Do I Need Both Landlord and Homeowners Insurance?

Property owners often ask: “Do I need landlord insurance and homeowners insurance?” The answer depends entirely on how you use your property.

We at Direct Insurance Services see this confusion daily. Homeowners insurance protects owner-occupied homes, while landlord insurance covers rental properties.

Most people need only one policy type, but some situations require switching from homeowners to landlord coverage.

What Coverage Gaps Exist Between These Policies

Homeowners and landlord insurance share basic property protection, but their coverage models differ fundamentally. Both policies cover dwelling damage from fire, storms, and vandalism. Both provide liability protection when someone gets injured on your property. Personal property coverage exists in both, though landlord policies typically cover only appliances and fixtures you provide as the owner.

Standard Homeowners Insurance Excludes Rental Activities

Standard homeowners policies contain specific exclusions that void coverage the moment you collect rent. The Insurance Information Institute reports that homeowners insurance becomes invalid when you rent to anyone (including family members). Most policies explicitly exclude business activities, and rent collection qualifies as business use.

Claims get denied for any damage that occurs while tenants occupy the property. Your insurer will investigate occupancy status during claims, and misrepresentation can result in policy cancellation plus claim denial. This exclusion applies even for short-term rentals or occasional rent collection.

Landlord Insurance Addresses Rental-Specific Risks

Landlord policies include loss of rental income coverage, which pays for lost rent when covered damage makes your property uninhabitable. Liability limits start at $1 million per occurrence compared to the typical $300,000 in homeowners policies. This higher coverage reflects increased lawsuit risks from tenant injuries.

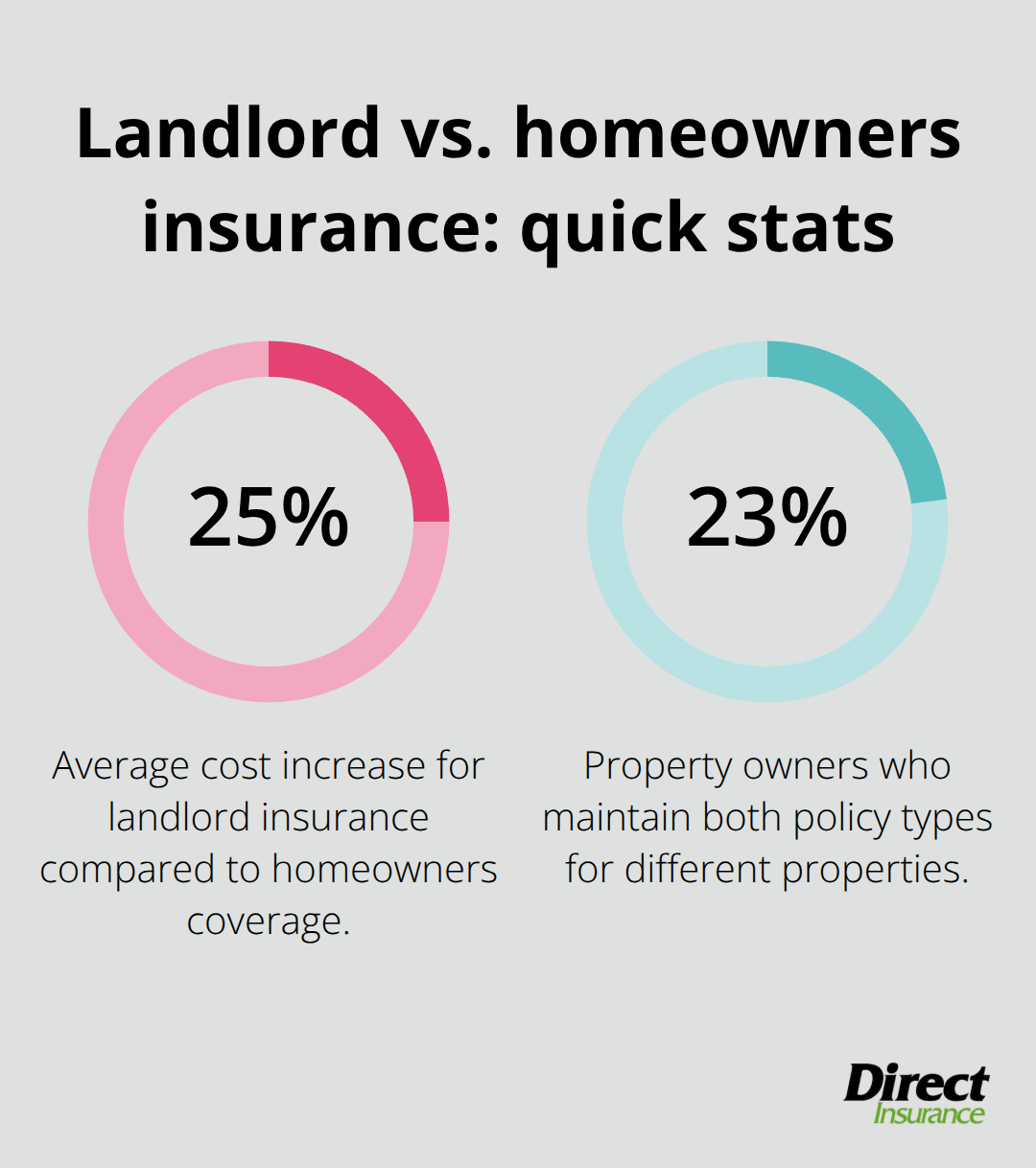

Landlord insurance costs average 25% more than homeowners coverage, with premiums that reach $1,500 annually versus $1,200 for standard homeowners policies. The National Association of Insurance Commissioners found that 23% of property owners maintain both policy types for different properties.

You Cannot Carry Both Policies on the Same Property

Insurance companies prohibit dual coverage on a single property. You must choose either homeowners or landlord insurance based on how you use the property. This restriction prevents coverage conflicts and potential fraud issues.

The transition from homeowners to landlord insurance becomes necessary the moment you decide to rent your property, which leads us to examine specific situations that require this policy switch.

When Your Property Requires Landlord Coverage

Property owners face three specific situations where they must switch from homeowners to landlord insurance. The first occurs when you rent out your current home while you move elsewhere. Your homeowners policy terminates coverage the moment you collect rent from tenants, regardless of rental duration. Even month-to-month arrangements or rentals to family members trigger this requirement. Properties rented for six months or longer always need landlord coverage, while shorter rentals may qualify for temporary endorsements (depending on your insurer).

Investment Properties Need Specialized Protection

Investment properties purchased specifically for rental income require landlord insurance from day one. Standard homeowners policies never apply to non-owner-occupied properties. Landlord insurance can help ensure that you protect yourself against the costs of property damage and personal injury to a tenant or a visitor to your property. These properties need substantial liability coverage compared to typical homeowners policies. Mortgage lenders typically require landlord insurance before they approve investment property loans, which makes this coverage a financing necessity rather than just a protection choice.

Home Conversions Create Immediate Coverage Gaps

Property owners who convert their primary residence to a rental property create the most dangerous coverage gap. Your existing homeowners policy becomes void immediately upon tenant occupancy, which leaves you completely unprotected until landlord coverage begins. Properties left vacant during this transition face additional risks (with most insurers that cancel coverage after 30-60 days of vacancy). You should secure landlord insurance before you list your property to avoid any coverage interruptions.

The transition process requires you to notify your current insurer about the change and shop for landlord policies that match your property’s rental timeline and tenant demographics. These coverage requirements directly impact your insurance costs, which vary significantly between policy types.

How Much More Does Landlord Insurance Cost

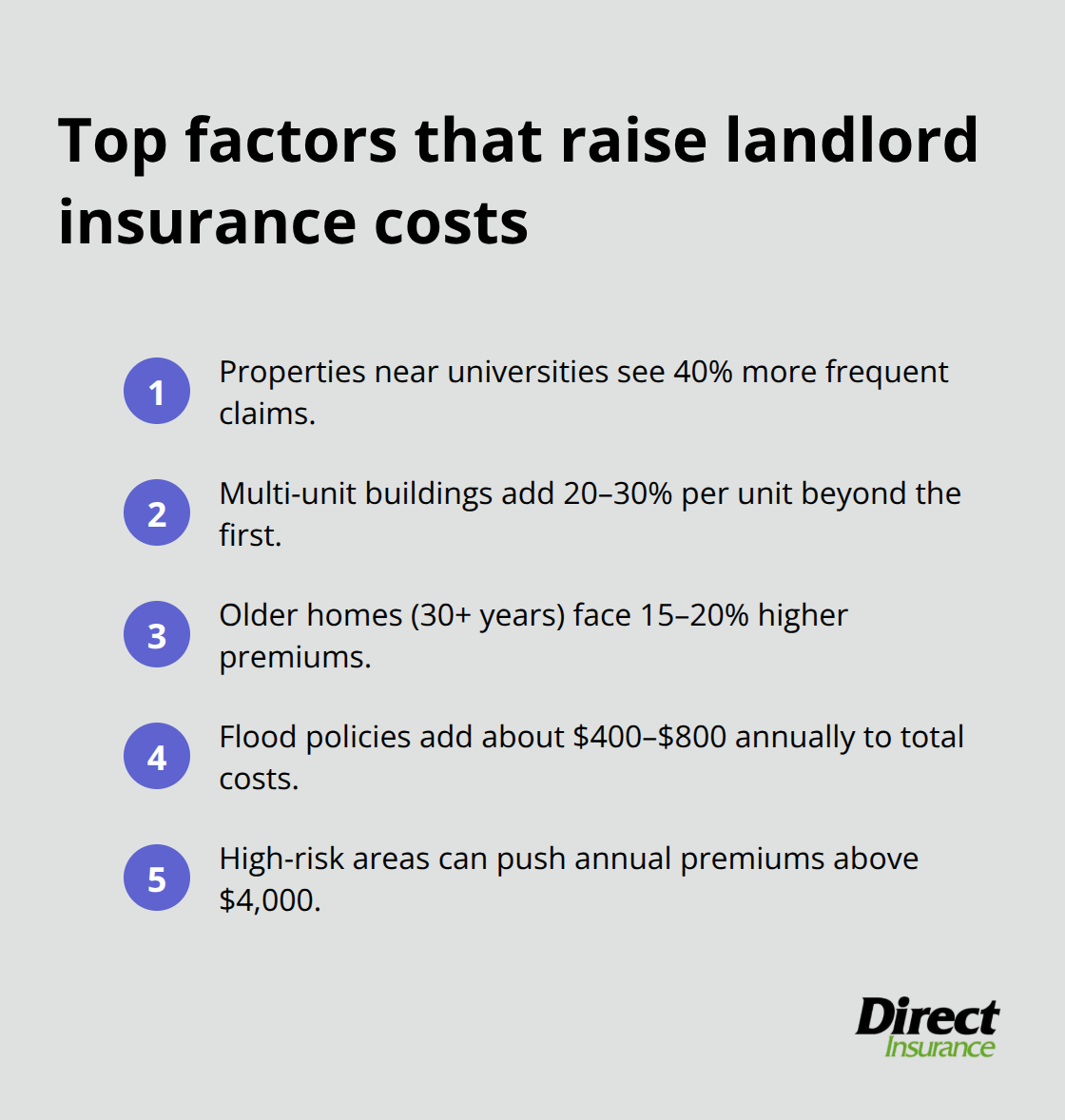

Landlord insurance generally costs about 25 percent more than standard homeowners coverage, with premiums averaging $1,500 annually compared to $1,200 for homeowners policies. This premium difference reflects the higher risks that rental properties carry, including increased liability exposure and potential tenant-related damages. Properties in high-risk areas can see landlord insurance costs that exceed $4,000 annually, while older properties (over 30 years) typically face 15-20% higher premiums due to outdated infrastructure.

Location and Property Type Drive Premium Variations

The location significantly impacts your rates, with college town properties that command higher rates due to increased turnover and damage risks from younger tenants. Properties near universities see claims 40% more frequently than standard residential areas.

Multi-unit buildings face additional premium increases of 20-30% per unit beyond the first rental unit. Coastal properties and flood-prone areas require separate flood insurance policies that add $400-800 annually to your total insurance costs.

Liability Coverage Requirements Demand Higher Limits

Standard homeowners policies provide $300,000 in liability coverage, but landlord insurance typically starts at $1 million per occurrence due to increased lawsuit risks from tenant injuries. Property owners face substantially higher legal exposure when they rent, as tenants and their guests can pursue claims for slip-and-fall accidents, inadequate maintenance, or property defects. Most rental properties need $2 million in liability coverage, particularly those with swimming pools, stairs, or other high-risk features. The additional premium for higher liability limits remains relatively modest compared to the financial protection it provides.

Essential Add-On Coverage Options Protect Your Investment

Loss of rental income coverage compensates landlords when covered damage makes properties uninhabitable (typically covers 12 months of lost rent). This coverage costs approximately $50-100 annually but can save thousands in lost rental income. Vandalism endorsements protect against intentional damage in high-risk neighborhoods, while vacant property endorsements maintain coverage during extended vacancy periods beyond the standard 30-60 day limit. These endorsements typically add 10-15% to base premiums but provide protection for gaps that standard policies miss.

Final Thoughts

The question “Do I need landlord insurance and homeowners insurance?” has a clear answer: you need one or the other, never both for the same property. Your property’s use determines which policy protects you best. Property owners who rent their homes must switch to landlord insurance immediately, while those who live in their homes need homeowners coverage.

Investment property owners require landlord policies from purchase day. The 25% premium increase for landlord insurance reflects the real risks rental properties face. We at Direct Insurance Services help Utah property owners navigate these insurance complexities and find policies that match their specific situations.

Whether you own rental properties or live in your home, proper insurance coverage protects your investment from claim denials and financial losses. The wrong policy leaves you exposed when disasters strike. Contact our team to review your current coverage and determine if your policy matches how you use your property.