Why Do Landlords Require Renters Insurance?

Most rental agreements now include a renters insurance requirement, leaving many tenants wondering about the reasoning behind this policy. Understanding why landlords require renters insurance helps both property owners and tenants make informed decisions.

We at Direct Insurance Services see this trend growing across Utah’s rental market. The benefits extend far beyond simple property protection, creating advantages for everyone involved in the rental relationship.

Why Do Property Owners Insist on Renters Insurance?

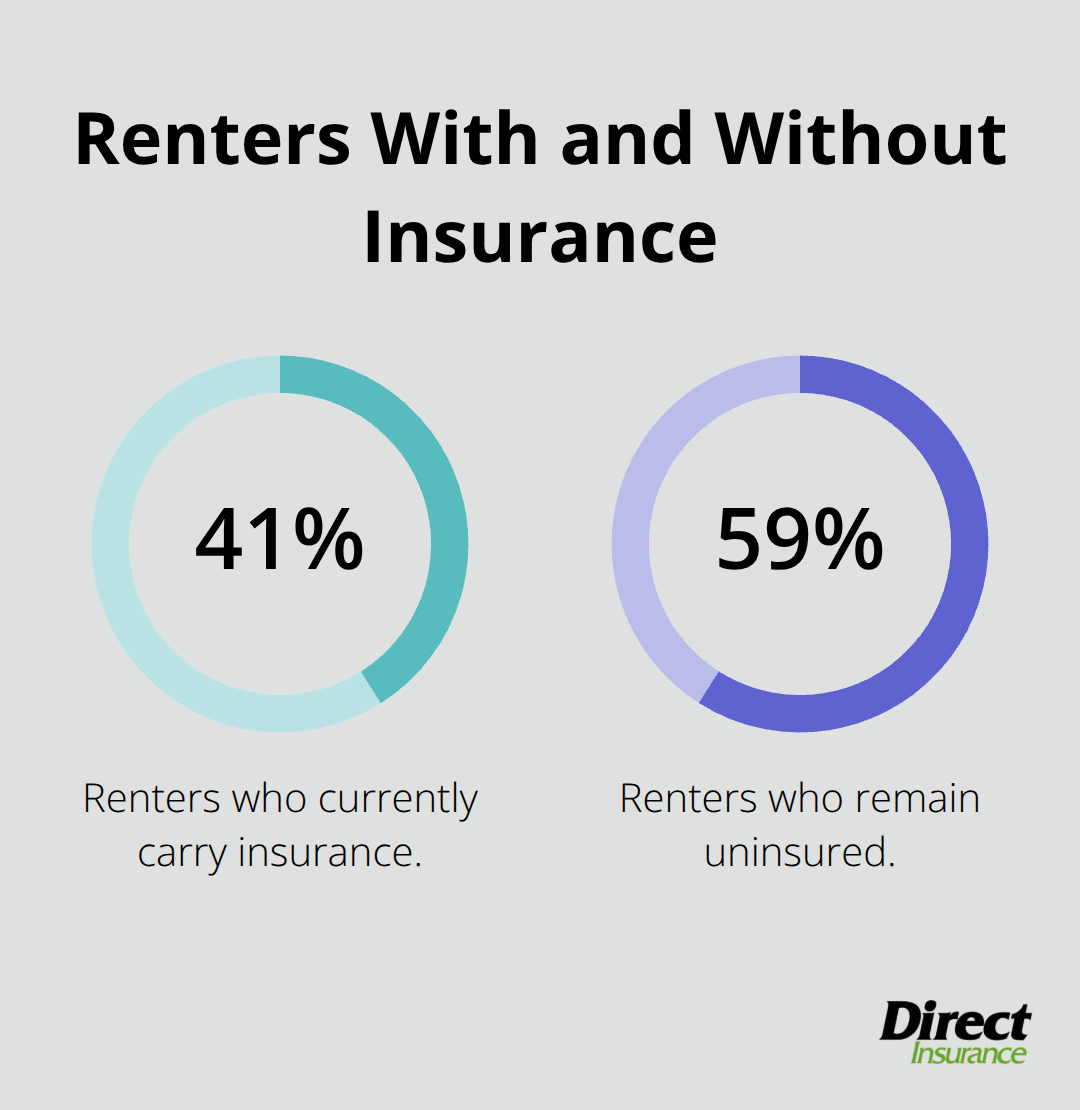

Property owners require renters insurance because it shields them from massive financial liability when tenant-related incidents occur. According to the Insurance Information Institute, approximately 41% of renters currently carry insurance, but landlords face serious exposure when the other 59% remain unprotected. When uninsured tenants cause kitchen fires, floods from bathtubs, or injuries to guests, landlords often become the primary target for lawsuits and damage claims.

Financial Protection Against Tenant Negligence

Smart landlords recognize that their property insurance won’t cover tenant-caused damages or liability claims from injured visitors. The National Association of Insurance Commissioners reports that renters insurance typically provides $100,000 to $500,000 in liability coverage, which protects landlords from costly legal battles. When tenants lack this protection, property owners face direct financial responsibility for guest injuries, property damage from tenant negligence, and legal defense costs that can reach tens of thousands of dollars per incident.

Tenant Responsibility Assessment Tool

The Urban Institute found that neighborhoods with higher renters insurance rates experience lower eviction rates, which makes insurance requirements an effective tenant assessment method. Approximately 81% of landlords believe a tenant’s willingness to obtain renters insurance significantly influences rental decisions. Tenants who proactively secure insurance demonstrate financial responsibility and commitment to property protection (which reduces the likelihood of rent defaults, property damage, and lease violations).

Risk Management Framework

Property owners use renters insurance requirements to create a powerful risk management system. When disasters strike and units become uninhabitable, insured tenants receive additional expense coverage that prevents them from breaking leases or demanding landlord compensation for temporary housing costs. This coverage protects landlords from lost rental income while maintaining positive tenant relationships during difficult circumstances.

The financial benefits extend beyond simple risk reduction, creating cost advantages that benefit both property owners and tenants in multiple ways.

What Does Renters Insurance Actually Cover

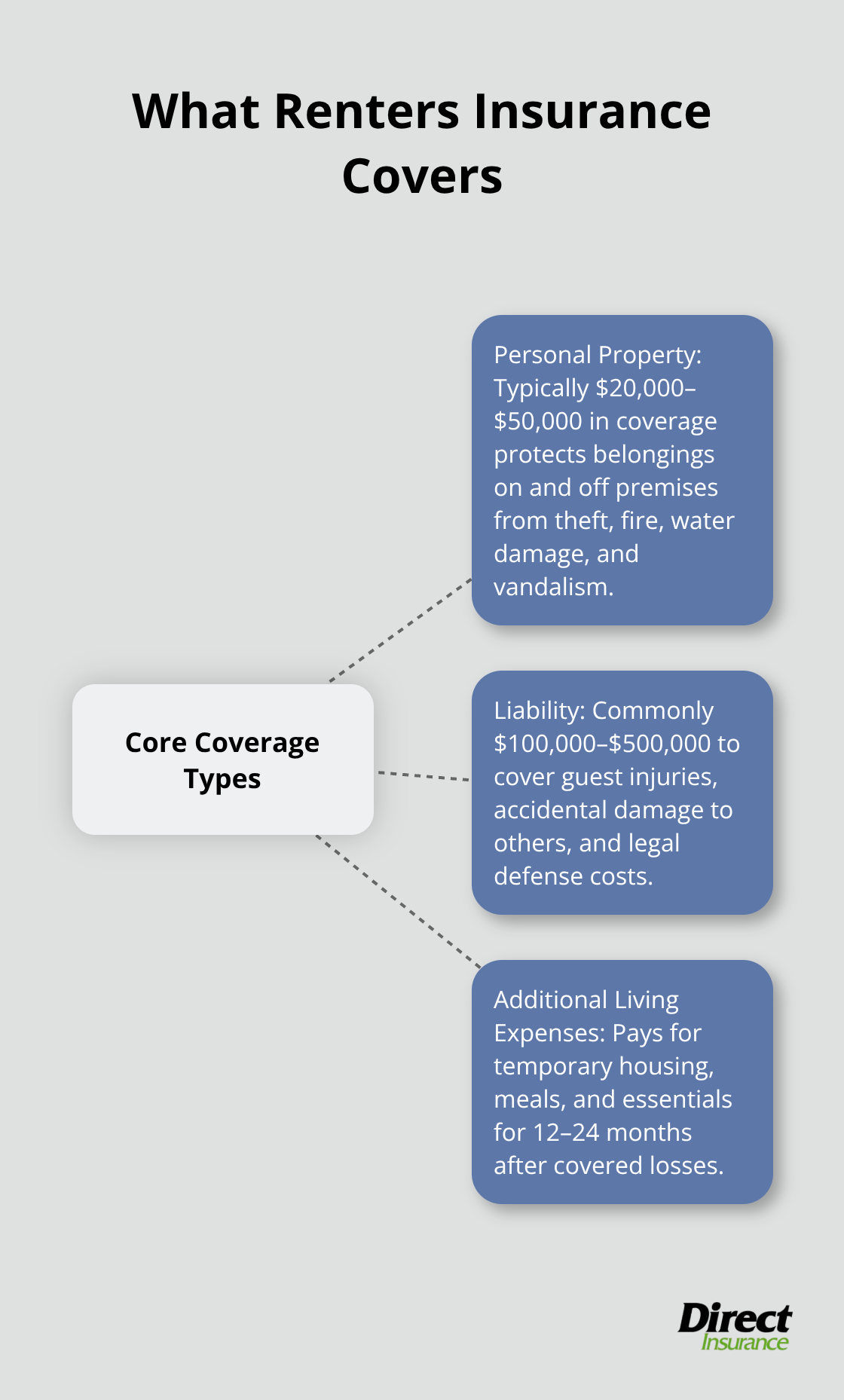

Renters insurance provides three essential coverage types that protect tenants from financial devastation while simultaneously shielding landlords from liability exposure. Personal property coverage typically ranges from $20,000 to $50,000 according to industry standards, protecting electronics, furniture, clothing, and other belongings from theft, fire, water damage, and vandalism. This coverage applies both inside and outside the rental unit, meaning stolen laptops from cars or damaged items during moves receive protection.

The Insurance Information Institute reports that replacement cost coverage costs only slightly more than actual cash value policies but provides significantly better protection since it replaces items at current market prices rather than depreciated values.

Liability Protection Beyond Property Damage

Personal liability coverage represents the most valuable component for both tenants and landlords, typically providing $100,000 to $500,000 in protection against lawsuits from guest injuries, accidental property damage to neighboring units, and legal defense costs. When tenants accidentally cause kitchen fires that spread to adjacent apartments or when dinner party guests slip on wet floors, this coverage handles medical bills, legal fees, and damage settlements.

Medical payments coverage within renters policies automatically covers minor guest injuries up to $5,000 without requiring fault determination (which prevents small incidents from becoming major legal disputes).

Emergency Housing and Living Expenses

Additional living expense coverage pays for temporary housing, meals, and other necessary costs when rental units become uninhabitable due to covered losses like fires or severe water damage. This coverage typically provides 12 to 24 months of assistance, preventing tenants from breaking leases or demanding landlord compensation during displacement periods.

The National Association of Insurance Commissioners confirms this coverage maintains rental income for property owners while keeping responsible tenants in their units long-term (creating stability that benefits everyone involved).

These comprehensive protections create significant financial advantages that extend beyond basic coverage, generating cost savings and risk reduction benefits for both landlords and tenants.

How Much Money Does Renters Insurance Actually Save?

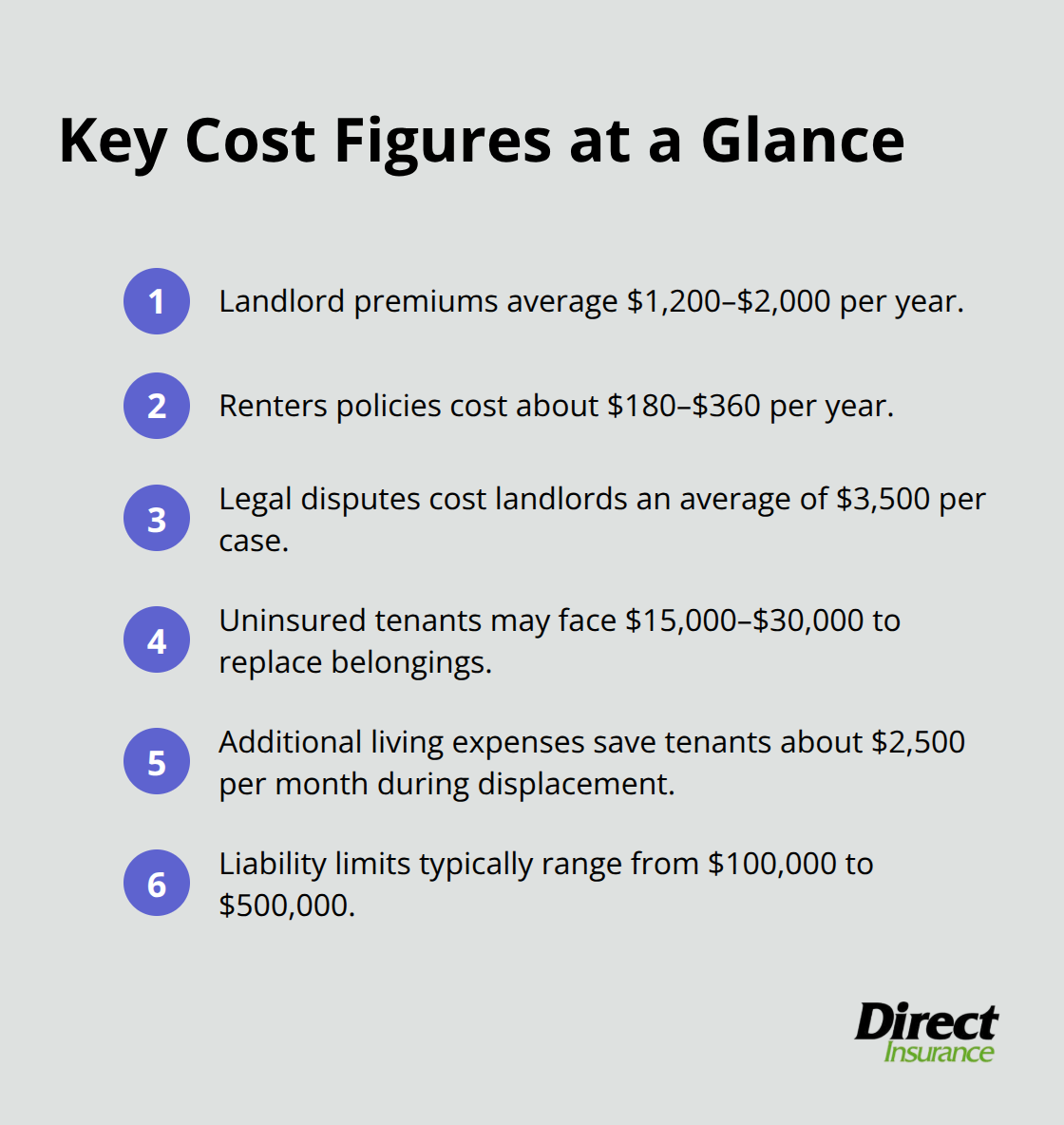

Renters insurance creates measurable cost savings that reach thousands of dollars annually for both landlords and tenants through reduced claims frequency and liability protection. According to Progressive, landlords with tenant insurance requirements benefit from having tenants carry coverage because both parties need protection in the event of a covered loss. The Insurance Information Institute reports that landlord policies cost significantly more than renters insurance, with property owner premiums that average $1,200 to $2,000 annually while tenant policies cost just $180 to $360 per year.

Legal Costs Drop Dramatically with Insurance Coverage

Legal disputes between landlords and tenants cost property owners an average of $3,500 per case according to the American Apartment Owners Association, but renters insurance virtually eliminates these expensive conflicts. When tenants carry $300,000 liability policies, guest injury claims get resolved through insurance companies rather than costly court battles that can stretch for months. Property owners avoid legal defense fees, settlement payments, and lost rental income during prolonged disputes because insurance adjusters handle claims professionally and efficiently.

Tenants Avoid Catastrophic Financial Losses

Tenants without insurance face devastating out-of-pocket expenses when disasters destroy their belongings (often spending $15,000 to $30,000 to replace furniture, electronics, and clothing after fires or theft incidents). Renters policies with replacement cost coverage eliminate these financial shocks by paying current market prices for damaged items rather than depreciated values that leave coverage gaps. The National Association of Insurance Commissioners confirms that additional living expense coverage saves tenants an average of $2,500 monthly during displacement periods.

Property Owners Reduce Insurance Claim Frequency

Landlords see immediate premium benefits when tenants carry their own insurance policies because fewer claims against property insurance translate to lower renewal rates and better carrier relationships. Insurance companies reward property owners who require tenant coverage with preferred pricing tiers and reduced deductibles (recognizing the decreased risk profile these requirements create). Landlord insurance premiums run 25% higher than homeowners policies, making tenant insurance requirements even more valuable for cost control.

Final Thoughts

Property owners require renters insurance because it creates a protective barrier that shields them from massive liability exposure while tenants receive comprehensive financial protection. The evidence demonstrates clear advantages for both parties in rental relationships. Landlords avoid expensive legal disputes and maintain stable income streams while tenants protect their belongings and receive emergency assistance during disasters.

Coverage limits play a vital role when tenants select policies that meet landlord requirements. Tenants should choose liability coverage between $300,000 and $500,000 to provide adequate protection, while personal property limits must reflect actual belongings value. Higher coverage costs only slightly more but prevents devastating financial gaps during major losses (which can reach tens of thousands of dollars).

We at Direct Insurance Services help Utah renters find affordable policies that satisfy landlord requirements while providing comprehensive protection. Our independent agency works with top-rated carriers to deliver personalized coverage solutions. We make the insurance process straightforward for both tenants and property owners across Utah’s rental market.