Does Home Insurance Cover Wildfire Damage?

Wildfire season brings real anxiety for homeowners. The question of whether home insurance covers wildfires isn’t always straightforward, and many policies have significant gaps.

At Direct Insurance Services, we’ve helped countless homeowners understand their actual coverage when it matters most. This guide breaks down what your policy protects and where you need additional safeguards.

What Your Standard Policy Actually Covers

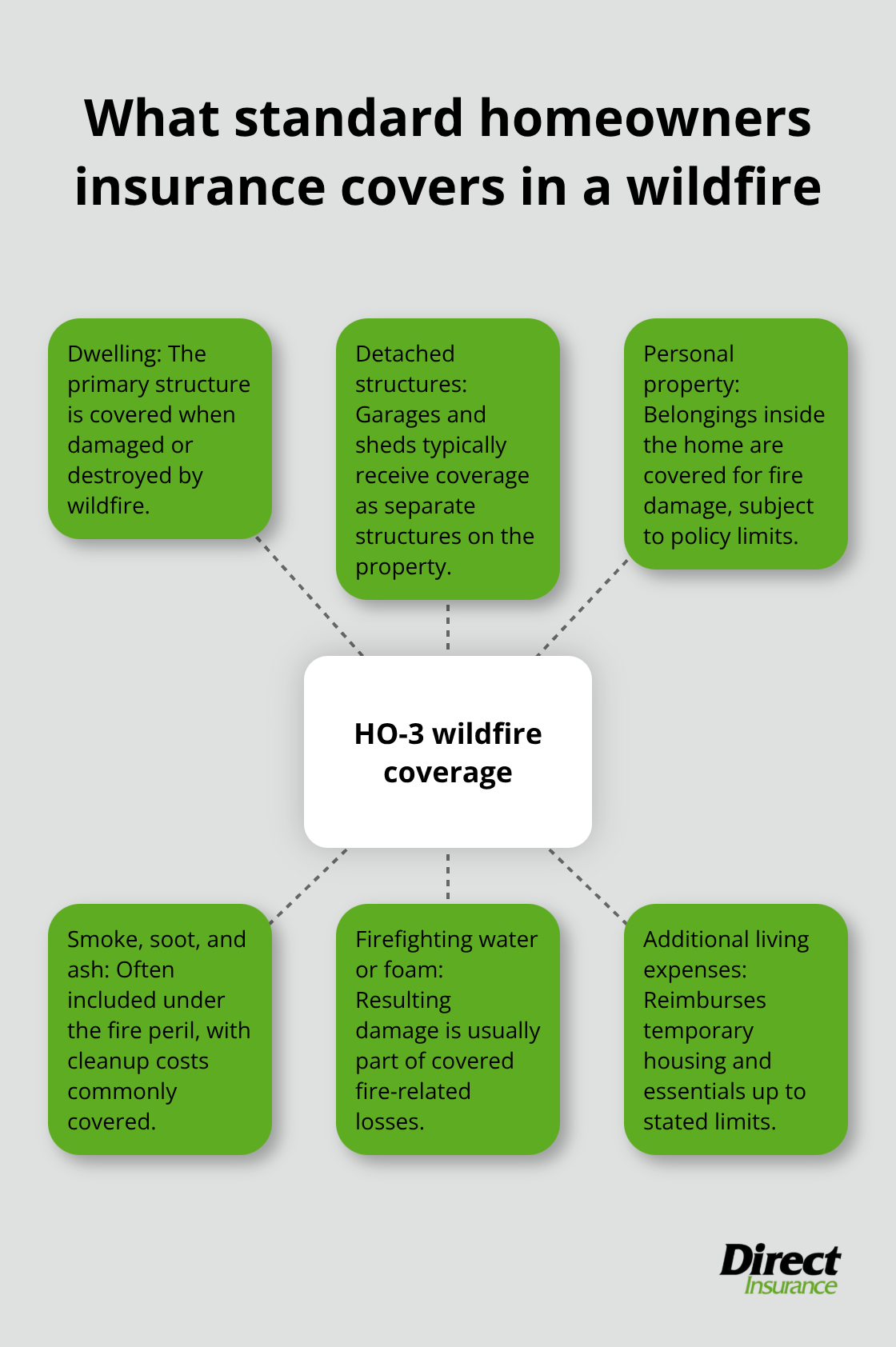

Standard homeowners insurance treats wildfire damage as a fire peril, which means your dwelling, detached structures like garages and sheds, and personal belongings inside your home receive protection if flames destroy them. The Insurance Information Institute confirms that HO-3 policies (the most common type) provide this coverage automatically. However, coverage limits matter far more than most homeowners realize.

If your home is insured for $400,000 but rebuilding costs spike to $600,000 after a wildfire-which happens regularly when labor and materials surge in fire-affected regions-you face a $200,000 gap. Replacement cost coverage pays current construction prices, while actual cash value deducts depreciation and leaves you substantially short. Replacement cost endorsements reflect reality after a loss, not outdated valuations.

Smoke and Ash Damage Receives Coverage More Often Than People Think

Smoke damage from wildfires falls under the fire portion of your policy and typically receives coverage, including cleanup costs and temporary housing during repairs. Soot and ash that infiltrate your home, damage to belongings from smoke exposure, and even firefighting water or foam damage are usually included. The National Fire Protection Association notes that many homeowners overlook this coverage because they assume only direct flame damage counts. The practical takeaway is straightforward: photograph smoke damage inside your home before cleanup begins, document all affected items, and submit these records with your claim. Insurers need visual evidence to process reimbursement efficiently.

Additional Living Expenses Reimburse Your Actual Costs During Evacuation

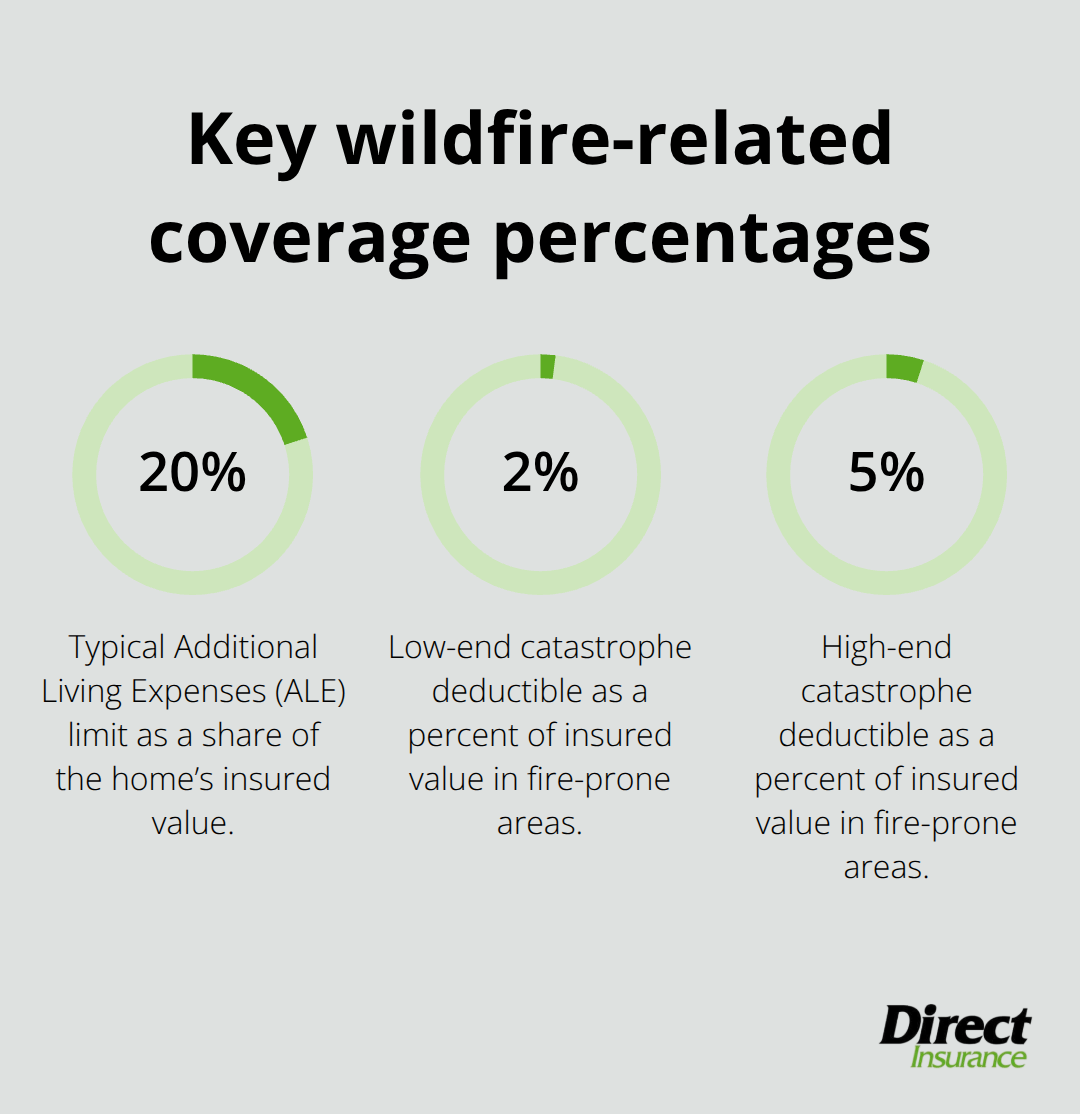

If a wildfire forces evacuation and your home becomes uninhabitable, additional living expenses coverage reimburses hotel stays, meals, pet care, and other necessary costs up to your policy limits, which typically run around 20 percent of your home’s insured value. In high-risk areas, this limit often proves insufficient. A family displaced for three months in a region where hotels cost $150 per night quickly exhausts an $80,000 limit.

You should keep every receipt-lodging, groceries, temporary storage, laundry services-because your insurer will request documentation. Some policies cap daily hotel reimbursement at specific amounts, so contact your agent before booking to confirm what qualifies and avoid unexpected denials.

Coverage Gaps Emerge in Specific Wildfire Scenarios

Your standard policy covers direct flame damage, but significant gaps exist in wildfire situations. Landscaping damage, outdoor structures in certain high-risk areas, and damage from uncontrolled vegetation fires that don’t directly reach your home may fall outside your coverage. Additionally, if you fail to evacuate when ordered and suffer losses as a result, your insurer may deny the claim entirely. These gaps highlight why understanding your exact policy language matters before wildfire season arrives. Your agent can identify which specific perils your policy covers and which ones require additional endorsements or separate policies to address.

What Your Policy Won’t Cover When Wildfire Strikes

Your standard homeowners policy coverage for wildfire damage limitations and exclusions has real limits that catch many people off guard when a wildfire passes through their neighborhood. Vegetation fires that don’t directly reach your home but cause smoke, ash, or debris damage often fall outside coverage because your policy covers fire damage to structures and belongings, not ambient environmental harm. If a wildfire burns vegetation on adjacent properties and smoke seeps into your home for weeks, damaging walls and contents through exposure, your insurer may classify this as smoke damage from a fire that didn’t touch your property-a technical distinction that results in denial.

Smoke Damage from Nearby Fires Creates Coverage Confusion

The practical reality is that you need to review your policy’s specific language about what constitutes a covered fire peril. Ask your agent directly whether smoke damage from nearby fires qualifies or whether only direct flame contact triggers reimbursement. This distinction matters enormously in wildfire zones where smoke travels miles from the actual fire. Your policy language determines whether ambient smoke exposure receives coverage or falls into a gap that leaves you responsible for thousands in damage.

Landscaping and Vegetation Receive No Protection

Landscaping and vegetation on your property receive no coverage under standard homeowners insurance, even though these elements directly affect wildfire risk. If flames destroy mature trees, shrubs, and grass around your home, your policy won’t reimburse replanting or restoration costs. This gap forces homeowners to choose between accepting permanent landscape loss or paying out of pocket for restoration-a significant expense that compounds the financial impact of a wildfire event.

Detached Structures Face Limits in High-Risk Areas

Detached structures in high-risk areas present another coverage issue. While garages and sheds are typically covered, some insurers in California and other fire-prone regions impose separate limits or exclusions for these buildings, particularly if they’re located away from your main dwelling. You should verify with your agent whether your detached structures carry the same protection as your primary residence or whether they face reduced limits that could leave you underinsured.

Evacuation Order Violations Eliminate Coverage Entirely

If a mandatory evacuation order is issued and you choose to stay behind or return to your property prematurely without authorization, any losses you suffer may result in claim denial because you violated evacuation directives. Insurance companies view this as a failure to mitigate risk. The consequence is substantial: a house that catches fire while you remain inside despite evacuation orders could leave you completely uninsured for that loss.

Contact your local fire department before wildfire season to understand evacuation procedures in your area, and treat evacuation orders as absolute requirements for maintaining coverage. This step protects both your safety and your ability to recover financially after a wildfire. Understanding these coverage gaps positions you to take the next critical action: working with an independent agent who can identify which specific endorsements or additional policies address the vulnerabilities in your current coverage.

How to Secure the Right Coverage Before Wildfire Season

Work with an Independent Agent to Identify Coverage Gaps

An independent insurance agent serves as your strongest defense against coverage gaps that emerge during wildfire claims. Unlike captive agents who represent a single insurer, independent agents access multiple carriers and identify which policies offer wildfire protection tailored to your specific risk profile. When you meet with an agent, bring your current declarations page and ask three direct questions: Does my policy cover smoke damage from nearby fires, or only direct flame contact? What are my dwelling coverage limits compared to current rebuilding costs in my area?

Do I have replacement cost coverage, or does my policy use actual cash value?

The National Fire Protection Association notes that many homeowners carry replacement cost coverage for their dwelling but actual cash value for personal belongings, creating a dangerous mismatch where belongings receive only depreciated payouts. An agent can identify these misalignments and recommend endorsements like scheduled personal property coverage for high-value items such as jewelry, artwork, or electronics. They should also explain your deductible structure-standard deductibles typically run $500 to $1,000, but catastrophe deductibles in fire-prone areas can reach 2 to 5 percent of your home’s insured value (meaning a $500,000 home carries a $10,000 to $25,000 out-of-pocket cost after a wildfire claim). This calculation matters enormously when you evaluate whether your coverage is adequate.

Document Your Home’s Contents and Value Before Wildfire Season

A detailed home inventory transforms your claims process from guesswork into solid documentation. Photograph or video-record every room, closet, garage, and storage area, capturing items on shelves, in drawers, and hanging in closets. Include close-ups of serial numbers on electronics and appliances. Store receipts for major purchases alongside these records in a secure location outside your home-a cloud storage account, safe deposit box, or external hard drive kept at a relative’s house.

The National Association of Insurance Commissioners emphasizes that homeowners who maintain inventories resolve claims 40 percent faster than those submitting claims from memory. When documenting, note brand names and approximate purchase dates; your insurer will use this information to determine replacement cost. This preparation pays dividends when you file a claim and need to prove what you owned.

Create Defensible Space and Upgrade Fire-Resistant Features

Take concrete preventive steps that reduce wildfire risk and often qualify for insurance discounts. Create defensible space by removing dead trees and branches within 30 feet of your home, trimming tree branches 6 to 10 feet above ground level, and clearing gutters and roof valleys of pine needles and leaves. Replace wood mulch with gravel or rock in landscaping beds within 5 feet of structures, as wood mulch ignites easily from flying embers.

Install or upgrade to a Class A fire-rated roof, which the National Fire Protection Association identifies as the single most effective home-hardening measure. Ask your agent which specific mitigation measures your insurer rewards with premium discounts-some carriers offer 10 to 15 percent reductions for homes with defensible space and fire-resistant roofing. Document completed improvements with photographs and contractor receipts, then notify your agent so these upgrades can be reflected in your policy and potentially reduce your premiums.

Final Thoughts

Wildfire risk demands action before evacuation orders arrive. Your standard homeowners policy covers direct flame damage, smoke exposure, and temporary housing during evacuation, but significant gaps exist in most policies-landscaping damage, ambient smoke from nearby fires, and evacuation order violations fall outside coverage. Whether home insurance covers wildfires depends entirely on your specific policy language, coverage limits, and deductible structure, which could reach tens of thousands of dollars in a catastrophe scenario.

Review your declarations page immediately and contact your agent to confirm replacement cost coverage for both dwelling and personal belongings, verify your coverage limits against current rebuilding costs in your area, and understand your exact deductible structure. Create a detailed home inventory with photographs and receipts stored outside your home, then implement defensible space measures and fire-resistant upgrades that reduce risk and often qualify for premium discounts. These three actions position you to face wildfire season with actual protection rather than false confidence.

We at Direct Insurance Services work with multiple carriers to identify homeowners policies that address wildfire exposure in your specific situation. Contact Direct Insurance Services to discuss your wildfire coverage with an agent who understands your area’s fire season and can recommend solutions tailored to your home and budget.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation