Owning rental property in Utah comes with real financial exposure. Landlord insurance quotes in Utah vary widely depending on your property type, location, and coverage needs.

At Direct Insurance Services, we help landlords understand their options and find policies that actually protect their investment. This guide walks you through comparing quotes, spotting savings opportunities, and selecting coverage that fits your situation.

What Is Landlord Insurance and Why You Need It

Landlord insurance differs fundamentally from homeowners insurance, and this distinction matters enormously for your rental business. While homeowners policies protect owner-occupied properties, landlord insurance covers rental dwellings and addresses risks specific to property management. The coverage includes dwelling protection for the structure itself, liability coverage if someone is injured on your property, loss of rental income if the unit becomes uninhabitable, and protection against tenant-caused damage. Utah landlord insurance averages about $875 per year according to Simply Insurance, which is well below the national median of roughly $1,300 annually. This cost advantage exists because Utah has less natural disaster risk compared to coastal states and benefits from a diverse economy spanning tech in Salt Lake City to tourism in Moab and St. George. Your rate per $1,000 of insured value in Utah sits around $1.89, tied for the lowest in the United States. For perspective, two identical duplexes renting at $2,500 monthly could cost over $2,000 annually in high-insurance states versus around $875 in Utah, saving approximately $1,125 per year or $11,250 over a ten-year hold.

Utah Does Not Legally Require Landlord Insurance, But Your Lender Likely Will

While Utah law does not mandate landlord insurance for rental property owners, most mortgage lenders require it as a condition of financing. The protection is too valuable to skip regardless. Adequate dwelling coverage is non-negotiable because underinsuring triggers coinsurance penalties that force you to absorb losses yourself. If you carry only 50% of needed coverage and suffer a $100,000 loss when you should have had $400,000 in coverage, you might receive only $50,000. Loss of rental income coverage protects your cash flow while the property is rebuilt, and you need to calculate this based on how many months repairs typically take in your area. Liability coverage should start at $1 million minimum, though many landlords increase it to $300,000 or $500,000 for additional protection. Ordinance and Law coverage pays to bring the undamaged portion of your property up to code after a covered loss, which is especially important for older buildings. Most Utah rental properties qualify for DP-3 Special Form coverage, which is the broadest dwelling form available and significantly better than DP-2 or DP-1 options when you can obtain it.

Require Your Tenants to Carry Renters Insurance

Landlord insurance does not cover your tenants’ personal belongings, and this creates a critical gap in your overall protection strategy. Require renters insurance from every tenant and list yourself as a certificate holder on their policies so you receive notice if coverage lapses. Renter’s insurance primarily protects your tenants’ personal property and personal liability needs. This adds a layer of liability protection and reduces your risk exposure substantially. Tenants often resist this requirement, but it is not optional if you want comprehensive risk management. Additionally, establish clear safety rules in your lease: prohibit aggressive dogs to reduce liability risk, ban candles indoors, and require grills to remain at least 5 feet from the dwelling. Inspect the property to confirm it meets code standards before tenants move in (stairs with handrails, clear debris removal), because negligence from code violations can devastate your defense in a lawsuit.

Coverage Elements That Protect Your Bottom Line

Dwelling coverage pays for repairs to the rental structure and attached buildings after perils such as fire, smoke, vandalism, wind, or hail. Contents coverage protects appliances and other removable items you keep on the rental property. Personal Injury coverage protects against allegations such as discrimination or wrongful eviction and can be a low-cost addition. If your rental property is part of a homeowners association, Loss Assessments coverage may be necessary to cover your share of HOA claims. Service Line Insurance covers main sewer or water lines from your home to the street, and if your carrier does not offer this, you can explore programs like HomeServe through Dominion Energy.

Finding the Right Coverage for Your Situation

The coverage options available to you depend on your property type, location, age, and construction. Single-family rentals, multi-family properties (duplexes through fourplexes), rental condos, rental townhomes, and apartment buildings all qualify for landlord coverage in Utah. Your specific property characteristics will influence which coverage forms you can access and what premiums you’ll pay. Some properties may only qualify for DP-2 or DP-1 depending on age, location, or claims history, while others can access the broader DP-3 Special Form. Understanding these distinctions helps you evaluate quotes accurately and avoid policies that leave gaps in your protection.

How to Compare Landlord Insurance Quotes in Utah

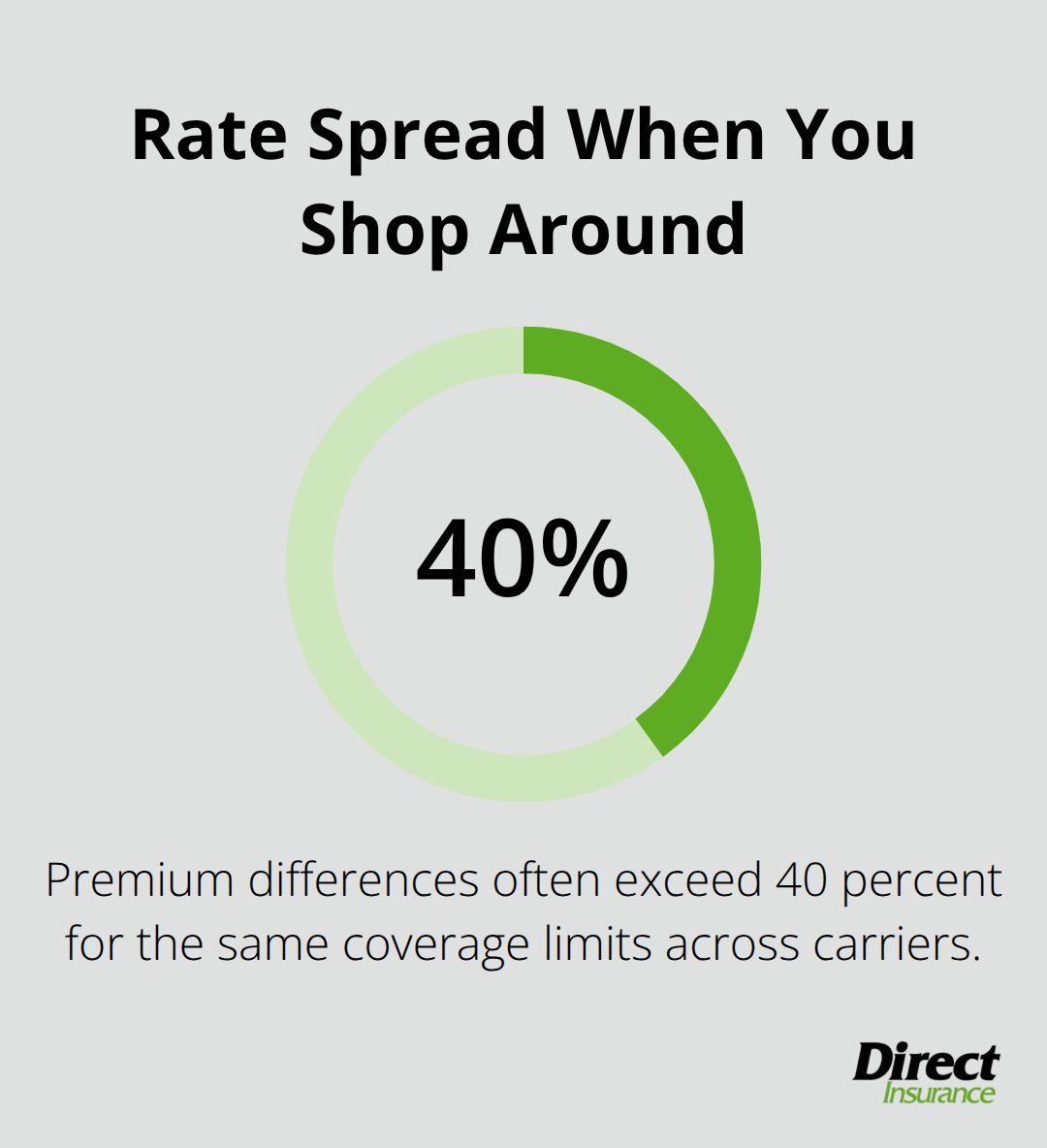

Getting multiple quotes is the only way to understand what you’re actually paying for in Utah landlord insurance, but most landlords stop after comparing premiums alone. This mistake costs thousands in uncovered losses. Property value, location, age, construction type, and coverage limits all drive your quote, and two policies with identical premiums can offer vastly different protection. St. George landlord insurance averages around $700 annually while Moab properties run approximately $650 per year, reflecting the local risk profiles in those markets. Salt Lake City properties typically fall in the $875 range according to Simply Insurance. A quote of $600 might sound attractive until you discover it excludes loss of rental income coverage or caps your liability at $300,000 instead of $1 million. The rate per $1,000 of insured value matters more than the total premium because it reveals whether you’re paying a fair price for your specific property. Utah’s average sits around $1.89 per $1,000 of insured value, so calculate this metric for every quote you receive and reject anything significantly higher unless the carrier offers materially broader coverage.

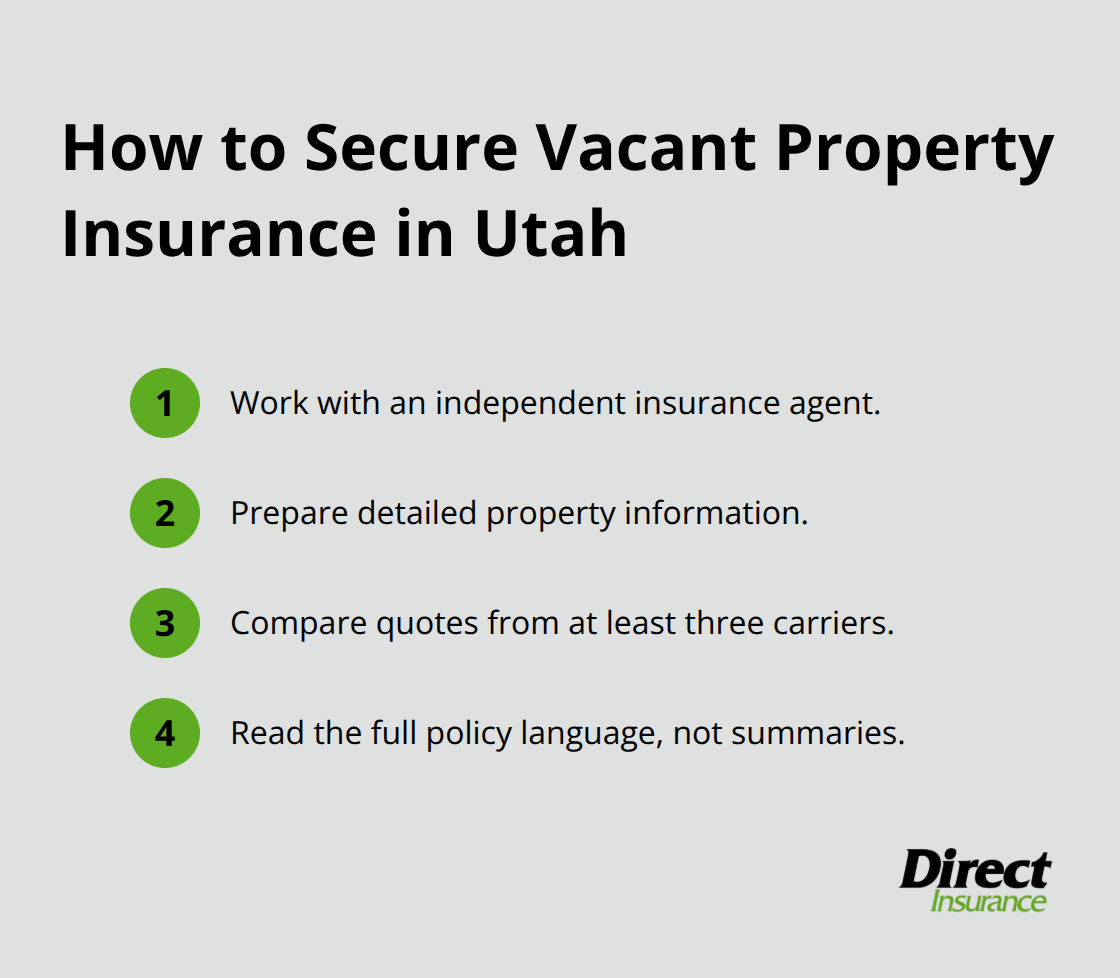

Request Identical Information From Multiple Carriers

Contact at least three carriers or independent agents and provide identical property details to each one so comparisons are actually meaningful. Tell them your property age, square footage, number of units, current tenant situation, and whether the structure meets current building codes.

Ask specifically what DP form they’re quoting (DP-3 Special Form is what you want), whether loss of rental income coverage is included and for how many months, what the liability limit is, and whether Personal Injury coverage or Ordinance and Law coverage are part of the base policy or cost extra. Request information about discounts for multi-policy bundling since you likely carry auto or homeowners insurance elsewhere. Many carriers offer 10 to 15 percent reductions when you consolidate policies. Ask whether they offer credits for security systems, deadbolt locks, or fire extinguishers because these tangible safety measures can lower your premium. Demand clarity on what perils are excluded and whether endorsements can add coverage for sewer backup or flood damage if needed in your specific location. Never accept vague answers about what is or isn’t covered because the quote itself won’t contain this detail.

Work With Independent Agents to Compare Multiple Options

Independent agents in Utah can shop multiple carriers simultaneously, which saves time and often reveals better pricing than online quote tools. These agents hold valid Utah licenses and can explain coverage differences in plain language rather than industry jargon. They understand local market conditions and can recommend carriers that perform well in your specific area. When you work with an independent agent, you gain access to carriers that may not offer online quotes, expanding your options significantly. The agent’s job is to find you the best fit, not to push you toward one particular carrier.

Identify Quotes That Leave You Exposed

Online quote tools frequently generate artificially low numbers by stripping away essential coverage, and you won’t realize the gaps until you file a claim. A quote that seems 30 percent cheaper than others should trigger immediate suspicion rather than excitement. Compare the actual coverage limits across quotes line by line instead of just looking at the total premium. If one quote offers $1 million liability and another offers $300,000 for significantly less money, the savings disappear the moment someone is injured on your property and sues for more than $300,000. Quotes that don’t mention loss of rental income coverage are hiding a major gap because you’ll lose that income out of pocket if the property becomes uninhabitable from a covered loss. Some carriers intentionally quote lower coverage amounts to attract your business, then pressure you to add protection later at higher rates. Avoid carriers that make it difficult to speak with a real person or won’t explain their quotes in detail. The Utah Department of Insurance requires all agents and companies to hold valid licenses, so verify this before committing to any policy. Quotes from carriers without strong AM Best or BBB ratings deserve extra scrutiny because claims handling matters more than premium savings when disaster strikes.

Evaluate Carrier Strength and Service Quality

The cheapest quote won’t protect you if the carrier denies your claim or takes months to process it. Progressive, Foremost, and Stillwater all carry high AM Best and BBB ratings and offer 24/7 claims reporting, which matters enormously when you need to file a claim quickly. These carriers have demonstrated financial strength and reliability in handling landlord claims across Utah. When you compare quotes, ask each carrier about their average claims processing time and whether they offer online claim filing. A carrier that processes claims in five days instead of thirty days can mean the difference between covering your mortgage and facing financial hardship. An independent agent can help you access the best coverage options without pressure for one-size-fits-all policies. This approach means you can compare quotes from multiple strong carriers and select the one that best fits your property and risk tolerance.

How to Cut Your Utah Landlord Insurance Costs Without Sacrificing Protection

Bundle Policies to Unlock Immediate Savings

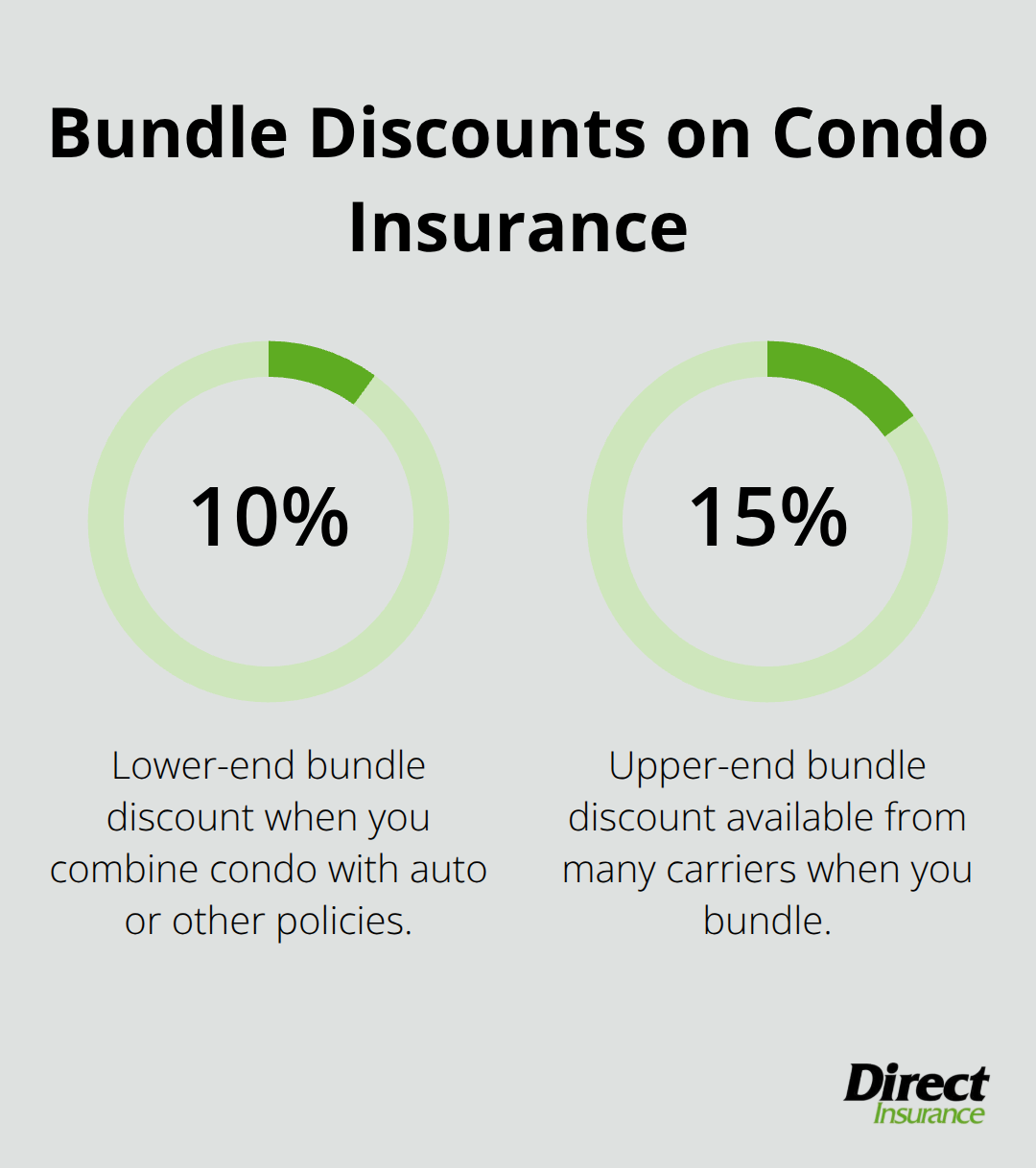

Consolidating your landlord policy with auto or homeowners insurance can help you save money through multi-policy discounts of anywhere from 10% to 25%. Many Utah landlords overlook this option because they assume their current auto insurer won’t offer competitive landlord rates, but independent agents can quickly determine which carriers offer the best bundle discounts for your specific situation. Progressive, Foremost, and Stillwater all reward consolidation, so requesting quotes that include your existing coverage reveals the true savings. The difference between a higher premium and a discounted one after bundling is money that stays in your cash flow and compounds over years of ownership. Some landlords hesitate to bundle because they worry about losing flexibility, but you can always adjust coverage independently later if your situation changes, so the upfront savings far outweigh that minor concern.

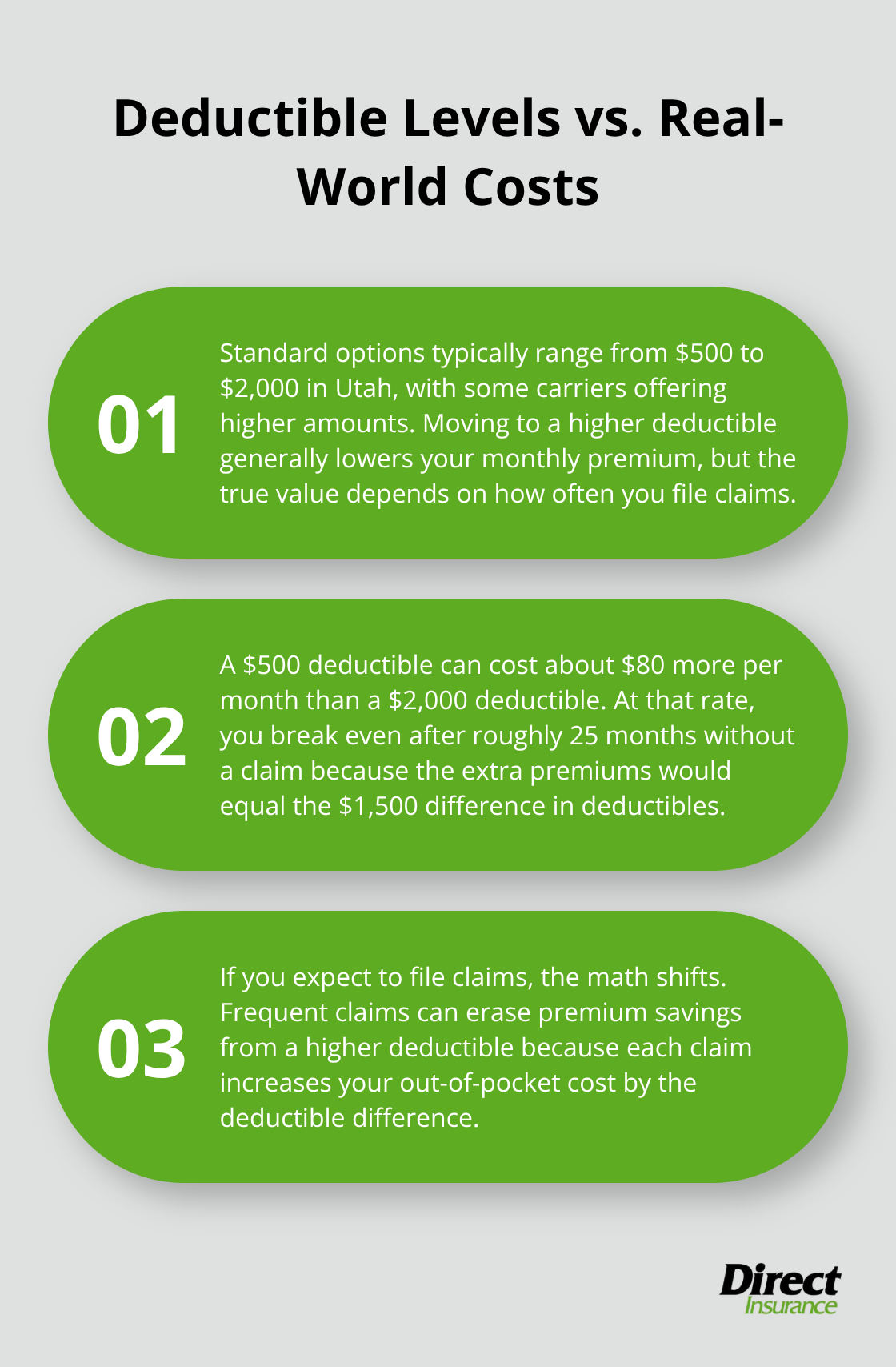

Raise Your Deductible Strategically

Increasing your deductible from $500 to $1,000 or even $2,500 typically reduces your premium by 5 to 10 percent, but only if you can absorb that out-of-pocket cost without stress. A $1,000 deductible increase saving you $75 annually means you recover that savings in just over 13 months, making it worth considering if you have emergency reserves set aside. The trap many landlords fall into is selecting a deductible they can’t actually afford when a claim occurs, which forces them into debt or leaves repairs incomplete. Calculate your deductible based on what you can pay immediately, not what sounds good on paper.

Install Safety Features to Qualify for Credits

Property safety features and security credits offer genuine premium reductions without the risk of higher deductibles. Installing deadbolt locks, smoke detectors, and fire extinguishers can lower premiums by 2 to 5 percent depending on the carrier. Some insurers credit properties with monitored security systems or sprinkler systems by 10 percent or more, which makes the installation cost recoverable in just a few years. Ask every carrier you contact exactly which safety features they credit and what percentage reduction each feature provides. A $400 investment in upgraded locks and fire extinguishers might reduce your annual premium by $35 to $40, but the cumulative savings across a ten-year hold exceeds $350 while simultaneously reducing actual fire and theft risk.

Prioritize Code Compliance Above All Else

The most valuable property improvement is ensuring the rental meets current building code standards-stairs with proper handrails, electrical systems that pass inspection, and clear egress paths. Code compliance eliminates the coinsurance penalties that devastate your claims payout. A property that fails code inspection won’t just cost you more in premiums; it exposes you to massive out-of-pocket losses when you file a claim and the insurer applies coinsurance penalties to your payout.

Final Thoughts

Your landlord insurance policy protects your dwelling from fire, wind, hail, and vandalism while covering liability if someone is injured on the property. Loss of rental income coverage prevents cash flow collapse during rebuilds, and DP-3 Special Form coverage provides the broadest protection available. Personal Injury coverage and Ordinance and Law endorsements cost little but shield you from discrimination lawsuits and code compliance penalties that can devastate your finances.

Landlord insurance quotes in Utah require you to contact multiple carriers with identical property information so you can compare apples to apples. Calculate the rate per $1,000 of insured value for each quote to determine whether you’re paying a fair price in Utah’s market, and reject quotes that seem suspiciously cheap without explanation. Always verify that the carrier holds a valid Utah license and maintains strong AM Best and BBB ratings before committing to any policy.

An independent agent transforms the quote process from frustrating to straightforward by shopping multiple carriers simultaneously and explaining coverage differences in plain language. We at Direct Insurance Services understand Utah’s rental market, know which carriers perform best in your area, and adjust your coverage as your portfolio grows. Rather than spending hours comparing online quotes that strip away essential protection, we handle the legwork and present you with options from carriers that actually deliver when you file a claim.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation