Is Water Damage Covered by Home Insurance?

Water damage can strike without warning, and most homeowners aren’t sure what their policy actually covers. The line between covered incidents and excluded damage is often blurry, leaving you vulnerable to unexpected costs.

At Direct Insurance Services, we’ve seen too many claims denied because homeowners didn’t understand their coverage. This guide breaks down exactly what water damage is covered by home insurance, how to file a claim, and how to prevent costly damage before it happens.

What Your Policy Actually Covers

Your homeowners insurance covers water damage, but only under very specific circumstances. The distinction between what’s covered and what isn’t determines whether you’ll receive a claim payment or face a denial. Water damage accounts for 1.5% of insured homes having such a loss according to the Insurance Information Institute. This frequency makes understanding your coverage essential.

Sudden and Accidental Water Damage

Standard policies cover sudden and accidental water damage from internal sources like burst pipes, leaking appliances, or roof leaks caused by storms. If a pipe ruptures and floods your basement, or your water heater malfunctions and damages your flooring, your policy pays for these events. Roof leaks from wind-driven rain or damage caused by ice dams also fall under standard coverage. The key word is sudden-the damage must happen unexpectedly, not develop over time.

Your policy pays for both the structural repairs through dwelling coverage and replacement of your belongings through personal property coverage, though deductibles and limits apply. If you experience a covered loss, your insurer reimburses you based on your chosen coverage limits and deductible amount.

Gradual Damage Gets Rejected

Water damage from slow leaks, poor maintenance, or wear and tear receives explicit exclusion from standard policies. If your roof has leaked for months because you neglected repairs, or if a pipe gradually corrodes and seeps water into your walls, insurers will deny the claim. Insurance companies view gradual damage as a maintenance responsibility, not an insurable loss.

Mold and mildew fall into a gray area-they receive coverage only as an extension of a covered water event, and remediation costs face limits in your policy. Many homeowners discover too late that their mold coverage cap falls far short of actual remediation costs. Adding a mold remediation endorsement warrants discussion with your agent. Sewage backup, groundwater seeping through foundation walls, and water damage from poorly maintained plumbing receive no coverage under standard policies. These exclusions are deliberate, and they leave significant gaps that require separate endorsements or riders to address.

Flood Damage Requires Different Insurance

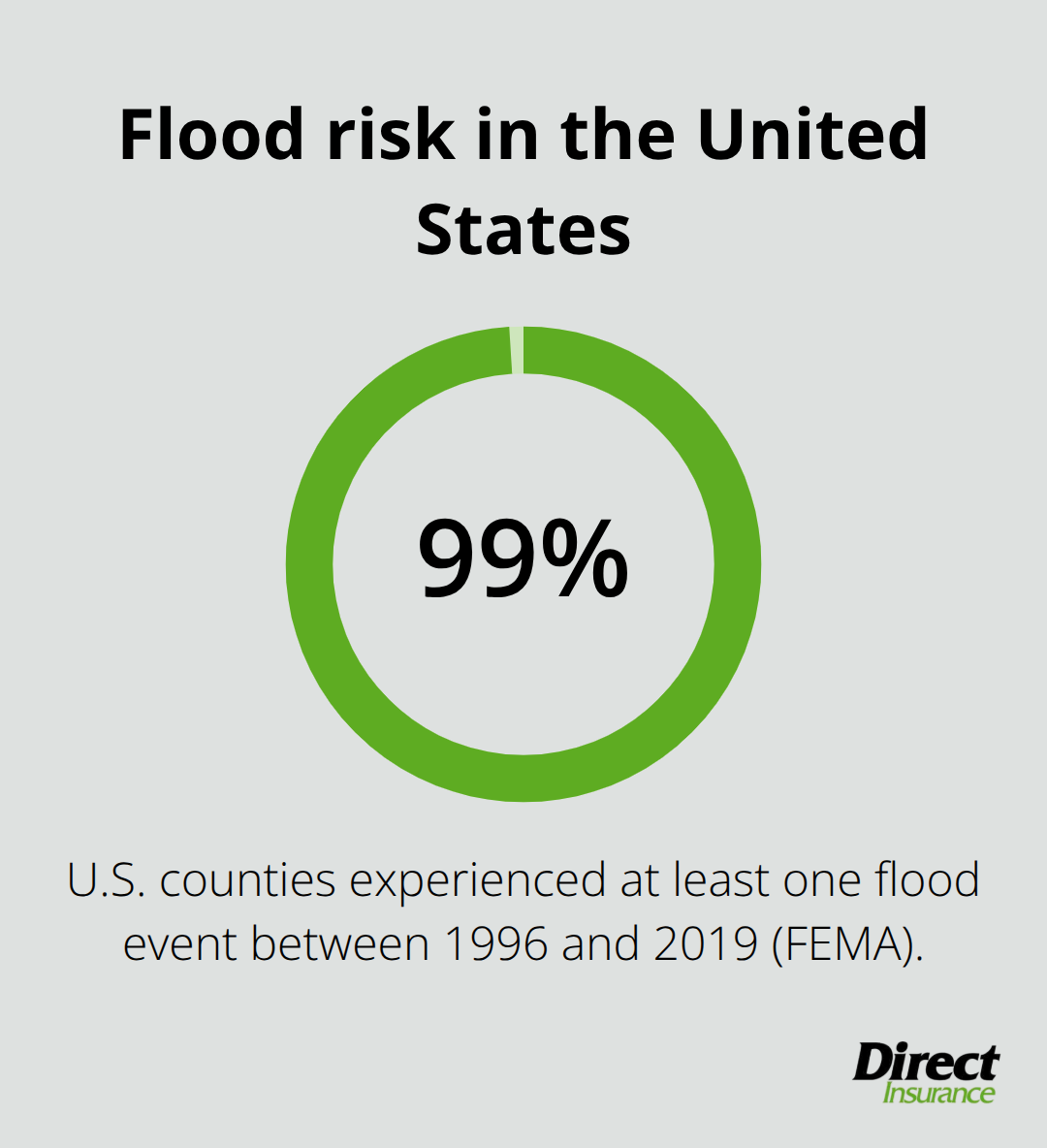

Flooding represents the biggest exclusion in homeowners insurance, and it applies absolutely. Whether water rises from rivers, heavy rainfall overwhelms drainage systems, or storm surge affects coastal properties, standard policies provide zero coverage. According to FEMA, flood damage has caused about $1 trillion in damages since 1980, and 99% of U.S. counties experienced a flood event between 1996 and 2019.

The National Flood Insurance Program defines flood as a general and temporary inundation affecting two or more acres or two or more properties. If only your home experiences interior water intrusion while neighbors remain dry, that’s typically a water damage claim. If multiple properties flood together, it’s a flood claim and requires separate flood insurance. NFIP flood policies cover residential buildings up to $250,000 and contents up to $100,000, though private flood insurance can offer higher limits.

Most flood policies require a 30-day waiting period before coverage takes effect, so purchasing coverage before storm season is critical. If you live in a flood-prone area or even moderate-risk zone, flood insurance is not optional-it’s financial protection you cannot afford to skip. Understanding these coverage gaps helps you identify which endorsements and additional policies you need before water damage strikes your home.

Filing Your Water Damage Claim the Right Way

Act Fast to Protect Your Coverage

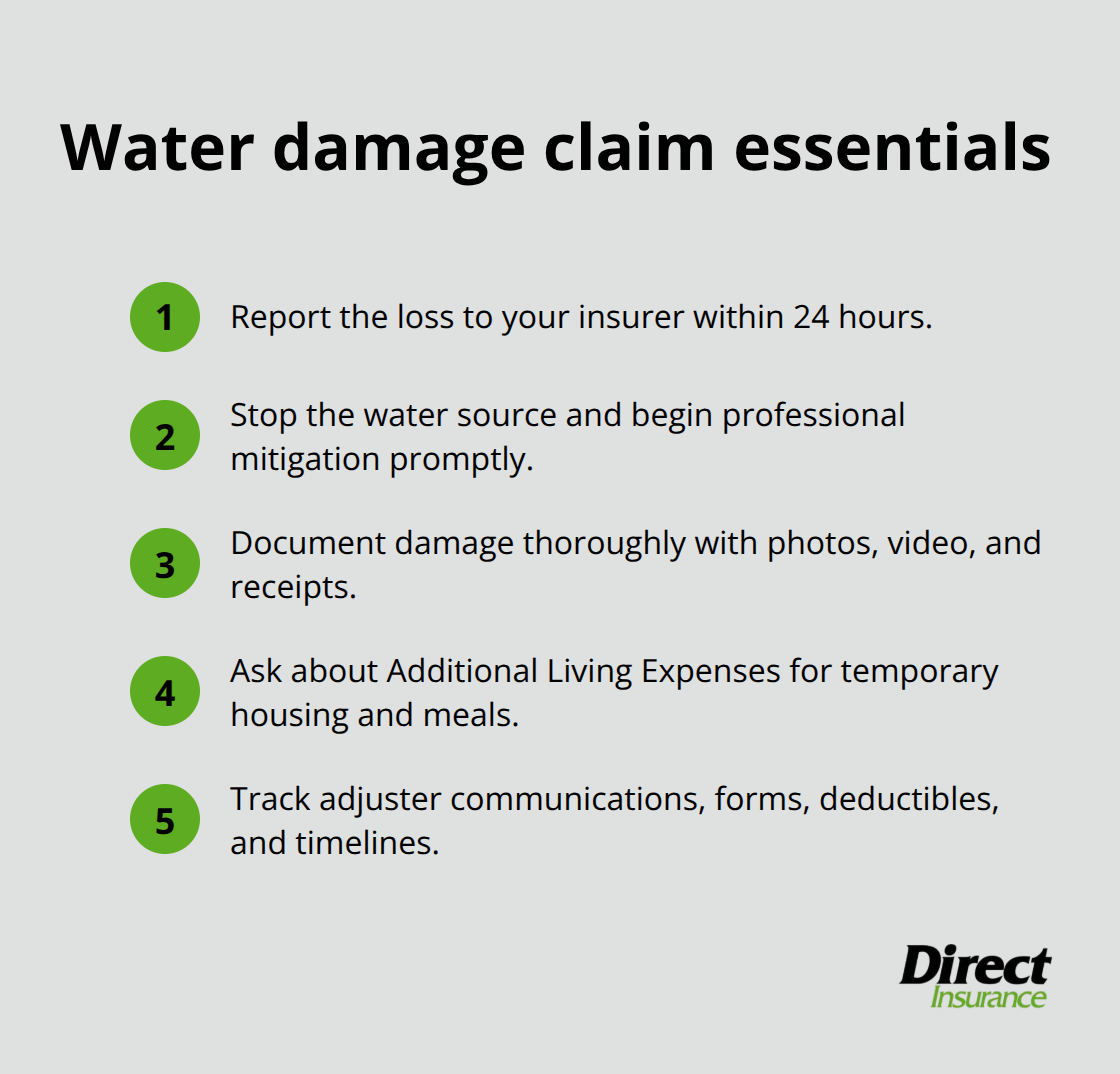

Contact your insurance agent or claims department within 24 hours of discovering water damage-most policies require timely notification to maintain coverage eligibility, and waiting weeks gives insurers grounds to reject your claim outright. When you call, have your policy number ready and provide a clear description of what happened, the date you discovered the loss, and which areas of your home were affected. Your insurer will assign an adjuster who inspects the property and assesses repair costs, so prepare to discuss your deductible, the expected claims timeline, and any required forms.

Stop the Damage Immediately

Take immediate action to stop the water source if safe to do so-shut off a burst pipe, turn off your water main, or move belongings away from standing water to prevent further damage. Then hire licensed, insured professionals to remove water and moisture promptly, as mold develops within 24-48 hours and structural issues worsen quickly. Industrial dehumidifiers and air movers accelerate drying and reduce secondary damage, so professional water damage cleanup becomes essential when significant water is involved.

Document Everything Before Cleanup Starts

Photograph and video document every aspect of the damage before cleanup begins-capture wet walls, damaged flooring, saturated belongings, and the water source itself from multiple angles. These images provide visual proof that supports your claim and helps the adjuster assess repair costs accurately. Keep every receipt and contractor invoice related to water removal, drying, and repairs, as insurers require documentation of proper remediation for reimbursement. Write down dates, times, and names of anyone you speak with at your insurance company, along with what was discussed and any promises made about coverage or timeline.

Understand Your Additional Coverage Options

If your home becomes uninhabitable due to water damage, your policy may cover Additional Living Expenses for hotel, meals, and other necessary costs while repairs proceed-ask your adjuster specifically about this coverage. Many homeowners overlook this benefit and pay out-of-pocket for temporary housing when their policy would have covered these costs. Review your policy language to understand what qualifies as an insurable expense under this provision.

Know When to Seek Professional Help

For complex claims, denials, or situations where the payout seems inadequate, consider contacting a public adjuster or attorney and maintain detailed records of all interactions and fees. These professionals help navigate disputes when insurers underpay or deny valid claims, potentially recovering thousands more than you’d receive alone. Understanding your claim options positions you to move forward with confidence-but preventing water damage in the first place remains far more cost-effective than managing claims after the fact.

How to Stop Water Damage Before It Starts

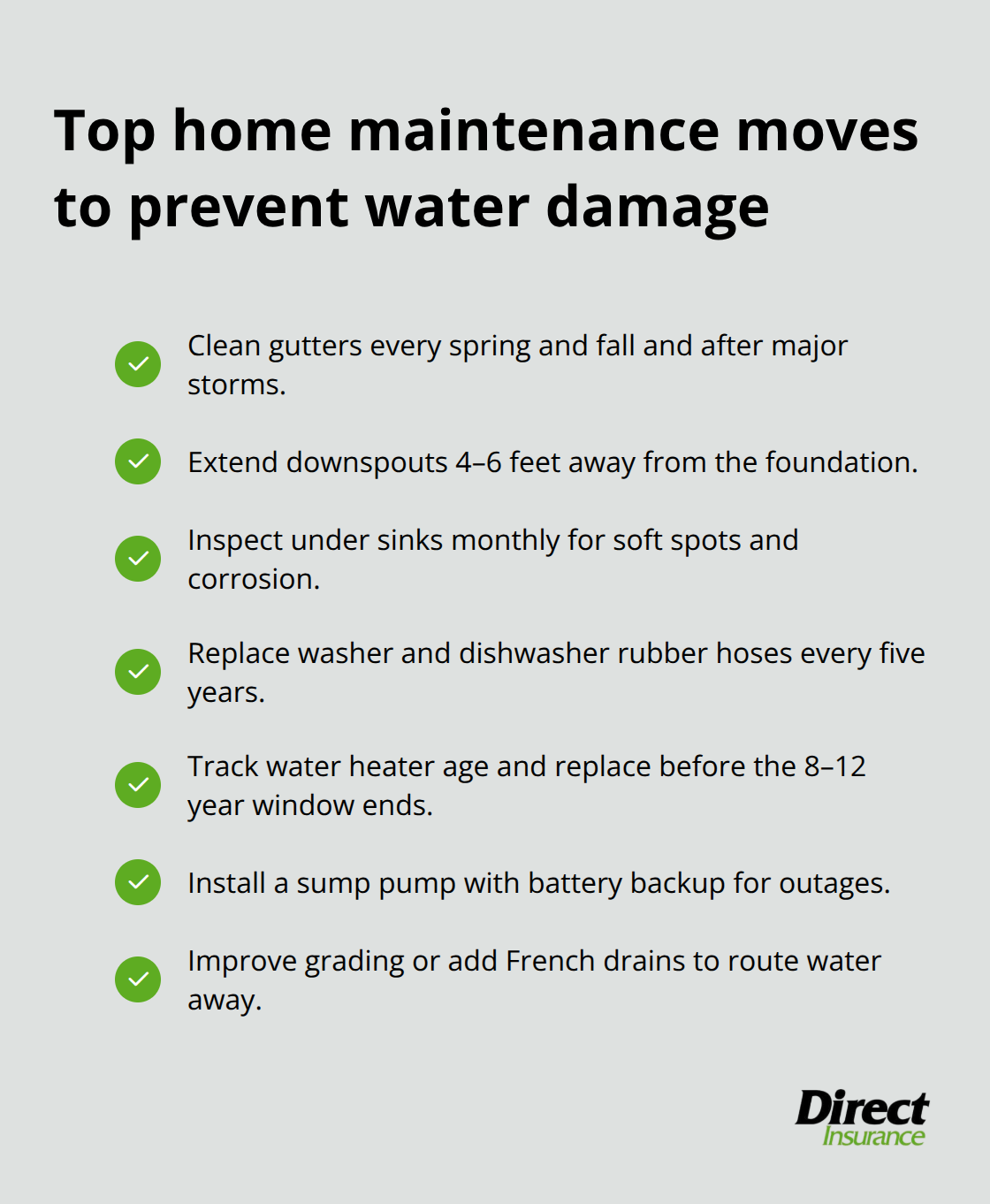

The best water damage claim is the one you never file. We’ve worked with homeowners who’ve experienced devastating water losses, and nearly every conversation includes the same regret: they wish they’d invested a few hours in maintenance beforehand. Water damage prevention costs almost nothing compared to the average claim payout of around $13,954 according to the Insurance Information Institute. Your gutters clogged with leaves and debris funnel water directly into your foundation instead of away from your home, making gutter cleaning the single most effective prevention task you can perform.

Clean Your Gutters Twice Yearly

Clean your gutters at least twice yearly-spring and fall-and after heavy storms, since standing water in gutters creates ice dams in winter that force water under your roof and into your attic. Downspouts must extend at least four to six feet away from your foundation; if yours dumps water right next to your home, water seeps into your basement and foundation walls, causing the expensive groundwater seepage that standard policies exclude from coverage. This simple maintenance task prevents thousands in potential repairs and protects your foundation from chronic water exposure.

Inspect Plumbing and Appliances Monthly

Plumbing and appliances fail silently until catastrophic damage forces you to act. Inspect under sinks monthly for soft spots, discoloration, or corrosion on pipes, since corroded pipes burst without warning and flood entire rooms within minutes. Washing machines and dishwashers develop leaks around supply line connections that worsen over time; replace rubber hoses every five years regardless of condition, as they degrade from heat and pressure and cost roughly $15 to $30 per hose compared to thousands in water damage repair. Water heaters typically last 8 to 12 years before rupturing, so know your unit’s age and plan replacement before failure strikes.

Address Basement Water Intrusion Immediately

Check your basement or crawlspace for standing water, dampness, or efflorescence (white mineral deposits on concrete), which signals groundwater intrusion that requires immediate waterproofing action. Professional sump pumps with battery backup protect basements during power outages when pump failure would be most catastrophic, though sump pumps are not substitutes for flood insurance in flood-prone areas. French drains and proper grading direct water away from your foundation, and these investments typically cost between $500 and $2,000 depending on your property size and soil conditions-far less than repairing structural damage from chronic water exposure.

Final Thoughts

Your homeowners policy covers water damage from sudden, accidental events like burst pipes and storm-related roof leaks, but gradual deterioration and flood damage receive no protection under standard policies. The gap between what you think is covered and what actually is covered creates financial risk that costs thousands to repair after the fact. Prevention eliminates this risk entirely by stopping damage before it starts.

Cleaning gutters twice yearly, inspecting plumbing monthly, and maintaining proper drainage systems cost almost nothing compared to the average water damage claim of $13,954. These simple tasks protect your home’s structural integrity for decades and reduce the likelihood that you’ll ever need to file a claim. Your insurance exists to handle unexpected catastrophes, not to cover maintenance failures you could have prevented.

We at Direct Insurance Services recommend reviewing your current homeowners policy with a licensed agent who understands your specific situation and can identify whether water damage covered by home insurance matches your actual risk. Ask whether you need additional endorsements for sewer backup or mold remediation, and determine whether flood insurance makes sense for your location (most policies require a 30-day waiting period before protection takes effect). Contact Direct Insurance Services to discuss your homeowners policy, identify coverage gaps, and build protection that matches your needs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation