 in Louisiana (with a national average of $126 monthly as of January 2024).

Liability Protection Beyond Basic Coverage

Homeowners liability coverage assumes you control who enters your property. Landlord insurance recognizes that tenants bring guests, hold parties, and create situations beyond your control. Most insurance experts recommend landlord liability limits of at least $500,000, with many property owners who choose $1 million coverage. This higher protection becomes vital when tenant guests suffer injuries on your property and create lawsuit exposure that standard homeowners policies won’t cover.

Why Family Relationships Don’t Change Insurance Requirements

Property owners often believe family relationships eliminate insurance risks, but accidents and property damage occur regardless of tenant relationships. The same liability exposure exists whether your tenant shares your last name or pays market rent. Family members can still cause property damage, have guests who get injured, or create situations that lead to expensive claims (making proper coverage essential even for family rentals).

Special Considerations When Renting to Family Members

Family rental arrangements create complex insurance situations that property owners consistently underestimate. The Insurance Information Institute reports that 48.2 percent of renter occupied units spend more than 30 percent on rent and utilities, yet approximately 40% of landlords skip tenant-related risk coverage. This gap exposes property owners to substantial financial liability because family relationships don’t eliminate legal responsibilities or accident risks.

Family tenants can still cause property damage, have guests who suffer injuries, or create situations that generate expensive claims. Property owners need proper documentation and coverage to protect themselves from these risks.

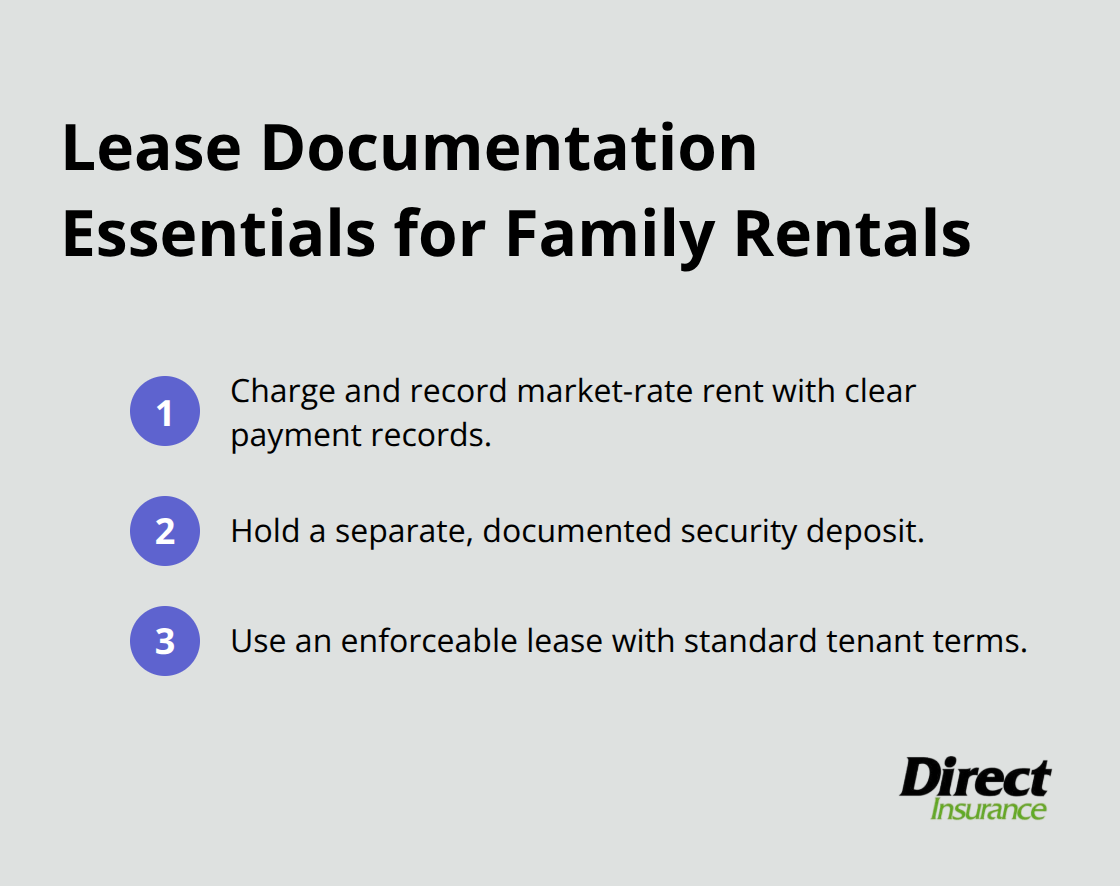

Written Lease Agreements Protect Insurance Coverage

Insurance companies require written rental agreements to process claims, regardless of family relationships. Without formal documentation, insurers often deny coverage because they cannot verify legitimate rental activity versus informal family arrangements.

Property owners must establish market-rate rent payments with documented transactions, maintain separate security deposits, and create enforceable lease terms that match standard tenant agreements.

The National Association of Insurance Commissioners emphasizes that informal family arrangements frequently void insurance protections. This leaves property owners personally liable for damages and legal costs that proper landlord policies would otherwise cover.

Insurance Claims Face Additional Scrutiny

Family rental claims trigger additional insurance company investigations because fraud potential increases when relatives are involved. Insurers examine payment records, lease documentation, and damage circumstances more thoroughly to verify legitimate tenant relationships versus insurance manipulation.

Property owners should maintain detailed records of all rent payments, property maintenance, and tenant communications to support future claims. Family members might feel less obligated to report damages immediately or might handle repairs informally (which creates coverage gaps that insurance companies use to deny legitimate claims later).

These documentation requirements become particularly important when insurance adjusters investigate family rental situations. The extra scrutiny means property owners need comprehensive records that prove legitimate landlord-tenant relationships exist, which directly impacts the benefits that proper landlord insurance provides.

How Landlord Insurance Protects Family Rental Investments

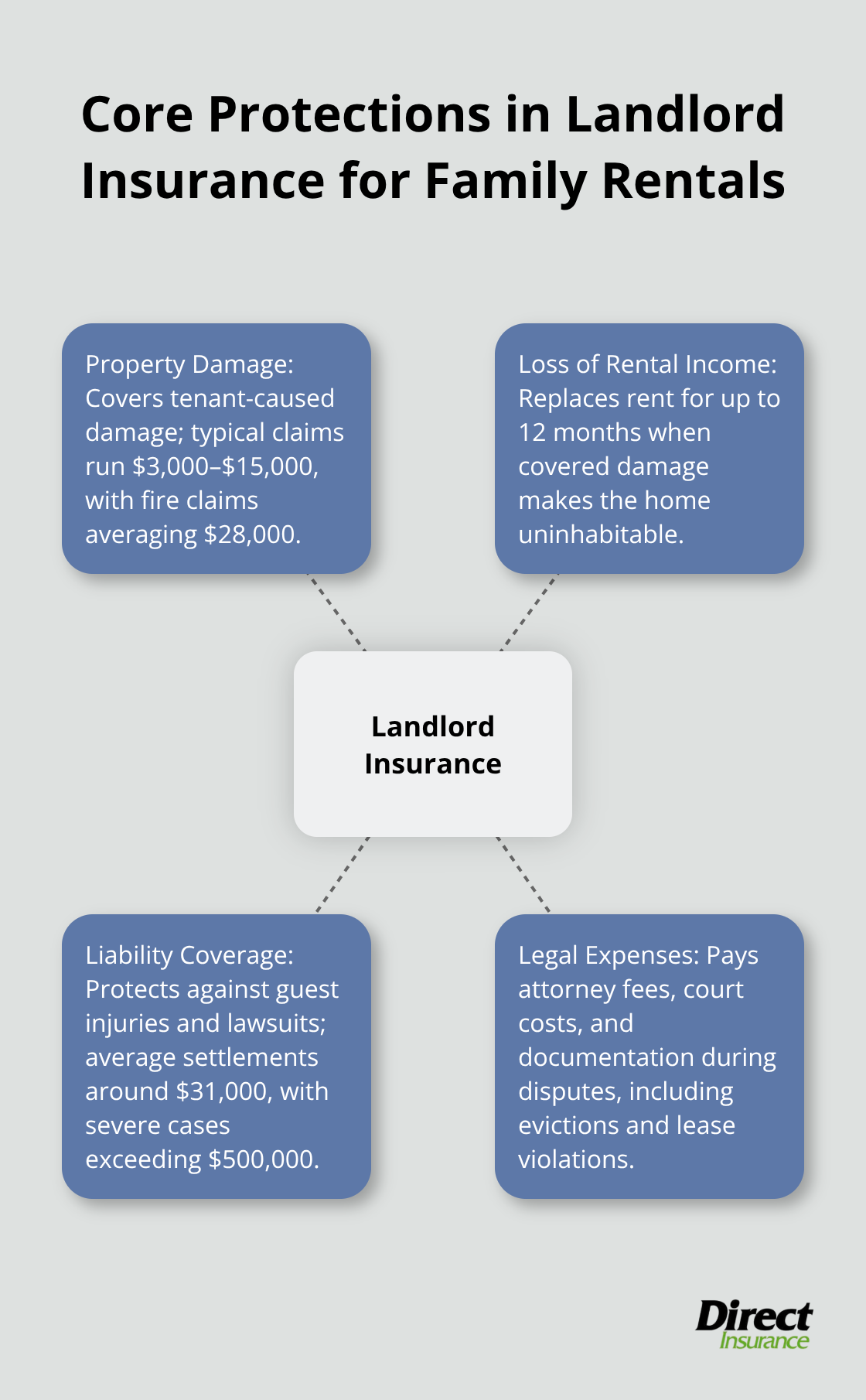

Property Damage Coverage Delivers Financial Protection

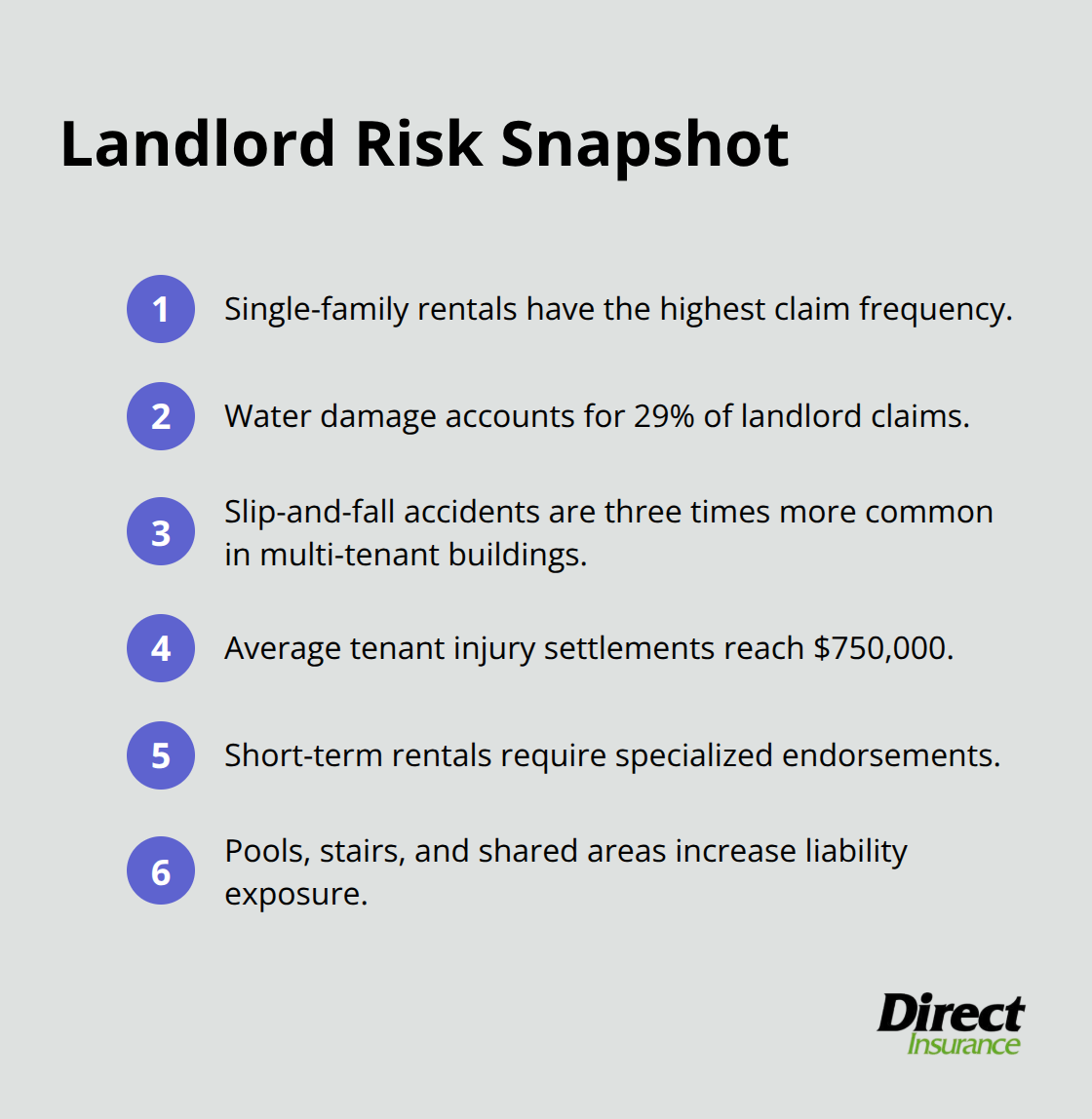

Landlord insurance provides comprehensive property protection that homeowners policies cannot match for rental situations. Family members who rent your property create identical damage risks to non-family tenants, yet the financial protection becomes more valuable. The average landlord insurance claim for property damage ranges from $3,000 to $15,000 according to industry data, with fire damage claims that average $28,000 per incident.

Family tenants can accidentally cause kitchen fires, flood bathrooms, or create damage from pets that standard homeowners coverage would reject. Property owners face these exact situations where family relationships provide no protection against expensive repair bills that proper landlord coverage handles completely.

Loss of Rental Income Coverage Prevents Financial Hardship

Property owners who collect family rent depend on that income for mortgage payments, property taxes, and maintenance costs. Landlord insurance includes loss of rental income coverage that continues payments when covered damage makes the property uninhabitable.

This coverage typically provides 12 months of rental payments at market rate (even when family members pay below-market rent).

The Insurance Information Institute confirms this benefit applies regardless of tenant relationships. This makes it particularly valuable for family rental arrangements where informal payment structures might otherwise complicate income replacement claims.

Liability Coverage Handles Expensive Legal Situations

Family rental liability exposure creates the same lawsuit risks as traditional tenant relationships, yet property owners often underestimate these dangers. Landlord insurance liability coverage protects against slip-and-fall accidents, guest injuries, and property-related incidents that can generate six-figure legal judgments.

The average premises liability claim settlement reaches $31,000, with severe injury cases that exceed $500,000 in damages. Family members host parties, have children visit, and create the same accident scenarios that lead to expensive lawsuits. This coverage includes legal defense costs that can reach $50,000 before any settlement discussions begin (which protects your financial assets when family tenant situations turn into legal complications).

Legal Expense Protection Covers Tenant Disputes

Landlord insurance provides legal expense coverage for tenant disputes that can arise even with family members. Eviction proceedings, lease violations, and property damage disputes require legal representation that costs thousands of dollars. Family relationships can complicate these situations when personal emotions interfere with business decisions, yet the legal requirements remain identical to standard tenant relationships.

This coverage handles attorney fees, court costs, and legal documentation expenses that property owners face during tenant disputes. The protection becomes particularly valuable when family rental arrangements deteriorate and require formal legal intervention to resolve conflicts.

Final Thoughts

The question “Do I need landlord insurance if renting to family?” has a clear answer: yes, absolutely. Family relationships don’t eliminate property damage risks, liability exposure, or income loss potential. The same accidents, injuries, and disputes that affect traditional tenant relationships occur with family members.

Property owners who skip landlord insurance face personal liability for expensive repairs, medical bills, and legal costs that proper coverage would handle. The average landlord insurance premium of $126 monthly provides protection against claims that routinely exceed $30,000 (making this investment particularly valuable when family rental situations create complex legal and financial complications). This coverage becomes essential regardless of tenant relationships.

Professional guidance helps you secure appropriate coverage that protects against the real risks that family rentals create. We at Direct Insurance Services work with experienced agents to provide tailored insurance solutions that protect your rental investment. Don’t let family relationships create a false sense of security that leaves your property and finances exposed.