Auto Liability Insurance Utah: What It Covers And Why It Matters

Auto liability insurance in Utah isn’t optional-it’s the law. Every driver on Utah roads must carry minimum coverage, yet many don’t understand what they’re actually protected against or why the limits matter.

At Direct Insurance Services, we’ve seen firsthand how confusion about liability coverage leads drivers to either under-insure or overpay. This guide breaks down exactly what your policy covers, what Utah requires, and the real consequences of getting it wrong.

What Your Liability Coverage Actually Pays For

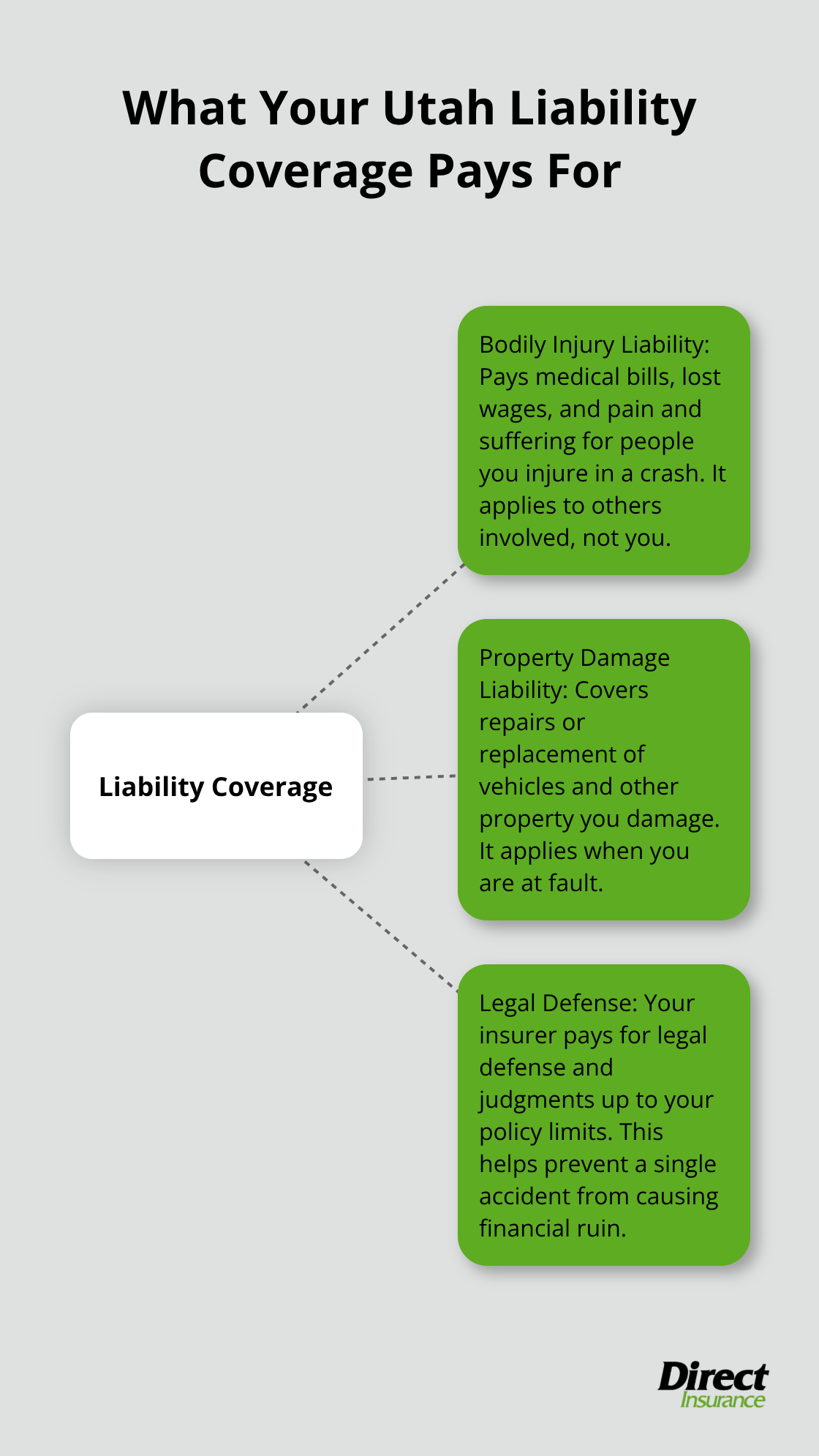

Auto liability insurance in Utah covers two critical areas when you cause an accident: injuries to other people and damage to their property. Bodily injury liability covers medical expenses, lost wages, and pain and suffering for anyone you injure in a crash. Property damage liability covers repairs or replacement of vehicles and other property you damage. These aren’t optional add-ons-they’re mandatory under Utah law.

As of January 1, 2025, Utah’s minimum requirements increased to 30/65/25, meaning $30,000 per person and $65,000 per accident for bodily injury, plus $25,000 for property damage. Utah House Bill 113 enacted this change because medical costs and vehicle repair expenses have climbed substantially over the past decade. The Utah Department of Insurance updated these thresholds to reflect the real financial impact of accidents on injured parties and property owners.

Why the New Minimums Address Real Coverage Gaps

The jump from the old 25/65/15 limits to 30/65/25 addresses genuine gaps in protection. A single serious injury requiring surgery and rehabilitation can easily exceed $50,000 in medical costs. When you’re found liable for an accident involving multiple people or significant injuries, your bodily injury limit gets divided among all injured parties. One person with $75,000 in damages exhausts most of a $65,000 per-accident limit, leaving other injured parties with inadequate compensation and potentially exposing you to a lawsuit for the difference.

Property damage limits matter equally-a newer vehicle damaged in a collision can cost $20,000 to $30,000 to repair, and luxury vehicles cost far more. Utah’s minimum limits provide baseline protection, but they’re genuinely bare-bones coverage. Many drivers with financed vehicles discover their liability limits don’t cover the damage they cause, forcing them to pay out of pocket for judgments against them.

Evaluating Whether Minimums Fit Your Situation

Your current coverage situation depends on your assets and driving patterns. If you own a home, significant savings, or drive regularly for work, minimum liability coverage exposes you to serious financial risk. A judgment against you for $150,000 can result in wage garnishment and asset seizure. Higher limits-typically $100,000 per person and $300,000 per accident-cost only slightly more than minimums, often an additional $15 to $30 per month. This marginal increase in premium provides substantially better protection.

Drivers with commercial vehicle use face even greater exposure. If you use your vehicle for deliveries or ride-sharing, standard personal policy limits may not apply, and you need commercial coverage to avoid claim denial. When your policy renews after January 1, 2025, you’ll automatically receive the new 30/65/25 minimums. That renewal presents an opportunity to evaluate whether higher limits make sense for your situation and to discuss your options with an insurance professional who understands Utah’s specific requirements.

Why Liability Coverage Protects Your Financial Future

The Real Cost of Driving Uninsured in Utah

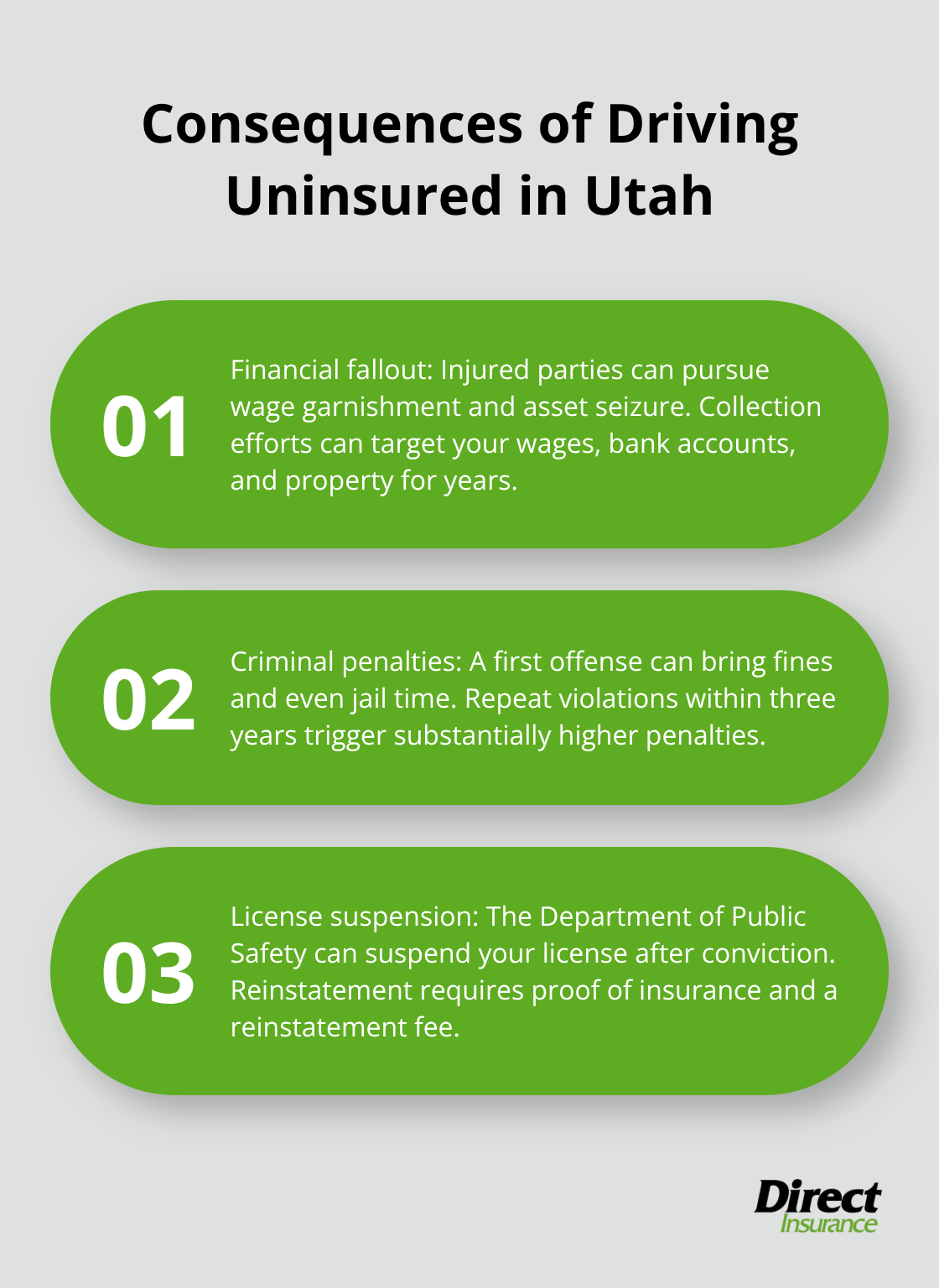

Driving without liability insurance in Utah isn’t a minor oversight-it’s a criminal offense with consequences that extend far beyond a traffic ticket. The state treats uninsured driving seriously because accidents create real financial damage. A single collision can generate medical bills exceeding $100,000, property damage claims of $50,000 or more, and ongoing care costs for injured parties. When you cause that accident without liability coverage, those costs fall directly on you.

Utah law allows injured parties to pursue wage garnishment and asset seizure against uninsured drivers, meaning your wages, bank accounts, and property become vulnerable to collection efforts that can last years. A first offense carries penalties including potential jail time and fines, with substantially higher penalties for repeat violations within three years. The Utah Department of Public Safety can suspend your driver’s license after conviction for driving without insurance, and reinstating it requires proof of coverage plus a reinstatement fee.

How Liability Coverage Shields Your Assets

Liability coverage transforms this equation entirely. When you carry insurance at Utah’s minimum requirements or higher, your insurance company handles defense costs and pays judgments up to your policy limits. This protection prevents personal bankruptcy from a single accident.

Consider a realistic scenario: you cause a multi-vehicle collision where one driver requires spinal surgery costing $120,000 and loses six months of income. With adequate coverage limits, your insurer covers the full amount and you face no additional judgment. Without sufficient coverage, you’re personally liable for the gap between your policy limits and the injured driver’s actual damages.

Why Your Assets Matter More Than You Think

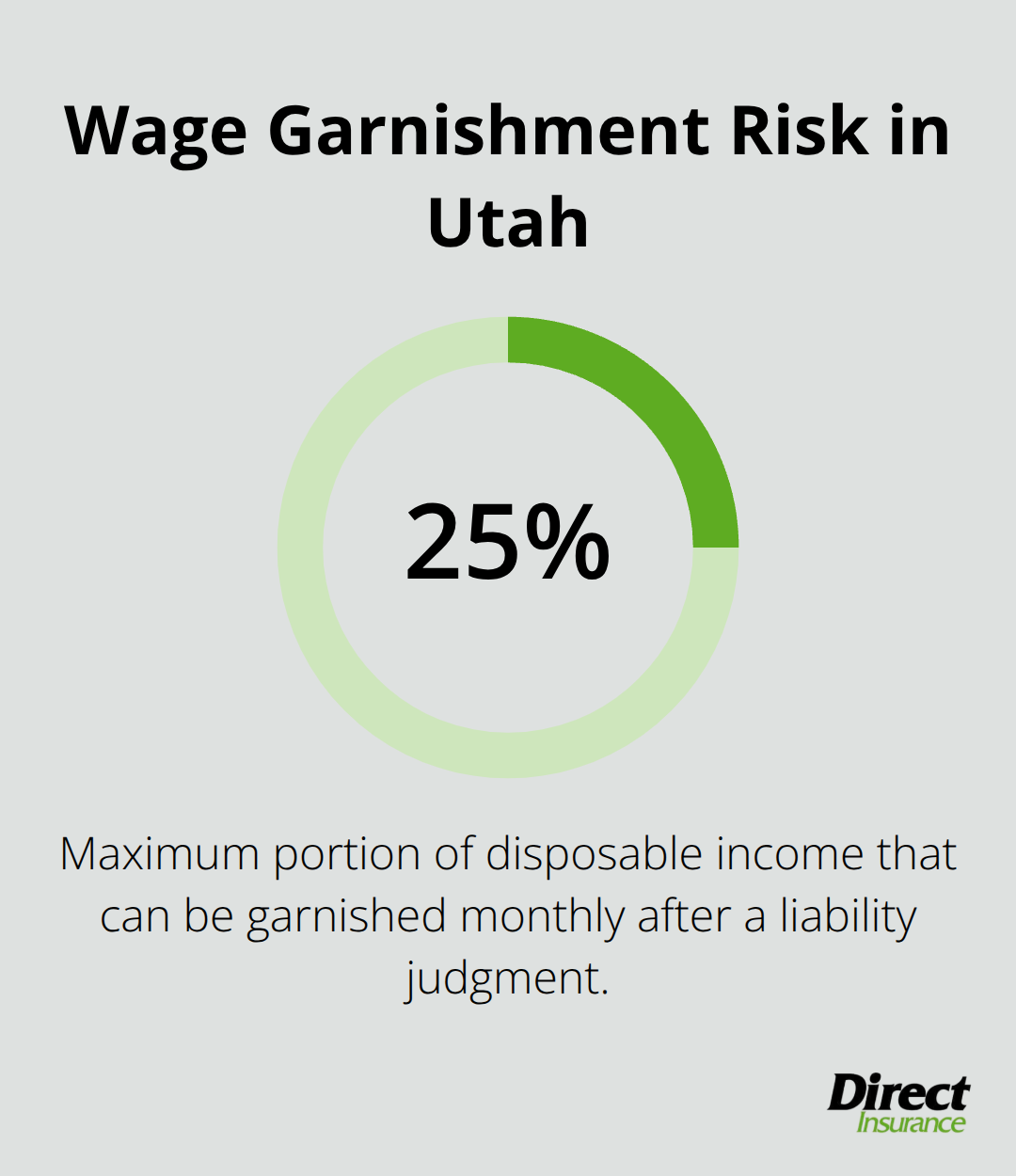

Drivers with assets-a home, retirement accounts, or steady income-face the greatest exposure to uninsured liability claims. A lawsuit judgment can result in monthly wage garnishment of up to 25 percent of your disposable income indefinitely. The financial protection liability coverage provides isn’t theoretical; it’s the difference between a manageable insurance claim and financial devastation.

Higher limits typically cost only a modest amount more per month than minimum coverage. This premium increase provides substantially better protection for your financial future. When your policy renews, you’ll receive updated minimum requirements-but that renewal also presents an opportunity to evaluate whether higher limits make sense for your situation.

Assessing Your Coverage Needs

Your appropriate coverage level depends on your assets and driving patterns. If you own a home, significant savings, or drive regularly for work, minimum liability coverage exposes you to serious financial risk. A judgment against you can result in wage garnishment and asset seizure that extends for years. Drivers with commercial vehicle use face even greater exposure; if you use your vehicle for deliveries or ride-sharing, standard personal policy limits may not apply, and you need commercial coverage to avoid claim denial.

An insurance professional can help you assess your assets and driving patterns to determine appropriate coverage levels for your circumstances. This evaluation becomes especially important as your policy renews and updated requirements take effect.

What Liability Coverage Actually Protects

Most drivers misunderstand what auto liability insurance actually covers, and this confusion creates dangerous coverage gaps. Liability insurance protects the other driver and their passengers when you cause an accident-not you. Your bodily injury liability pays for medical bills, lost wages, and pain and suffering for people you injure. Your property damage liability covers repairs to their vehicle or other property you damage. This distinction matters enormously because it means your own medical bills, vehicle repairs, and lost wages fall under different coverage types entirely. If you’re injured in an accident you cause, your own medical costs come from your Personal Injury Protection coverage, which is required in Utah and provides $3,000 minimum per person according to the Utah Department of Insurance. Many drivers carry liability limits thinking they’re protected if they cause an accident involving serious injuries-then discover their coverage pays the other party, not them.

One Policy Does Not Fit Every Driver

A major misconception is that one policy structure fits every driver equally. A 25-year-old renting an apartment with minimal assets faces fundamentally different liability exposure than a 45-year-old homeowner earning $150,000 annually. The homeowner’s wages and property become vulnerable to garnishment and seizure if a judgment exceeds policy limits, making higher coverage essential. A rideshare driver using their vehicle for commercial purposes cannot rely on personal auto insurance at all-their standard policy explicitly excludes commercial use, and claims get denied when commercial activity surfaces. Delivery drivers face identical exclusions. A parent with teenage drivers in the household needs higher limits because drivers under 20 have the highest crash rates; one serious accident involving a teen driver can generate $200,000 in liability exposure, far exceeding minimum coverage. Your driving patterns matter equally-someone commuting 50 miles daily on highways faces greater accident probability than someone driving 5 miles weekly.

Utah’s Updated Minimums Still Leave Gaps

Utah’s minimum 30/65/25 limits work for some drivers and expose others to catastrophic financial risk. The January 1, 2025 increase to these minimums reflects updated accident costs, but minimums remain inadequate for most drivers with assets, commercial use, or household members with elevated risk profiles. A single serious accident involving two injured people can quickly exhaust per-accident limits while leaving you personally liable for the difference. That personal liability translates directly into wage garnishment and asset seizure that extends for years.

Higher Limits Cost Far Less Than Most Drivers Think

The third misconception drives poor coverage decisions: the belief that higher liability limits cost substantially more. In reality, the premium difference between 30/65/25 minimums and 100/300/100 coverage typically ranges from $15 to $40 monthly depending on your driving record and age. This marginal increase provides dramatically better protection. If you cause an accident involving two injured people with $80,000 in combined damages, your $65,000 per-accident limit leaves you personally liable for $15,000. That $15,000 judgment can result in monthly wage garnishment of up to 25 percent of your disposable income indefinitely, according to Utah law. The extra $20 monthly for higher limits completely eliminates this exposure.

Assess Your Coverage During Policy Renewal

Drivers with clean records often qualify for higher limits at surprisingly low costs because insurers view them as lower risk. A homeowner with a mortgage cannot afford to carry minimum liability coverage-a single serious accident can trigger foreclosure through wage garnishment. Yet many homeowners never evaluate their coverage levels during policy renewals, defaulting to whatever minimum the insurer assigns. When your policy renews after January 1, 2025, you’ll automatically receive updated minimums, but that renewal presents the critical moment to discuss whether higher limits make financial sense for your specific situation. An insurance professional can help you assess your assets and driving patterns to determine appropriate coverage levels for your circumstances.

Final Thoughts

Auto liability insurance in Utah protects your financial future when you cause an accident. The state’s updated minimum requirements of 30/65/25 reflect the genuine costs of modern accidents, but these minimums remain bare-bones coverage for most drivers. A single serious collision can generate liability claims far exceeding minimum limits, exposing you to wage garnishment and asset seizure that extends for years.

Review your current coverage during your next policy renewal and compare your existing limits against Utah’s new 30/65/25 minimums. If you own a home, drive regularly for work, or have significant savings, minimum coverage leaves you financially vulnerable. Higher limits typically cost only $15 to $40 monthly more than minimums, yet provide substantially better protection against catastrophic liability claims.

We at Direct Insurance Services work with top-rated carriers to help you find auto liability insurance in Utah that fits both your needs and budget. Contact us to discuss your coverage options and ensure you carry limits that match your assets and driving patterns.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation