Does Home Insurance Cover Termite Damage?

Termite damage can cost homeowners thousands of dollars in repairs, yet most people don’t realize their standard homeowners insurance won’t cover it. We at Direct Insurance Services want to help you understand this coverage gap and protect your home.

The question of whether home insurance covers termite damage has a straightforward answer: it typically doesn’t. Learning why-and what you can do about it-is the first step toward real protection.

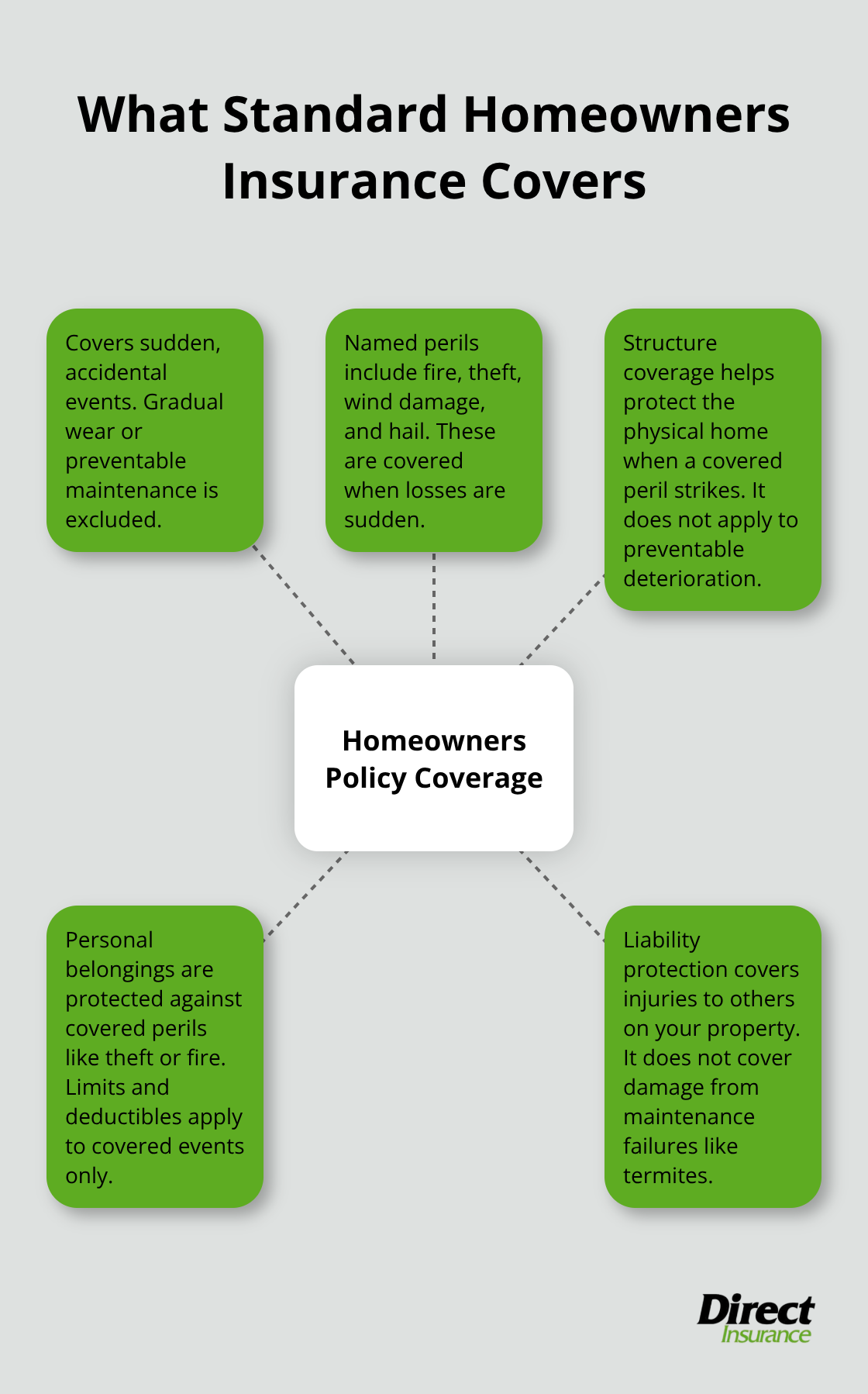

What Your Homeowners Policy Actually Covers

Standard homeowners insurance protects against sudden, accidental events-not gradual wear or preventable maintenance. Your policy covers perils like fire, theft, wind damage, and hail.

It shields your home’s structure, personal belongings, and provides liability protection if someone gets injured on your property. However, the moment damage results from something preventable or happens slowly over time, insurers exclude it.

Why Insurers Exclude Termite Damage

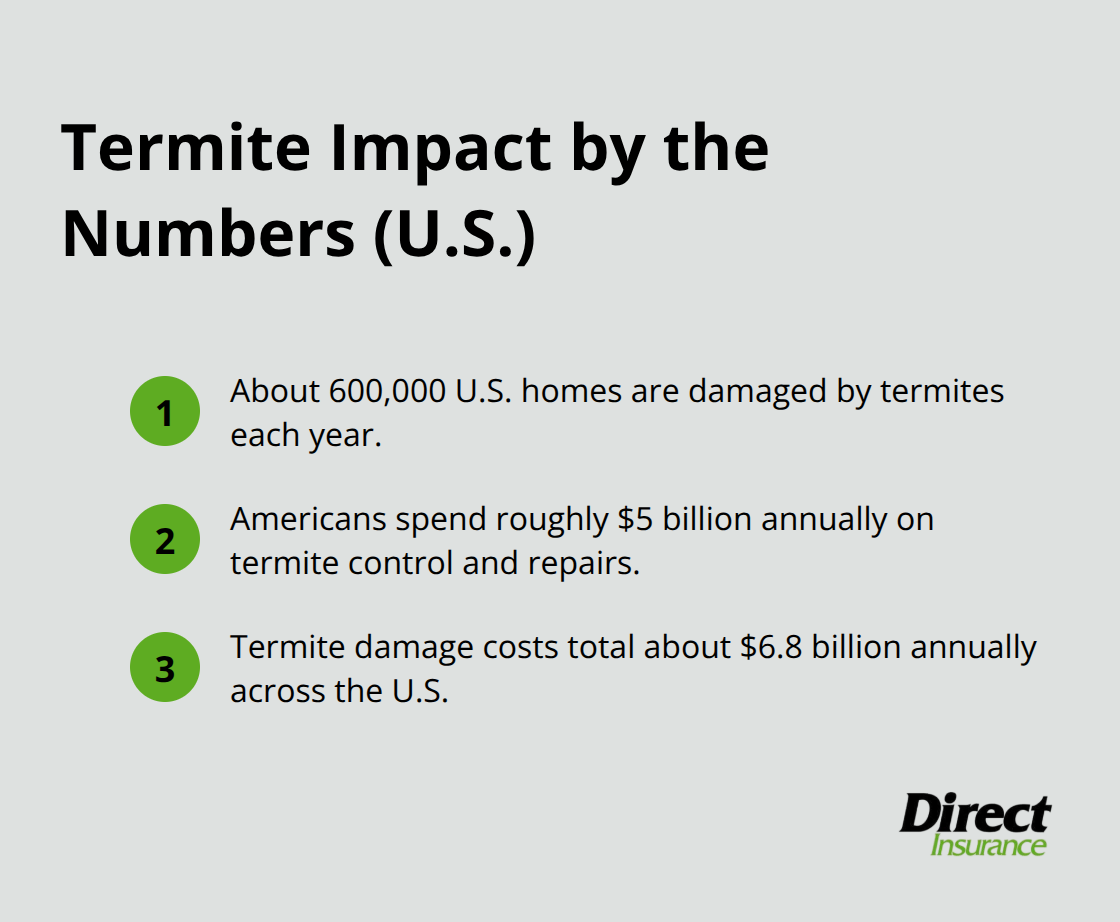

Insurers classify termite damage as a maintenance issue you should have prevented. Termites damage approximately 600,000 homes in the U.S. each year, and U.S. residents spend an estimated $5 billion annually to control termites and repair termite damage, yet homeowners insurance policies almost universally deny these claims. The reason is straightforward: termites don’t strike suddenly like a lightning fire. They work invisibly for months or years, which insurers view as a failure of preventative care rather than an insurable event.

The Hard Line Between Sudden and Gradual Loss

Insurance companies draw a hard line between sudden losses and gradual deterioration. A pipe bursting overnight and flooding your basement gets covered; termites slowly consuming your joists do not. Insurers argue that you have the ability to prevent termite infestations through inspections, maintenance, and professional treatments. This classification matters because it shifts the financial responsibility entirely to you.

Coverage Limits Don’t Apply to Excluded Perils

Coverage limits and deductibles become irrelevant when the damage itself falls outside your policy’s scope. Your deductible might be 500 or 1,000 dollars, but it won’t apply to termite repairs because termite damage isn’t a covered peril at all. The only rare exception occurs when termite damage indirectly causes a covered loss-for instance, if termites damage electrical wiring and spark a fire, the fire damage itself might be covered (though the termite damage remains your responsibility).

What This Means for Your Home

This coverage gap leaves homeowners vulnerable to substantial out-of-pocket costs. The financial burden falls entirely on you to detect termites early and address them before they cause expensive structural damage. Understanding this reality makes prevention and early detection not just smart choices-they become your primary defense against devastating repair bills.

Why Insurance Won’t Pay for Termite Damage

Insurers refuse to cover termite damage because they classify it as a maintenance failure, not an insurable event. The National Pest Management Association reports that termite damage costs approximately $6.8 billion annually across the U.S., yet homeowners absorb nearly all of these costs themselves. Insurance companies take this position because termites operate gradually-they spend months or years consuming wood before you notice the damage. This slow, preventable process falls outside what insurers consider a covered peril. A sudden fire from lightning receives coverage; termites silently destroying your foundation do not. The distinction matters financially because it means your policy’s deductible, coverage limits, and protections simply don’t apply. Insurers view termite prevention as your responsibility through regular inspections and maintenance, making any resulting damage your financial obligation.

Why Gradual Damage Gets Excluded

Insurance policies protect against unexpected events, not foreseeable deterioration. Termites don’t surprise you overnight-they give you time to catch them through inspections and preventative treatments. This is precisely why insurers exclude gradual damage across all policy types. A water pipe that bursts suddenly qualifies for coverage; water damage from a slow leak you ignored does not. The same logic applies to termites. Insurers argue that you have affordable options to prevent infestations through professional inspections, which cost between $200 and $500 annually according to pest control industry standards. This preventative accessibility is why insurance companies consistently deny termite claims. They see the damage as resulting from negligence rather than chance. Your policy protects against risks you cannot control; termite prevention falls squarely into the category of risks you can.

The Rare Exception That Doesn’t Help

A narrow exception exists in insurance contracts: if termite damage causes a secondary covered loss, that secondary damage might be covered. For example, if termites damage electrical wiring and spark a house fire, the fire damage itself could be covered (though the termite damage remains entirely your responsibility). This exception sounds helpful until you realize it rarely applies in practice. Most termite damage causes structural deterioration, not fires or other covered perils. The exception also requires you to prove that termites caused a specific covered event, adding complexity and legal costs to your claim. Essentially, this exception provides almost no practical protection for homeowners facing typical termite situations.

What You Can Do Instead

Since your standard homeowners policy won’t cover termite damage, you need to take action yourself. Professional pest control treatments, regular inspections, and preventative home maintenance become your primary defenses against costly repairs. The next section walks you through these practical steps to protect your home before termites cause expensive structural damage.

How to Protect Your Home from Termites

Catch Termites Early Through Professional Inspections

Annual professional inspections represent your best defense against costly repairs, and EPA recommendations for termite prevention emphasize this approach as effective. A certified pest inspector identifies termite activity before visible damage appears-a critical advantage since termites often remain hidden for years before swarmers or structural deterioration becomes obvious. Annual inspections typically cost between $200 and $500 according to pest control industry standards, far less than the $5 billion Americans spend annually on termite treatment and repairs. During an inspection, professionals look for mud tubes near your foundation, probe exposed wood for hollow spots with a flathead screwdriver, and check for telltale signs that indicate active colonies. If you spot mud tubes, maze-like patterns in wood, hollow-sounding timber when tapped, or salt-and-pepper droppings from drywood termites, contact a licensed exterminator immediately. The National Pest Management Association emphasizes that prevention costs less than remediation, and early detection prevents the kind of structural damage that can cost thousands of dollars and complicate selling your home.

Apply Professional Pest Control Treatments

Licensed pest management professionals use multiple treatment methods depending on your situation and termite type. Soil-applied termiticides create a chemical barrier around your foundation-professionals must install these correctly to avoid contaminating your home and drinking water wells. Termite baits offer another approach, using slow-acting insecticides in cellulose-based stations that workers transport back to the colony. For new construction or during renovations, borates sprayed on wood provide long-term protection. Each method targets termites differently, so a licensed professional helps you select the right approach for your specific infestation or prevention needs.

Eliminate Moisture and Block Access Points

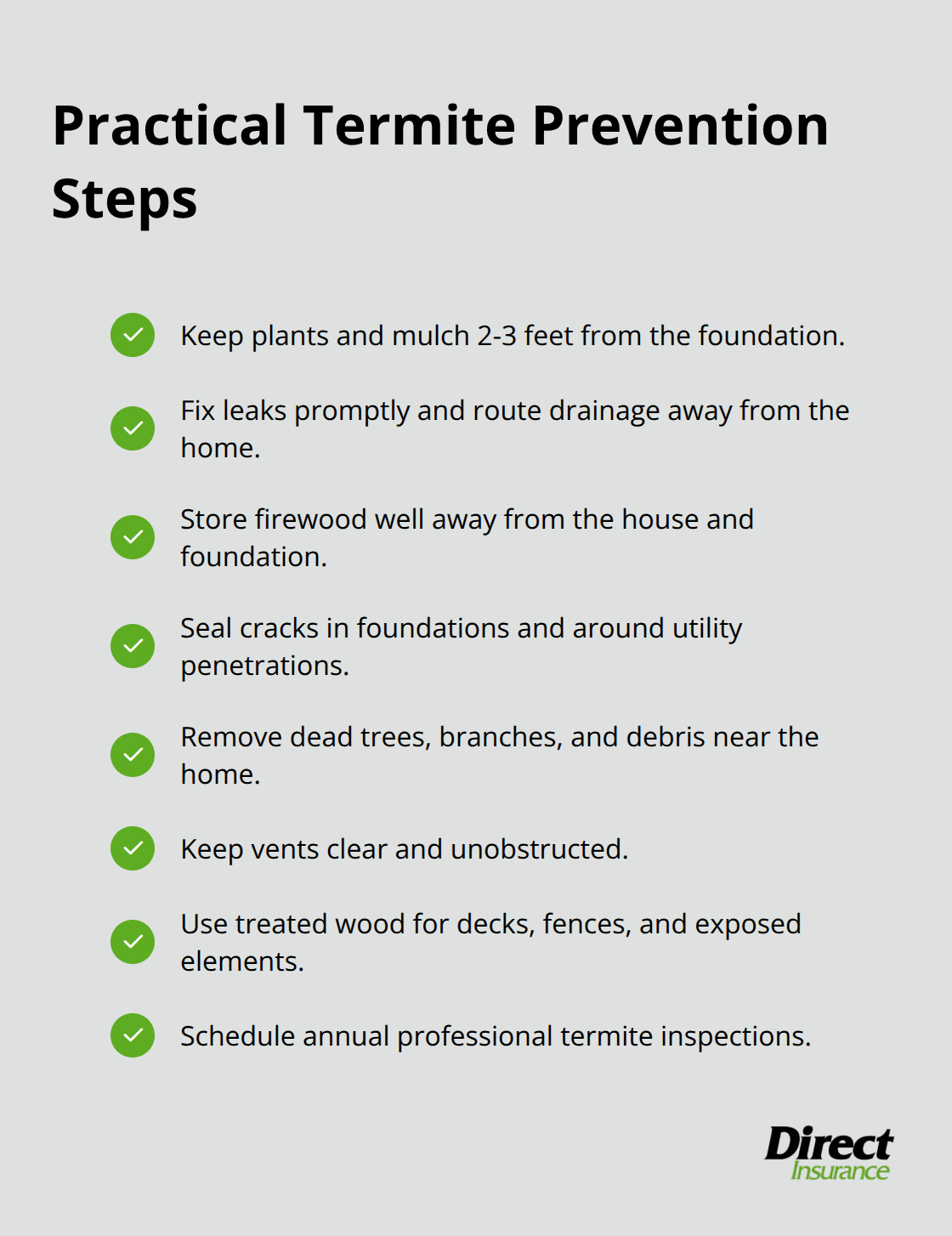

You control moisture and access through practical maintenance that costs little compared to structural repairs. Keep plants and mulch 2-3 feet away from your foundation to reduce moisture and termite access. Repair leaks in faucets, gutters, and roofs immediately, and direct storm drains away from your home. Never stack firewood next to your house, as wood stored near the foundation attracts termites. Reduce termite entry points by filling cracks in cement foundations and around utility penetrations with cement, grout, or caulk.

Remove dead trees, branches, and debris near your home, and keep vents free from blockage. Use treated wood for decks, fences, and any exposed wood elements throughout your property. Keeping rodents and insects away from your home is preventable with proper maintenance, and these preventative measures eliminate the conditions termites need to survive and thrive near your home.

Final Thoughts

Homeowners insurance won’t cover termite damage because insurers classify it as a maintenance issue you can prevent, not an insurable event. This means you bear the financial responsibility to detect termites early and address them before they cause expensive structural damage. The answer to “does home insurance cover termite damage” is no, but prevention works and costs far less than repairs.

Annual professional inspections catch termite activity before visible damage appears, costing between $200 and $500 compared to the thousands you’d spend on repairs. Soil-applied termiticides, termite baits, and borates provide effective treatment options when professionals apply them correctly. Simple maintenance steps like keeping mulch away from your foundation, fixing leaks promptly, removing firewood from your property, and using treated wood eliminate the conditions termites need to survive.

Your homeowners policy protects against sudden, accidental events, but termites operate gradually over months or years. We at Direct Insurance Services understand that homeowners insurance has limits, and we’re here to help you understand your coverage and identify protection gaps. Contact our team to review your policy and ensure you have the right coverage for what matters most.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation