Can a Landlord Force You to Get Renters Insurance?

Many renters face this question when signing lease agreements: can a landlord force you to get renters insurance? The answer varies by state and lease terms.

We at Direct Insurance Services see this confusion regularly among Utah tenants. Understanding your rights and obligations helps you make informed decisions about rental coverage requirements.

Legal Rights and Requirements for Renters Insurance

State Laws Create the Foundation for Insurance Requirements

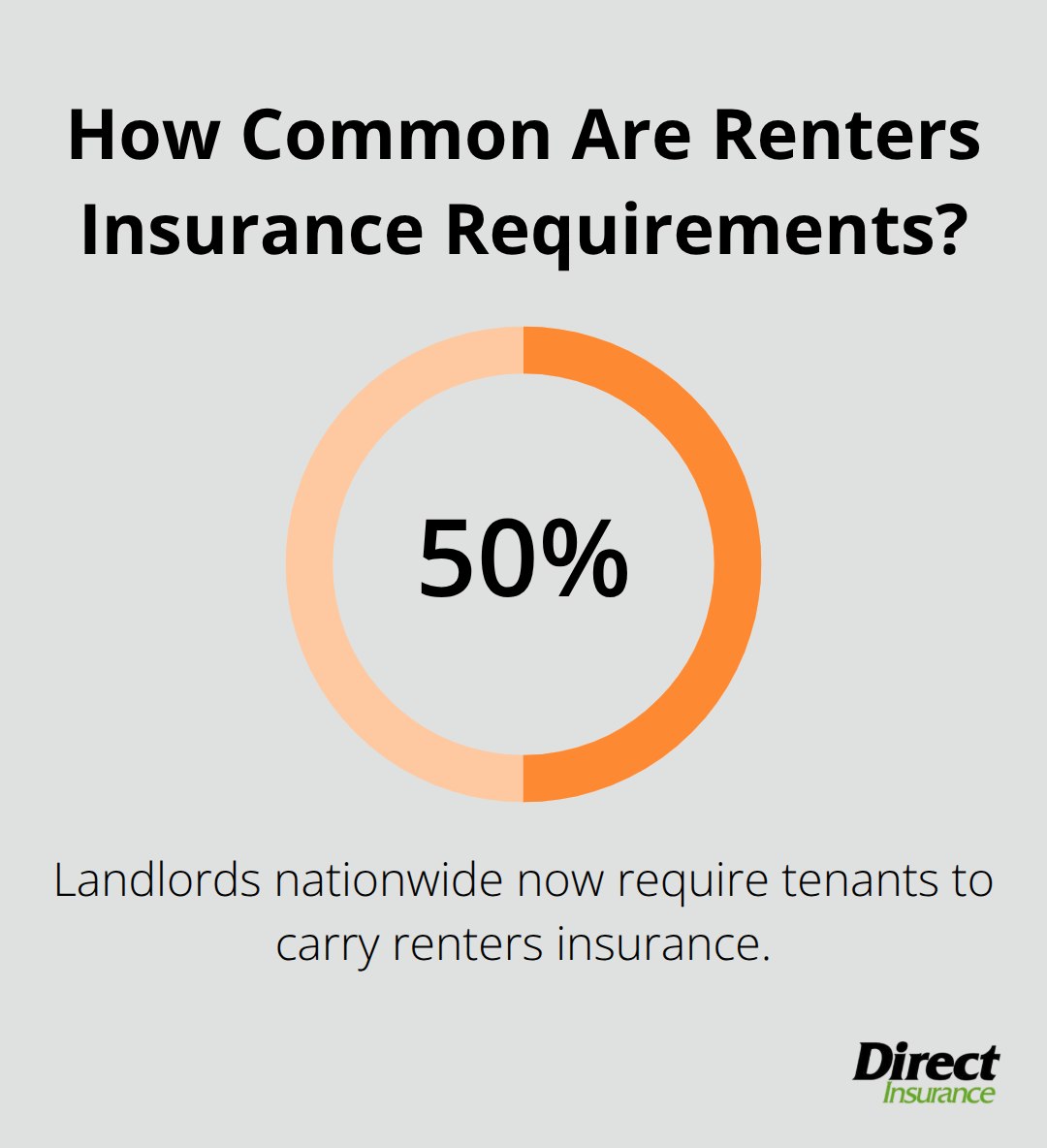

No state law mandates renters insurance, which leaves individual states to regulate these requirements. Most states grant landlords broad authority to include insurance mandates in lease agreements. The National Association of Insurance Commissioners reports that approximately 50% of landlords nationwide now require tenants to carry renters insurance.

Utah follows this trend and permits landlords to mandate coverage as a lease condition. State law requires landlords to include these requirements in the original lease agreement rather than add them mid-lease without tenant consent.

Landlords Exercise Strong Legal Authority Over Coverage

Property owners can legally require minimum coverage amounts (typically $100,000 to $300,000 in liability protection). The Insurance Information Institute reports that landlords face significant financial exposure when tenants lack coverage, particularly for water damage claims that average $10,000 per incident.

Smart landlords specify exact coverage requirements in lease documents and name themselves as additional interested parties on policies. This practice protects their investment while it transfers liability risks to tenants. Tenants who refuse to obtain required insurance violate their lease terms and face potential eviction proceedings.

Tenant Rights Provide Some Protection

Tenants cannot be forced to purchase insurance from specific companies and maintain the right to shop for competitive rates. The average monthly cost of $15 to $30 makes this requirement reasonable in most courts. Landlords must provide adequate notice before they implement new insurance requirements (typically 30 days minimum).

Existing tenants cannot be compelled to add insurance mid-lease unless the original agreement included provisions for policy updates. Documentation becomes vital when disputes arise, which makes thorough lease review necessary before tenants sign any rental agreement.

The next consideration involves understanding how renters insurance actually benefits tenants beyond just meeting landlord requirements.

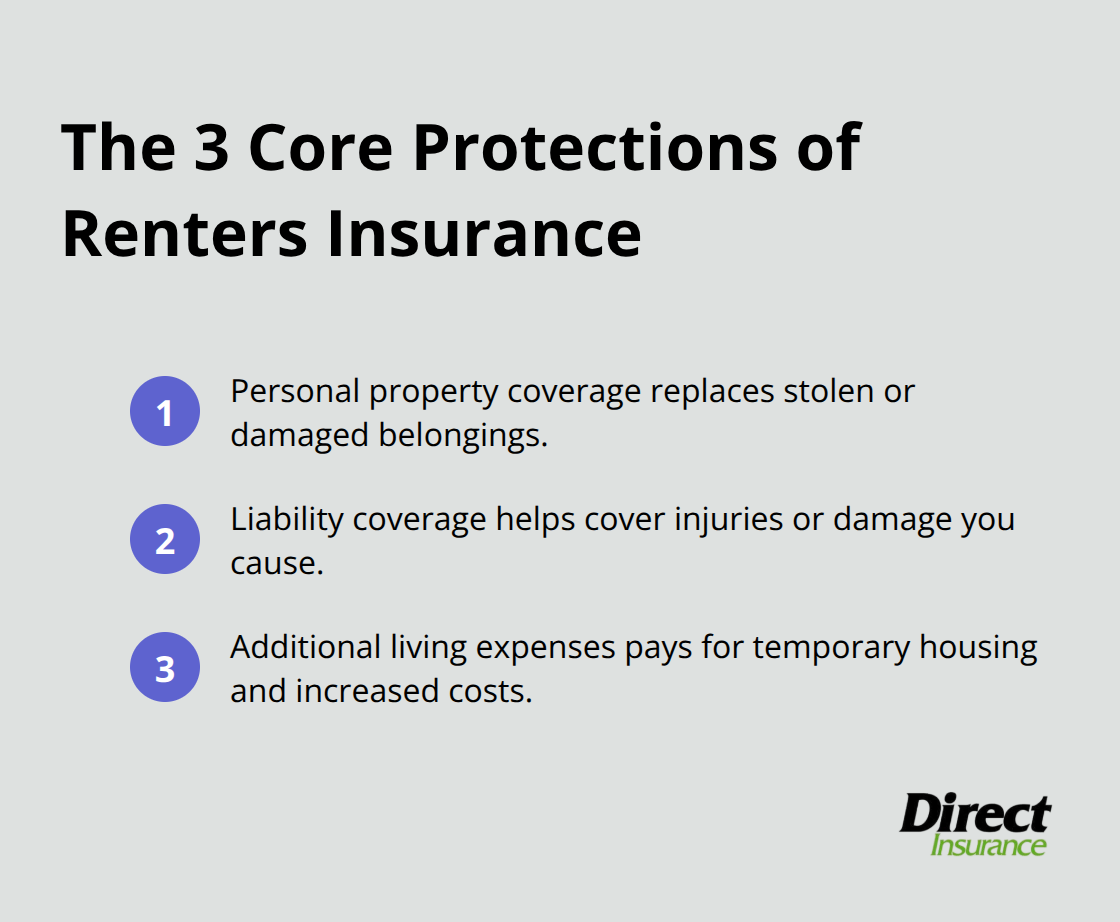

What Financial Protection Does Renters Insurance Actually Provide

Renters insurance delivers three major financial protections that make the monthly cost worthwhile. Personal property coverage protects belongings worth far more than most tenants realize. The Insurance Information Institute found that 80% of renters underestimate their personal property value by thousands of dollars.

A typical renter owns $20,000 to $40,000 in belongings (electronics, clothing, furniture, and appliances). Without coverage, replacement after a fire or theft creates devastating financial hardship.

Personal Property Coverage Protects Your Investment

Standard renters policies cover personal belongings at replacement cost rather than depreciated value. This means you receive enough money to buy new items rather than used equivalents. Coverage typically ranges from $15,000 to $50,000 for personal property. Theft claims account for 31% of all renters insurance claims according to the National Association of Insurance Commissioners, with average payouts that exceed $2,500 per incident. Electronics, jewelry, and sports equipment face the highest theft risks.

Liability Protection Prevents Financial Ruin

Liability coverage protects against lawsuits when accidents happen in your rental unit or when you accidentally damage someone else’s property. Medical payments to others coverage handles minor injuries without liability claims. Most insurance companies offer three standard choices for personal liability coverage limits: $100,000, $300,000, or $500,000. A single slip-and-fall lawsuit can cost $50,000 or more in legal fees and damages. Pet-related incidents generate significant liability exposure, with dog bite claims that average $64,555 (according to the Insurance Information Institute).

Additional Living Expenses Coverage Prevents Displacement Hardship

When fire, water damage, or other covered perils make your rental uninhabitable, additional living expenses coverage pays for temporary housing and increased costs. This coverage typically provides 20% of your personal property limit for hotel bills, restaurant meals, and moving expenses. Average displacement periods last 6 to 12 months for major damage incidents. Without this protection, tenants face impossible choices between financial ruin and homelessness during property repairs.

These financial protections become even more important when you consider what happens if you refuse to obtain required coverage.

What Happens If You Refuse Required Renters Insurance

Tenants who refuse landlord-mandated renters insurance face immediate lease violations with serious financial consequences. Landlords typically provide 30-day cure periods for insurance compliance, but tenants who fail to obtain coverage face eviction proceedings. The National Association of Insurance Commissioners reports that insurance-related lease violations account for 12% of all eviction cases nationwide. Utah courts consistently side with landlords when tenants violate clearly stated insurance requirements, which makes refusal a high-risk strategy that rarely succeeds.

Eviction Proceedings Move Fast Without Insurance Compliance

Eviction for insurance non-compliance follows accelerated timelines compared to rent-related evictions. Utah law permits landlords to file eviction notices within 3 days of insurance requirement violations. Legal fees for eviction defense average $2,500 to $5,000 (according to the Utah State Bar Association), while successful evictions create permanent rental history marks that prevent future housing approvals. Credit scores drop 50 to 130 points from eviction judgments, and most property management companies automatically reject applicants with eviction records. When surveyed, 56 percent of landlords reject at least 25 percent of applicants.

Alternative Solutions Require Strategic Timing

Smart tenants negotiate insurance alternatives before they sign leases rather than after violations occur. Some landlords accept higher security deposits (typically 2-3 months rent) instead of insurance requirements, though this approach costs more than annual premiums. Tenant-paid master policies represent another option where landlords purchase coverage and tenants reimburse costs monthly. Successful negotiations happen when tenants propose equivalent coverage through existing policies or demonstrate financial capacity to self-insure property damage risks. Documentation becomes critical for any alternative arrangements, and verbal agreements provide zero legal protection during disputes.

Final Thoughts

The question “can a landlord force you to get renters insurance” has a clear answer: yes, landlords possess legal authority to mandate coverage as a lease condition in Utah and most states. Property owners can specify minimum coverage amounts, require policy documentation, and pursue eviction for non-compliance. Tenants retain rights to shop for competitive rates and cannot be forced to purchase from specific insurers.

Lease agreements prevent costly surprises and legal disputes when tenants understand insurance requirements before they sign. Insurance requirements must appear in original lease documents, and landlords cannot add mandates mid-lease without tenant consent. The average monthly cost of $15 to $30 makes compliance far more affordable than eviction consequences or property replacement costs.

Utah renters benefit when they review insurance options before lease execution rather than scramble after violations occur. We at Direct Insurance Services help Utah tenants find affordable renters insurance that meets landlord requirements while it protects personal property and liability exposure. Contact our experienced team for personalized coverage solutions that fit your budget and rental situation (smart tenants recognize that renters insurance protects their financial future beyond just lease obligations).