How to Choose Home Insurance Dwelling Coverage

Most homeowners underestimate how much it costs to rebuild their house after a disaster. Getting your home insurance dwelling coverage right protects your biggest asset and prevents financial hardship when you need it most.

At Direct Insurance Services, we help homeowners understand exactly how much coverage they actually need. This guide walks you through the process step by step.

What Dwelling Coverage Actually Covers

Dwelling coverage protects the physical structure of your home-the walls, roof, foundation, floors, and built-in appliances that form the core of your house. When a covered peril like fire, lightning, windstorm, or vandalism damages your home, dwelling coverage pays to repair or rebuild those structural elements. What matters here is understanding that dwelling coverage does not protect your belongings inside the home; that falls under personal property coverage, which is a separate component of your policy. Detached structures like a garage or shed are also covered separately under other structures coverage. Many homeowners confuse what gets protected, so knowing this distinction prevents costly gaps when you file a claim.

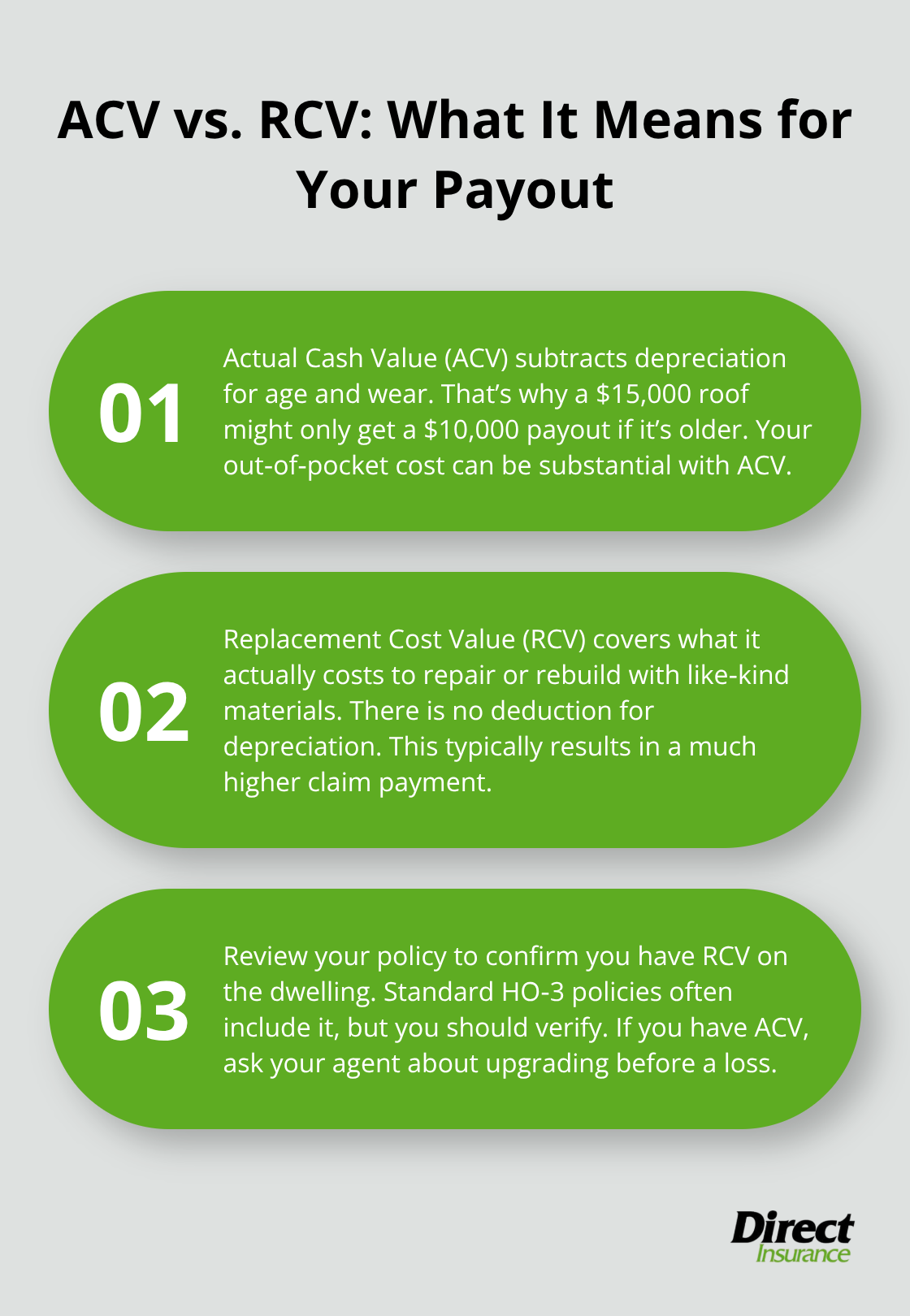

Actual Cash Value Versus Replacement Cost

This choice fundamentally changes how much you receive after a loss. Actual Cash Value coverage pays for damage minus depreciation based on the age and wear of your home’s materials and structure. If your roof suffers hail damage and costs $15,000 to replace, an ACV policy might pay only $10,000 because the roof is older and has depreciated. Replacement Cost Value coverage, by contrast, pays what it actually costs to repair or rebuild using like-kind materials without subtracting depreciation. That same $15,000 roof repair gets covered at full value under RCV. The difference can amount to thousands of dollars on major claims. We strongly recommend replacement cost coverage because it reflects the real expense of rebuilding your home in today’s market.

Standard HO-3 homeowners policies typically include replacement cost dwelling coverage, but always verify this on your declaration page. If you have ACV instead, ask your agent about upgrading to RCV before a disaster strikes.

The 80 Percent Rule and Coinsurance Penalties

Underinsuring your home creates a coinsurance penalty if a major loss occurs. Insurance companies typically enforce an 80 percent rule, meaning you must carry at least 80 percent of your home’s full replacement cost or face reduced payouts on claims. If your home costs $400,000 to rebuild but you only insure it for $250,000, you’ve triggered this penalty, and the insurer may pay significantly less than your actual damages. Construction costs have risen substantially over the past decade due to inflation and supply-chain pressures, making this calculation more critical than ever.

Lender Requirements and Your Mortgage

Mortgage lenders require dwelling coverage to meet or exceed your loan amount, which means your lender has a vested interest in keeping your home properly insured. This requirement protects both you and the lender from financial catastrophe. Setting the right coverage amount now prevents the nightmare scenario of losing your home and facing a shortfall when you rebuild. Your next step involves calculating exactly how much your home would cost to reconstruct from the ground up-a figure that differs significantly from what you paid for the property or what it would sell for today.

What Drives Your Dwelling Coverage Needs

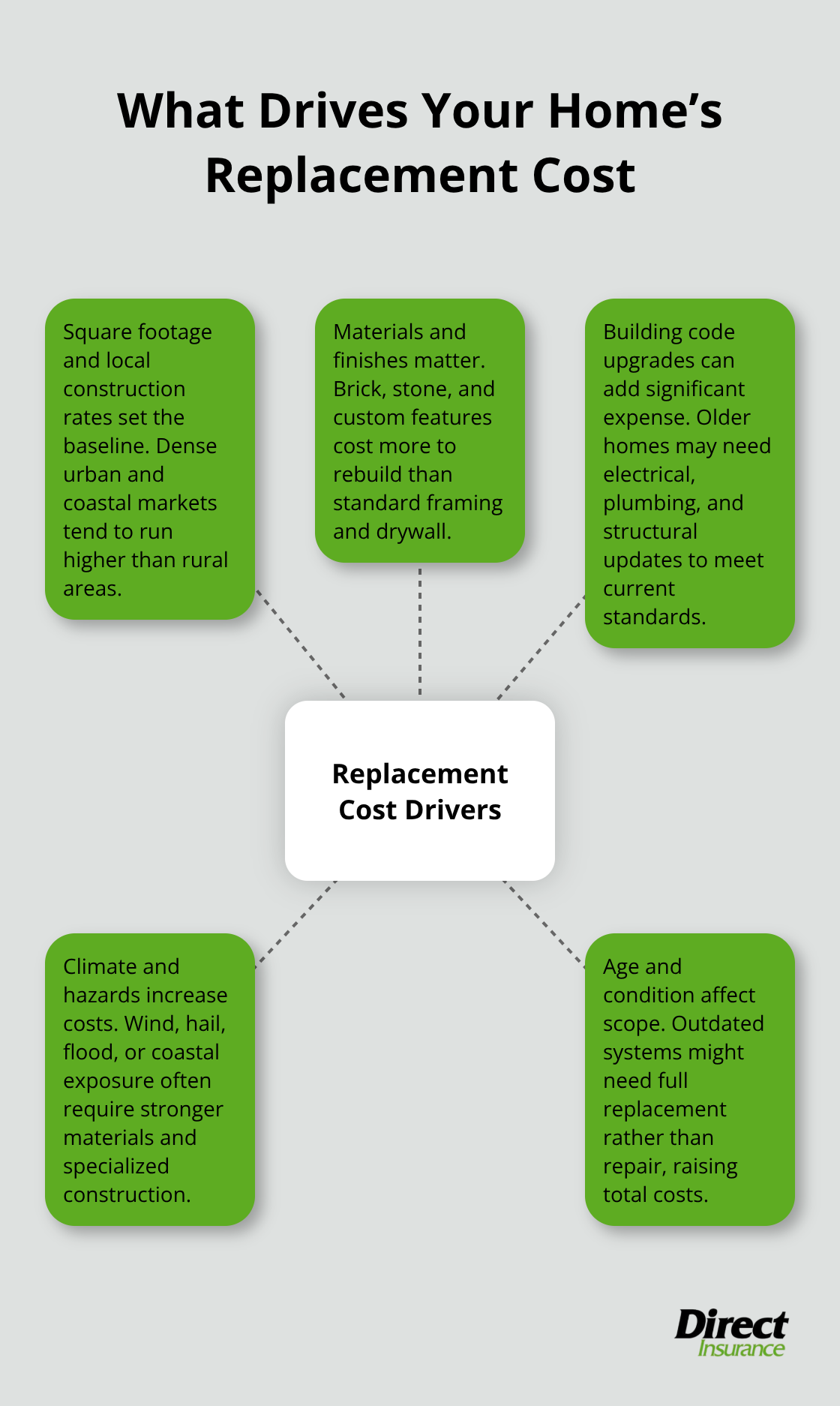

Square Footage and Local Construction Costs

Your home’s replacement cost starts with square footage, but location determines the real expense. A 2,500-square-foot home in rural Utah costs significantly less to rebuild than an identical home in a dense urban area where labor rates and material costs run higher. The Insurance Information Institute recommends multiplying your home’s square footage by the local cost per square foot of residential construction in your area, then adjusting for materials and custom features. Building material costs have risen 41.6% since the COVID-19 pandemic, with rebuilding expenses climbing faster than home values in many markets. This means a dwelling coverage amount that was adequate five years ago may leave you underinsured today.

Materials and Building Standards

The materials used in your home’s construction directly affect replacement costs. A home built with standard framing and drywall costs far less to rebuild than a home with brick, stone, or specialty materials. Older homes often require updated construction to meet current building codes, which increases rebuilding expenses beyond the original construction price. If your home was built in the 1970s or earlier, code upgrades for electrical systems, plumbing, and structural requirements can add 15 to 25 percent to replacement costs.

Climate, Location, and Regional Factors

Climate and location play a critical role in your coverage needs. Homes in areas prone to severe weather, high winds, or hail face higher replacement costs because construction standards in those regions demand stronger materials and reinforced structures. Coastal properties and homes in flood-prone zones typically require specialized construction that increases rebuilding expenses. Your home’s age and condition matter as well because older homes may have outdated systems that need complete replacement rather than repair, driving up total reconstruction costs.

Moving Forward with Accurate Estimates

These regional and property-specific factors shape how much coverage you actually need. The next step involves calculating your home’s exact replacement cost using concrete data from your area rather than relying on outdated estimates or assumptions about what your home might sell for today.

Calculate Your Home’s Replacement Cost

Getting an accurate replacement cost estimate forms the foundation of proper dwelling coverage. Start by finding your home’s square footage and researching the cost per square foot for residential construction in your specific area. The Insurance Information Institute provides data showing that typical construction costs range from $100 to $200+ per square foot depending on region, with urban markets and coastal areas commanding higher rates. Multiply your square footage by your local rate, then adjust upward for your home’s specific features. A home with granite countertops, hardwood floors, and custom cabinetry costs more to rebuild than one with standard finishes. If your home underwent renovation within the last five years, factor in the actual costs from those projects since they reflect current material and labor rates in your market. Many homeowners overlook this step and rely on outdated estimates, which leaves them dangerously underinsured. Your insurance company can provide a replacement cost estimate as part of the quoting process, but you should verify this number independently. Online calculators exist, though they often underestimate for homes with premium materials or unique architectural features. The most reliable approach involves obtaining a professional appraisal specifically for replacement cost purposes, which typically costs $200 to $500 but provides documentation that protects you if a claim dispute arises.

Why Land Value Doesn’t Count

A critical mistake homeowners make involves basing dwelling coverage on their home’s market value or purchase price. Your home’s market value includes the land beneath it, which doesn’t burn down or suffer damage from storms. If you paid $500,000 for your property but the land represents $150,000 of that value, your dwelling coverage should reflect only the $350,000 needed to rebuild the structure. This distinction matters enormously because it prevents you from over-insuring and paying unnecessary premiums. Standard policies exclude land from coverage, so your declaration page should show a dwelling limit that represents the cost to reconstruct the building itself, not the total property value. Additionally, your dwelling coverage should exclude any permanent improvements you’ve made to the land, such as driveways, landscaping, or pools, since these fall under other structures coverage with its own limits. Review your declaration page to confirm your dwelling limit makes sense relative to what rebuilding would actually cost. If the number seems disconnected from your home’s actual replacement cost, contact your agent immediately to discuss whether inflation adjustments or recent renovations warrant an increase.

Construction Costs Rise Faster Than Home Values

Construction costs have risen significantly since 2020, which means your coverage from three years ago is likely insufficient today. Material shortages and labor demand have pushed rebuilding expenses upward at rates that outpace typical home value appreciation in many markets. Your coverage from five years ago probably leaves you significantly underinsured if a major loss occurs. Homes in areas that experienced recent natural disasters face even steeper cost increases because material and labor demand spike after widespread damage. Check local news about construction cost trends in your region and discuss any significant increases with your agent. These regional variations mean that a dwelling limit appropriate for your neighbor’s home may fall short for yours, depending on your specific construction materials and architectural complexity.

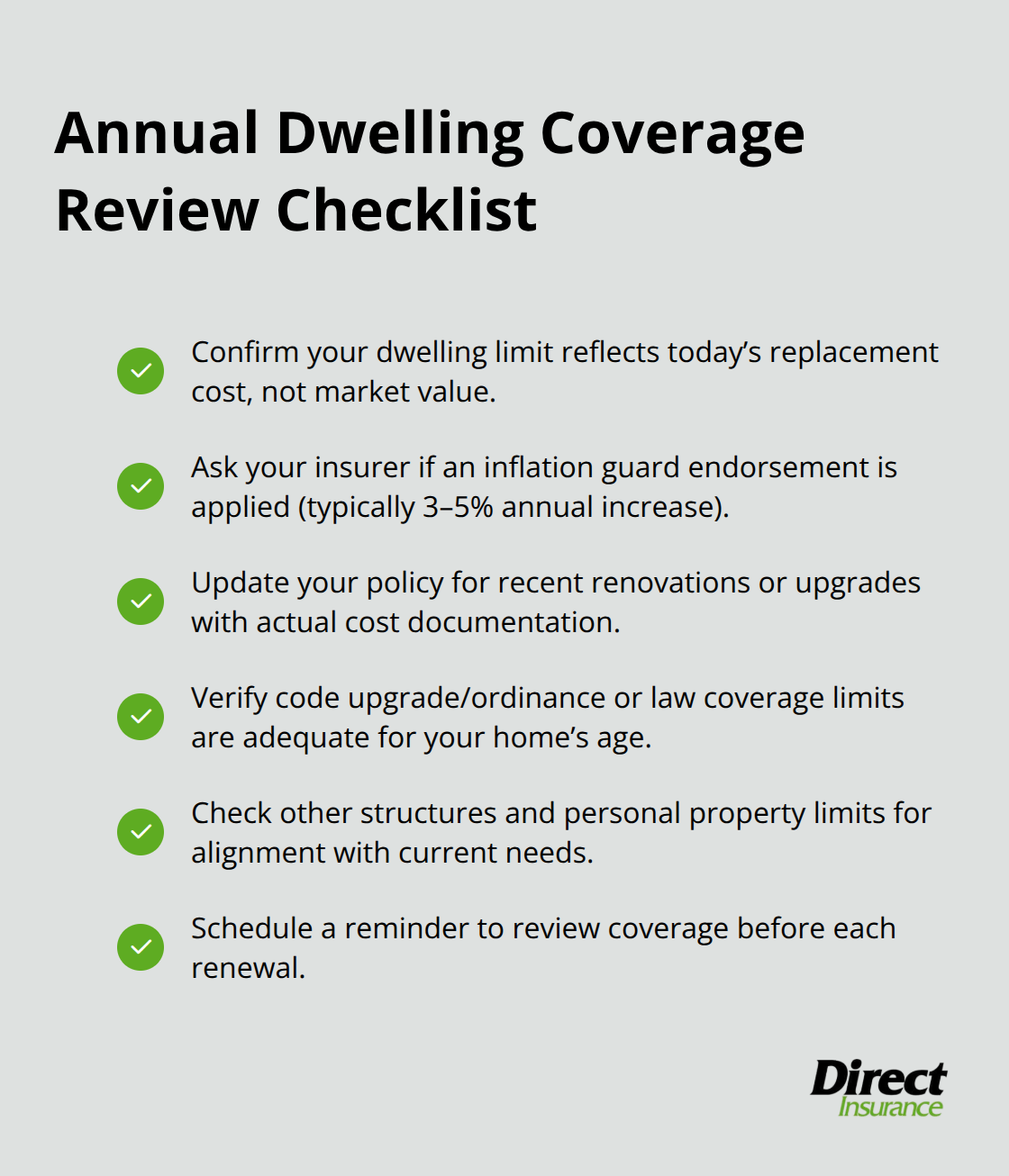

Annual Reviews Prevent Coverage Gaps

We recommend reviewing your dwelling coverage at minimum annually, ideally before your policy renews. During this review, ask whether your insurer has applied inflation adjustments automatically or whether you need to request a higher limit. If you’ve completed any home improvements, provide documentation of the costs to your agent so coverage reflects the increased replacement value. Some insurers offer inflation guard endorsements that automatically increase your dwelling limit by a set percentage each year, typically 3 to 5 percent, which helps protect against rising construction costs without requiring annual adjustments. This feature costs very little but prevents the costly gap between your coverage and actual rebuilding expenses. Homeowners who skip annual reviews often discover too late that a loss leaves them thousands of dollars short, especially if major reconstruction is needed.

Final Thoughts

Calculate your home’s actual replacement cost using square footage and local construction rates, then adjust for your specific materials and features. Verify that your coverage meets the 80 percent rule to avoid coinsurance penalties when you file a claim. Commit to reviewing your home insurance dwelling coverage annually because construction costs rise faster than home values, and skipping this step leaves you dangerously underinsured.

The most common mistake homeowners make involves basing coverage on market value instead of rebuilding cost. Your home’s market value includes land, which doesn’t need rebuilding after a disaster-strip away the land value and focus only on what it costs to reconstruct the structure itself. Check your declaration page right now to confirm your dwelling limit reflects this reality, and if you completed renovations in the past few years, your coverage probably needs adjustment upward.

An insurance agent transforms this process from confusing to straightforward by running replacement cost estimates specific to your home and explaining whether your current coverage leaves you exposed. At Direct Insurance Services, our team helps homeowners select adequate dwelling coverage without pressure, and we work with top-rated carriers to find coverage that matches both your home’s actual replacement cost and your budget. Contact us today to discuss your dwelling coverage needs and ensure your home is properly protected.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation