Landlord Home Insurance: Protecting Your Rental Property

Owning rental property comes with unique risks that standard homeowners insurance won’t cover. Landlord home insurance protects your investment from tenant-related damages, liability claims, and lost rental income.

We at Direct Insurance Services see property owners face costly surprises when they rely on inadequate coverage. The right policy safeguards both your physical property and your rental business income.

Why Landlord Insurance Differs From Regular Homeowners Coverage

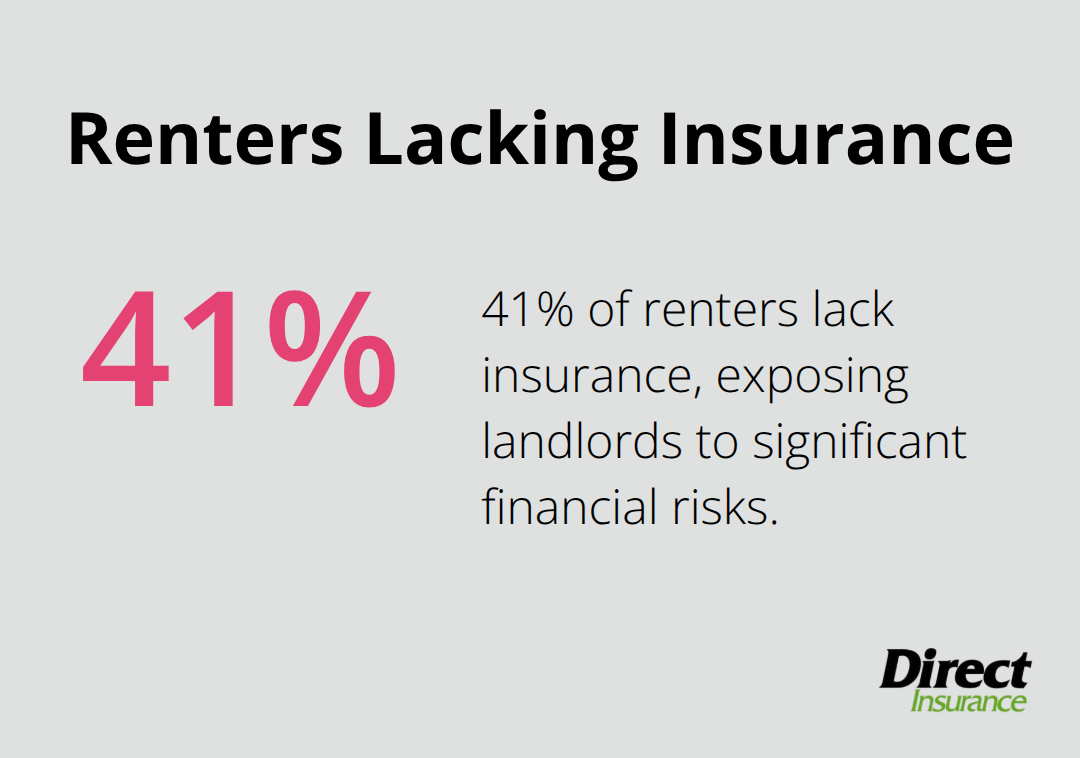

Homeowners insurance becomes inadequate the moment you rent out your property. Standard policies explicitly exclude coverage for tenant-related damages, liability claims from renters, and business activities like rent collection. The Insurance Information Institute reports that 41% of renters lack insurance, which leaves landlords exposed to significant financial risks when tenant belongings cause damage or liability issues arise.

Property Damage Protection Beyond Basic Coverage

Landlord insurance covers intentional and accidental tenant damage that homeowners policies reject. Your standard policy might cover a kitchen fire from faulty wiring, but it won’t pay for tenant-caused grease fires or damage from unauthorized pets. Property owners face repair bills that average $3,000 to $8,000 for tenant damage that homeowners insurance won’t touch. Dwelling coverage in landlord policies specifically addresses wear and tear from multiple occupants (something residential policies consider normal use exclusions).

Loss of Rental Income Coverage Protects Your Cash Flow

Landlords frequently experience rental income loss due to property damage. Landlord policies include coverage for lost rent when your property becomes uninhabitable from covered perils. If a pipe burst makes your rental unlivable for two months, this coverage pays your mortgage and expenses while repairs happen. Standard homeowners insurance provides zero protection for lost rental income, which leaves property owners to absorb these costs entirely.

Liability Coverage Handles Tenant and Guest Injuries

Liability limits in landlord policies start at $100,000, but experts recommend $1 million coverage minimum. When tenants or their guests suffer injuries on your property, landlord insurance covers medical expenses and legal fees. A slip-and-fall lawsuit can easily exceed $50,000 in medical costs alone (homeowners policies may deny these claims entirely if they determine the incident relates to your rental business rather than personal residence use).

These coverage differences highlight why landlords need specialized protection, but the specific types of coverage within your policy determine how well your investment stays protected.

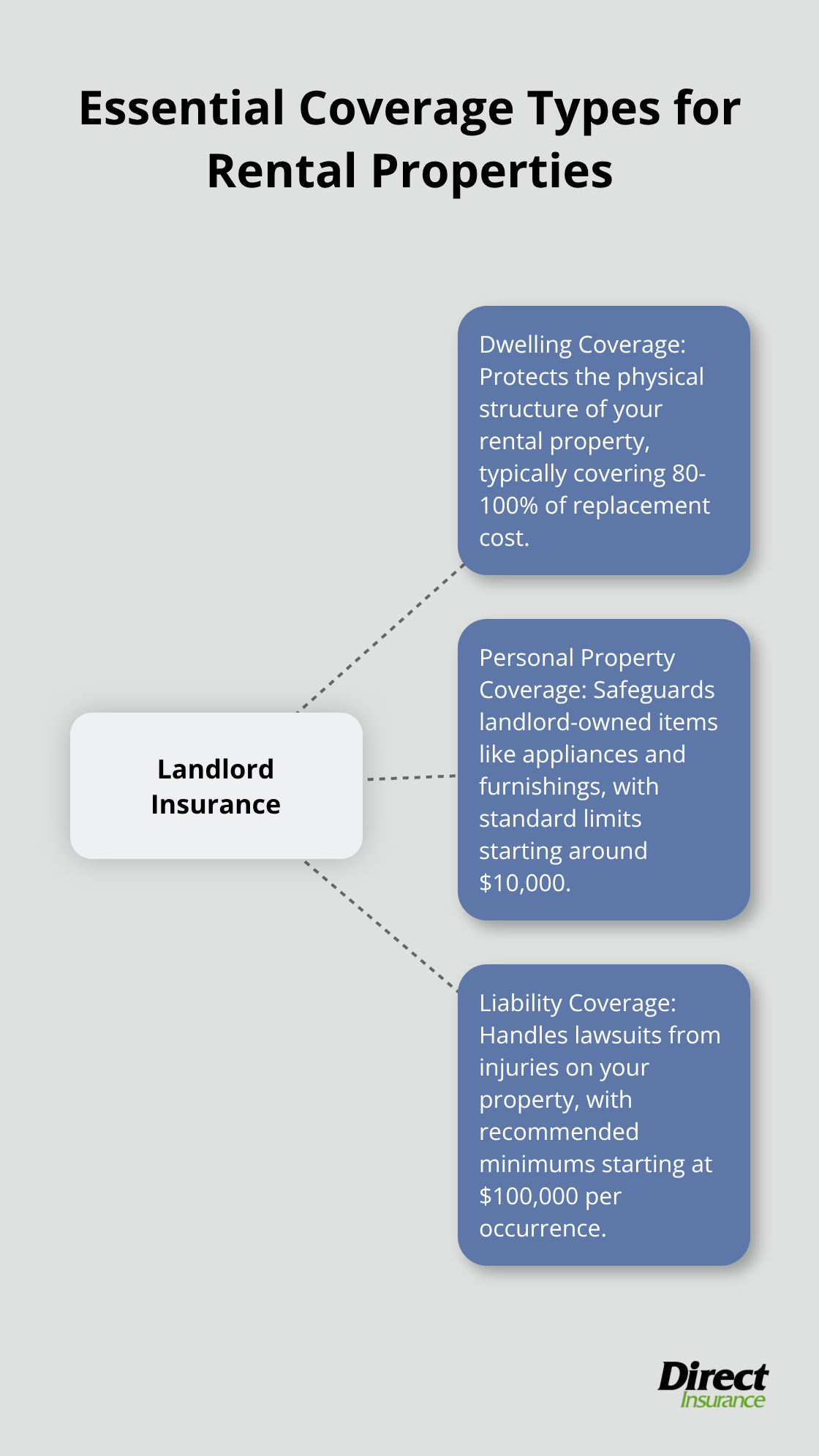

Essential Coverage Types for Rental Properties

Landlord policies contain three essential coverage components that determine whether your rental investment survives major incidents or drains your finances. Each coverage type addresses specific risks that property owners face when they rent to tenants.

Dwelling Coverage Protects Your Physical Structure

Dwelling coverage protects the physical structure and represents your largest coverage need. Most policies require limits between 80% and 100% of your property’s replacement cost. Insurers typically use replacement cost coverage rather than actual cash value, which means you receive funds to rebuild without depreciation deductions.

Properties built before 1980 often need building code upgrade coverage since current construction standards differ significantly from older requirements. This endorsement covers the additional costs to bring damaged structures up to current codes (which can add $50,000 or more to reconstruction expenses). Modern fire safety requirements, electrical codes, and accessibility standards create substantial upgrade costs that basic dwelling coverage won’t address.

Personal Property Coverage for Landlord-Owned Items

Personal property coverage protects appliances, fixtures, and furnishings you provide as the landlord. Standard limits start around $10,000, but property owners with furnished rentals need much higher limits. A fully furnished rental can contain $25,000 to $40,000 in landlord-owned items that tenant damage or theft can destroy.

This coverage excludes tenant possessions entirely, which makes tenant insurance requirements non-negotiable for your protection. Smart landlords require proof of tenant insurance before lease execution and add themselves as additional interested parties to receive cancellation notices.

Liability Coverage Determines Your Financial Protection

Liability coverage handles lawsuits from injuries on your property, with recommended minimums starting at $100,000 per occurrence. Legal defense costs alone average $15,000 to $25,000 per claim according to industry data, even when you win the case.

Medical payments coverage provides immediate payment for minor injuries without fault determination. This coverage typically handles amounts between $1,000 and $5,000 per person and prevents small incidents from escalating into major lawsuits since injured parties receive prompt medical expense reimbursement.

Properties with swimming pools, trampolines, or other attractive nuisances need higher liability limits since these features increase injury risks substantially. The cost differences between adequate and inadequate liability coverage pale compared to the financial devastation a single lawsuit can create.

Your premium costs depend on multiple factors that insurers evaluate when they price your specific policy.

What Drives Your Landlord Insurance Costs

Insurance companies analyze multiple risk factors when they price landlord policies. Property owners who understand these variables make strategic decisions that reduce premiums. Location stands as the most significant cost driver, with properties in high-crime areas carrying higher premiums than identical properties in safer neighborhoods.

Chicago landlords face average premiums between $2,400 and $6,600 for a three-unit property according to Steadily, while similar properties in lower-risk areas cost substantially less. Crime statistics, natural disaster frequency, and local lawsuit trends all influence regional models that insurers use to calculate base rates.

Property Type and Unit Count Impact Premium Structure

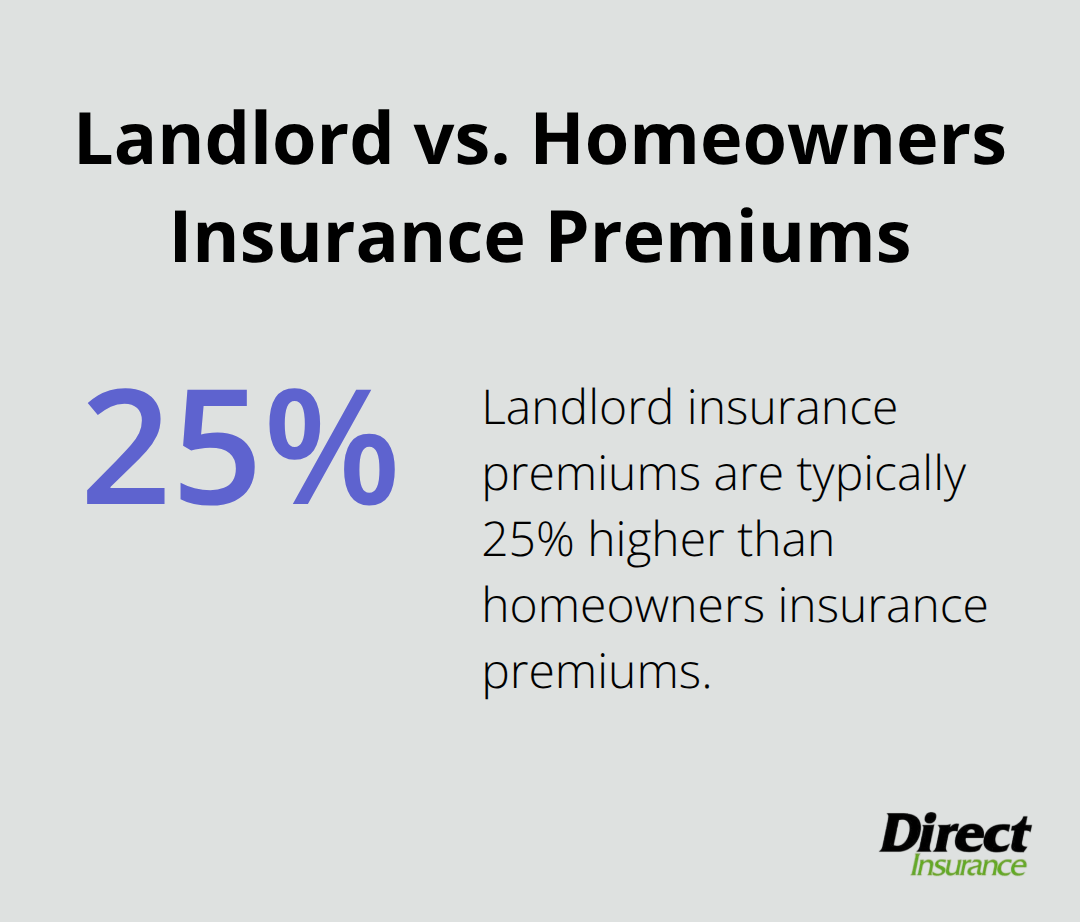

Single-family rentals typically cost 25% more than homeowners insurance. The Insurance Information Institute reports average landlord premiums at $1,478 versus $1,192 for homeowners coverage. Multi-unit properties face exponentially higher costs because each additional unit multiplies liability exposure and damage potential.

Older buildings built before 1980 carry premium surcharges of 15% to 30% due to outdated electrical systems, plumbing, and building materials that increase claim frequency. Properties with swimming pools, detached structures, or commercial spaces within residential buildings face additional premium increases that reflect their elevated risk profiles.

Tenant Screening Practices Reduce Insurance Costs

Insurers reward landlords who implement thorough tenant screening with premium discounts of 5% to 15%. Properties with consistent long-term tenants demonstrate lower claim rates than those with frequent turnover, which creates opportunities for rate reductions during policy renewals.

Professional property management companies often negotiate group discounts with carriers, though self-managed properties can achieve similar savings through proactive maintenance documentation and tenant insurance requirements that demonstrate risk management commitment to underwriters.

Safety Features Lower Premium Costs

Property owners who install security systems, smoke detectors, and central monitoring systems can reduce premiums by 10% to 20% according to claims data from major insurers. Hardwired smoke detectors save landlords between 5% to 20% on their insurance premiums based on industry data.

Upgrading roofs to impact-resistant materials can potentially lead to premium savings of 10% to 20% by reducing storm damage risk. These safety investments pay for themselves through reduced premiums while protecting your property investment.

Final Thoughts

Landlord home insurance delivers protection that standard homeowners policies cannot match. Property owners who invest in proper coverage shield themselves from tenant damage, liability lawsuits, and lost rental income that can devastate their financial stability. The specialized coverage components work together to protect your investment from risks that regular policies exclude entirely.

Independent agents offer access to multiple carriers and can compare coverage options that captive agents cannot provide. They understand local market conditions and can identify discounts for safety features, tenant screening practices, and bundled policies that reduce your overall costs. Professional guidance helps you avoid coverage gaps that leave your rental property exposed to financial losses.

We at Direct Insurance Services work with top-rated carriers to find comprehensive insurance solutions that fit your specific property needs and budget. Our independent approach means you receive unbiased advice without pressure to accept inadequate coverage. Document your property value, rental income, and current safety features, then contact an independent agent to review quotes from multiple carriers and identify the coverage limits that protect your investment.