Is Landlord Insurance Necessary for Property Owners?

Property owners often ask: do you have to have landlord insurance? The answer depends on your specific situation and location.

We at Direct Insurance Services see many Utah landlords face significant financial losses without proper coverage. While not always legally required, landlord insurance protects against property damage, liability claims, and lost rental income.

What Landlord Insurance Covers

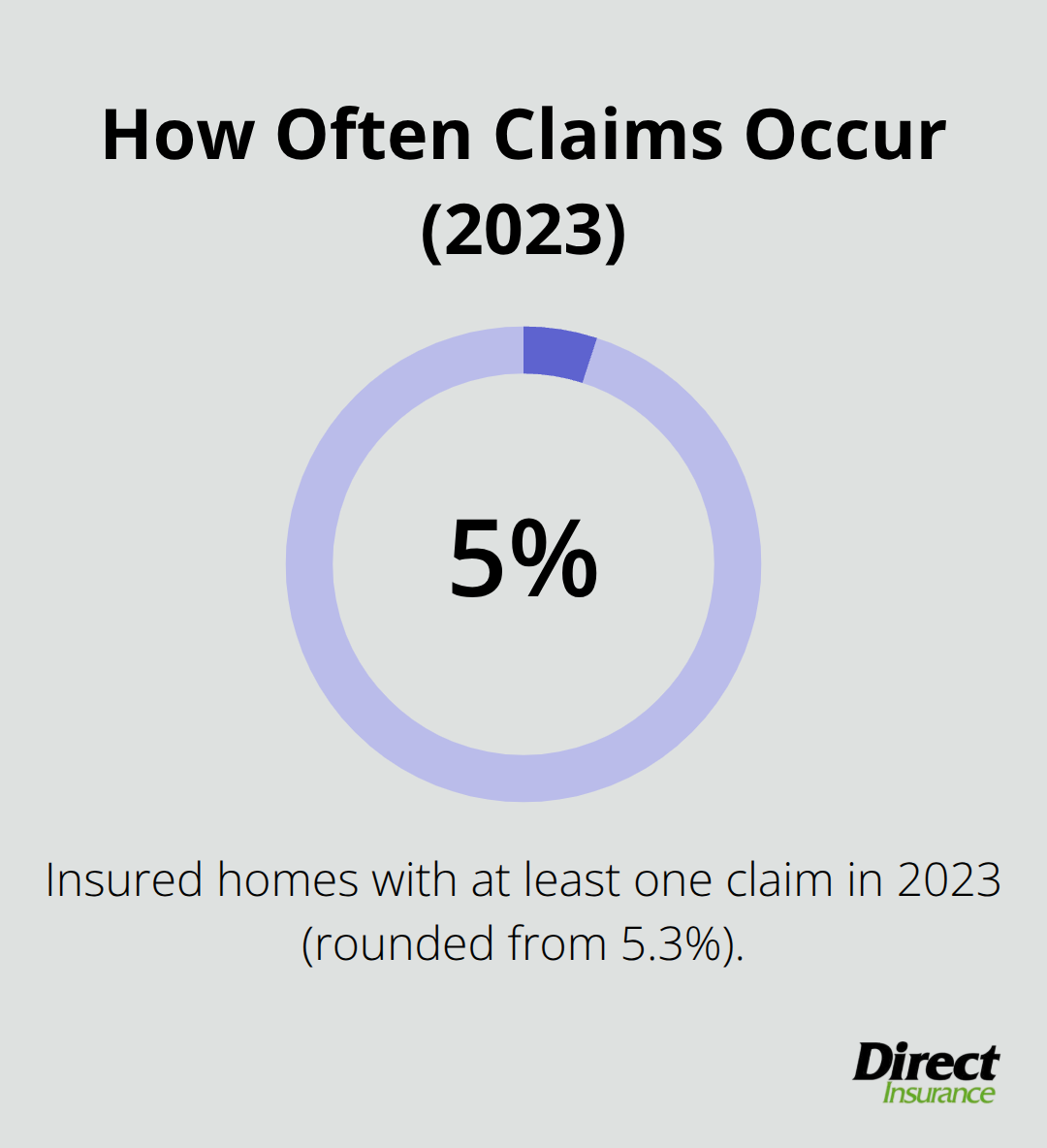

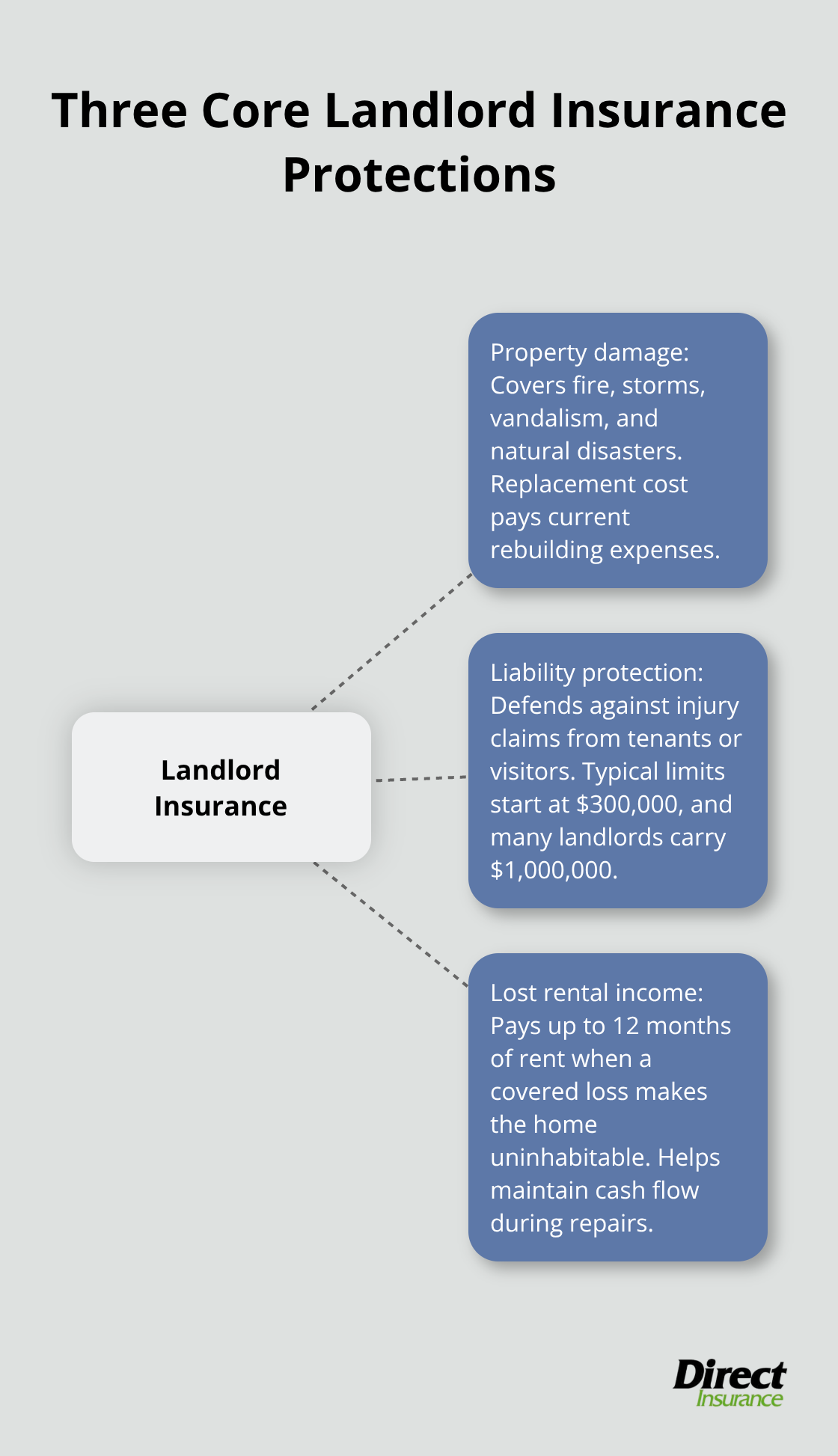

Landlord insurance delivers three essential protections that standard homeowners policies exclude. Property damage coverage protects your rental investment from fire, storms, vandalism, and natural disasters with replacement cost coverage that pays current rebuilding expenses rather than depreciated values. The Insurance Information Institute reports that 5.3 percent of insured homes had claims in 2023, making this protection vital for Utah landlords who face wildfire risks and severe weather patterns.

Property Damage Protection

Fire damage represents the most expensive risk for rental property owners. Replacement cost coverage pays full rebuilding expenses using current material prices, while actual cash value policies only reimburse depreciated amounts. Utah landlords who own older properties benefit most from replacement cost protection since construction costs have increased significantly in recent years. Natural disasters like hailstorms and windstorms cause extensive roof damage that can cost 15,000 to 30,000 dollars to repair without proper coverage.

Liability Protection Against Lawsuits

Liability coverage defends against expensive lawsuits when tenants or visitors suffer injuries on your property. This coverage typically starts at 300,000 dollars but smart landlords carry at least one million dollars given rising legal costs in Utah. Medical payments coverage handles immediate expenses for minor injuries and prevents small incidents from becoming major claims. Property owners face significant liability settlements according to recent industry data, making this coverage essential for serious investors.

Lost Rental Income Coverage

Loss of rental income protection compensates for monthly rent payments when covered damage makes your property uninhabitable. This coverage typically pays 12 months of lost rent while repairs occur and protects your cash flow during extended restoration periods. Utah landlords who collect 2,000 dollars monthly rent could lose 24,000 dollars during major repairs without this protection. The coverage activates immediately after covered incidents and continues until tenants can safely return or you find replacement renters.

Understanding these coverage types helps property owners evaluate their risk exposure, but legal requirements add another layer of complexity that varies significantly across Utah municipalities.

Legal Requirements and State Regulations

Utah state law does not mandate landlord insurance for rental properties, but mortgage lenders universally require comprehensive coverage before they approve financing. Banks typically demand dwelling coverage equal to the loan amount plus liability protection of at least 300,000 dollars to protect their investment. Fannie Mae and Freddie Mac guidelines require landlords to maintain continuous coverage throughout the loan term, and lapses trigger immediate lender notifications that can accelerate loan payments or force costly lender-placed insurance policies.

Mortgage Lender Insurance Requirements

Lenders impose stricter requirements than state law because they hold financial stakes in rental properties. Most require replacement cost coverage rather than actual cash value policies to protect against total losses. Utah landlords with investment property mortgages must provide annual insurance certificates that prove continuous coverage, and carriers require lender approval to maintain compliance when property owners switch policies. Lender-placed insurance costs three to five times more than standard policies and provides minimal coverage (often excluding liability protection), which makes voluntary compliance the smart financial choice for property owners.

Local Municipality Variations

Several Utah cities impose additional insurance requirements beyond state minimums. Salt Lake City requires rental property owners to carry at least 500,000 dollars in liability coverage for multi-unit properties, while Park City mandates one million dollars for short-term rental properties. These local ordinances often include specific coverage requirements for lead paint remediation, mold damage, and tenant displacement costs that standard policies exclude. Property owners who violate municipal insurance requirements face fines that range from 500 to 2,500 dollars plus potential rental license revocation.

Compliance Consequences

Smart landlords exceed minimum requirements because legal mandates represent baseline protection rather than adequate coverage for serious property investors. Most states grant landlords broad authority to set lease terms, including insurance-related requirements that protect their investments. The financial consequences of inadequate coverage extend far beyond legal compliance issues and create substantial risks that can destroy rental property investments.

Financial Risks of Going Without Coverage

Property owners who skip landlord insurance face catastrophic financial exposure that can destroy their investment portfolios overnight. Major property damage creates immediate out-of-pocket costs that average $25,000 to $75,000 for fire incidents and $15,000 to $40,000 for water damage according to recent insurance industry data. Utah landlords who experienced the 2020 windstorms paid average repair costs of $18,500 per property, while those with coverage paid only their deductibles. Legal defense costs compound these expenses rapidly, with tenant injury lawsuits that average $89,000 in settlements plus attorney fees before cases reach trial.

Massive Repair Bills That Bankrupt Landlords

Kitchen fires cause the most expensive single-incident damage to rental properties, with restoration costs that range from $35,000 to $85,000 depending on smoke and water damage extent. Utah’s dry climate creates additional fire risks that can consume entire properties within minutes, which leaves landlords with total reconstruction bills that exceed $200,000 for average single-family rentals. Water damage from burst pipes costs $8,000 to $15,000 per incident but grows exponentially when structural elements require replacement (mold remediation adds another $10,000 to $30,000 to repair expenses).

Liability Lawsuits That Devastate Finances

Slip and fall accidents generate the highest liability claims against rental property owners, with average settlements that reach $45,000 plus legal defense costs. Utah courts awarded a $340,000 judgment against a Park City landlord in 2023 after a tenant suffered serious injuries from defective stairs, which demonstrates how quickly liability exposure escalates beyond most property owners’ financial capacity. Legal defense costs run $150-$300 per hour for property attorneys, and discrimination lawsuits can exceed $25,000 in legal fees before they reach trial. Dog bite incidents on rental properties create additional liability exposure that averages $64,000 per claim according to the Insurance Information Institute.

Extended Income Loss During Repairs

Major property damage creates rental income interruptions that last 6 to 18 months for significant repairs, which forces landlords to continue mortgage payments without rental revenue while they cover temporary housing costs for displaced families. Utah landlords who collect $2,500 monthly rent lose $15,000 to $45,000 during extended restoration periods, and these losses compound when repair delays extend timelines beyond initial estimates. Property owners often discover that restoration costs exceed their available cash reserves (this creates situations where incomplete repairs prevent re-renting while mortgage obligations continue to accumulate).

Final Thoughts

The evidence overwhelmingly supports landlord insurance as essential protection for Utah property owners. While the question “do you have to have landlord insurance” has no universal legal mandate, the financial risks make coverage indispensable for serious investors. Utah landlords face unique challenges from wildfire risks, severe weather patterns, and construction costs that can destroy uninsured investments overnight.

Property damage averages $25,000 to $75,000 per incident, liability settlements reach $340,000, and rental income losses during extended repairs create financial exposure that exceeds most property owners’ capacity to self-insure. Smart landlords carry replacement cost coverage with at least one million dollars in liability protection. This investment protects against catastrophic losses while it maintains positive cash flow during covered incidents (the annual premium cost represents a fraction of potential out-of-pocket expenses from a single major claim).

We at Direct Insurance Services help Utah property owners evaluate their specific risk exposure and secure appropriate coverage. Our independent agency approach means we compare multiple options to find policies that fit your budget and protection needs. Contact our experienced team to review your current coverage and identify potential gaps before they become expensive problems.