How to Get Cheap Auto Insurance That Actually Works

Most people overpay for auto insurance without realizing it. At Direct Insurance Services, we’ve helped thousands of drivers find coverage that costs less while protecting what matters.

The question we hear most often is: how can I get cheap auto insurance without cutting corners on protection? This guide walks you through the exact strategies that work, from policy bundling to finding discounts you’ve likely missed.

What Really Drives Your Auto Insurance Cost

Insurance companies don’t pull rates out of thin air. They use detailed risk models based on thousands of data points, and understanding how these models work reveals why your premiums might be significantly higher than your neighbor’s.

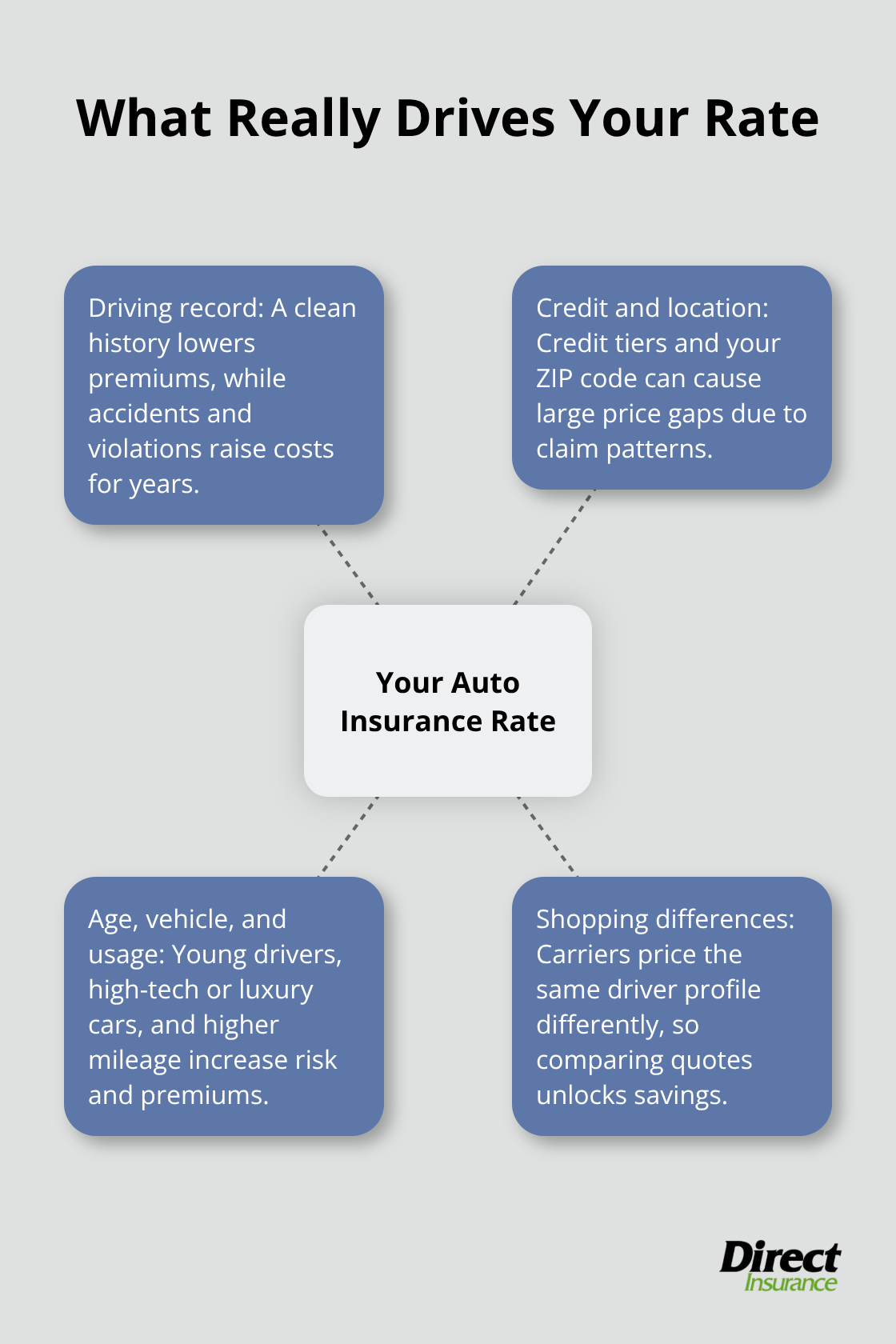

Your Driving Record Sets the Baseline

Your driving record is the single most influential factor-a clean history can save you hundreds annually, while even one at-fault accident can push your rates up 20% to 40% depending on the insurer. One accident or violation doesn’t doom you to high rates forever, but it does matter immediately. An at-fault collision typically increases your premium for 3 to 5 years, while a speeding ticket or minor violation might add 10% to 15% to your annual cost.

Some insurers offer accident forgiveness programs-you’ll want to ask about this when shopping quotes. Defensive driving courses can offset some of these increases. In 34 states plus Washington DC, completing an approved defensive driving course qualifies you for a discount of up to 15%, and the courses themselves cost around $25. New York specifically offers about a 10% discount through state-approved programs, and you can repeat these courses every few years. Your past driving behavior directly predicts your future risk in the eyes of insurers, so maintaining a clean record is far cheaper than trying to recover from accidents or violations.

Credit Score and Location Create Hidden Cost Gaps

Credit score matters more than most drivers realize. According to the Consumer Federation of America, drivers with excellent credit (800+) pay about 49% less than those with fair credit (580–669), and poor credit (below 580) can cost 115% more. Two drivers with identical vehicles and driving records can pay vastly different premiums based solely on where they live and their credit profile.

Florida, Louisiana, and Nevada all exceed $3,500 in average annual premiums, while New York tops $4,000. These regional differences reflect higher claim frequencies, repair costs, and theft rates. Your credit score carries equal weight in most states because insurers have found a strong correlation between financial responsibility and claim likelihood. Three states-California, Hawaii, and Massachusetts-ban credit-based pricing, so residents there avoid this penalty entirely.

Age, Vehicle Type, and Usage Patterns

Your age, location, and the specific vehicle you drive heavily influence what you pay. Young drivers aged 16–19 face premiums roughly 3 times higher than adults, while moving from a suburban area to an urban location can increase rates by 8% or more due to higher accident and theft frequencies. Insurance companies also scrutinize how you use your vehicle-annual mileage, commute distance, and whether you park in a garage versus on the street all factor into your quote. A driver who logs 5,000 miles yearly might save $116 or more compared to someone driving 15,000 miles annually.

The type of vehicle matters too. Repair costs for luxury vehicles, newer models with advanced technology, and certain foreign-made cars can be 30% to 50% higher than mainstream sedans, which translates directly into higher premiums. Vehicles with active safety features (automatic emergency braking, blind-spot monitoring) and strong crash-test ratings often qualify for lower premiums.

Shopping Across Multiple Carriers Reveals Real Savings

When you shop for quotes, always compare rates across multiple carriers because the same driver profile can produce hundreds of dollars in variation between insurers due to their different risk models and pricing philosophies. This variation means that finding affordable coverage requires you to test your profile against several companies rather than accepting the first quote you receive.

Strategies That Actually Lower Your Premium

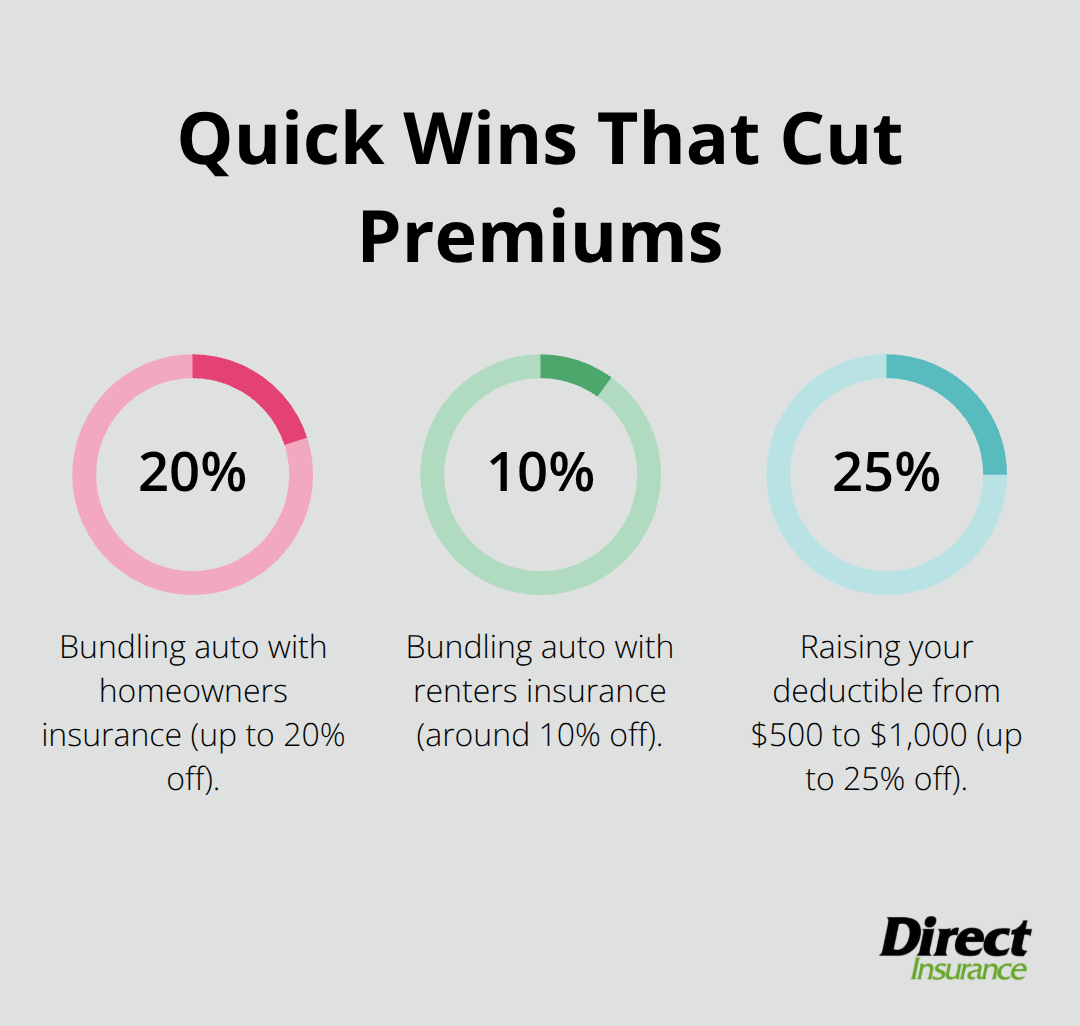

The gap between what you’re paying now and what you could pay is often wider than you think. Three specific moves cut premiums significantly: bundling policies, raising deductibles strategically, and hunting for overlooked discounts.

Bundle Your Policies for Immediate Savings

Bundling auto with homeowners insurance cuts your annual premium by up to 20%, though results vary by insurer and situation. If you bundle with renters coverage instead, expect savings around 10%. Insurers reward loyalty across multiple policies because it reduces their administrative costs and customer acquisition expense. When you shop quotes, always ask carriers what bundling discounts apply to your specific situation before comparing final prices.

Raise Your Deductible Strategically

Raising your deductible from $500 to $1,000 typically cuts premiums by 20% to 25%, which translates to roughly $464 to $525 annually depending on your vehicle and location. This works only if you can actually cover that higher deductible without financial strain when a claim happens. Some drivers raise their deductible to $1,500 or $2,000 and save even more, but that strategy backfires if an accident forces you into debt. The real savings come when you pair deductible increases with policy bundling-one driver might save $800 annually through bundling alone, then add another $500 by raising the deductible.

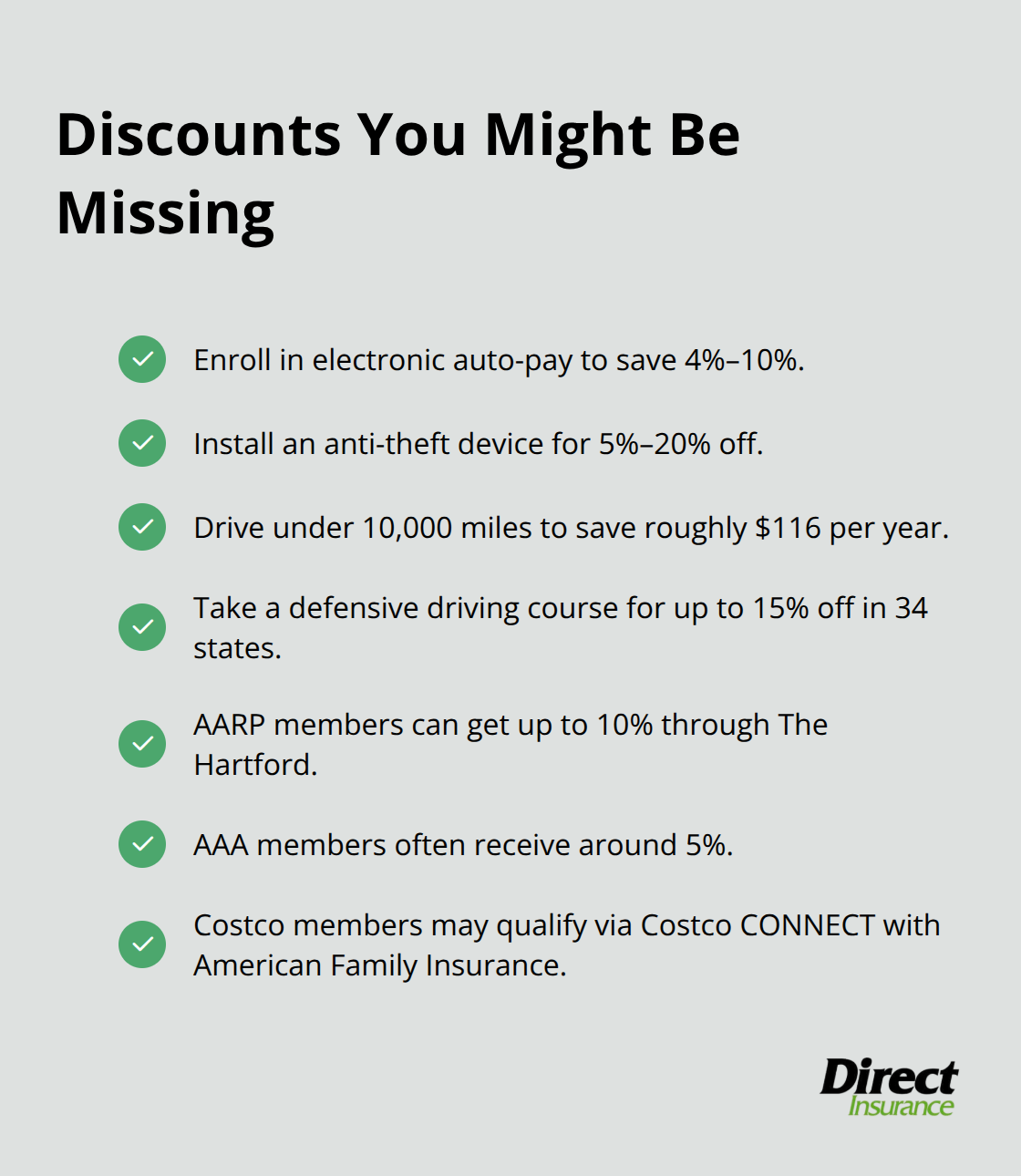

Capture Discounts You’re Probably Missing

Electronic auto-pay typically saves 4% to 10%, while anti-theft device discounts range from 5% to 20% depending on your device and location. Drivers who log under 10,000 miles annually qualify for low-mileage discounts worth roughly $116 per year. Completing a defensive driving course qualifies you for up to 15% off in 34 states, and these courses cost around $25-you can repeat them every few years to maintain the discount.

Membership discounts add up quickly. AARP members get up to 10% through The Hartford, AAA members receive around 5%, and Costco members can access discounts through Costco CONNECT with American Family Insurance. Most drivers miss at least two of these discounts simply because they never ask about them during the quote process.

Shop Multiple Carriers and Time Your Switch

Identical drivers see premium differences of $200 to $500+ between carriers because each insurer weights risk factors differently-one company might penalize your location heavily while another focuses more on your driving history. Consumer Reports found that drivers who switched insurers in the past five years saved a median $461 annually, meaning you’re potentially leaving hundreds on the table if you renew with your current company without testing other quotes.

Get quotes from major carriers like Progressive, State Farm, Geico, Liberty Mutual, and USAA, then use comparison tools like CarInsurance.com, Insurify, or The Zebra to speed up the process. When comparing quotes, ensure you’re using the same coverage limits across all quotes so the numbers actually mean something. A quote that looks $200 cheaper might include lower liability limits, which leaves you exposed if you cause a serious accident.

Pay annually rather than monthly if possible-you’ll avoid monthly payment fees and often receive a small discount for paying in full. This single move can save $50 to $150 depending on your insurer. Shop for new quotes 30 to 60 days before your renewal date so you have time to switch if you find something better. Waiting until your renewal date passes means you’ll either stick with a higher rate or face a gap in coverage if you switch late.

The strategies above work best when combined, but they only matter if you actually apply them to your specific situation. The next section walks you through assessing your actual coverage needs so you don’t waste savings on protection you don’t need.

How to Find Coverage That Fits Your Budget Without Sacrificing Protection

The difference between cheap insurance and affordable insurance is coverage. Cheap insurance leaves you exposed to catastrophic financial loss after an accident, while affordable insurance protects your assets without draining your monthly budget. Most drivers either over-insure minor risks or under-insure major ones, and fixing this imbalance is where real savings happen.

Assess Your Coverage Needs Based on What You Own

Start by understanding what you actually need to protect. If you own your car outright with no loan, you can drop collision and comprehensive coverage entirely-this single move saves roughly $1,165 annually depending on your vehicle’s value. But if you still owe money on a loan, your lender requires full coverage, meaning collision and comprehensive are non-negotiable. The math is straightforward: if your car’s worth $5,000 and collision costs $800 annually, you’re throwing money away because you’ll never recover more than $5,000 even after a total loss.

Your deductible choice ties directly to your emergency fund-if you can’t cover a $1,000 deductible without borrowing money, you’re not actually saving anything by raising it because you’ll end up paying interest on a loan. Set your deductible at the highest amount you can genuinely afford to pay out of pocket within 24 hours if an accident happens.

Prioritize Liability Coverage to Protect Your Assets

Liability coverage protects you financially if you’re responsible for someone else’s injuries or property damage. Minimum state requirements exist in every state, but they’re dangerously low-most states allow 15/30/5 liability limits, which means $15,000 per person and $30,000 total for injuries you cause, plus $5,000 for property damage. A single serious injury can easily exceed $100,000 in medical bills and lost wages.

Try 100/300/100 liability limits as your floor, and add an umbrella policy for around $250 to $300 annually to gain an extra $1 million in protection. This combination costs far less than the financial devastation of a lawsuit that exhausts your home equity and future wages.

Adjust Coverage When Your Life Changes

Review your actual driving patterns before accepting any quote. If you transitioned to remote work and now drive 5,000 miles annually instead of 15,000, you qualify for low-mileage discounts that some insurers verify through odometer readings or telematics. Conversely, if your commute changed and you’re now driving 20,000 miles yearly, your risk profile shifted upward and your old discount disappeared-this is why rates creep up even when nothing else changes.

Life events matter equally: adding a 16-year-old driver to your policy increases premiums by $1,000 to $2,000 annually or more, while removing an adult child who moved out cuts costs significantly. Getting married typically lowers rates, while divorce can raise them. A move from suburban to urban areas increases premiums roughly 8% due to higher accident and theft frequencies, while relocating to lower-risk areas with better weather patterns works in your favor.

Review Your Policy Annually and Make Adjustments

Revisit your policy every 12 months and adjust coverage limits based on what’s actually changed in your life, not what your insurer suggests during renewal. Many drivers keep coverage they no longer need simply because they never questioned it. When you review your policy, compare your current coverage against your actual situation-your job, your vehicle’s value, your driving habits, and your financial capacity to handle a claim. This annual check prevents you from overpaying for protection you’ve outgrown while ensuring you maintain adequate limits for genuine risks.

Final Thoughts

Getting cheap auto insurance that actually works requires three concrete actions: understand what drives your rates, apply savings strategies that compound, and maintain coverage that protects your assets without overpaying. Bundling policies saves 10% to 20% immediately, raising your deductible cuts premiums by 20% to 25%, and shopping multiple carriers reveals savings of $200 to $500+ annually-these moves stack when combined, and drivers who apply all of them typically save $800 to $1,500 per year. Your driving record, credit score, location, and vehicle type set your baseline rate, but you control whether you bundle policies, raise deductibles, capture overlooked discounts, and switch carriers at renewal.

Start by gathering quotes from at least three major carriers 30 to 60 days before your renewal date, using the same coverage limits across all quotes so the numbers mean something. Ask each carrier about bundling discounts, low-mileage programs, defensive driving credits, and membership discounts that apply to your situation. Compare the final numbers, then assess whether your current coverage still fits your life or if adjustments make sense.

If you’re in Utah, Direct Insurance Services works with top-rated carriers to help you find coverage that fits both your needs and budget. Our independent agency approach means we match you with the carrier offering the best combination of price and protection for your specific situation. Contact us for a personalized quote and see how much you could save by applying these strategies with professional support.