Home and Contents Insurance: Complete Protection Guide

Your home is likely your biggest financial investment. Yet many homeowners don’t fully understand what their home and contents insurance actually covers-or whether they have enough protection.

At Direct Insurance Services, we’ve helped thousands of people navigate their coverage options and avoid costly gaps. This guide walks you through what’s protected, how to calculate the right coverage amount, and practical ways to reduce your premiums.

What Your Home and Contents Insurance Actually Covers

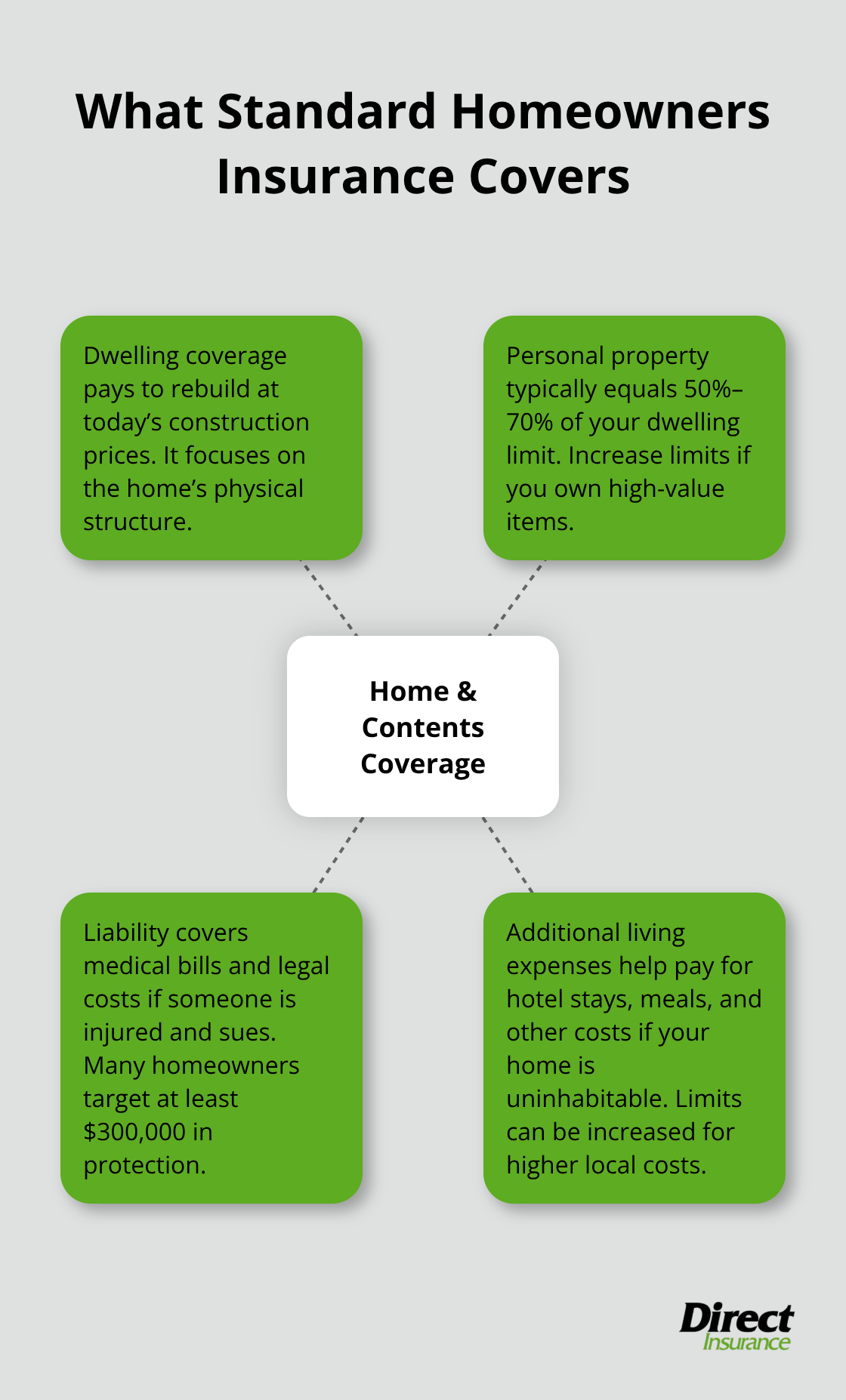

Standard homeowners policies protect four core areas: your home’s structure, personal belongings inside it, liability if someone gets hurt on your property, and additional living expenses if you cannot stay there temporarily. Dwelling coverage reimburses the cost to rebuild your home at today’s prices, not what you paid for it years ago. This matters because construction costs have climbed significantly. Personal property coverage usually runs between 50% to 70% of your dwelling limit, so a $200,000 home might include up to $140,000 for contents. That’s often not enough if you own expensive items like jewelry, electronics, or art collections.

Liability protection covers medical bills and legal costs if someone is injured at your home and sues you. Most policies start at $100,000 to $300,000, but at least $300,000 makes sense given today’s litigation costs. Many homeowners also add umbrella policies for an extra $1 million or more in liability protection at relatively low cost.

What Gets Left Out

The gaps in standard coverage frustrate homeowners more than anything else. Flood damage, earthquake damage, and mold from neglect are almost never covered by basic policies, yet these account for massive losses nationwide. If you live in a flood zone or area prone to earthquakes, you need separate riders or policies. Pest infestations, gradual roof wear, and plumbing neglect also fall outside standard protection. High-value items like jewelry typically hit coverage limits of just $1,500 to $2,500 per item unless you add a scheduled personal property rider with appraisals. Off-premises coverage reimburses some losses away from home, but limits are tight. Additional living expenses coverage helps if your home becomes uninhabitable after a covered loss, but it has daily caps and total limits you can increase for higher premiums.

Matching Coverage to Your Actual Situation

The biggest mistake homeowners make is accepting default coverage amounts without checking whether they match their actual needs. Your dwelling limit should equal what it costs to rebuild today, not your home’s market value or what you owe on the mortgage. A replacement cost calculator or conversation with an agent produces accurate numbers. Contents coverage requires a detailed inventory with photos and purchase dates. Most homeowners underestimate what they own until they actually list it room by room. For specialty items like collectibles, fine art, or watches worth more than standard limits, you should schedule them individually on your policy with formal appraisals. This guarantees full replacement cost without depreciation applied.

High-Value Items Need Extra Protection

Standard policies impose strict per-item limits on valuables. Jewelry typically maxes out at $1,500 to $2,500 per piece, electronics at similar levels, and art collections at even lower thresholds. If you own items that exceed these caps, a scheduled personal property rider with professional appraisals protects them properly. The appraisal documents the item’s condition and value, which speeds up claims and eliminates disputes over worth. Off-premises coverage also has limits, so items lost or damaged away from home may not receive full reimbursement without additional endorsements. Taking time to identify which possessions matter most and their actual replacement costs prevents costly underinsurance later.

Planning for Living Expenses After a Loss

Additional living expenses coverage pays for hotel stays, meals, and other costs if a covered loss makes your home uninhabitable. Most policies include this automatically, but the daily limits and total caps vary widely. A standard policy might cover $500 per day for up to 12 months, which sounds adequate until you face actual hotel and restaurant bills in your area. You can increase these limits for a modest premium increase. Understanding your current limits and whether they match your local cost of living matters before a loss occurs. Once you know what your policy covers and where the gaps exist, the next step involves calculating the right coverage amounts for your specific situation.

How to Calculate Your Coverage Needs

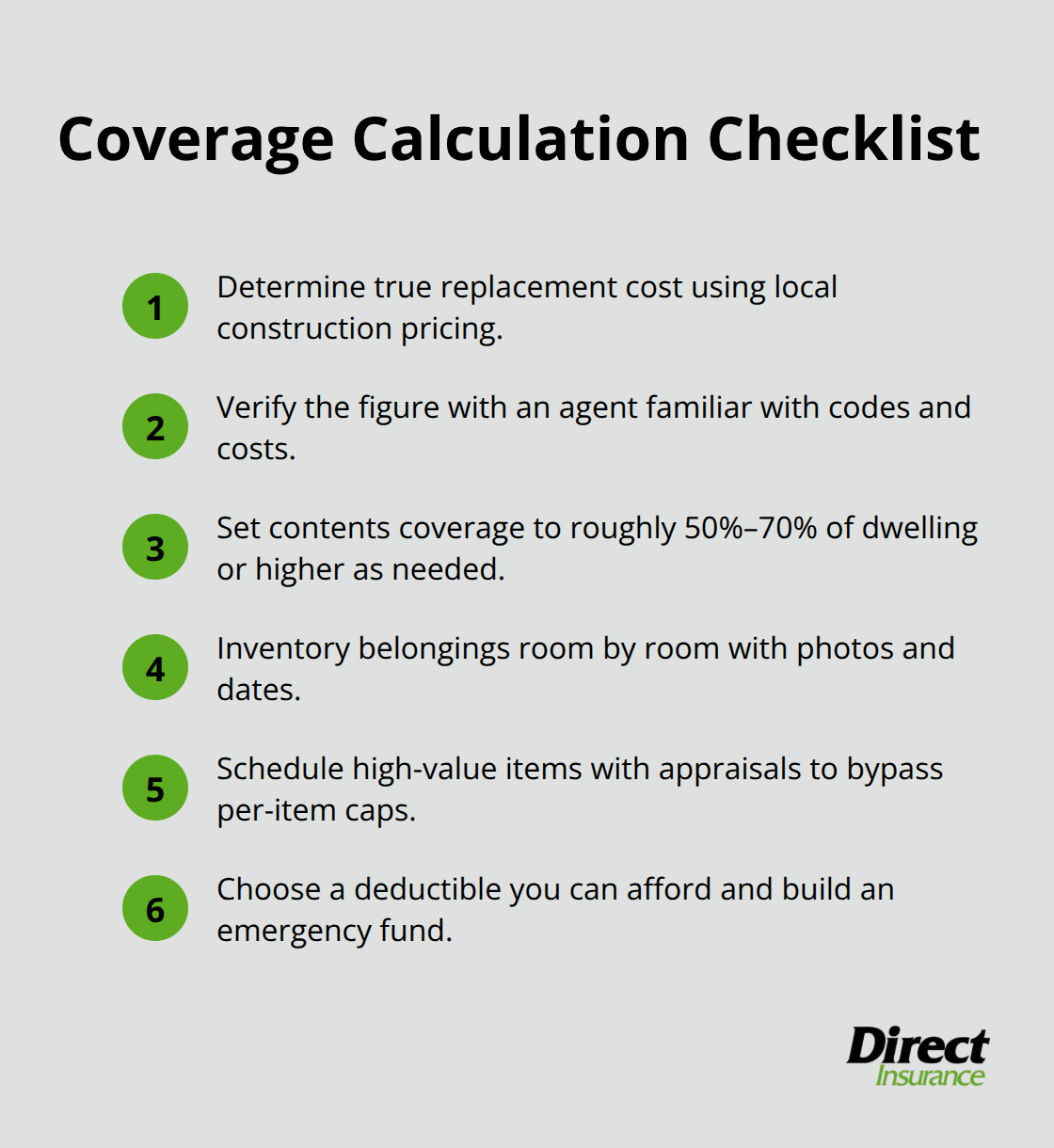

Getting the coverage amount right requires actual numbers, not guesses. Start with your home’s replacement cost, which is what it would cost to rebuild your house from the ground up at today’s prices and construction standards. This is not your home’s market value and not what you owe on your mortgage. If your home sold for $400,000 but rebuilding it would cost $500,000 due to labor and material prices, your dwelling coverage should be $500,000. You can calculate this yourself using online replacement cost estimators, but working with an agent who can verify the figure based on local building codes and current construction costs in your area produces more accurate results. Once you nail down the dwelling amount, contents coverage typically runs 50% to 70% of that figure, though you can adjust it higher if you own substantial belongings.

A $500,000 home might warrant $300,000 to $350,000 in contents coverage.

Inventory Your Possessions Room by Room

The real work starts when you actually inventory what you own. Most homeowners severely underestimate their possessions until they list them room by room with photos and purchase dates. Go through your closets, kitchen, garage, and storage areas. Electronics, furniture, clothing, tools, and hobby equipment add up fast. Once you total this value, compare it against your proposed contents limit. If your actual possessions exceed 70% of your dwelling coverage, increase your contents limit. Accepting a default limit that falls short of your actual needs sets you up for a painful claim experience where you receive partial reimbursement for items you can no longer replace.

Schedule High-Value Items Individually

Jewelry, art, collectibles, and high-end electronics hit per-item caps on standard policies. If you own items worth more than these thresholds, schedule them individually on your policy with professional appraisals. This rider removes the per-item limit and guarantees replacement cost without depreciation. The appraisal documents condition and value, which eliminates disputes during claims. This approach costs more upfront but prevents the scenario where an appraised $8,000 watch gets paid out at the policy’s limit. Spending $200 to $400 annually for a scheduled personal property rider protecting high-value items makes financial sense.

Choose a Deductible You Can Actually Afford

Your deductible directly controls your premium. Raising your deductible from $500 to $1,000 or $2,500 lowers your annual premium, sometimes substantially. A higher deductible means you pay more out of pocket when a loss occurs, but you save money on premiums every single year. The math works in your favor if you can afford the higher out-of-pocket cost. Choose a deductible you can actually afford to pay without financial strain. If a $2,500 deductible would create hardship, stick with $1,000 even if premiums cost slightly more. Some insurers offer deductible buyback options, where you pay extra to reduce your deductible for specific claim types. These rarely make financial sense compared to simply accepting a reasonable deductible and building an emergency fund to cover it.

Next Steps: Finding Discounts and Locking in Your Rate

Once you’ve determined your coverage amounts and selected a deductible that fits your budget, the next phase involves shopping for the best rate. Insurance companies offer multiple discounts that can substantially reduce your annual premium, and understanding which ones apply to your situation helps you maximize savings.

Cost Factors and Money-Saving Tips

Your premium depends on factors you control and factors you cannot. Location tops the list of things you cannot change, but understanding why helps you shop smarter. According to Matic data, the premium gap between homes with newer roofs and those with 11–15-year-old roofs widened to about $155 in 2025, up from just $49 in 2022. This shows that roof age has become a major pricing factor as insurers use satellite imagery, drones, and AI to assess actual property conditions rather than making broad assumptions. In 2025, average new homeowners insurance premiums rose to $1,952, an 8.5% increase, and deductibles climbed by 22% as insurers shifted more upfront costs to policyholders.

How Location and State Regulations Shape Your Rate

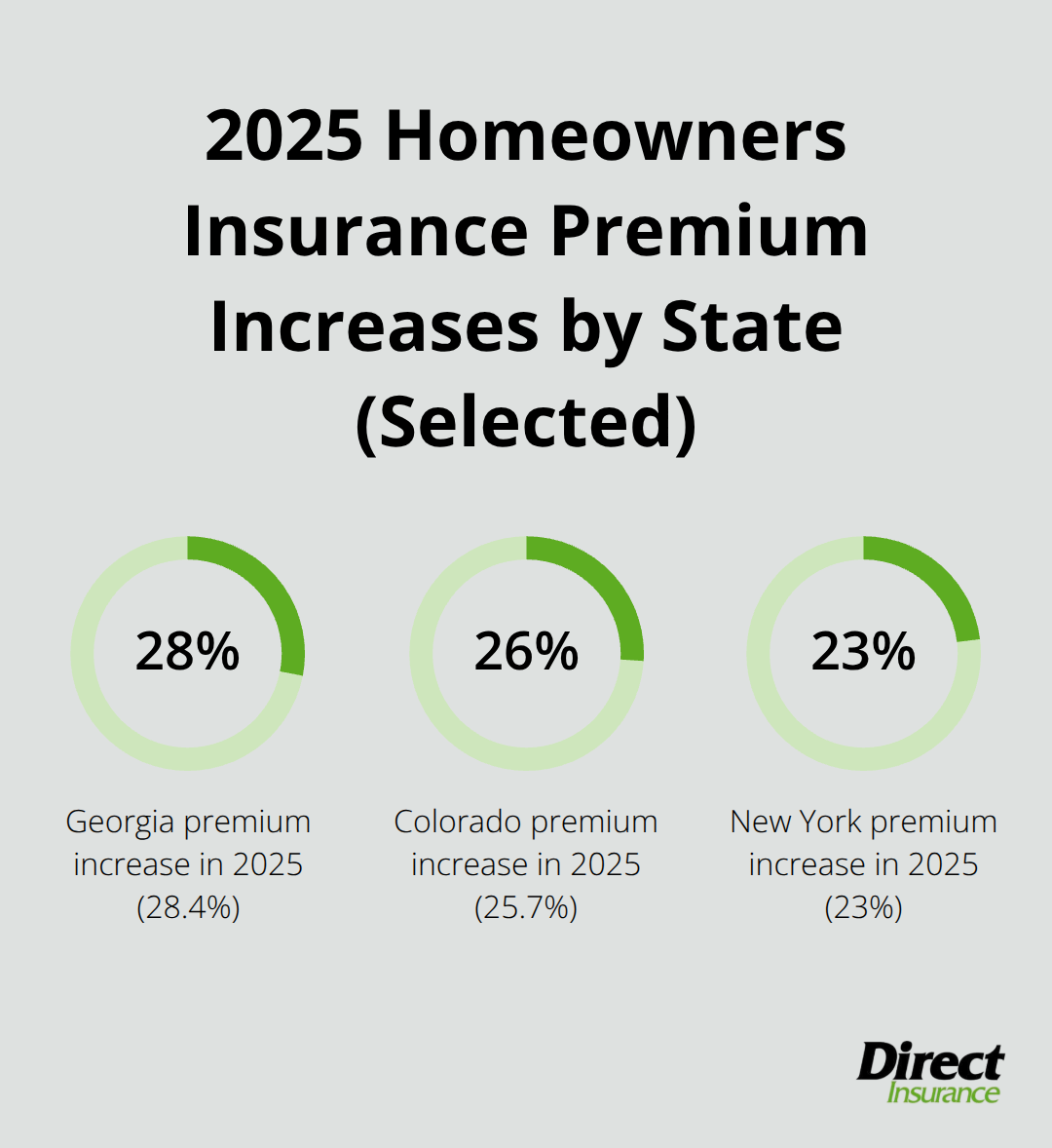

State matters enormously. Colorado saw premiums jump 25.7% in 2025, Georgia 28.4%, New York 23%, Texas 20.5%, and Mississippi 19.4%. These variations stem from local climate exposure, rebuilding costs, and each state’s Department of Insurance regulations.

Your home’s construction materials, electrical and plumbing updates, proximity to fire services, and claims history all influence what insurers charge.

Safety Features That Lower Your Premium

Installing a monitored security system typically reduces premiums by around 5% or more, while smoke alarms and carbon monoxide detectors can lower costs by 10% or more. These are real discounts with real impact on your annual bill. Taking action on these improvements pays for itself through premium savings over time.

Bundling and Loyalty Rewards

Bundling your home and auto policies with the same insurer delivers the most straightforward savings available. Most insurers offer multi-policy discounts ranging from 10% to 25% off your combined premiums, and consolidating billing simplifies your financial life. Beyond bundling, loyalty matters-insurers often reward customers who stay with them for multiple years with additional discounts. Check whether you qualify for group or association plans through your employer or professional memberships, as these negotiated rates sometimes beat standard discounts. If you work from home, mention it to your insurer, as some carriers offer discounts for reduced occupancy risk. Seniors also qualify for dedicated discounts at many companies.

Deductible Strategy and Shopping Around

The most effective way to lower your monthly payment remains choosing a higher deductible if you can afford the out-of-pocket cost. Jumping from a $500 to a $1,000 deductible typically saves 15% to 25% annually, and moving to $2,500 saves even more. Try selecting a deductible you can actually pay without financial hardship when a loss occurs. Building an emergency fund to cover your deductible makes this strategy work without creating stress. Shop around every two to three years. Coverage availability improved significantly in 2025 with quotes per person rising 78% from the market low in 2024, giving you more options than before. Getting five quotes from different insurers reveals the real price range for your situation and prevents overpaying out of inertia.

Final Thoughts

The foundation of protecting your home and contents insurance starts with understanding what your policy actually covers and where gaps exist. Most homeowners discover too late that their dwelling limit falls short of rebuilding costs, their contents coverage misses high-value items, or critical perils like floods require separate policies. Getting these details right before a loss occurs prevents financial devastation and claim disputes.

Pull out your current policy and compare it against what you’ve learned here. Check whether your dwelling limit matches today’s reconstruction costs in your area, verify that your contents coverage reflects what you actually own, and confirm that your liability protection aligns with your assets. If you’ve made home improvements, acquired valuable items, or experienced life changes, your coverage likely needs adjustment.

Shopping for better rates also matters-coverage availability improved significantly in 2025, giving you more options than before. We at Direct Insurance Services help Utah families and individuals navigate these decisions without pressure, working with top-rated carriers to find home and contents insurance that fits both your needs and budget. Reach out today to discuss your coverage and discover how much you might save.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation