Condo ownership in Utah comes with unique insurance needs that differ significantly from traditional homeowners policies. At Direct Insurance Services, we’ve helped countless Utah condo owners understand their coverage options and find the right protection for their investment.

This condo insurance Utah guide walks you through the coverage types you need, what affects your costs, and how to make informed decisions about your policy.

What Makes Condo Insurance Different in Utah

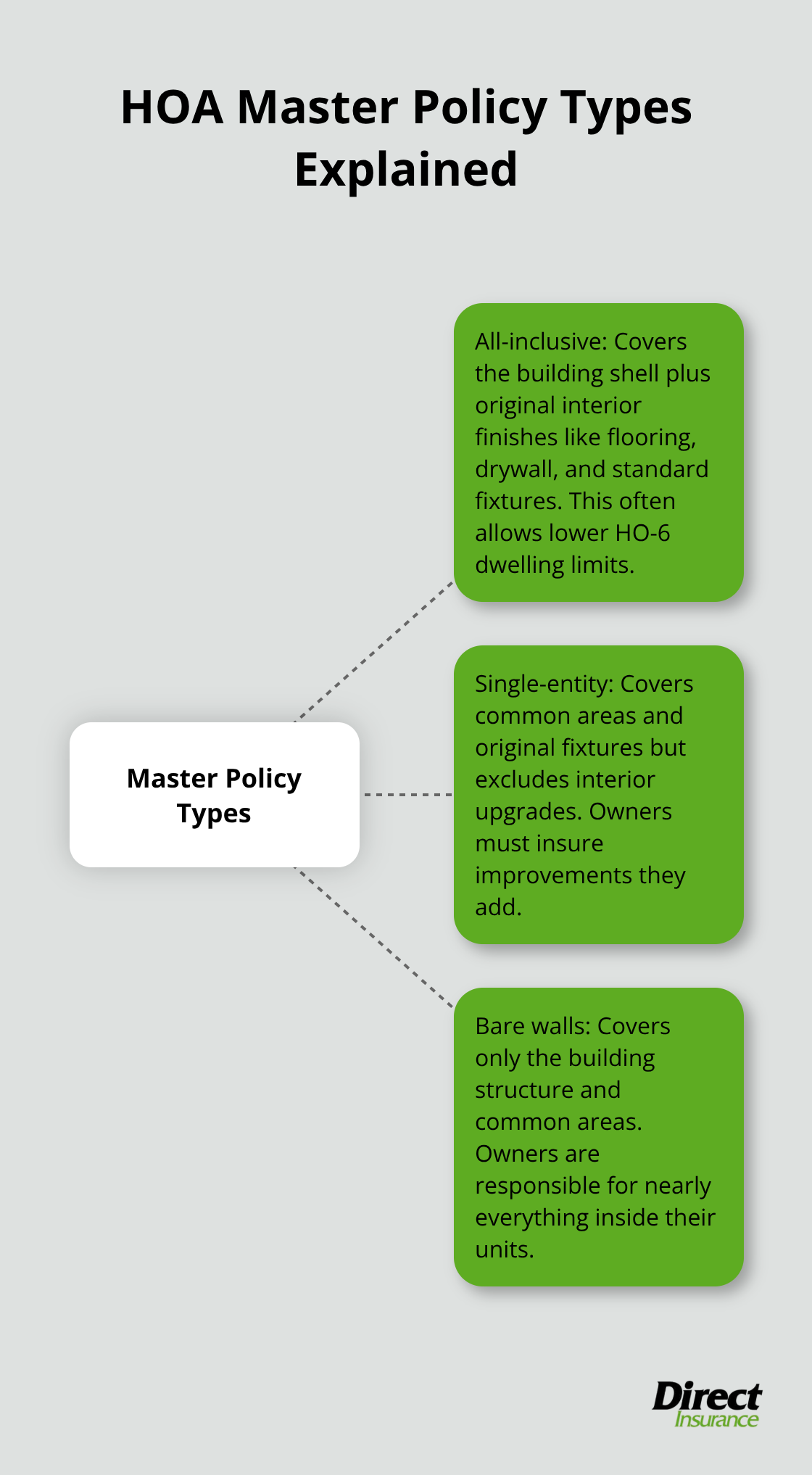

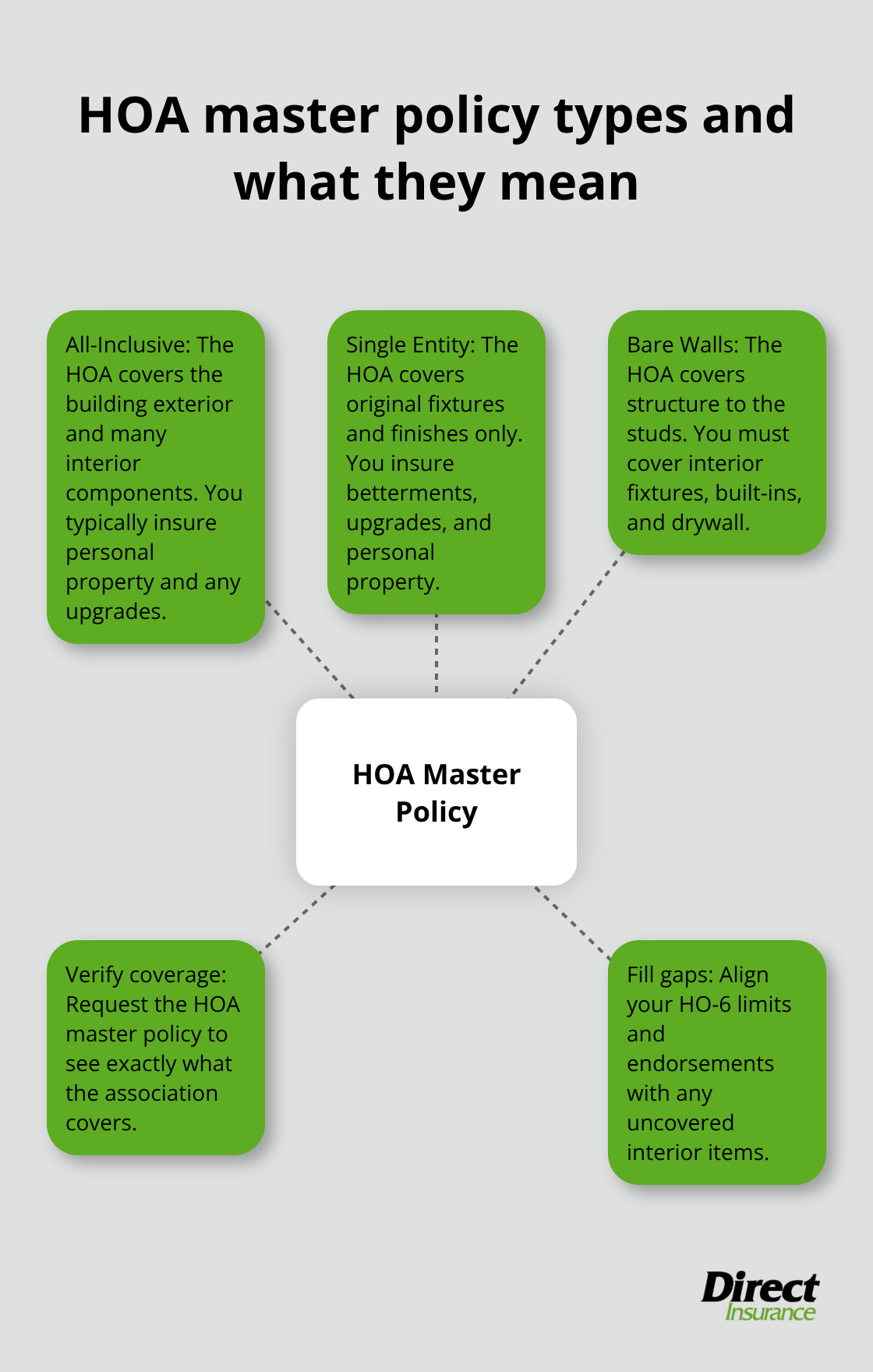

HO-6 condo insurance protects something fundamentally different from standard homeowners policies, and this distinction matters when you file a claim. Your HO-6 policy covers the interior of your unit, personal belongings, liability exposure, and loss of use expenses. The HOA master policy covers the building exterior and common areas. This split responsibility creates a critical gap that many Utah condo owners miss: if the HOA master policy is bare walls coverage (studs-out), your HO-6 must cover interior fixtures, built-ins, and drywall. Many owners underestimate what they need to cover because they assume the master policy handles everything. It doesn’t.

What You Actually Pay for Condo Insurance in Utah

According to data from Insure.com analyzing 34,588 ZIP codes across 145 companies, the average Utah condo owner pays about $668 annually for HO-6 coverage with $60,000 personal property, $300,000 liability, and a $1,000 deductible. That’s roughly $12 higher than the national average of $656, reflecting Utah-specific construction costs and local risks. State Farm leads Utah’s condo market at around $266 per year for comparable coverage, followed by Allstate at $321 and Iowa Farm Bureau at $330.

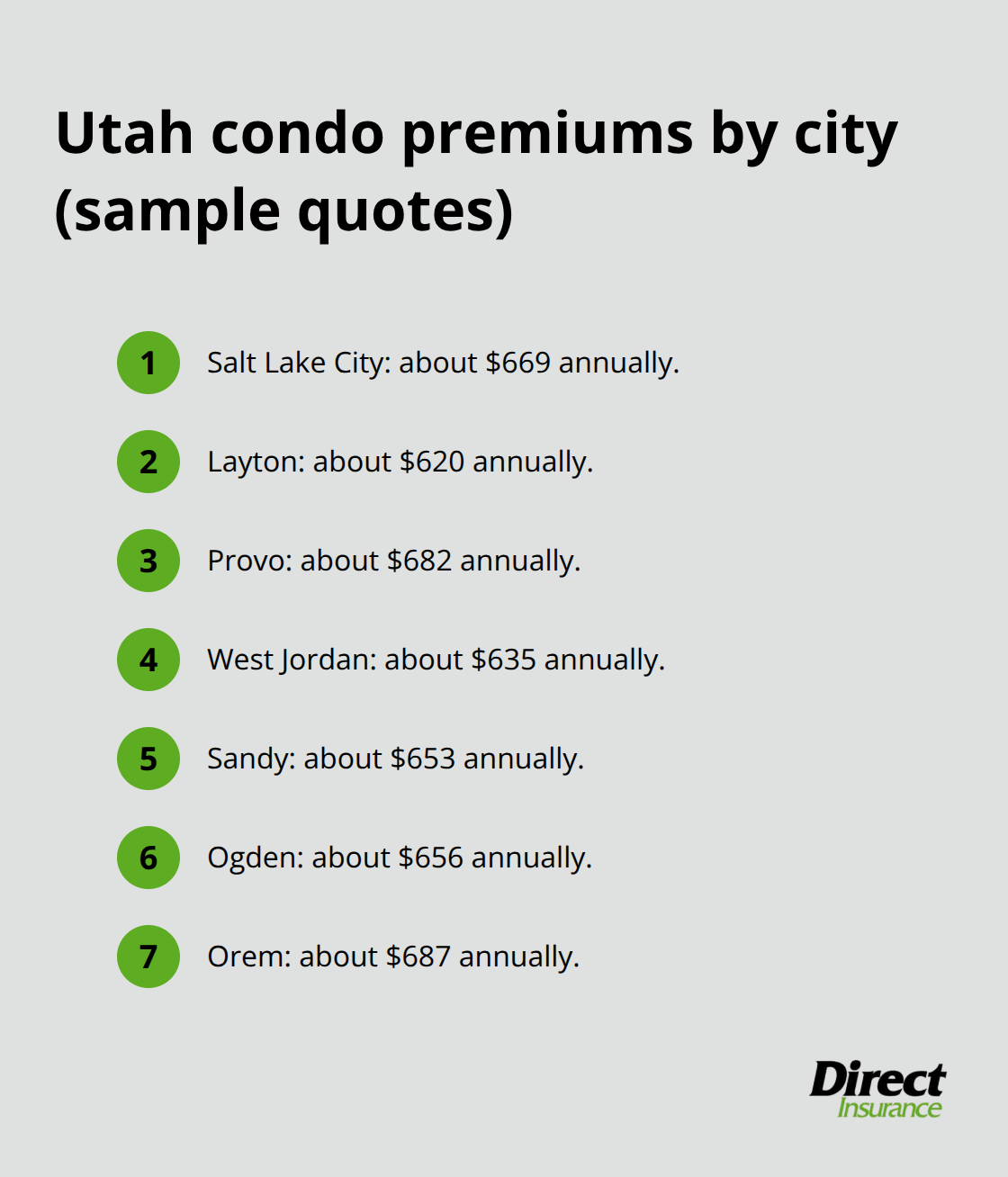

Your location within Utah affects your premium significantly. Salt Lake City condo insurance averages $669 annually, while Layton runs about $620 and Provo around $682, all reflecting local construction costs and exposure patterns.

Why Liability Coverage Matters More Than You Think

Your liability limits matter more than you think in Utah’s condo environment. About 68% of condo owners in Colorado and Utah carry insufficient liability coverage, and 33% of condo and townhome claims involve injuries or property damage. Average liability claims in the region exceed $30,000, with some reaching $300,000 or beyond.

A real Salt Lake City dog bite claim totaled $42,700, which nearly exhausted a $100,000 liability limit with no umbrella policy in place. This case shows how quickly a single incident can consume your entire liability protection. Without adequate coverage, you expose your personal assets to significant risk.

Utah’s Natural Disaster Exposure

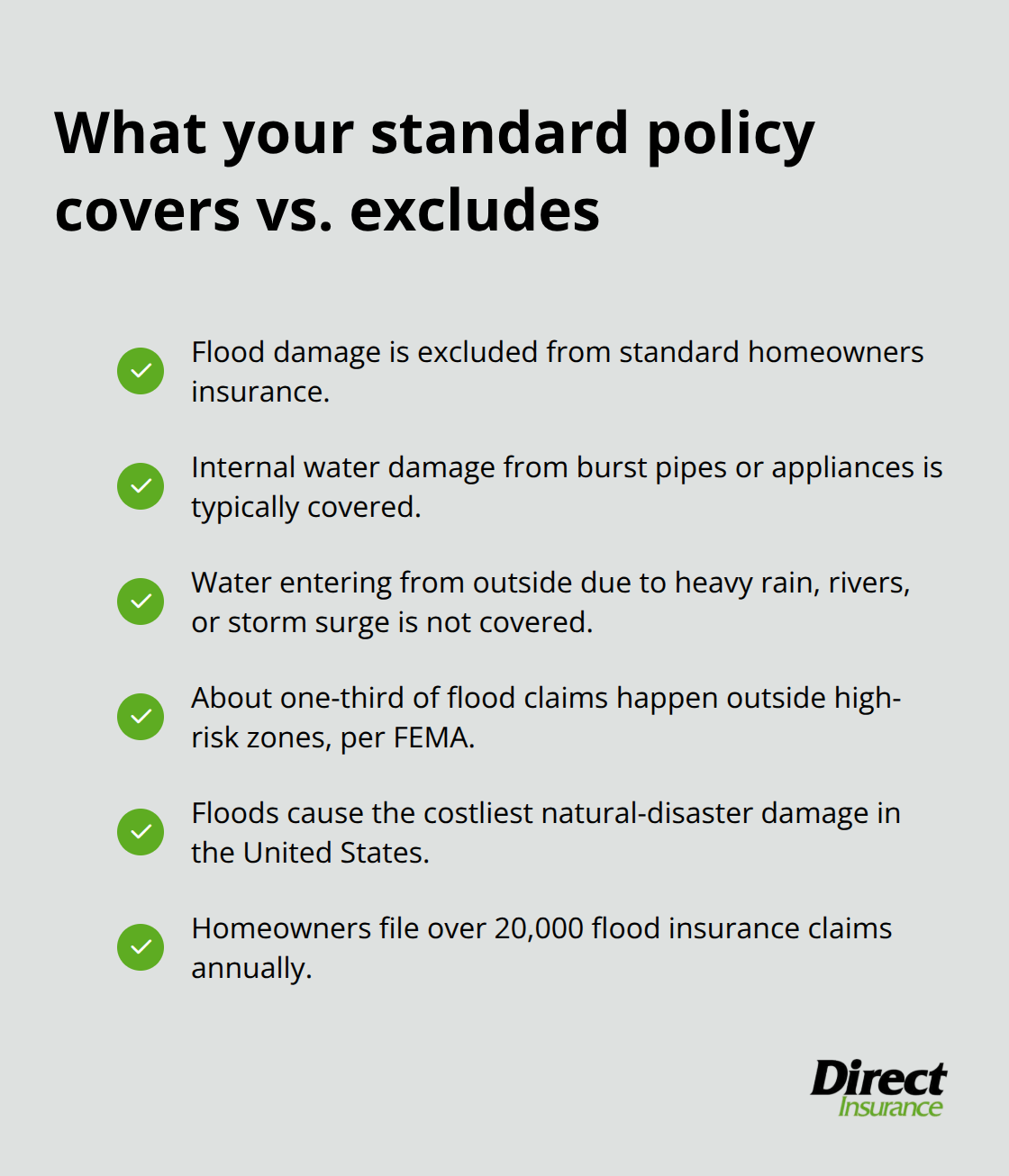

Wildfires represent Utah’s dominant natural disaster risk for condo owners. The Insurance Information Institute ranked Utah No. 9 among states with homes most at risk from wildfires as of 2025. Standard homeowners and HO-6 policies cover fire damage, but floods and earthquakes do not. You need separate endorsements or standalone policies to cover earthquake risk, and the National Flood Insurance Program (NFIP) or private flood insurers provide flood coverage.

Many Utah condo owners in flood zones delay adding flood protection until after a named weather event occurs, only to find insurers pause new policies. That timing gap leaves you unprotected during critical periods. Avalanche risk and weather-related damage also influence Utah condo premiums significantly.

Legal and Lender Requirements

Utah state law does not mandate condo insurance, but your mortgage lender almost certainly does. Lenders require HO-6 coverage to protect their investment in your unit. The Utah Condominium Ownership Act clarifies where your coverage responsibilities begin and where the HOA’s obligations end.

Many Utah condos operate under different master policy structures: All-Inclusive, Single Entity, or Bare Walls configurations. A bare walls HOA structure, more common in Colorado but present in Utah, shifts significant interior coverage responsibility to you. Before purchasing or renewing your HO-6, request a copy of the HOA master policy from your association.

This document reveals exactly what gaps exist and what your personal policy must cover. Skipping this step is how Utah condo owners end up underinsured-and that’s where understanding your specific coverage needs becomes essential for the next phase of your decision.

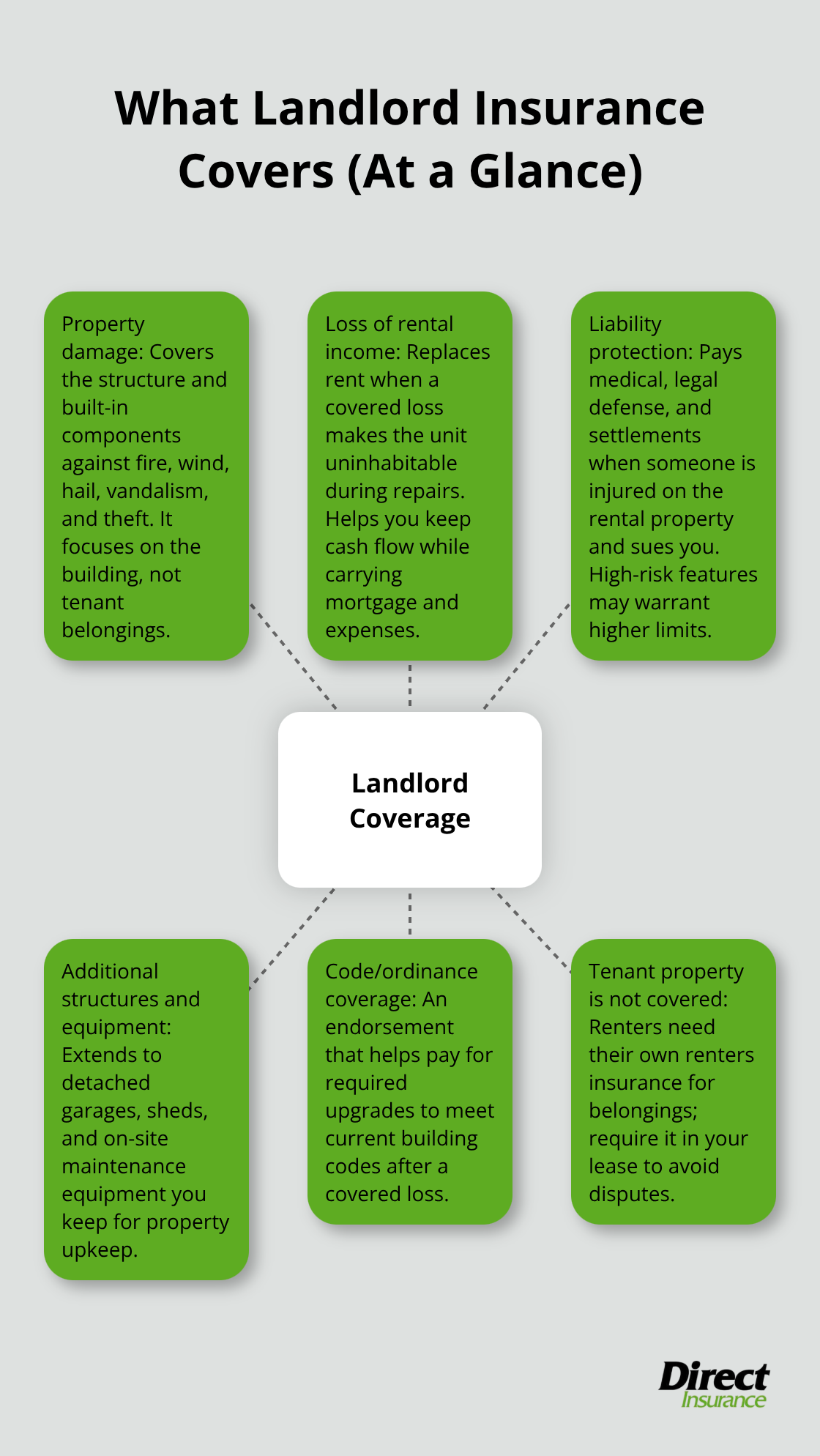

What Your HO-6 Policy Actually Covers

Personal Property Coverage and Your Replacement Choices

Personal property coverage protects your furniture, electronics, clothing, and other belongings inside your unit. This coverage pays to repair or replace these items if fire, wind, hail, or other covered perils damage them. Insure.com data shows Utah condo owners typically carry $60,000 in personal property coverage, which translates to roughly $668 annually in total premiums.

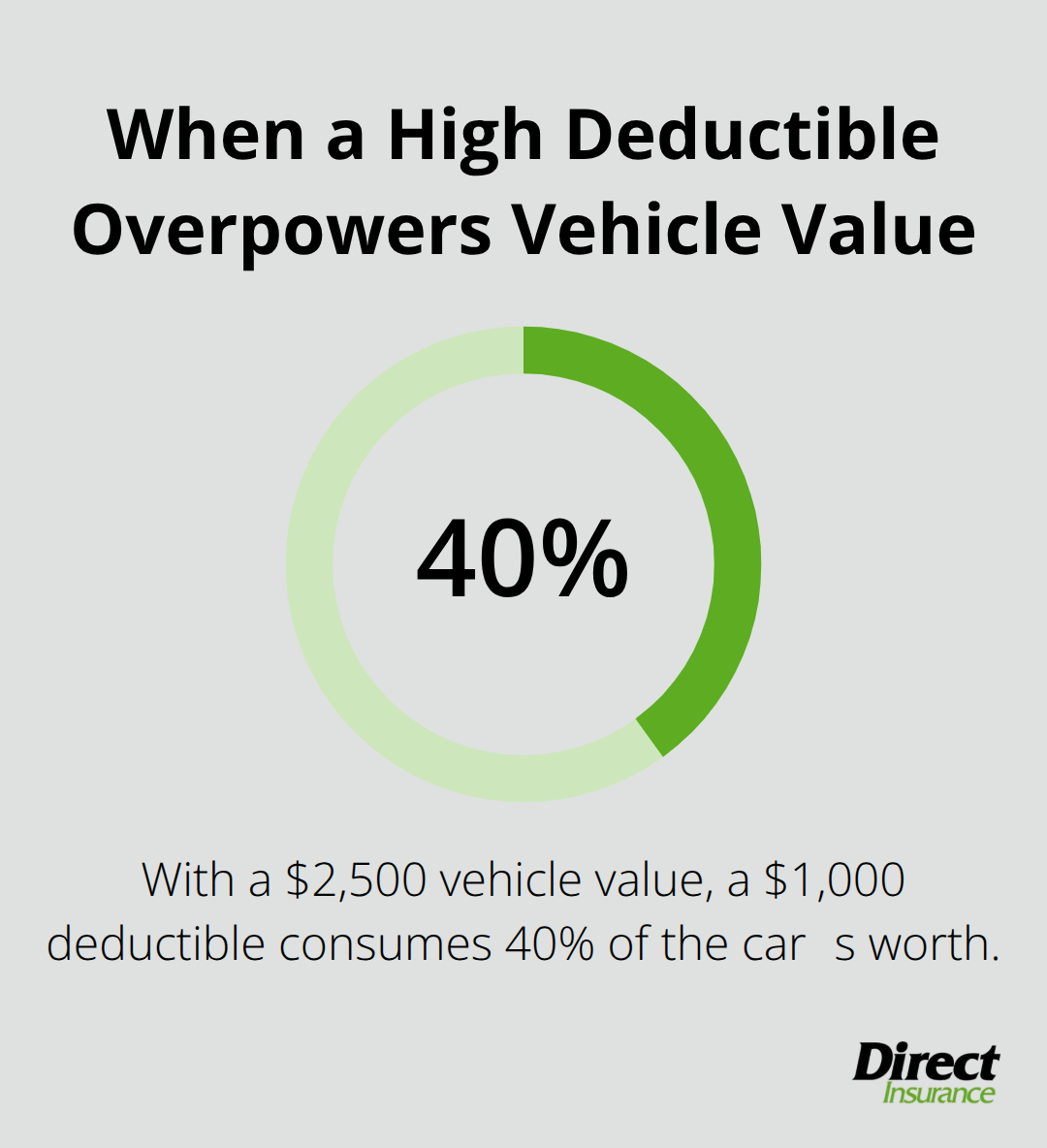

The critical decision involves choosing between replacement cost value (RCV) and actual cash value (ACV). RCV pays the full cost to replace damaged items with new equivalents, while ACV deducts depreciation based on age and wear. A ten-year-old television worth $800 new might only yield $200 under ACV coverage after depreciation, but RCV would cover the full replacement cost. RCV costs more monthly but eliminates the financial sting when you file a claim.

Your deductible directly affects both your premium and your out-of-pocket costs when damage occurs. Jumping from a $1,000 deductible to $2,500 can lower your annual premium by $50 to $100, but that savings vanishes if you experience even one claim. The trade-off between lower premiums and higher out-of-pocket costs requires honest assessment of your financial situation.

Liability Protection: Your Largest Exposure Gap

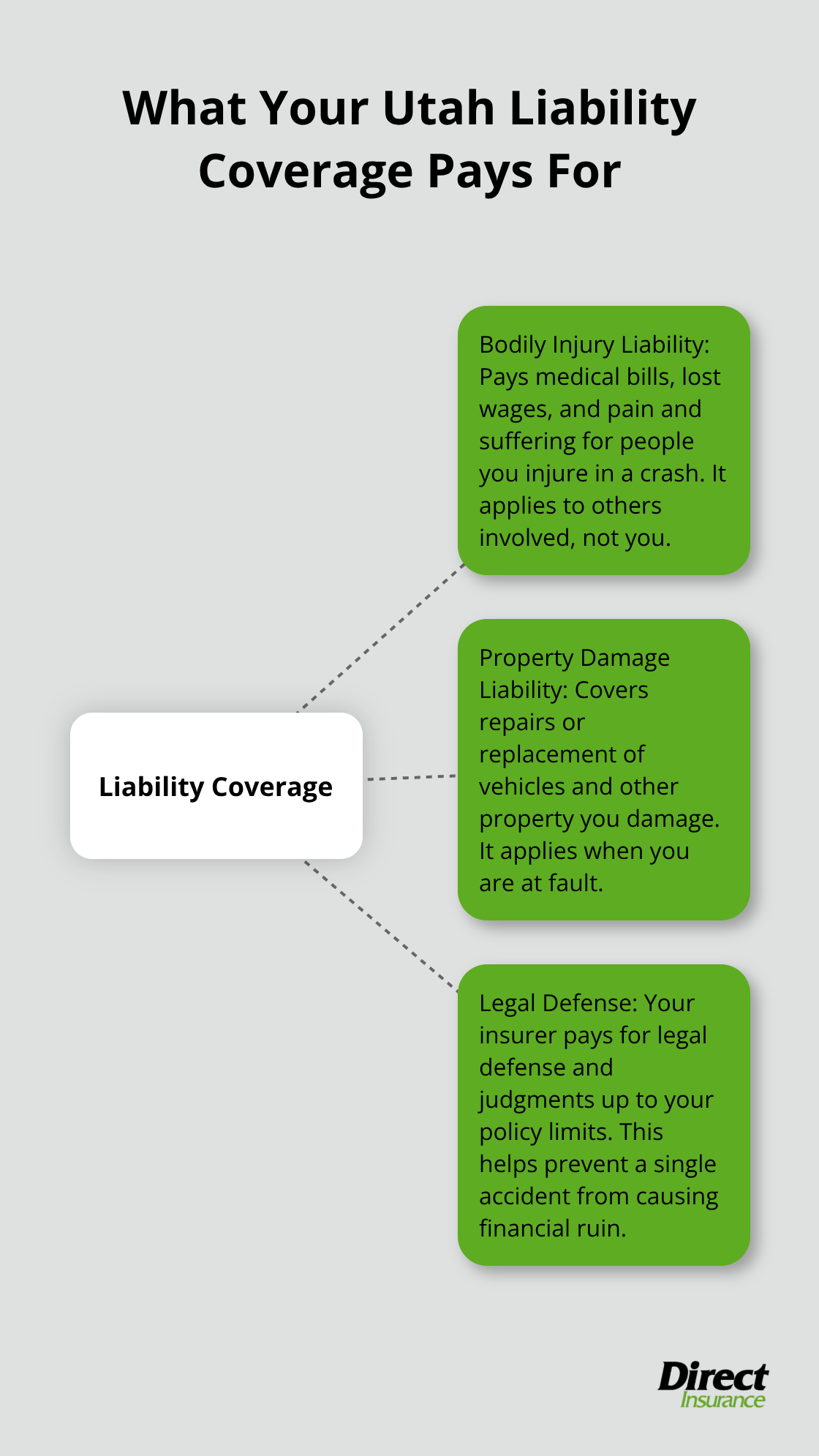

Liability protection is where Utah condo owners face their largest exposure gap. Your HO-6 liability coverage pays for medical expenses and legal defense if someone is injured inside your unit or if you accidentally damage someone else’s property. The standard starting point is $100,000 to $300,000, but this is dangerously low given Utah’s claims history.

According to data analyzed from Colorado and Utah claims, 68% of condo owners carry insufficient liability limits, and average liability claims exceed $30,000 across the region. A Salt Lake City homeowner faced a $42,700 dog bite claim that nearly exhausted a $100,000 liability limit, leaving minimal cushion for legal fees. This case demonstrates how quickly a single incident can consume your entire liability protection.

We recommend upgrading to at least $300,000 in liability coverage, with $500,000 as the stronger choice if you host guests regularly or own pets. An umbrella policy providing an additional $1,000,000 in liability protection costs roughly $100 to $200 annually and should be seriously considered if you have meaningful assets to protect.

Water Damage and Shared Wall Liability

Water damage claims represent another critical liability exposure in Utah condos because shared walls mean damage can spread to neighboring units, triggering claims that pull on your liability coverage. A Boulder multi-unit water leak resulted in $110,000 in total losses, but the insured with $500,000 liability coverage plus a $1,000,000 umbrella policy paid only a $1,000 deductible. This example shows how adequate liability limits protect you when water damage affects multiple units.

Additional coverages like loss assessment protection help cover your share of HOA charges if the master policy fails to cover damage to common areas, shifting costs to individual unit owners. Water backup coverage is practical if your unit sits on a lower floor or in an area prone to heavy snow melt.

Protecting High-Value Items and Building Code Changes

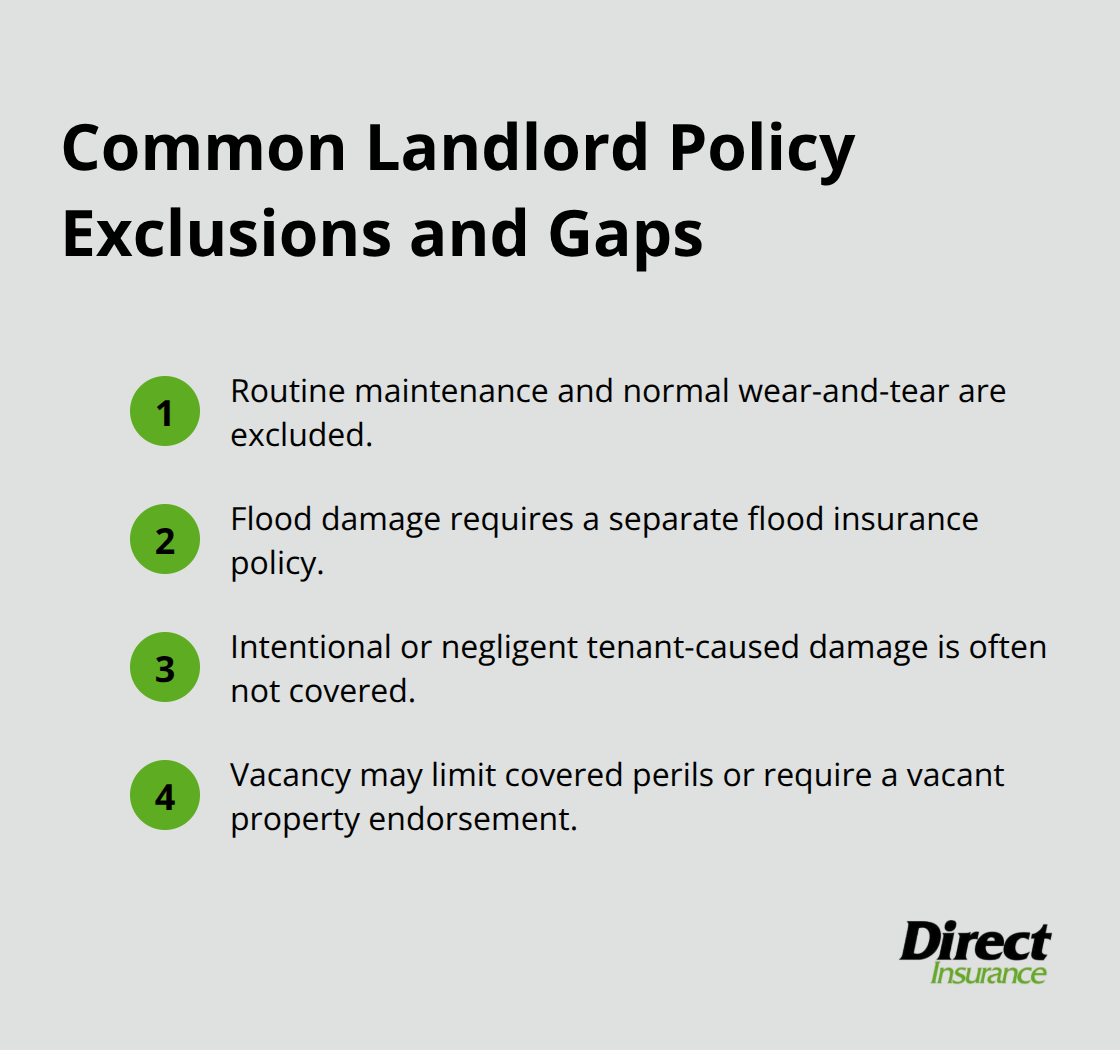

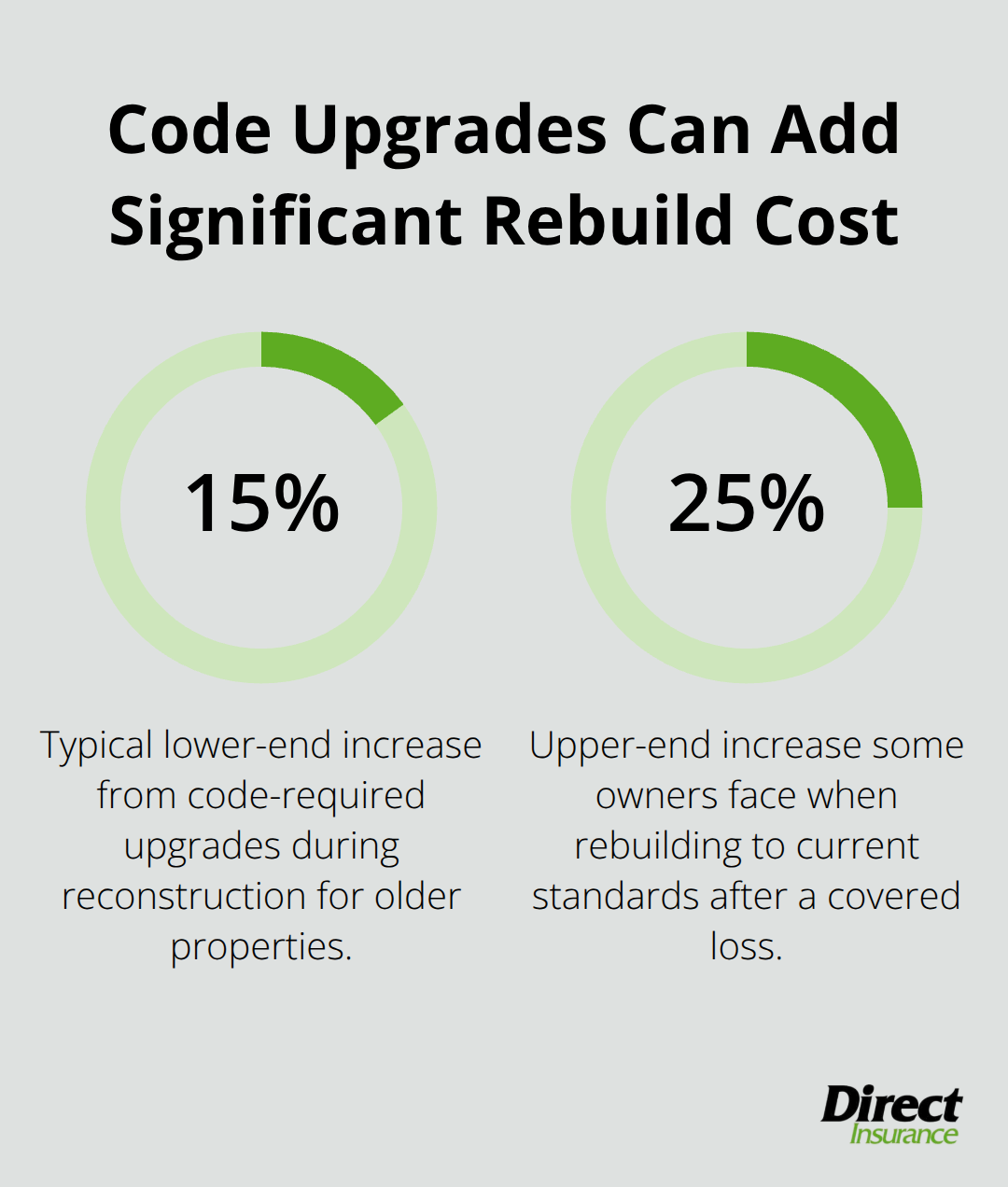

Scheduled personal property endorsements protect high-value jewelry, art, or collectibles that exceed standard coverage limits. Building code coverage pays the difference between pre-loss construction standards and upgraded codes now required by law, potentially saving thousands during major repairs. These endorsements address specific gaps that standard HO-6 policies leave unprotected.

The decisions you make about liability limits, deductibles, and additional endorsements directly shape how well your policy protects you when claims occur. Understanding what each coverage type actually pays for positions you to make informed choices about which protections matter most for your situation and assets. The next step involves examining how your specific location, building characteristics, and personal history affect what you’ll actually pay for this protection.

What Drives Your Utah Condo Insurance Premium

Your condo insurance premium in Utah reflects specific factors that insurers measure and weigh differently depending on the carrier. Geographic location stands as the single most influential cost driver. According to Insure.com’s analysis of 34,588 ZIP codes, Salt Lake City condo owners pay approximately $669 annually while Layton residents pay around $620 for identical coverage-a $49 difference that stems entirely from local construction costs, weather exposure, and claims history in each area. Provo sits at $682, West Jordan at $635, Sandy at $653, Ogden at $656, and Orem at $687. These variations exist because insurers track local loss patterns meticulously.

How Location Shapes Your Costs

A zip code with frequent water damage claims from snow melt or higher wildfire exposure commands higher premiums than areas with cleaner claims records. Building age and construction materials matter significantly because older structures with outdated electrical systems or materials create higher loss frequency. Homes built with fire-resistant materials may have lower premiums than more flammable materials such as wood roofs. Insurers also scrutinize whether the HOA has implemented protective devices like fire suppression systems or burglar alarms in common areas, which can lower your personal premium modestly.

Credit Score and Claims History Impact

Your credit score and claims history shape your premium just as decisively as physical building characteristics. Insure.com’s methodology, which surveyed rates across 145 companies, applied a good credit tier to all quotes, meaning lower credit scores would push premiums higher than the reported $668 average. Carriers in Utah use credit-based insurance scores because statistical data shows correlation between financial responsibility and claim frequency. One prior claim within five years can increase your annual premium by 10 to 25 percent depending on the carrier and claim type.

Pet Ownership and Lifestyle Factors

Pet ownership introduces another cost factor-pet-related claims in Salt Lake City rose 18 percent recently with average settlements around $38,000, prompting insurers to charge more for households with dogs or cats, particularly breeds flagged as higher liability risk. Your lifestyle choices and household composition directly affect how insurers price your coverage.

Comparing Carrier Pricing Models

State Farm, Allstate, and Iowa Farm Bureau command different premiums for the same coverage because each carrier weights these factors differently based on their own claims data and risk models. A quote from State Farm at $266 annually versus Allstate at $321 for comparable coverage illustrates how carrier underwriting philosophy affects your actual cost. Shopping multiple quotes reveals these differences immediately. Direct Insurance Services works with multiple carriers as an independent agency, which allows us to match your specific risk profile to the insurer offering the best rate for your situation rather than forcing you into a single carrier’s pricing model. The practical reality is that your premium reflects measurable risk, and understanding which factors drive your specific quote empowers you to make adjustments that lower costs without sacrificing protection.

Final Thoughts

Condo insurance in Utah requires understanding three core realities: your HO-6 policy covers what the HOA master policy doesn’t, liability protection is your largest exposure gap, and your premium reflects measurable risk factors specific to your location and building. The average Utah condo owner pays $668 annually, but this figure masks significant variation based on where you live, your building’s age and materials, and your personal claims history. State Farm’s $266 annual rate versus Allstate’s $321 for comparable coverage demonstrates how shopping multiple carriers directly impacts your wallet.

The practical steps forward involve requesting your HOA master policy to identify coverage gaps, then requesting quotes from at least three carriers to compare pricing and coverage options. Many Utah condo owners accept minimum $100,000 liability limits when 68% of condo owners in the region carry insufficient protection-a single dog bite or water damage claim can exceed $30,000, consuming your entire liability limit and exposing your personal assets. Upgrading to $300,000 or $500,000 in liability coverage costs modestly more but protects what matters.

An independent agent transforms this process from overwhelming to manageable by comparing options across multiple companies, explaining the trade-offs between deductibles and premiums, and identifying endorsements that address your actual risks. Contact Direct Insurance Services to review your current condo insurance Utah guide or get quotes for new coverage.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation