Types of Home Insurance Coverage Explained

Most homeowners don’t fully understand what their policy actually covers. The gap between what you think you’re protected for and what you’re actually protected for can be expensive.

We at Direct Insurance Services see this confusion firsthand. That’s why we’ve broken down the main types of home insurance coverage so you can make informed decisions about your protection.

What Your Dwelling Coverage Actually Protects

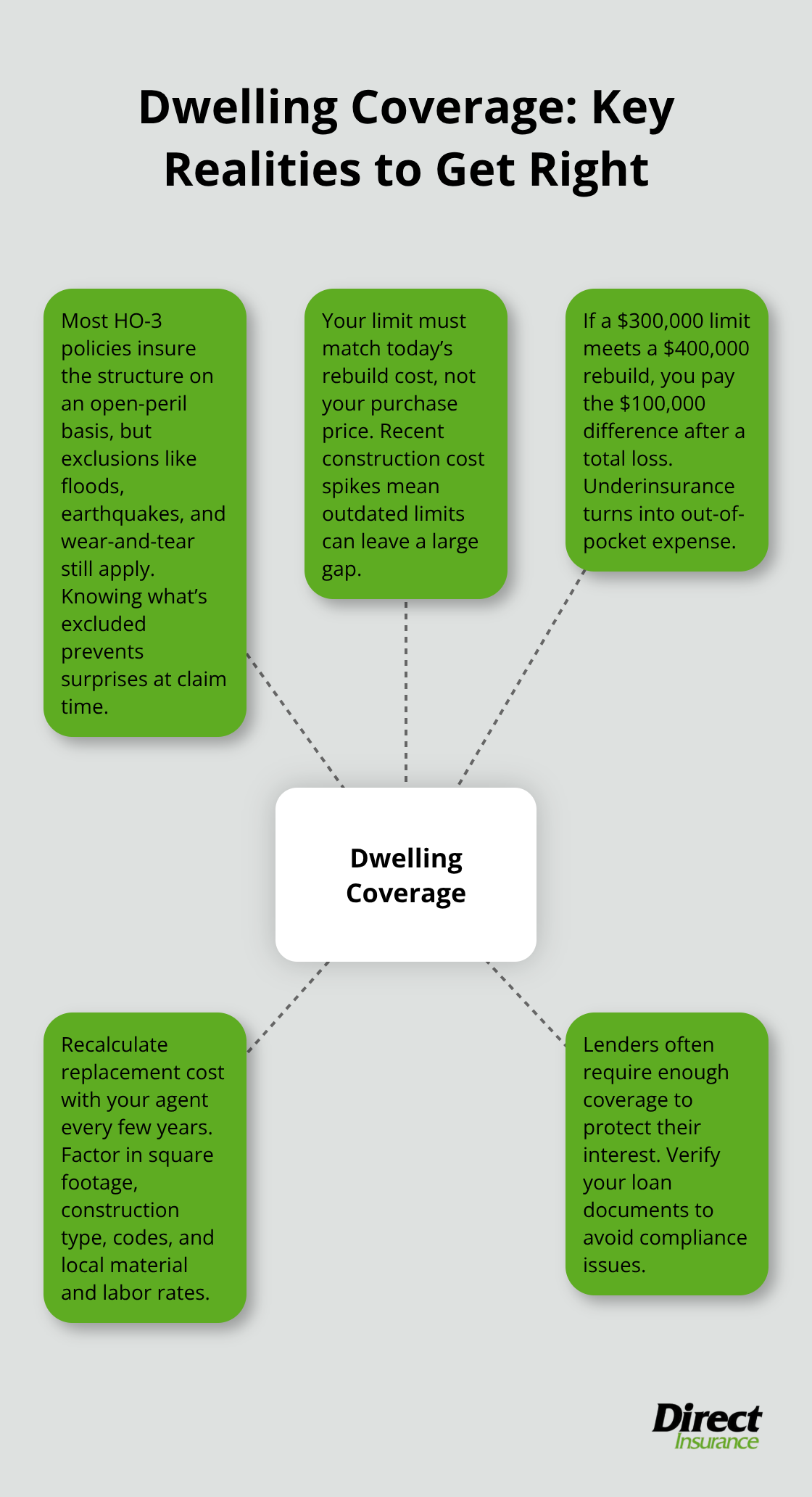

Your dwelling coverage forms the backbone of your homeowners insurance, and it’s where most policies diverge in what they actually pay out. Dwelling coverage protects the structure of your home-the walls, roof, foundation, built-in appliances, and attached structures like garages or decks. When you have an HO-3 policy (the most common form for single-family homes), your dwelling receives coverage on an open-peril basis. This means nearly everything receives protection except for the exclusions listed in your policy, such as floods, earthquakes, and wear-and-tear. The Insurance Information Institute reports that home replacement costs surged roughly 55 percent between 2019 and 2022, then climbed another 2.5 percent in 2023. This matters because your coverage limit must reflect what it actually costs to rebuild today, not what you paid for the house five years ago. If your limit sits at $300,000 but your home would cost $400,000 to rebuild, you’re underinsured and will absorb the difference out of pocket after a total loss.

Coverage Limits That Match Reality

Your dwelling limit should reflect replacement cost-what it would take to rebuild from the ground up with materials and labor at current prices. Many homeowners make the mistake of using their purchase price as a baseline, which almost guarantees underinsurance given how fast construction costs have climbed. The right approach involves working with your agent to calculate a replacement-cost assessment that accounts for your home’s square footage, construction type, local building codes, and current material and labor rates in your area. This assessment should happen at least every few years, especially if you’re in a market where costs are rising faster than the national average. Your mortgage lender may also require you to carry enough dwelling coverage to protect their investment, so check your loan documents.

Replacement Cost Versus Actual Cash Value

Here’s where policy language matters: replacement cost coverage pays what it costs to replace damaged items with new equivalents, while actual cash value subtracts depreciation. An HO-3 typically covers your dwelling at replacement cost but covers personal property at actual cash value unless you add an endorsement. This distinction can mean thousands of dollars in a claim. If your roof sustains damage in a hail storm and replacement cost coverage applies, the insurer pays for a brand-new roof. With actual cash value, they pay for a roof minus what they estimate it has depreciated-potentially leaving you short if your roof was already ten years old. The same principle applies to interior damage: replacement cost pays to restore your home to its pre-loss condition with new materials, while actual cash value accounts for the age and condition of what was damaged. For your dwelling structure, replacement cost is standard on most HO-3 policies, but always verify this with your agent because some carriers or older policies may differ.

Why Personal Property Coverage Requires Different Thinking

Your dwelling protection covers the structure itself, but what about everything inside? Personal property coverage operates under different rules and limits than your dwelling protection, which means you need to understand how these two coverages work together. Most HO-3 policies cover personal property at actual cash value rather than replacement cost, creating a significant gap in protection for your belongings. This is where the next layer of your policy becomes critical to understand.

Personal Property and Liability Coverage

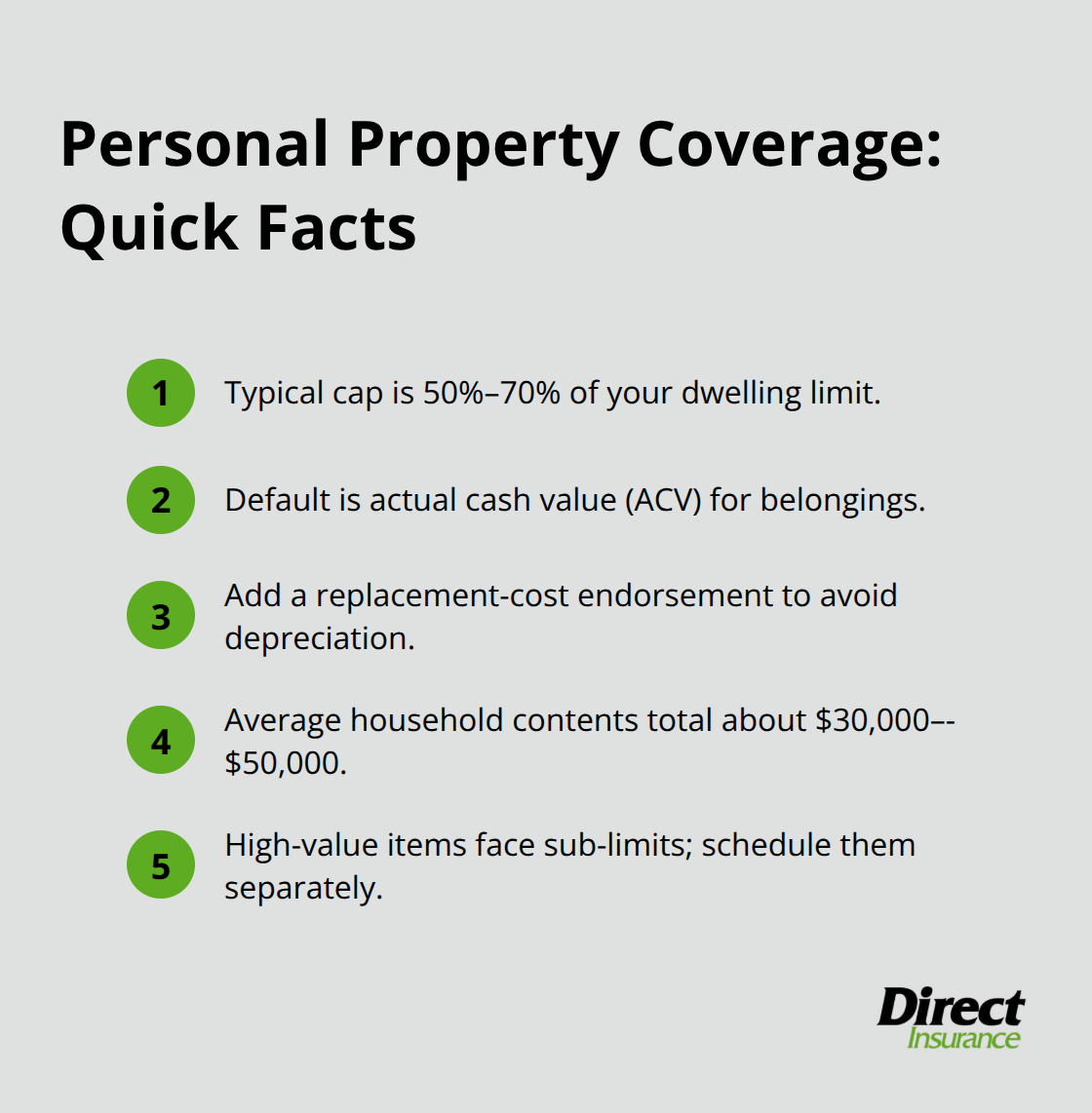

Personal property coverage protects the items inside your home-furniture, electronics, clothing, kitchenware, and everything else you own. Unlike your dwelling protection, which covers the structure itself, personal property coverage has a ceiling that typically sits at 50 to 70 percent of your dwelling limit. If your dwelling limit is $400,000, your personal property coverage might max out at $200,000 to $280,000. This matters because many homeowners don’t realize this cap exists until they file a claim and discover they’re significantly underinsured for their belongings.

How Personal Property Coverage Actually Works

Most HO-3 policies cover personal property at actual cash value, meaning a five-year-old television worth $800 new will be paid out at maybe $300 after depreciation is factored in. The Insurance Information Institute notes that the average American home contains approximately $30,000 to $50,000 worth of personal belongings, yet most standard policies won’t cover items close to replacement cost. To close this gap, you can add a replacement-cost endorsement for personal property, which pays what it costs to replace items with new equivalents rather than accounting for age and wear. This endorsement typically costs 10 to 15 percent more but protects you from the depreciation trap that catches most homeowners off guard.

Understanding Your Liability Protection

Liability coverage is fundamentally different from property protection-it covers your legal responsibility if someone gets injured on your property or you accidentally damage someone else’s property. Your HO-3 typically includes $100,000 to $300,000 in personal liability coverage, which sounds substantial until you consider that a serious injury lawsuit can easily exceed $500,000 in damages. If a guest slips on your icy walkway and breaks their leg requiring surgery and ongoing care, their medical bills plus pain and suffering could quickly surpass your policy limit, leaving you personally liable for the difference.

Why Higher Liability Limits Make Financial Sense

Most homeowners carry insufficient liability protection relative to their actual risk exposure. Try carrying at least $300,000 in liability coverage, and those with significant assets should consider $500,000 or higher. The cost difference between a $300,000 and $500,000 liability limit is typically just $10 to $20 per year, making the upgrade a practical decision rather than an expensive one. Your policy also covers medical payments to others, which is a separate benefit that pays up to $1,000 or $5,000 (depending on your policy) toward minor injuries without requiring someone to prove you were negligent. This coverage is valuable because it can resolve small claims quickly without involving your liability coverage limit.

What Happens When Coverage Gaps Appear

The combination of personal property and liability coverage creates the foundation for protecting both your belongings and your finances, yet gaps often emerge when homeowners don’t assess their actual needs against their policy limits. Your next layer of protection-additional coverages and optional add-ons-fills many of these gaps and addresses the specific hazards that standard policies exclude.

Closing the Gaps Standard Policies Leave Behind

Water Damage: The Hidden Risk Most Homeowners Face

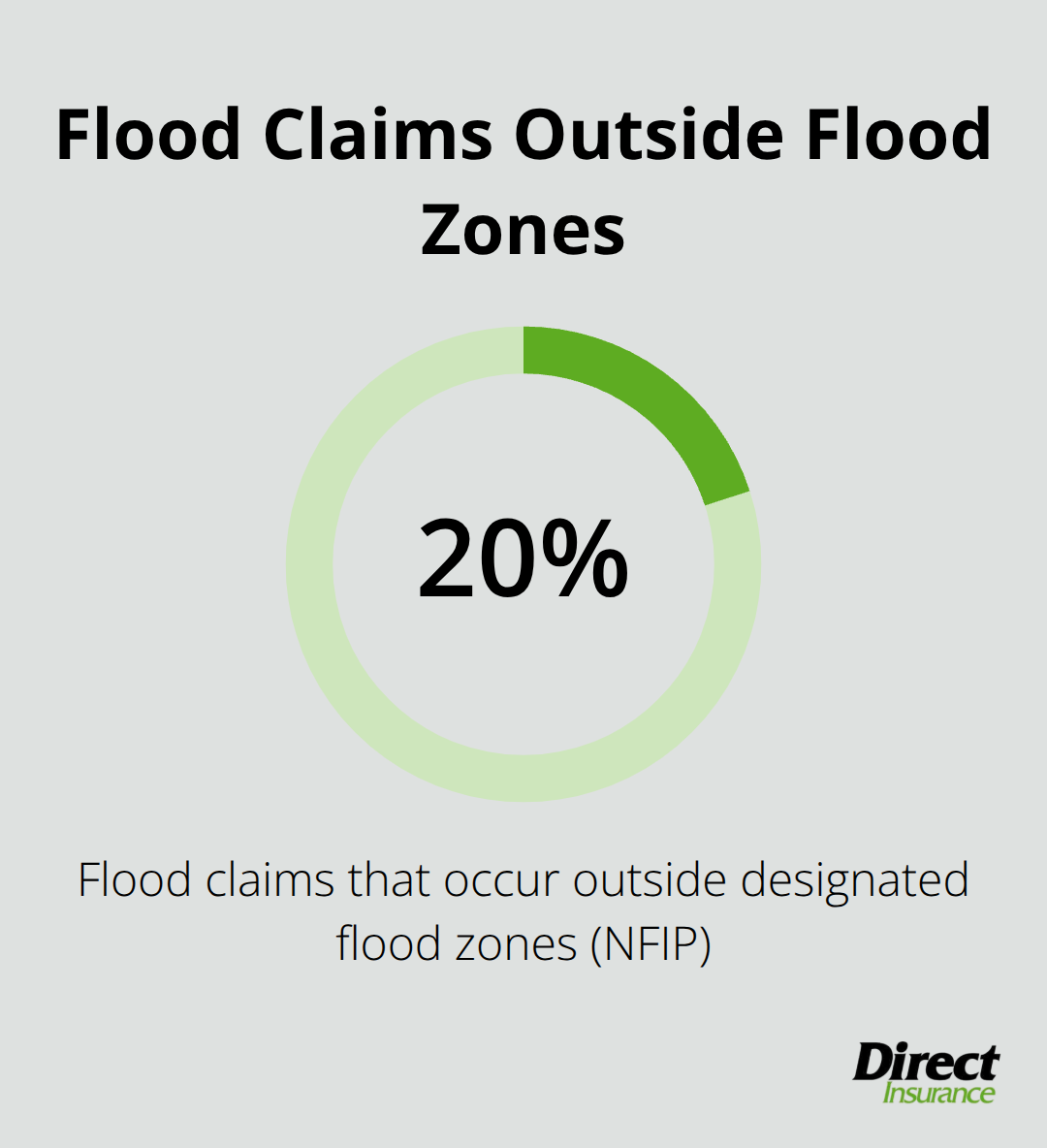

Water damage represents one of the largest sources of home insurance claims, yet most homeowners remain dangerously underprotected. Your standard HO-3 policy covers sudden water damage from burst pipes or failed appliances, but it explicitly excludes flooding from external sources, sewer backups, and groundwater seepage. The National Flood Insurance Program reports that just one inch of flooding in an average home costs approximately $25,000 in damages, and flood claims occur outside designated flood zones roughly 20 percent of the time. This means your zip code’s flood risk rating does not determine whether you need coverage.

If you carry a mortgage in any flood zone, your lender mandates flood insurance through the National Flood Insurance Program, administered by FEMA. However, even if your lender does not require it, the math favors protection: flood insurance through NFIP costs between $400 and $1,200 annually for most homeowners, while a single flood event can cost $25,000 to $100,000 out of pocket. Obtaining a flood insurance quote makes sense regardless of your perceived risk, since the premium difference between protected and unprotected often proves negligible compared to actual loss exposure.

Adding a sewer-backup endorsement to your standard policy typically costs $50 to $150 per year and covers damage from backed-up sewers or drains, a peril that catches many homeowners unprepared. This low-cost addition protects you from one of the most expensive and unpleasant water-related claims.

Earthquake Coverage: Protection in Seismically Active Regions

Earthquake coverage operates similarly to flood insurance: it remains excluded from standard policies and requires separate purchase. California, Washington, and other seismically active states see earthquake insurance premiums ranging from $100 to $500 annually depending on your home’s age and construction, yet most homeowners skip this coverage based on perceived low risk. When earthquakes strike, the damage often exceeds $100,000 per home, making the annual premium investment modest relative to exposure.

Your agent can help you assess whether earthquake coverage makes financial sense for your location and property value. The cost-to-benefit ratio typically favors protection in high-risk areas, particularly if your home sits on older construction or unstable soil.

Protecting High-Value Items Through Scheduled Coverage

Valuable items like jewelry, art, collectibles, and high-end electronics face sub-limits under standard personal property coverage, typically capped at $1,500 to $2,500 total for jewelry and $2,500 to $5,000 for fine arts. If you own items exceeding these limits, scheduled personal property endorsements allow you to list specific pieces and insure them at replacement cost without depreciation.

A diamond ring appraised at $8,000 or a painting valued at $12,000 requires this scheduled coverage to receive full protection. The process involves obtaining appraisals from certified professionals, then adding each item to your policy with its documented value. This costs roughly $25 to $50 per item annually but eliminates the depreciation problem that plagues standard personal property coverage. Your agent can walk you through which items warrant scheduled coverage based on your inventory and values.

Final Thoughts

Understanding the different types of home insurance coverage protects you from financial disaster when loss strikes. Your dwelling coverage protects your structure, personal property coverage protects your belongings, and liability coverage protects your finances when someone gets injured on your property. Standard policies leave gaps-floods, earthquakes, and high-value items require additional protection through separate policies or endorsements.

The real work starts when you assess your actual needs against your current coverage. Review your dwelling limit to confirm it reflects today’s rebuilding costs, not your purchase price from years ago, and check whether your personal property coverage sits at actual cash value or replacement cost. Look at your liability limits and ask yourself whether $100,000 or $300,000 truly protects your assets if someone sues you, then evaluate your specific risks like flood zones, earthquake exposure, or jewelry and art that exceeds your policy’s sub-limits.

This assessment works best with professional guidance. At Direct Insurance Services, we help Utah homeowners navigate these decisions by reviewing their actual needs and matching them to coverage that fits both their protection goals and budget. Contact us for a policy review that identifies gaps and explores solutions tailored to your situation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation