How to Choose the Right Home Contents Insurance

Your home contents insurance protects the belongings inside your home from theft, damage, and disasters. Without it, you’d face significant financial loss if something happened to your furniture, electronics, or other personal items.

At Direct Insurance Services, we help homeowners find coverage that matches their actual needs and budget. This guide walks you through assessing your belongings, comparing policies, and securing the best rates.

What Home Contents Insurance Actually Covers

Home contents insurance protects the personal belongings inside your home from theft, fire, windstorms, and other covered perils. This includes furniture, electronics, clothing, kitchen appliances, and nearly everything else you own. The coverage applies to items permanently installed in your home as well as portable possessions. Most policies cover belongings both inside your home and away from it, though away-from-home coverage typically has limits. If your laptop gets stolen while traveling, contents insurance can help pay for its replacement. The actual scope depends on your policy wording, so reading what’s included and excluded matters before you buy.

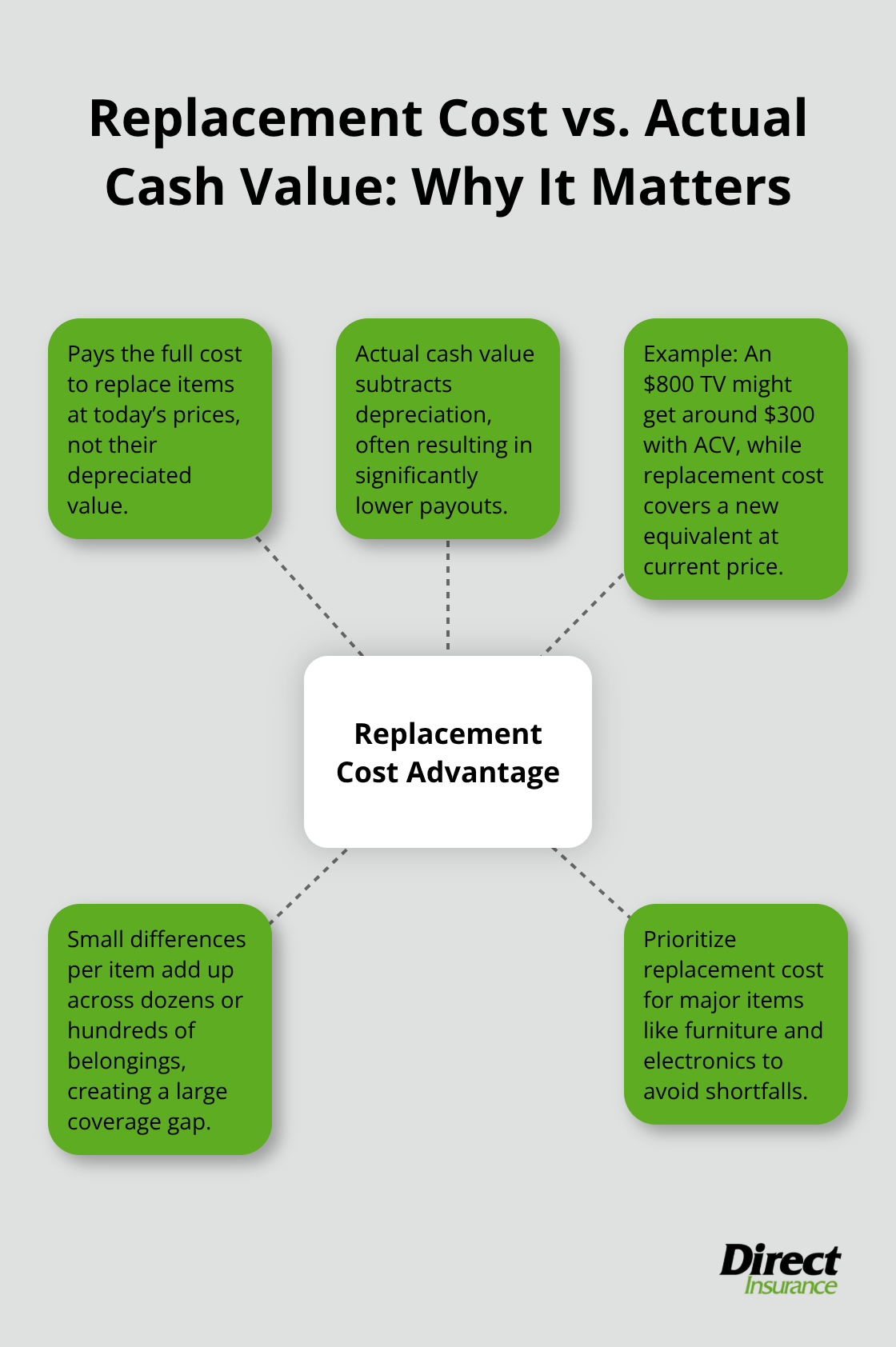

Why Replacement Cost Outperforms Actual Cash Value

The Insurance Information Institute emphasizes that replacement cost coverage significantly outperforms actual cash value coverage when you file a claim. Replacement cost pays what it costs to replace an item at today’s prices, while actual cash value subtracts depreciation from the payout. A five-year-old television worth $800 new might only receive $300 under actual cash value after depreciation, but replacement cost would cover a new TV at current market price. This difference becomes enormous when you add up dozens or hundreds of items. Insisting on replacement cost coverage for major items like furniture and electronics prevents this financial gap.

High-Value Items Need Separate Protection

High-value items like jewelry, art, and watches often require separate scheduling and professional valuations to protect them fully. Standard policies cap coverage on valuables, which means your expensive watch or diamond ring may not receive full replacement cost protection under the main policy. A separate rider or scheduled endorsement covers these items at their full replacement value without depreciation. Professional appraisals establish the actual value of your possessions and support your claim if loss occurs. This extra step takes time upfront but saves thousands of dollars when you need to replace something irreplaceable.

Security Features Lower Your Premium Significantly

Homes with monitored security systems, burglar alarms, and deadbolt locks qualify for meaningful premium discounts with most carriers. The Association of British Insurers reports that security features can reduce your annual premium by several percentage points. A home with a professionally monitored alarm system might pay $50 to $150 less per year than an identical home without one. Safes for valuables and upgraded door locks also trigger discounts. These improvements protect your belongings while directly lowering what you pay for coverage. Installing a new alarm system costs $500 to $2,000 upfront but pays for itself through premium savings over three to five years.

Next Steps: Assessing Your Actual Coverage Needs

Now that you understand what contents insurance covers and how replacement cost works, the next step involves calculating the total value of your belongings and comparing what different policies offer. This assessment determines whether you have adequate coverage limits and identifies which additional options make sense for your situation.

What Your Belongings Are Actually Worth

Start by creating a detailed home contents inventory with replacement costs for each item or category. This isn’t theoretical-you need actual numbers. Walk through your home room by room and estimate what it would cost to replace each possession at today’s prices, not what you paid years ago. Furniture, electronics, clothing, kitchen appliances, artwork, and collectibles all add up quickly. Most homeowners underestimate their total by 20 to 40 percent because they forget items stored in closets, basements, and attics. A modest home typically contains $30,000 to $50,000 worth of belongings, while homes with more furniture, electronics, or valuables can easily exceed $75,000.

Calculate Your Total and Match It to Your Coverage Limit

Once you have this total, you’ll know what coverage limit you actually need. Many policies set contents limits as a percentage of your dwelling coverage, often around 70 percent, but this standard doesn’t match every home. If your calculated total is $45,000, you need a contents limit of at least $45,000, not whatever default your policy offers. Use receipts, online pricing tools, and professional valuations for high-value items to make your numbers solid. Take photos of major possessions and store them in cloud storage so you have proof if you ever need to file a claim.

Deductibles Create Real Trade-offs Between Premium and Out-of-Pocket Cost

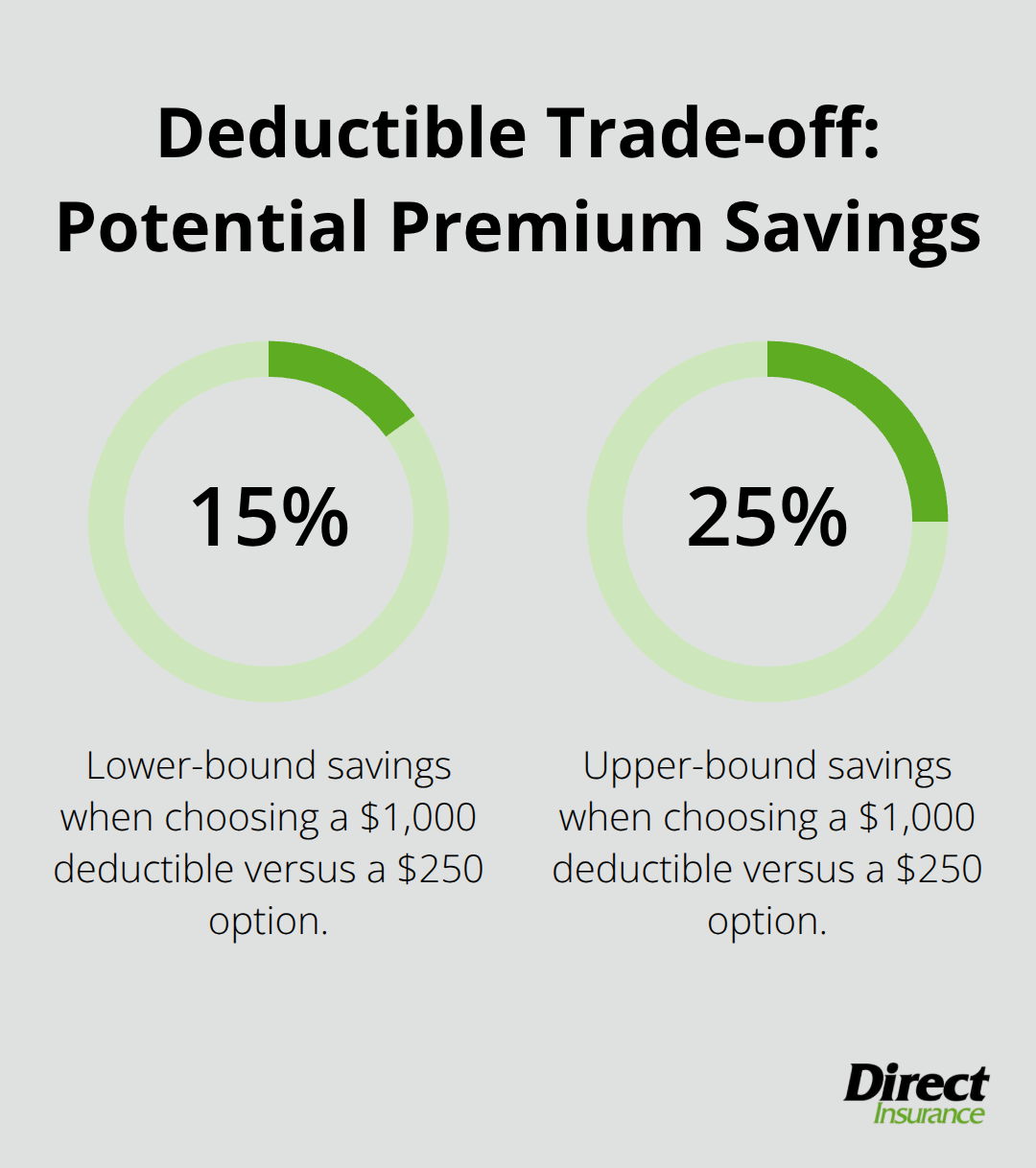

Your deductible is the amount you pay out of pocket when you file a claim, and it directly affects your premium. A $500 deductible costs less annually than a $250 deductible, but you’ll pay $500 if you claim something. A $1,000 deductible can save you 15 to 25 percent on your annual premium compared to a $250 option. The math works only if you can actually afford that deductible when a loss happens. If a fire damages your home and you have a $1,000 deductible, you need to have that money available immediately.

Choose a deductible you can genuinely pay without financial strain. Avoid the trap of picking the highest deductible just to lower your premium if it means you couldn’t cover a real loss. Many homeowners benefit from a $500 or $750 deductible-low enough to manage but high enough to reduce what you pay annually.

High-Value Items Demand Individual Attention and Professional Assessment

Standard contents policies cap coverage on specific categories of valuables. Jewelry typically has a $2,500 limit, watches might be $5,000, and collectibles often face similar restrictions. If you own a diamond ring worth $8,000 or a collection of vintage watches, that standard limit leaves you vastly underinsured. A scheduled endorsement or separate rider for valuables removes these caps and covers items at their full appraised value. This requires obtaining professional appraisals from qualified gemologists or specialists, which costs $200 to $500 per item but becomes essential documentation if you ever claim. Professional appraisals also give you credibility with your insurer when you file a claim-they’ve verified the value independently. Update these appraisals every three to five years because values change.

Accidental Damage Coverage Protects Against Everyday Mishaps

Accidental damage coverage is another option worth evaluating separately. Standard policies exclude damage from spills, drops, or accidents, but accidental damage riders cover these mishaps. If you have expensive electronics or artwork, accidental damage protection prevents a costly accident from becoming a total loss. This rider adds to your premium but protects items that face real risk in daily life. The cost-benefit analysis depends on what you own and how you use it-a household with young children or pets faces higher accident risk than a careful, adult-only home.

Understanding what your belongings are worth and selecting appropriate coverage limits sets the foundation for adequate protection. The next step involves comparing actual policies and identifying which carriers offer the best combination of coverage, price, and service for your specific situation.

Lower Your Premium Without Sacrificing Coverage

Bundle Policies to Cut Your Total Cost

Bundling your home contents insurance with auto coverage delivers the most straightforward savings available. Bundling homeowners with auto insurance is one of the most common discounts available. If you currently carry auto insurance with one company and home coverage elsewhere, consolidating both policies with a single insurer immediately cuts your total premium. Many carriers offer 10 to 15 percent off each policy when you bundle, which compounds into real money across multiple years. The math is simple: if your bundled annual premium would be $1,800 instead of $2,200 without the discount, you save $400 per year or $2,000 over five years. Start with bundled quotes from your current auto insurer, then compare those quotes against standalone home contents policies from other carriers to confirm you’re actually getting the best rate.

Install Security Features That Lower Premiums

Home security improvements directly lower your premium while protecting your belongings simultaneously. The Association of British Insurers confirms that security features including monitored alarm systems, burglar alarms, and deadbolt locks qualify for meaningful reductions. A professionally monitored security system typically reduces your annual premium by $50 to $150 depending on your carrier and location. A new impact-resistant roof, which takes security further by protecting against weather damage, can save up to 35 percent in some states according to the Insurance Information Institute. Other improvements that trigger discounts include leak detection systems, upgraded door locks, and safes for valuables, each typically saving 2 to 6 percent on your annual premium. These improvements pay for themselves through premium savings within three to five years while simultaneously reducing your actual risk of loss.

After you implement security upgrades, contact your insurer to confirm they’ve applied the corresponding discounts to your policy.

Compare Quotes Annually to Avoid Overpaying

Annual policy reviews matter because your coverage needs and available discounts change over time. Consumer Reports data shows that 20 percent of homeowners switched insurers in the last five years, with 44 percent doing so specifically because of premium increases. Rather than accepting annual rate hikes, spend 30 minutes each year comparing quotes from three to five carriers using platforms like The Zebra, which processes over 74 million quotes and shows real insurer quotes without markups or additional fees. You can obtain personalized quotes in approximately 5 minutes after answering basic questions about your home and belongings. Shopping annually prevents loyalty from costing you money since carriers rarely reward long-term customers with competitive rates. When comparing options, look for proven strategies to lower your premiums that apply across both auto and home coverage, since many discount principles overlap between policy types.

Final Thoughts

Choosing the right home contents insurance means matching your coverage to what you actually own, not settling for whatever default limit your policy offers. You’ve calculated your belongings’ replacement cost, understood the difference between actual cash value and replacement cost coverage, and identified which additional protections matter for your situation. The work you’ve done to inventory your possessions and assess your needs directly translates into adequate protection when you need it most.

The balance between cost and coverage requires honest evaluation of your deductible tolerance and which add-ons genuinely protect your lifestyle. A $500 deductible paired with replacement cost coverage on major items and a separate rider for valuables costs more than bare-minimum coverage, but it prevents the financial devastation that comes from underinsurance. One spilled drink on expensive electronics could cost thousands, so skipping accidental damage coverage to save $100 annually often backfires.

At Direct Insurance Services, our team helps Utah families and individuals navigate these decisions by comparing options from top-rated carriers and explaining what each home contents insurance policy actually covers. We handle the complexity so you can focus on selecting coverage that fits your needs and budget. Contact us today to review your current coverage or get quotes on new protection that safeguards what matters most to you.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation