How to Handle Home Insurance Dog Bite Claims

A dog bite incident can turn stressful quickly, especially when you’re unsure about your coverage. At Direct Insurance Services, we know that homeowners often have questions about whether their insurance will actually pay for a home insurance dog bite claim.

This guide walks you through what your policy covers, how to file a claim properly, and what to expect during the process.

Understanding Dog Bite Coverage Under Homeowners Insurance

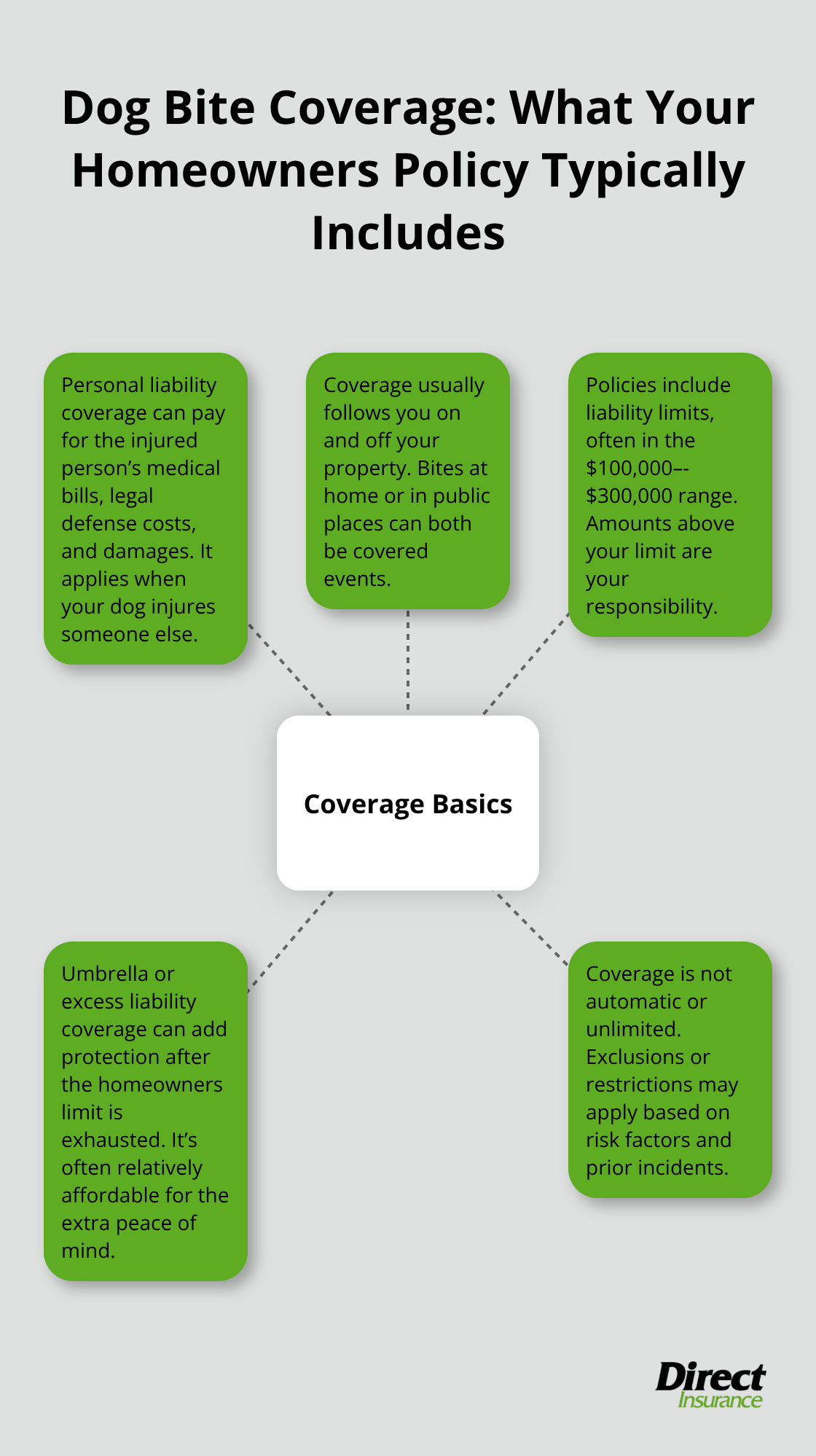

Your homeowners insurance likely covers dog bite liability, but the specifics matter more than you think. Most standard homeowners policies include personal liability coverage that pays for injuries your dog causes to someone else, including medical bills, legal fees, and damages. Your policy typically covers incidents both on and off your property, which means you’re protected whether someone is bitten in your backyard or at a park down the street. However, coverage isn’t automatic or unlimited.

Most homeowners policies come with liability limits ranging from $100,000 to $300,000. If a claim exceeds your limit, you pay the difference out of pocket.

Your Policy Limits and What Happens When Claims Exceed Them

The liability limit on your homeowners policy is the maximum your insurer will pay for a dog bite claim. If the injured person’s medical costs, lost wages, and pain and suffering damages total $150,000 but your limit is only $100,000, your insurer pays $100,000 and you’re responsible for the remaining $50,000. This gap can be significant, especially with serious bites that require multiple surgeries or cause permanent scarring. Some insurers offer umbrella or excess liability coverage that activates when your homeowners policy limit is exhausted, providing an extra layer of protection at a relatively low cost. Many homeowners carry insufficient coverage for their actual risk exposure.

Breed Restrictions and Exclusions You Need to Know

Some insurers exclude certain breeds entirely from coverage or require additional riders and restrictions to maintain it. The Insurance Information Institute notes that some insurers maintain breed-specific ban lists while others evaluate each dog individually based on behavior and history. Pennsylvania and Michigan actually prohibit insurers from canceling or denying coverage based solely on breed, reflecting a shift toward individual risk assessment. What matters most to insurers isn’t necessarily the breed itself but whether your dog has a bite history. A dog with prior bites becomes significantly harder to insure, often resulting in higher premiums, required safety measures like muzzles or secure fencing, or outright exclusions from your policy. The best approach is to contact your insurer directly and disclose your dog’s breed and any history upfront. Hiding information or hoping they don’t ask creates a real risk that coverage could be denied when you need it most.

What You Should Do Right Now

Contact your insurance agent and ask three specific questions: What is your exact liability limit for dog bite claims? Does your policy exclude any dog breeds? What documentation do you need if a bite incident occurs? Your agent can review your current coverage, identify any gaps, and discuss whether you need additional protection through umbrella policies or breed-specific riders. This conversation takes minutes but prevents costly surprises later. Once you understand your coverage, you’ll be prepared to act quickly if an incident happens-and you’ll know exactly what steps to take next.

What to Do Right After a Dog Bite Happens

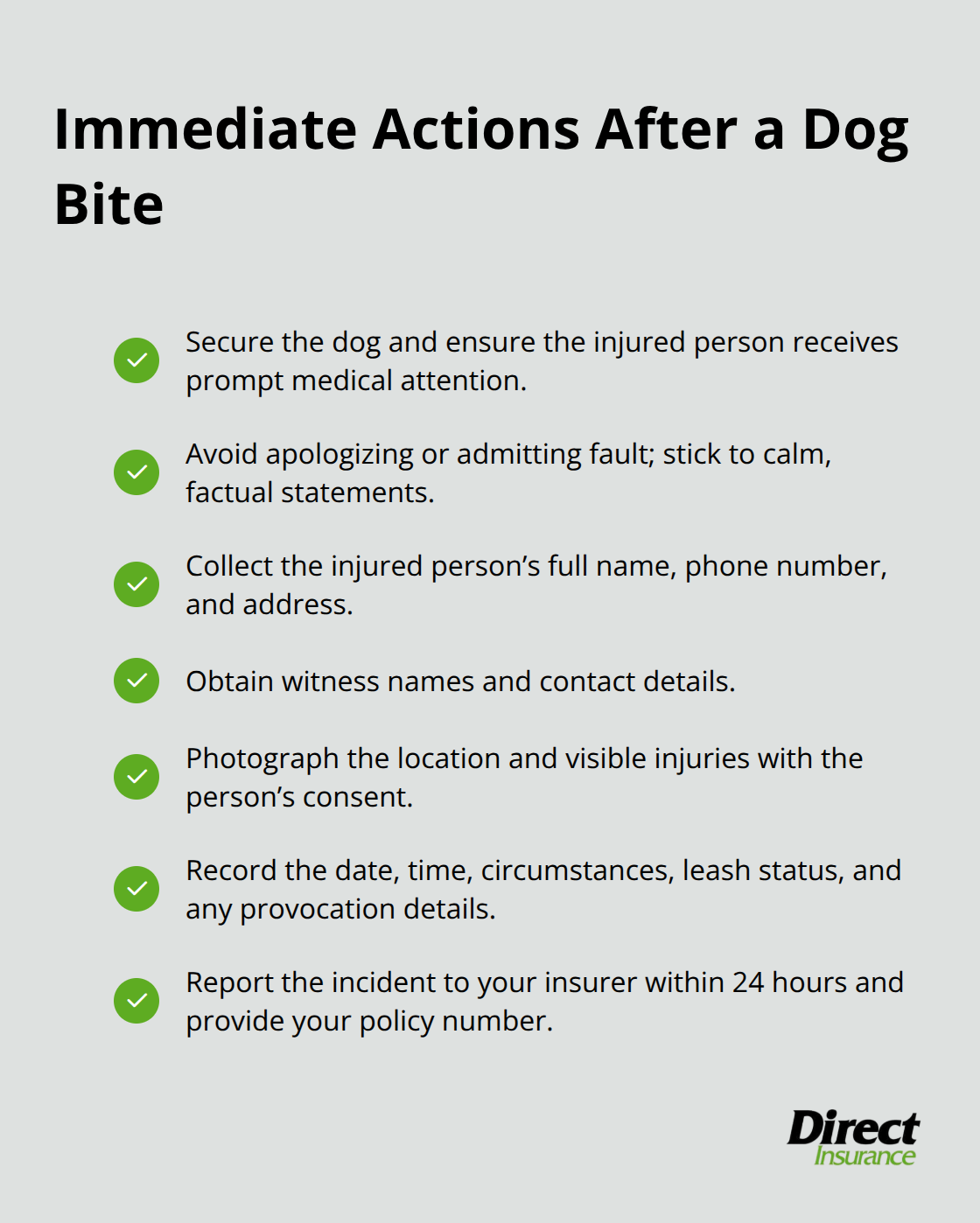

The first few minutes after a dog bite incident determine how smoothly your claim will proceed. Your immediate priority is securing the dog and ensuring the injured person receives medical attention, but what happens next directly affects your insurance outcome. Avoid apologizing or admitting fault at the scene, as insurers can interpret these statements as admissions of liability that complicate claim handling. Instead, stay calm and focus on gathering specific information.

Gather Information at the Scene

Collect the injured person’s full name, phone number, and address. Ask about their injuries and whether they’re seeking medical care. Obtain names and contact details from anyone who witnessed the bite. Photograph the location where the bite occurred and any visible injuries if the person consents. Note the date, time, and circumstances of the incident. Write down everything you remember while details are fresh, including what your dog was doing before the bite, whether the dog was leashed, and whether the injured person provoked the dog in any way.

According to the Insurance Information Institute, thorough documentation at this stage strengthens your claim significantly.

Report to Your Insurer Immediately

Contact your insurance agent or company within 24 hours, not days or weeks. Delays in reporting can actually jeopardize coverage, and insurers need to begin their investigation quickly while evidence and witness memories are reliable. When you call, have your policy number ready and provide a clear, factual account of what happened without speculation or emotion. Your insurer will ask detailed questions about the dog’s age, breed, vaccination status, and whether it has any prior bite history, so answer honestly.

Secure Medical Records and Evidence

If the injured person received medical treatment, confirm you have their medical records and bills, as documented injuries are critical evidence that strengthens settlement value. Medical records serve as the primary proof of a bite and help determine your claim’s strength and appropriate settlement amount. Gather these documents as soon as possible and provide them to your insurer.

Let Your Insurer Handle Communications

Don’t sign anything or make financial offers to the injured party without consulting your insurer first, as this could complicate the claims process. Your home insurance company handles communication with the injured party’s attorney or medical providers, not you directly. This separation protects you legally and ensures all statements are documented properly for your defense. Your role is to provide accurate information to your insurer and cooperate fully with their investigation.

Once you’ve taken these immediate steps and your insurer begins investigating, the process moves into the formal claim filing stage. Understanding what information your insurer needs and how to work effectively with your agent during this phase will help you navigate the next critical steps.

Managing Your Claim Through Settlement

How Your Insurer Investigates the Incident

Your insurer’s investigation moves quickly once you report the incident. Within days, an adjuster will contact you with specific questions about the dog, the injured party, and the exact circumstances of the bite. Answer every question truthfully and completely. The insurance claim investigation process includes reviewing medical records to confirm puncture wounds, which serve as the strongest evidence of an actual bite. Without documented puncture wounds, claim value drops significantly because the injury severity becomes harder to prove.

Your insurer will also request statements from any witnesses you identified at the scene, photographs of the incident location, and your dog’s vaccination records. Provide everything requested promptly. Delays frustrate your adjuster and slow the process, while cooperation signals you have nothing to hide. Your insurer will simultaneously contact the injured party’s medical providers to obtain treatment records and bills. These documents become the foundation for settlement negotiations because they show exactly what the injury cost to treat.

Settlement Offers and Negotiation Timelines

Settlement negotiations typically begin within two to four weeks if the claim is straightforward. According to Triple-I data, the average dog bite claim in 2024 cost insurers $69,272, but this figure varies dramatically based on injury severity and your state. New York claims averaged $110,488 while Pennsylvania averaged $88,668, so geographic location matters significantly for settlement expectations.

Your insurer will make an initial settlement offer based on medical costs, lost wages documented in the injured party’s records, and pain and suffering damages appropriate to the injury type.

Most claims settle out of court because litigation costs both sides money and time. If the injured party’s attorney demands more than your policy limit allows, your insurer may recommend accepting the demand or proceeding to trial. This is where your decision matters. Accepting a settlement within your limit protects you from personal liability for amounts above it. Rejecting it and proceeding to trial risks a jury verdict exceeding your limit, leaving you responsible for the excess.

Evaluating Your Case Strength

Work closely with your insurer’s defense attorney to understand the strength of your case. If your dog has no prior bite history and evidence suggests the injured party provoked the dog, your position strengthens considerably. If your dog has bitten before, settlement becomes more attractive because a jury will likely view your dog as a known hazard. The presence or absence of prior incidents fundamentally shapes how a jury perceives your liability and influences settlement value.

What Happens After Settlement

Once settlement is reached, the injured party signs a release preventing future claims related to that incident, and your insurer issues payment. Your claim file closes, though your insurer may impose restrictions on your coverage going forward, such as requiring a muzzle in public or secure fencing, to continue coverage for your dog. These restrictions reflect the insurer’s assessment of ongoing risk and your willingness to implement safety measures that reduce the likelihood of another incident.

Final Thoughts

Dog bite claims are expensive and stressful, but understanding your coverage and acting quickly makes the process manageable. Know your policy limits before an incident happens, disclose your dog’s breed and history to your insurer, and report any bite immediately. Most homeowners policies cover dog bite liability, but gaps exist if your limits are too low or your breed faces exclusion.

Prevent future incidents through responsible dog ownership. Train your dog early and consistently, socialize it in varied environments, and supervise interactions with children and visitors. Keep your dog leashed in public, maintain secure fencing at home, and watch for stress signals that indicate your dog feels threatened or uncomfortable.

Contact your insurance agent and ask about your current liability limits, breed exclusions, and whether umbrella coverage makes sense for your situation. If you need to adjust your home insurance dog bite coverage or identify gaps in your policy, Direct Insurance Services can review your homeowners insurance with top-rated carriers to find coverage that fits your needs and budget. Reach out today to ensure you’re covered.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation