Utah Condo Insurance Essentials: Protect Your Investment

Condo ownership in Utah comes with unique insurance challenges that many owners overlook. Your building’s master policy doesn’t cover your personal belongings, interior upgrades, or liability inside your unit-leaving significant gaps in your protection.

At Direct Insurance Services, we’ve seen too many condo owners discover these gaps the hard way. This guide walks you through the Utah condo insurance coverage you actually need.

What Makes Condo Insurance Different

Condo insurance and homeowners insurance look similar on the surface, but they protect fundamentally different things. A homeowners policy covers the entire structure of your house, from the roof to the foundation. A condo policy, known as HO-6 in Utah, covers only what’s inside your individual unit and your personal liability. This distinction matters because your condo building’s master policy handles the common areas and exterior structure, which means you fill the gaps that master policies intentionally leave uncovered.

The master policy typically insures hallways, lobbies, roofs, foundations, and shared amenities like pools or fitness centers. What it does not cover are the walls, fixtures, flooring, appliances, and personal belongings inside your unit. According to the Utah Insurance Department, many condo owners mistakenly assume their building’s master policy protects their personal space, then face devastating losses when claims are denied. This misunderstanding is one of the costliest mistakes you can make.

How Master Policies Work Against Your Protection

Your HOA master policy comes in three types: all-in coverage, bare-walls coverage, and single-entity coverage. All-in policies cover the building structure plus fixtures and improvements originally installed by the developer, which means you need less dwelling coverage on your HO-6 policy because less of your unit falls to you. Bare-walls policies cover only the structural shell and common areas, leaving you responsible for everything inside your unit including walls, wiring, plumbing, fixtures, and flooring. Single-entity policies cover common areas and HOA-owned property but may include some fixtures in your unit from original construction.

Contact your HOA and request a copy of your master policy to determine which type covers your building. Once you know this, you can calculate the correct dwelling coverage amount for your HO-6 policy. With an all-in master policy, you might need only $25,000 in dwelling coverage; with bare-walls coverage, you could need $50,000 or more depending on your unit’s size and upgrades. This single step prevents the underinsurance problem that leaves owners paying out-of-pocket for water damage, fire damage, or theft.

Why Your Personal Coverage Matters More Than You Think

An HO-6 policy coverage in Utah protects your personal property, interior elements, and liability. That coverage buys you three essential protections that your master policy completely ignores: personal property coverage for your belongings, liability protection if someone is injured in your unit, and loss of use coverage if your condo becomes uninhabitable. Personal property coverage reimburses you for stolen or damaged items like furniture, electronics, clothing, and kitchen appliances up to your chosen limit. Liability coverage protects you financially if a guest slips on your floor and sues you, or if your negligence causes property damage to another unit. Loss of use coverage pays for temporary housing, meals, and other living expenses if a fire or other covered event forces you to vacate.

Without these three components, a single incident could cost you tens of thousands of dollars from your own pocket. Create a detailed home inventory of your belongings and assign realistic replacement values, then match your personal property limit to that total. If your inventory totals $65,000, a $50,000 personal property limit leaves you short by $15,000-a gap that could force you to absorb significant losses yourself.

The Coverage Gap That Catches Most Owners Off Guard

Most condo owners discover their protection gaps only after a loss occurs. Your master policy covers the building’s structure and common areas, but it stops at your unit’s walls. Everything from interior paint to custom fixtures to your personal items falls entirely on you. This separation of responsibility (master policy for structure, HO-6 for contents and liability) creates confusion because owners naturally assume one policy covers everything.

The Utah Insurance Department receives complaints regularly from condo owners who thought their master policy protected their personal space. These owners then face denials when they file claims for water damage, theft, or liability incidents. Understanding this split responsibility now prevents costly surprises later. Your next step involves reviewing what coverage gaps exist in your current situation and how much protection you actually need.

What Coverage Actually Protects Your Utah Condo

Your dwelling coverage forms the foundation of your HO-6 policy, and it’s where most Utah condo owners make critical mistakes. Dwelling coverage reimburses you for damage to interior walls, flooring, built-in appliances, plumbing, electrical wiring, and fixtures you’ve installed or upgraded. A burst pipe destroys your drywall, cabinets, and flooring-dwelling coverage pays to repair or replace those items. You renovate your kitchen with custom cabinetry and granite countertops-that coverage extends to those improvements. The critical detail most owners miss: your master policy type determines how much dwelling coverage you actually need.

Contact your HOA today and request a copy of your master policy declaration page. If your building has all-in coverage, the association’s policy covers most structural elements, so you might need only $20,000 to $35,000 in dwelling coverage. If your building has bare-walls coverage, you’re responsible for everything inside your unit, which means you likely need $50,000 to $75,000 or more depending on your unit’s square footage and finishes. This single piece of information prevents the underinsurance trap that forces owners to pay thousands out-of-pocket after water damage, fire, or theft.

Personal property coverage protects thousands in belongings

Your belongings represent thousands of dollars in replacement value, and your master policy covers none of it. Personal property coverage reimburses you for stolen or damaged furniture, electronics, clothing, kitchen equipment, and other movable items up to your chosen limit. Many Utah condo owners carry only $30,000 in personal property coverage when their actual belongings total $60,000 or more. The Utah Insurance Department data shows that underinsured personal property ranks among the top reasons condo owners face significant out-of-pocket losses.

Create a detailed home inventory right now. Walk through your unit and photograph or list every item of value: your television, laptop, furniture, artwork, jewelry, kitchen appliances, bedding, and clothing. Assign realistic replacement costs to each category based on current retail prices, not what you originally paid. If your inventory totals $70,000, carry at least $70,000 in personal property coverage. Many carriers offer a 10% to 15% discount when you bundle condo insurance with auto or other policies, which makes adequate coverage more affordable than owners realize.

Liability protection shields your personal assets from lawsuit costs

Your liability coverage protects you if a guest is injured in your condo or if you accidentally cause damage to another unit. Someone slips on your kitchen floor and breaks their leg-they can sue you for medical bills, lost wages, and pain and suffering. A single lawsuit easily exceeds $100,000 in damages, and your personal assets face risk if your liability limit is too low. Utah condo owners commonly carry $100,000 in liability coverage, which is the bare minimum and frankly insufficient given how quickly medical and legal costs accumulate.

Most Utah condo owners should carry at least $300,000 in liability coverage, and $500,000 if your unit sits on a ground floor where guest traffic is higher or if you frequently host gatherings. Umbrella insurance provides an additional $1,000,000 or more in liability protection for roughly $150 to $300 per year, which is inexpensive insurance against a catastrophic lawsuit.

Loss assessment coverage protects you from surprise HOA bills

Loss assessment coverage is a specialized endorsement that protects you when your HOA is forced to levy special assessments to cover damage to common areas that exceeds the master policy limits. A major fire damages the building’s roof and the master policy covers only $500,000 of a $750,000 loss-the HOA can assess unit owners for the $250,000 shortfall. Loss assessment coverage typically covers up to $1,000 in such assessments, though you can increase this limit to $5,000 or $10,000 for additional protection. This endorsement costs only $25 to $50 per year and prevents a surprise bill that could run into thousands of dollars.

Understanding these three coverage types sets you up to make informed decisions about your protection level. The next section examines the mistakes that leave Utah condo owners exposed and how to avoid them.

Where Utah Condo Owners Go Wrong with Coverage

Master Policy Myths Cost Owners Thousands

The most expensive mistake Utah condo owners make is assuming their HOA master policy covers damage inside their unit. This assumption costs owners thousands of dollars every year. When a water leak from upstairs soaks your kitchen cabinets, walls, and flooring, your master policy covers nothing because that damage occurred inside your unit’s boundaries. The HOA master policy covers the pipes in the building’s walls and common areas, but once water enters your personal space, you own the damage. Many condo owners face $15,000 to $40,000 in repairs because they carry only $20,000 in dwelling coverage, believing the master policy had them protected. The reality is blunt: that master policy exists to protect the association’s liability and the building structure, not your personal investment inside your walls.

Underestimating Personal Property and Improvements Creates Coverage Gaps

The second critical mistake involves underestimating the value of your personal belongings and interior improvements. Most Utah condo owners list their belongings at $30,000 to $40,000 when a realistic inventory totals $60,000 to $80,000. Electronics alone-your television, laptop, tablet, and gaming system-total $3,000 to $5,000. Add furniture, kitchen equipment, artwork, jewelry, clothing, and bedding, and the number climbs fast. According to the Utah Insurance Department, underinsured personal property ranks among the top reasons condo owners face significant losses after theft or fire. You renovate your kitchen with new cabinets and appliances costing $12,000, or install custom flooring for $8,000, and your HO-6 dwelling coverage limit sits at $25,000. A kitchen fire destroys those upgrades and your personal items, but your coverage falls $5,000 short of the actual loss.

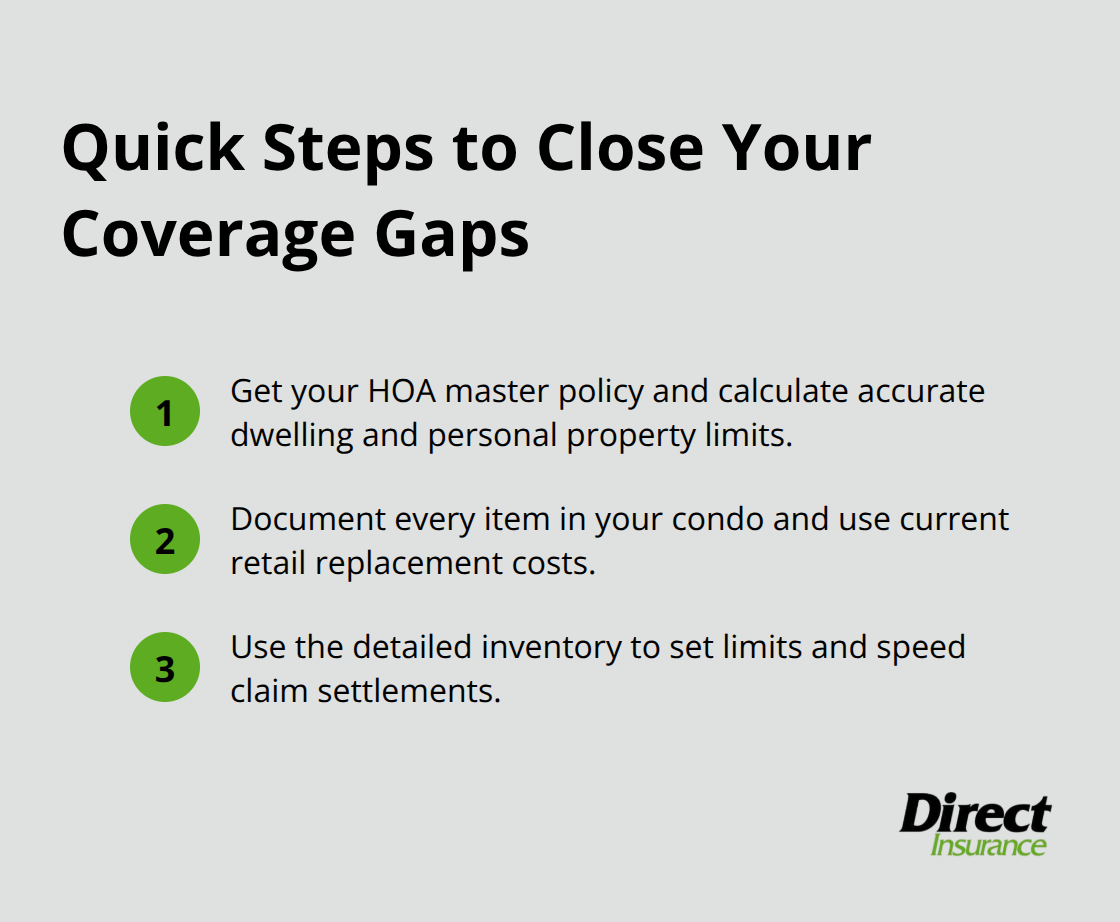

Two steps solve this problem. First, contact your HOA and obtain your master policy to understand exactly what type of coverage it provides, then calculate your dwelling and personal property limits based on realistic replacement costs, not guesses. If your building has bare-walls coverage, you need substantially higher dwelling limits than an all-in policy requires. Second, walk through your condo with a camera or notepad and document everything of value, assigning current retail replacement costs rather than original purchase prices. That detailed inventory becomes your coverage roadmap and accelerates claim settlements if loss occurs.

Insufficient Liability Coverage Exposes Your Personal Assets

The third mistake is carrying insufficient liability coverage because owners underestimate lawsuit costs and medical bills. A guest slips on your stairs, breaks their hip, and requires surgery, physical therapy, and lost income totaling $150,000. Your $100,000 liability limit covers only two-thirds of the claim, leaving $50,000 exposed on your personal assets. Medical costs in Utah have risen significantly, and a serious injury claim easily exceeds $200,000 in total damages. Ground-floor condo units face higher liability risk because more guests and foot traffic pass through your space, yet many owners with ground-floor units carry the same $100,000 limit as upper-floor residents.

We recommend Utah condo owners carry a minimum of $300,000 in liability coverage through their HO-6 policy, with $500,000 preferred for ground-floor units or if you frequently host gatherings. Umbrella insurance adds $1,000,000 in additional liability protection for roughly $150 to $300 annually, which is inexpensive protection against a catastrophic claim that could otherwise destroy your financial security. These three mistakes-ignoring master policy limitations, underestimating personal property and improvement values, and carrying inadequate liability limits-create a perfect storm of vulnerability that leaves Utah condo owners exposed to devastating financial losses.

Final Thoughts

Contact your HOA today and request a copy of your master policy declaration page to identify whether your building has all-in, bare-walls, or single-entity coverage. This document determines how much dwelling coverage you actually need on your HO-6 policy and prevents the underinsurance trap that costs owners thousands after water damage or fire. Walk through your condo with a camera and create a detailed inventory of your belongings, assigning realistic replacement costs based on current retail prices, then match your personal property coverage to that total value.

Review your liability limits and assess your actual risk honestly. Ground-floor units and owners who frequently host gatherings need higher liability protection than the $100,000 minimum most carriers offer, and umbrella insurance adds $1,000,000 in additional coverage for roughly $150 to $300 annually. Your Utah condo insurance strategy should combine dwelling coverage matched to your master policy type, personal property coverage equal to your belongings value, liability protection of at least $300,000, and loss assessment coverage to shield you from surprise HOA special assessments.

Direct Insurance Services helps Utah condo owners navigate these coverage decisions and find policies that protect their investment without overpaying for unnecessary add-ons. Our team works with top-rated carriers to compare quotes and explain exactly what your coverage includes and excludes. Contact us today to review your current policy or get quotes from multiple carriers.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation