How to Get Homeowners Insurance as a Landlord

Many landlords mistakenly believe their standard homeowners insurance will protect their rental properties. This assumption creates dangerous coverage gaps that could cost thousands in unprotected losses.

We at Direct Insurance Services see landlords face financial disasters when tenant-related incidents aren’t covered by basic homeowners insurance landlord policies. The right insurance approach protects both your property investment and rental income stream.

What Makes Landlord Insurance Different from Homeowners Insurance

Standard homeowners insurance operates on the assumption that you live in the property year-round. Once tenants occupy your home, this fundamental assumption breaks down completely.

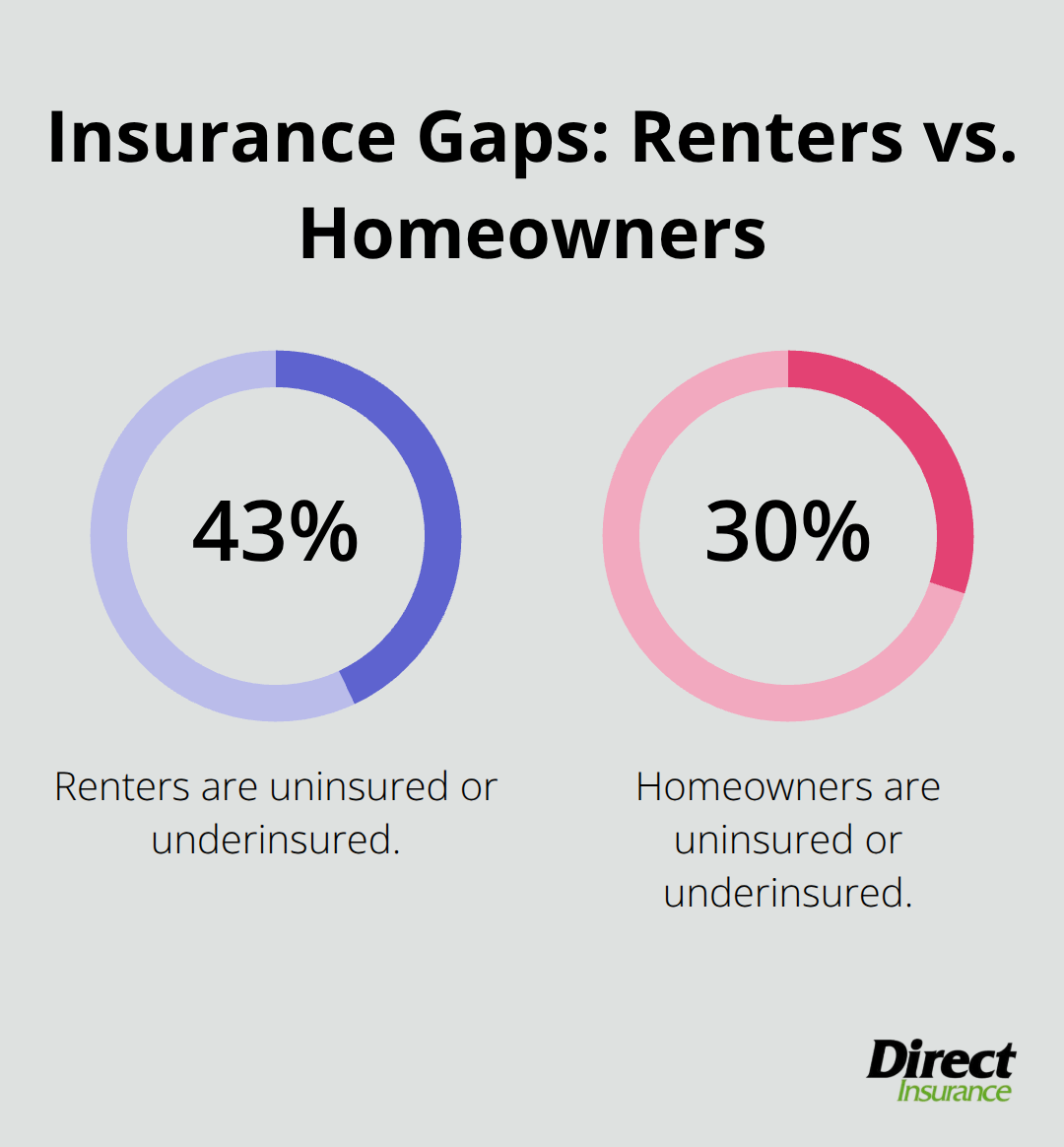

According to the Insurance Information Institute, 43 percent of renters are uninsured or underinsured, compared to 30 percent of homeowners. The moment you collect rent, you face entirely different liability exposures that homeowners policies simply don’t address.

Tenant-Related Damage Coverage

Homeowners insurance typically excludes damages that tenants cause, which leaves landlords financially exposed when renters cause property damage beyond normal wear and tear. Landlord insurance specifically covers tenant-caused damages, which include intentional destruction, water damage from negligence, and fire damage from tenant activities. This coverage difference becomes critical when you face repair costs that can easily reach thousands of dollars. Standard homeowners policies also fail to address vandalism by former tenants or damages that occur during eviction proceedings (situations that landlord insurance handles routinely).

Liability Protection Gaps

The liability coverage in homeowners insurance doesn’t extend to rental activities, which creates massive financial exposure for property owners. When tenants or their guests suffer injuries on rental property, homeowners insurance may deny claims entirely and leave landlords personally liable for medical expenses and legal costs. Landlord insurance provides specific liability protection for rental-related incidents, typically with coverage that starts at $1 million. Without proper landlord coverage, a single slip-and-fall lawsuit could result in financial ruin, especially in litigation-heavy states where settlement amounts frequently exceed $100,000.

Loss of Rental Income Protection

Homeowners insurance offers no protection for lost rental income when property damage makes units uninhabitable. Landlord insurance includes rental income protection, typically covers 10-20% of the dwelling coverage amount for periods when tenants cannot occupy the property due to covered damages. This protection becomes vital when fire, storm damage, or other covered perils force temporary relocations that can last months during repairs (particularly in areas prone to natural disasters).

These fundamental differences highlight why landlords need specialized coverage that addresses the unique risks of rental properties. The next step involves understanding exactly what types of coverage your rental property requires.

What Coverage Do Rental Properties Actually Need

Landlord insurance requires three non-negotiable coverage types that work together to protect your rental investment from financial catastrophe. Dwelling coverage forms the foundation and protects the physical structure from fire, storm damage, and other covered perils. The coverage amount should reflect current replacement costs, not market value, which means regular appraisals become necessary as construction costs rise. In 2025, replacement cost coverage averages 20-30% higher than actual cash value coverage, but this difference prevents devastating shortfalls when you rebuild after total losses.

Dwelling Coverage Must Match Replacement Costs

Property coverage extends beyond the main structure to include detached garages, sheds, and other permanent fixtures on the rental property. Most policies automatically include 10% of the dwelling coverage for other structures, but this amount often proves insufficient for properties with valuable outbuildings (particularly in rural areas where barns or workshops add significant value). Personal property coverage protects appliances and furnishings that you provide as part of the rental, typically ranging from $10,000 to $50,000 depending on what you include in the rental agreement.

Smart landlords document all provided items with photographs and receipts to support claims when tenant damage or theft occurs. This documentation becomes essential when insurance adjusters evaluate claims and determine replacement values.

Liability Protection Starts at One Million Dollars

Liability coverage protects against lawsuits when tenants, guests, or service providers suffer injuries on your rental property. The minimum recommended coverage amount is $1 million per occurrence, though many experienced landlords carry $2 million or more through umbrella policies. Medical payments coverage, typically $5,000 to $10,000, handles minor injuries without triggering liability claims and often prevents small incidents from escalating into lawsuits.

Loss of Rental Income Coverage Protects Your Cash Flow

Loss of rental income coverage compensates for lost rent when covered damages make your property uninhabitable, helping landlords stay protected when tenants can’t occupy a property. This protection becomes vital during extended repairs, particularly in areas where contractor shortages can delay reconstruction for months (especially after widespread natural disasters that create high demand for repair services).

The coverage typically pays your actual rental income, not potential market rates, which makes accurate documentation of rental agreements essential for claims processing. Once you understand these coverage requirements, the next step involves finding the right insurance company and policy structure for your specific rental situation.

How Do You Find the Right Landlord Insurance Policy

Start your search 60-90 days before your current policy expires to avoid non-renewal situations in high-risk markets. Major carriers like State Farm, Allstate, and Farmers offer competitive landlord policies, but their coverage terms and prices vary significantly based on property location and risk factors. Request quotes from at least five different insurers because premium differences can exceed 40% for identical coverage amounts (particularly in states prone to natural disasters where some carriers limit their exposure while others remain competitive).

Independent Agents Access Multiple Markets

Independent agents access multiple insurance markets through a single application process, which saves time and often uncovers better prices than direct carriers can offer. These agents handle the comparison process and explain policy differences that direct carrier representatives might not highlight, especially exclusions and coverage limitations that become critical during claims. Direct carriers like GEICO or Progressive offer streamlined online applications but limit you to their specific coverage options and prices, which may not provide the best value for your specific rental property situation.

Policy Features Determine Your Financial Protection

Choose replacement cost coverage rather than actual cash value because construction costs continue to rise with a 30-year average inflation rate of 4.1% for residential and nonresidential buildings. This difference makes adequate funds essential after total losses. Verify that loss of rental income coverage provides at least 12 months of protection because complex repairs often take longer than expected (particularly after widespread natural disasters that create contractor shortages).

Review Liability Limits and Deductibles

Examine liability limits carefully because the minimum $300,000 coverage that some policies offer proves insufficient in today’s litigation environment where settlement amounts frequently exceed $500,000. Named storm deductibles in hurricane-prone states can reach 2-5% of your property value rather than fixed dollar amounts, which dramatically increases your out-of-pocket costs during major weather events.

Document Policy Exclusions

Standard landlord policies often exclude flood damage, which requires separate National Flood Insurance Program coverage that takes 30 days to become effective. Review all exclusions before you purchase because these gaps can leave you financially exposed when disasters strike your rental property.

Final Thoughts

Landlords must secure proper insurance before they rent their property to tenants. Contact multiple insurers within the next 30 days to compare coverage options and prices because delays after tenant move-in create dangerous protection gaps. Most property owners make the mistake of assuming their existing homeowners insurance landlord coverage extends to rental activities, which leaves them financially exposed to tenant-related damages and liability claims.

Property owners should avoid the cheapest policy without reviewing coverage limits and exclusions. The difference between adequate and inadequate coverage often costs less than $500 annually but protects against losses that can reach tens of thousands of dollars. Document all property conditions and rental agreements before tenants move in because this documentation supports claims when damages occur.

We at Direct Insurance Services help Utah landlords transition from homeowners to landlord insurance with personalized coverage solutions that fit specific rental property needs (our independent agency works with top-rated carriers to find the best protection for your investment). Our team provides coverage reviews without the pressure of one-size-fits-all approaches. Contact our experienced team today to review your current coverage and secure proper protection for your rental property investment.