Auto Insurance Utah Rates: What Impacts Your Premium

Auto insurance Utah rates vary significantly based on your personal circumstances and driving habits. At Direct Insurance Services, we’ve helped thousands of Utah drivers understand exactly what pushes their premiums up or down.

Your age, driving record, vehicle type, and even where you live in Utah all play a role in determining what you pay. The good news is that many of these factors are within your control.

What Drives Your Utah Auto Insurance Premium

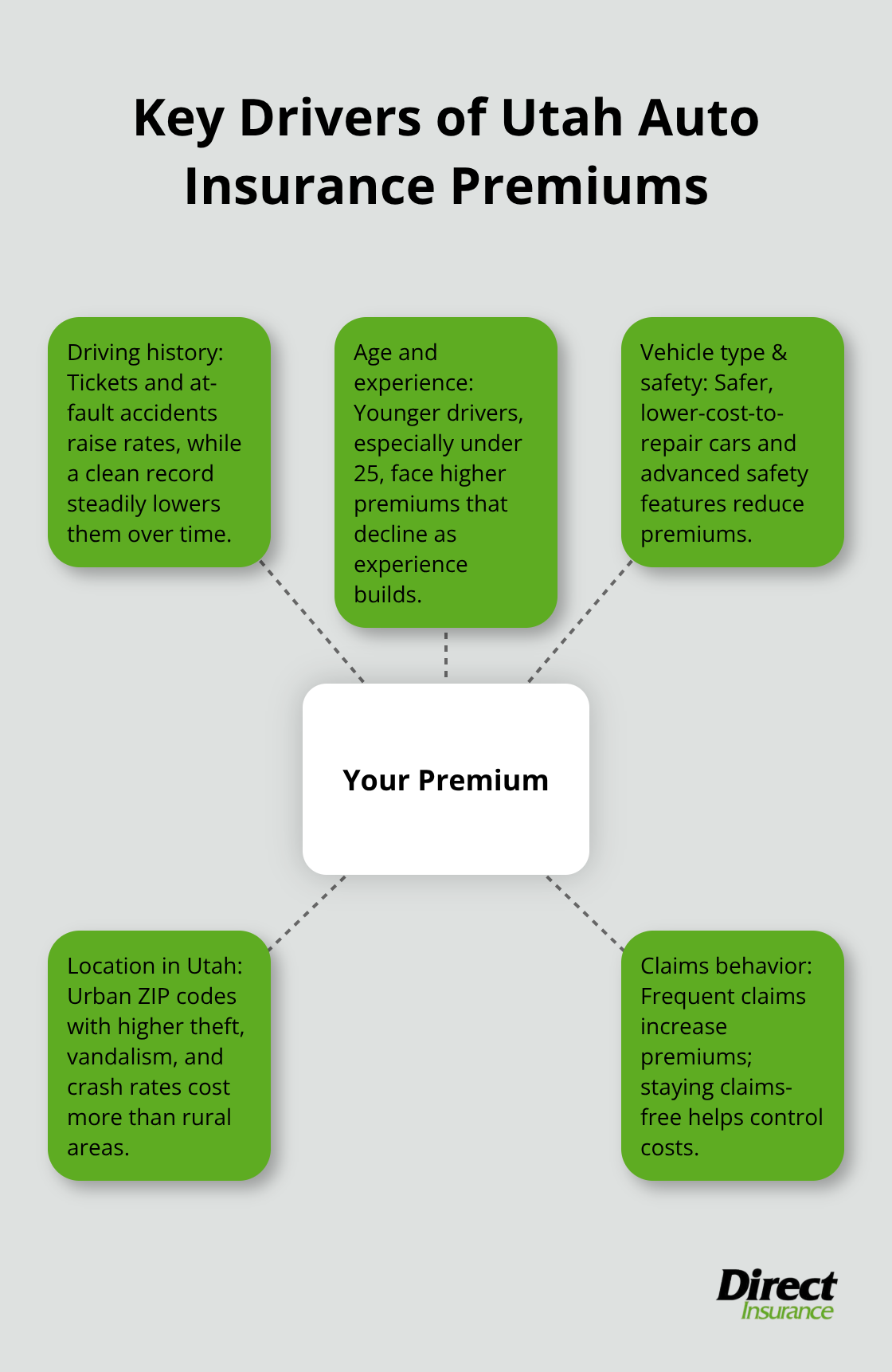

Your driving history stands as the single most important factor insurers examine when setting your rate, and this is where you have the most control. According to the Utah Department of Insurance and the National Association of Insurance Commissioners, a clean driving history lowers your premiums over time, while accidents or moving violations raise rates significantly and can take years to subside. One at-fault accident increases your premium by 20 to 40 percent depending on severity, and multiple violations compound the problem. Safe driving habits translate directly to lower costs. If you’ve had violations in the past, know that most insurers reset their assessment after three to five years of clean driving, so your current record doesn’t lock you into high rates permanently. Your claims history matters just as much-drivers who file frequent claims face higher premiums than those who stay claims-free.

Filing multiple small claims can work against you financially over time, even though you should still file legitimate claims when necessary.

Age and Experience Shape Your Rate

Age represents the second major factor insurers use when calculating your premium. Young drivers under 25 pay substantially more than experienced drivers because statistical data shows they cause accidents at higher rates. A 20-year-old driver typically pays 50 to 100 percent more than a 40-year-old with a clean record, according to NAIC data. As you gain driving experience and reach your mid-twenties, your rates drop noticeably. Marital status also plays a role-married drivers often qualify for discounts that single drivers don’t receive, and some insurers offer reductions when couples insure multiple vehicles together. Adding a teen driver to your policy will spike your costs significantly because of their inexperience, but a defensive driving course can offset some of that increase.

Vehicle Type and Safety Features Control Costs

The make, model, year, and repair costs of your vehicle determine a substantial portion of your premium. Safer vehicles with high Insurance Institute for Highway Safety ratings cost less to insure than less safe cars because they reduce injury risk and claim severity. Vehicles with advanced safety features like automatic emergency braking and lane-keeping assist often qualify for discounts. Luxury and exotic vehicles cost more to insure due to higher repair and replacement costs. Theft risk matters too-desirable models in high-theft areas face premium penalties. For older vehicles, consider whether comprehensive or collision coverage justifies the cost relative to your car’s actual value; if your premium exceeds 10 percent of the vehicle’s worth annually, dropping these coverages may save you money.

Location Within Utah Affects Your Premium

Your ZIP code within Utah affects rates because urban areas have higher theft, vandalism, and accident frequency than rural areas. Street parking in densely populated neighborhoods elevates your premium further due to increased theft and risk exposure. Where you park and drive your vehicle influences your final premium amount significantly. These location-based factors (theft rates, traffic density, and accident history) vary considerably across Utah’s cities and counties. Understanding how your specific area impacts your rate helps you anticipate what you’ll pay and identify which coverage adjustments make the most sense for your situation. With so many variables affecting your premium, the next step is learning which discounts and policy adjustments can actually reduce what you owe each month.

Strategies That Actually Lower Your Utah Auto Insurance Premium

Bundle Your Policies for Immediate Savings

Reducing your Utah auto insurance premium requires action, not wishful thinking. Bundling policies delivers real savings-combining auto with homeowners or renters insurance typically yields multi-policy discounts of anywhere from 10% to 25% depending on your insurer. This works because insurers reward customer loyalty and reduced administrative overhead. If you own a home or rent, bundling should be your first move before shopping elsewhere.

Maintain a Clean Driving Record

Your driving record remains your most powerful negotiating tool with insurers. A clean three to five years of driving allows you to access the lowest rates available, and some insurers offer accident forgiveness programs that prevent premium increases after your first at-fault claim. This means staying off the road’s wrong side pays dividends immediately. A clean driving history directly translates to lower costs month after month.

Leverage Low Mileage and Safety Features

Low mileage directly impacts your premium because higher annual mileage increases accident risk-drivers who travel 10,000 miles yearly pay noticeably less than those driving 25,000 miles or more according to NAIC data. If you work from home or use public transportation, inform your insurer about your actual mileage, as overestimating costs you money every month. Safety devices installed on your vehicle reduce theft risk and injury severity, which means discounts apply for anti-theft alarms, immobilizers, and advanced braking systems. Vehicles with high Insurance Institute for Highway Safety ratings automatically qualify for lower premiums, so your vehicle’s safety record matters more than its age alone.

Shop Around and Compare Quotes Regularly

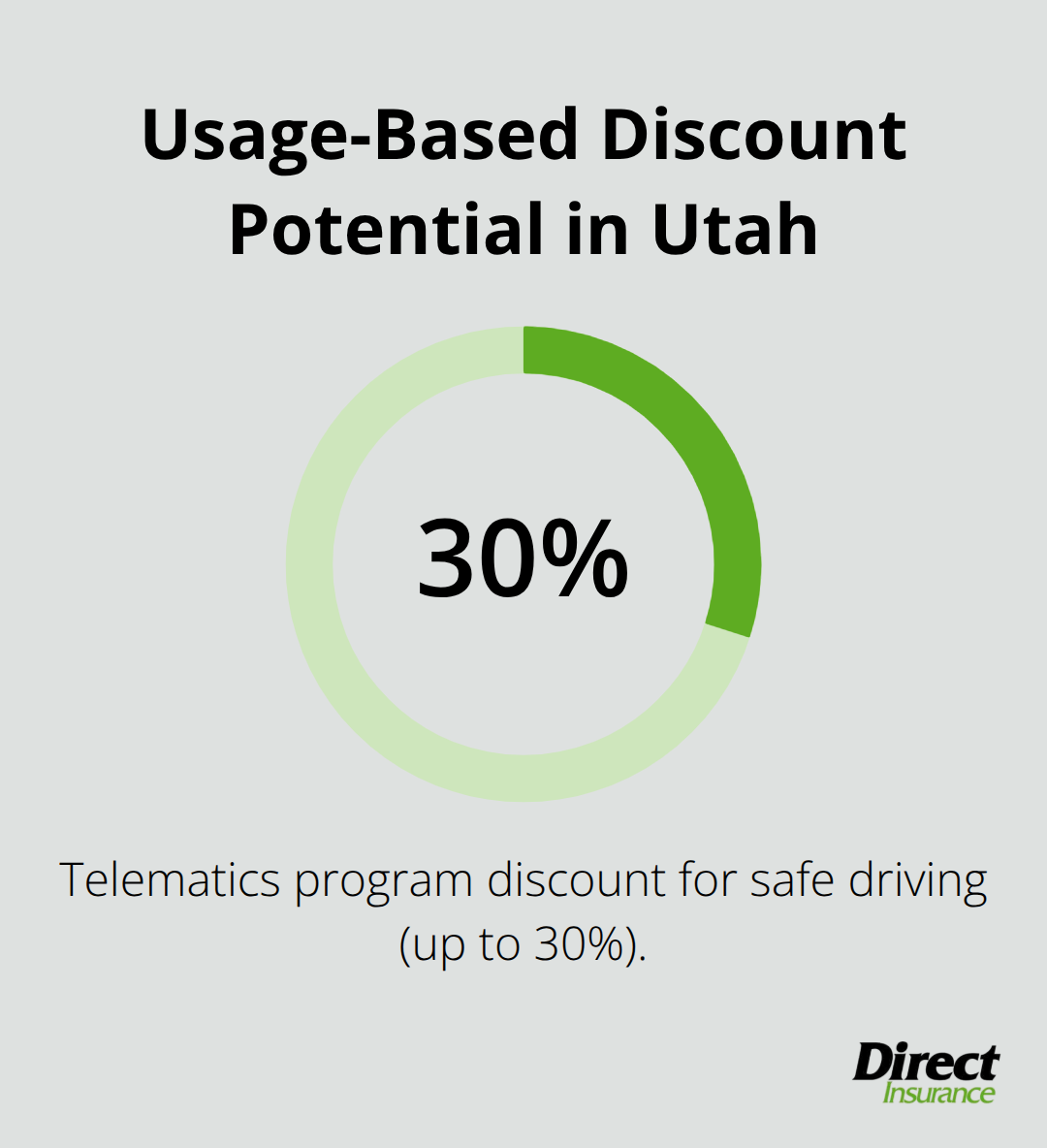

Shopping around for quotes separates drivers who overpay from those who pay fair prices. Insurance rates vary dramatically between carriers-the same coverage can cost 40 to 60 percent more at one insurer than another, making comparison shopping non-negotiable for Utah drivers. Obtain quotes from at least three insurers before renewing your policy, and do this every two to three years since your risk profile and available discounts change over time. State Farm offers usage-based programs like Drive Safe & Save that monitor your driving behavior and reward safe habits with discounts up to 30 percent in some cases, though participation is voluntary. These telematics programs track speeding, hard braking, rapid acceleration, and sharp turns-safe drivers benefit immediately.

Optimize Coverage and Deductibles

Defensive driving courses completed within the last three years can earn discounts for drivers 55 and older, with some programs available for younger drivers as well. Your insurance score, which incorporates credit-based factors, influences your rate, so maintaining good financial habits supports lower premiums. For older vehicles worth less than 10 times your annual comprehensive and collision premium, dropping these coverages saves money without leaving you dangerously exposed. Increasing your deductible from $500 to $1,000 reduces your premium if you can afford the out-of-pocket cost when filing a claim. With so many discount opportunities and coverage adjustments available, working with an independent agent who understands Utah’s specific insurance landscape becomes invaluable-they can identify which combinations of discounts and coverage levels align with your actual needs and budget.

How Utah Stacks Against National Insurance Costs

Utah’s Position in the National Rate Landscape

The average annual auto insurance cost in the United States sits around $1,553 according to US News & World Report data from 2022, but Utah drivers often pay rates that diverge significantly from this national baseline. Understanding where Utah falls relative to other states matters because it helps you determine whether you’re paying a fair price or overpaying compared to similar drivers elsewhere. Utah’s rates reflect specific regional factors that differ from states like California, Texas, or New York, which means direct comparisons require examining the underlying cost drivers that push premiums up or down across different regions.

Why Utah Rates Fall in the Middle Range

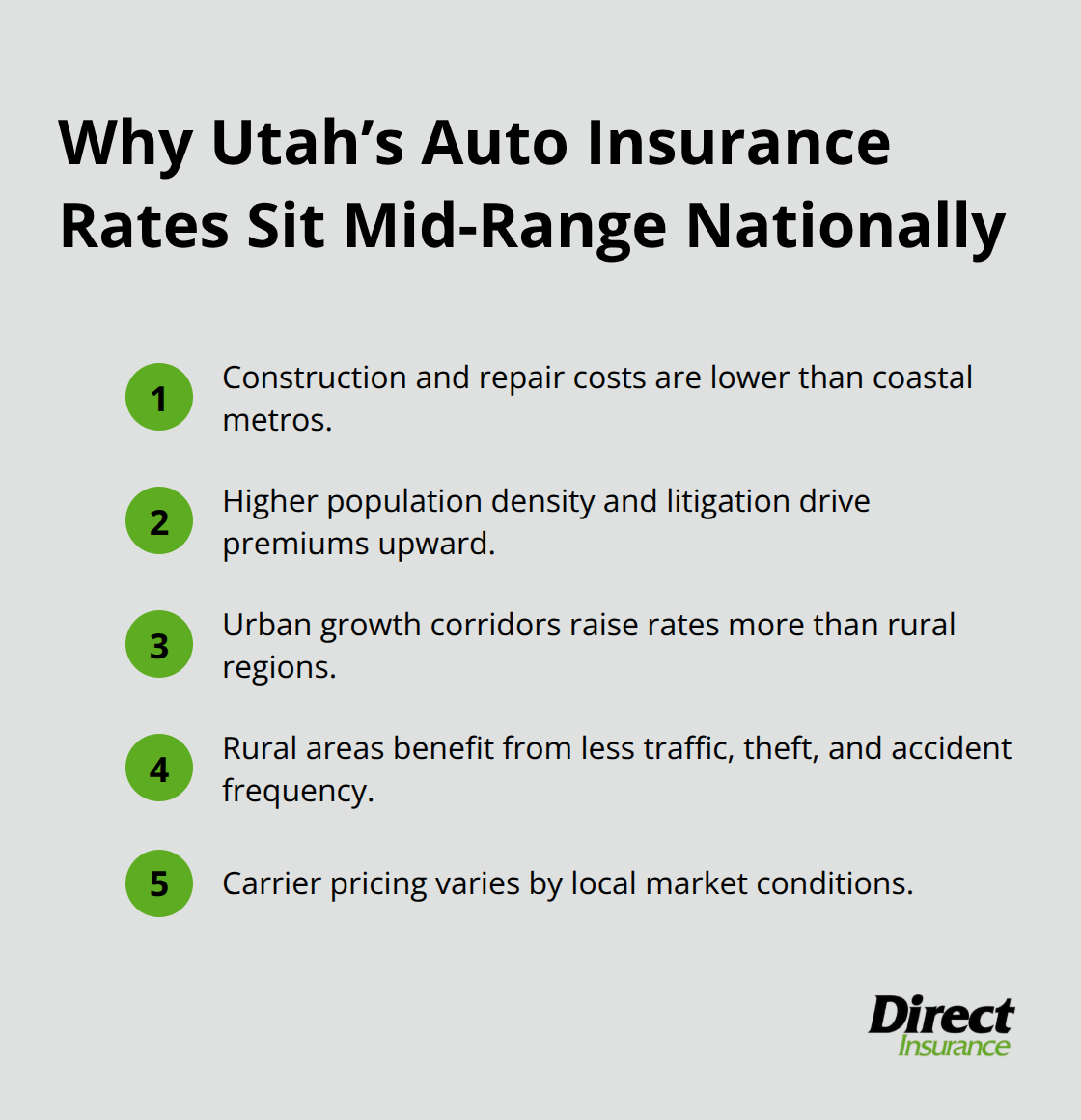

Utah experiences moderately higher premiums than some neighboring states but lower rates than coastal urban centers, primarily because construction and repair costs in Utah remain below levels in densely populated metropolitan areas like Los Angeles or Seattle. According to the National Association of Insurance Commissioners, states with higher population density and increased litigation costs naturally see elevated premiums across all carriers. This explains why Utah’s rates fall in the middle range nationally. However, Utah’s growing population in the Salt Lake City and Provo-Orem corridors has pushed rates upward in these urban zones, while rural areas like southwestern Utah maintain significantly lower premiums due to reduced traffic congestion, lower theft rates, and fewer accident claims.

How Inflation and Weather Impact Your Premiums

The inflation affecting construction materials and repair labor nationwide since 2021 has impacted Utah rates alongside rising interest rates that influence claim payouts and reinsurer costs. These factors affect all states equally but hit insurers’ bottom lines differently based on local market conditions. Extreme weather events have become increasingly severe across the western United States, driving more comprehensive and collision claims in Utah particularly during winter months when snow and ice cause accidents that spike claims frequency.

Location Within Utah Matters Most

Your location within the state matters far more than Utah’s national ranking, since a driver in downtown Salt Lake City pays substantially more than someone in rural Daggett County due to local risk concentration and repair costs specific to that area. Urban corridors concentrate theft, accidents, and traffic density, all factors that raise premiums significantly compared to rural regions.

Final Thoughts

Your auto insurance Utah rates reflect choices you make and circumstances beyond your control, but understanding this distinction puts you in charge of your premium. Bundling policies, maintaining a clean driving record, shopping for quotes every few years, and adjusting deductibles deliver real savings when you act on them consistently. Utah’s position in the national rate landscape means you likely pay a fair price compared to coastal states, though your specific ZIP code within Utah matters far more than regional comparisons.

Getting a personalized quote from multiple insurers is your next step because generic advice about average costs doesn’t help when your premium depends on your age, driving record, vehicle type, and exact location. Request quotes from at least three carriers and ask specifically about defensive driving discounts, usage-based programs, bundling options, and safety feature discounts relevant to your vehicle. An independent agent accesses multiple carriers simultaneously, identifies which discounts you qualify for, and explains coverage options in plain language without pressure.

We at Direct Insurance Services help Utah drivers navigate these decisions by offering tailored solutions that fit your actual needs and budget. Contact us for a personalized quote and find out how much you could save with the right coverage and discounts in place.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation