Home Based Business Insurance: Complete Coverage Guide

Running a business from home exposes you to gaps that standard homeowners insurance simply won’t cover. Your equipment, client injuries, and liability claims need protection designed specifically for your operation.

At Direct Insurance Services, we’ve seen too many home-based business owners discover these gaps the hard way. This guide walks you through the coverage types you actually need and how to build a policy that matches your specific risks.

What Home-Based Business Insurance Actually Covers

The Coverage Gap Your Homeowners Policy Won’t Fill

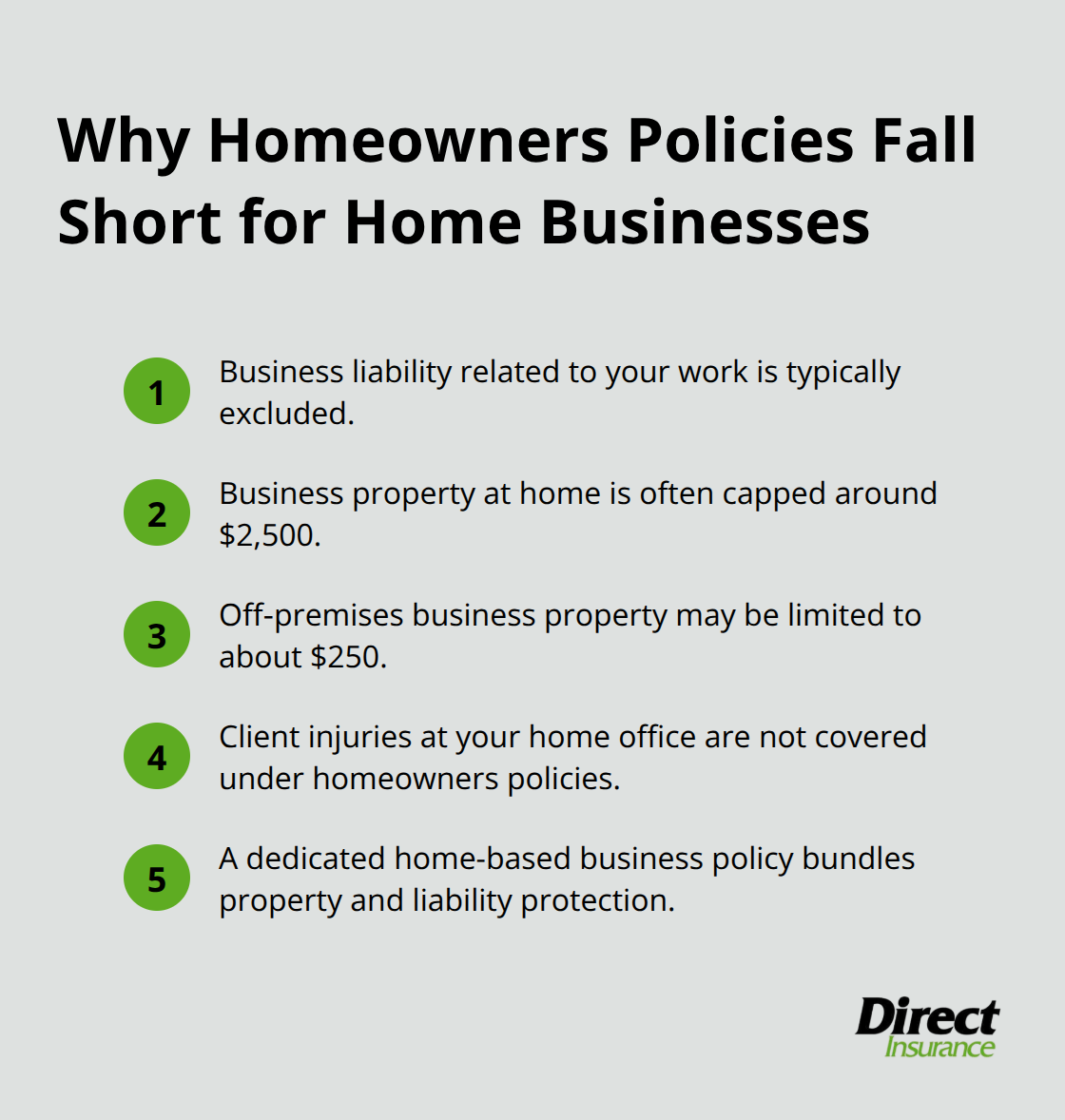

Home-based business insurance fills the protection gap that standard homeowners policies leave wide open. A typical homeowners policy provides only about $2,500 of coverage for business equipment at home and $250 off premises-nowhere near adequate for most operations. These policies exclude liability arising from business activities altogether. If a client visits your home office and suffers an injury, or if your business causes property damage, your homeowners insurance won’t protect you. Home-based business insurance addresses this by bundling property coverage for your equipment, inventory, and files with liability protection for claims made by clients or third parties.

Why Home-Based Businesses Face Unique Risks

The risks specific to home-based businesses differ fundamentally from traditional office environments. If clients visit your home to receive services-whether you’re a consultant, therapist, trainer, or contractor-you face premises liability exposure that a homeowners policy ignores. Equipment breakdown, cyber threats, and data breaches pose serious financial risks, especially if you handle client information or sensitive business documents. A home office fire that makes your living space uninhabitable can trigger coverage for additional living expenses under a business policy, whereas your homeowners policy may not address business income loss at all.

Who Faces the Greatest Vulnerability

Sole proprietors and independent contractors face particular vulnerability because they lack the liability protection built into corporate structures. If you have even one employee working from home, workers’ compensation becomes a legal requirement in most states once you cross certain thresholds, and your homeowners policy provides zero coverage for employee injuries. Standard policies also exclude business vehicles, so if you use a personal auto for client visits or deliveries, you’re driving without proper business coverage.

The Real Cost of Operating Without Proper Protection

The practical reality is that your homeowners insurance and personal auto policy were designed to protect your residence and family, not to shield a revenue-generating operation from the unique exposures it creates. Homebased businesses might require small business insurance since homeowners may not cover business needs. This explosive growth means millions of people operate without proper protection. The coverage your home-based business needs extends far beyond what standard policies offer, which is why understanding the specific types of protection available becomes essential as you assess your operation’s actual exposures.

Types of Coverage That Actually Protect Your Home Business

General Liability: Your First Line of Defense

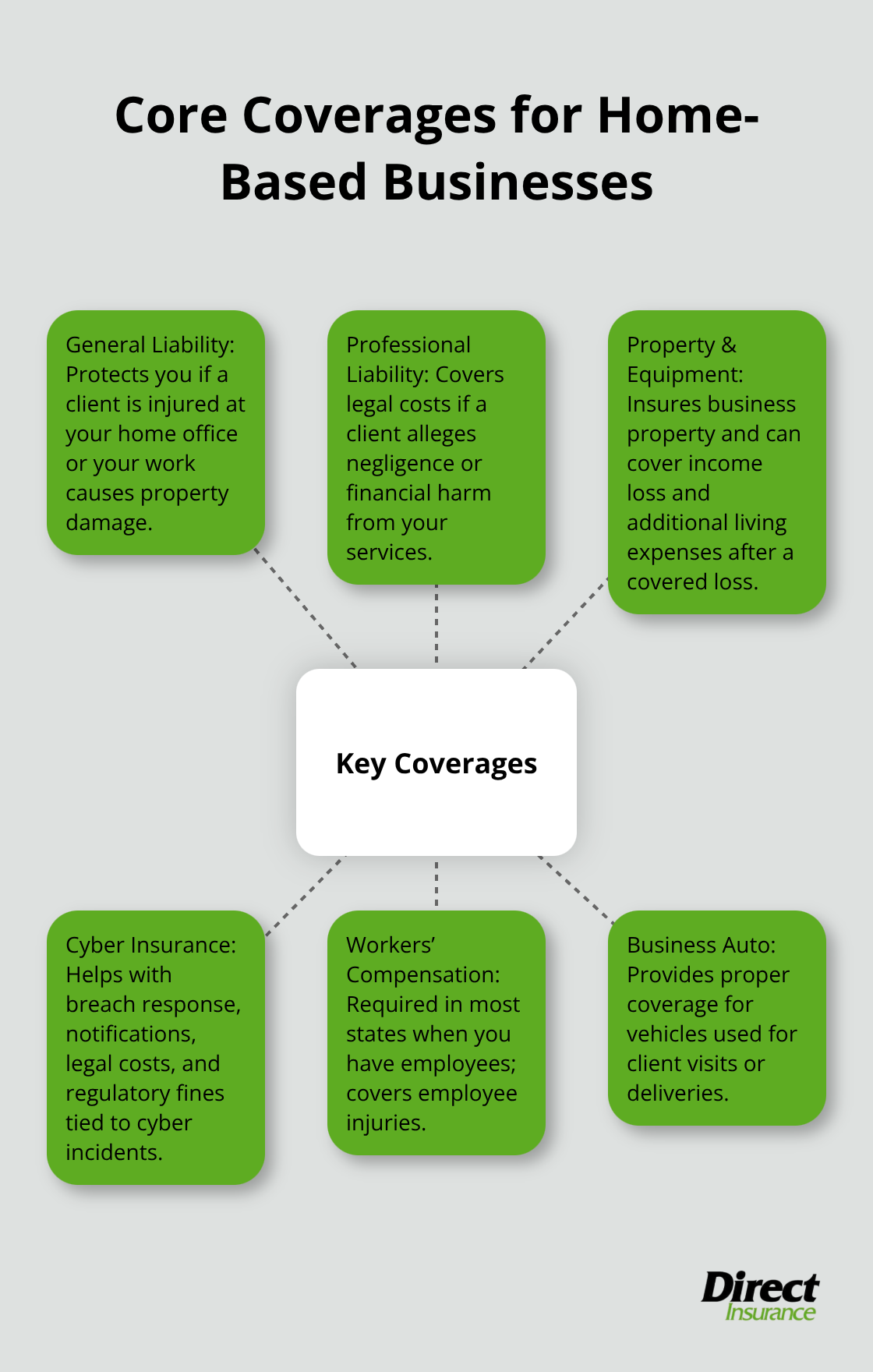

General liability insurance protects you from premises liability claims if a client slips in your home office, gets bitten by your dog, or suffers injury from your business activities. This coverage is non-negotiable for any home-based business where clients visit your property or where your work could injure someone. Typical general liability policies start around $300,000 to $1,000,000 in coverage limits and cost roughly $300 to $600 annually for home-based operations, according to industry data on small business insurance costs. If you’re a consultant, therapist, trainer, or contractor who meets with clients at home, this coverage protects your personal assets when liability claims arise.

Professional Liability for Service-Based Work

Professional liability insurance (also called errors and omissions) matters if your business involves providing advice or professional services. This coverage pays legal costs if a client sues for professional negligence or claims your work caused them financial harm. Service providers who handle client information or make recommendations face significant exposure without this protection.

Property and Equipment Coverage

Property and equipment coverage protects the physical assets that generate your income. A standard homeowners policy covers only about $2,500 of business equipment at home and $250 off premises, which falls short for most operations. An in-home business insurance policy typically costs under $300 per year and can insure business property around $10,000, making it affordable protection for your technology, files, and professional equipment. If a fire damages your home office and makes your space uninhabitable, a business policy covers additional living expenses while you rebuild, plus replaces your lost equipment and inventory. A Business Owners Policy bundles property and general liability coverage together, simplifying administration and often reducing costs compared to separate policies.

Cyber Insurance for Data-Heavy Operations

For technology-focused home businesses, cyber insurance becomes critical since data breaches and ransomware attacks expose you to notification costs, client lawsuits, and regulatory fines. This coverage protects your business when you handle sensitive client information or store valuable business data on your systems.

Workers’ Compensation and Vehicle Coverage

Workers’ compensation is legally required in most states once you hire employees, typically when you reach three or more workers (though some states have lower thresholds). Your homeowners insurance provides zero coverage for employee injuries, making a business workers’ compensation policy essential if you have staff. If you use a personal vehicle for business purposes like client visits or deliveries, your personal auto insurance likely excludes this use entirely. A separate business auto policy or business-use endorsement is necessary to avoid driving without proper coverage and facing personal liability for damages caused during business operations.

As your home-based business grows and your equipment investments increase, the question shifts from whether you need coverage to which policy structure fits your operation best. The next section walks you through assessing your specific business type and risk level to match the right protection to your actual exposures.

How to Choose the Right Policy for Your Home Business

Match Your Coverage to Revenue and Operations

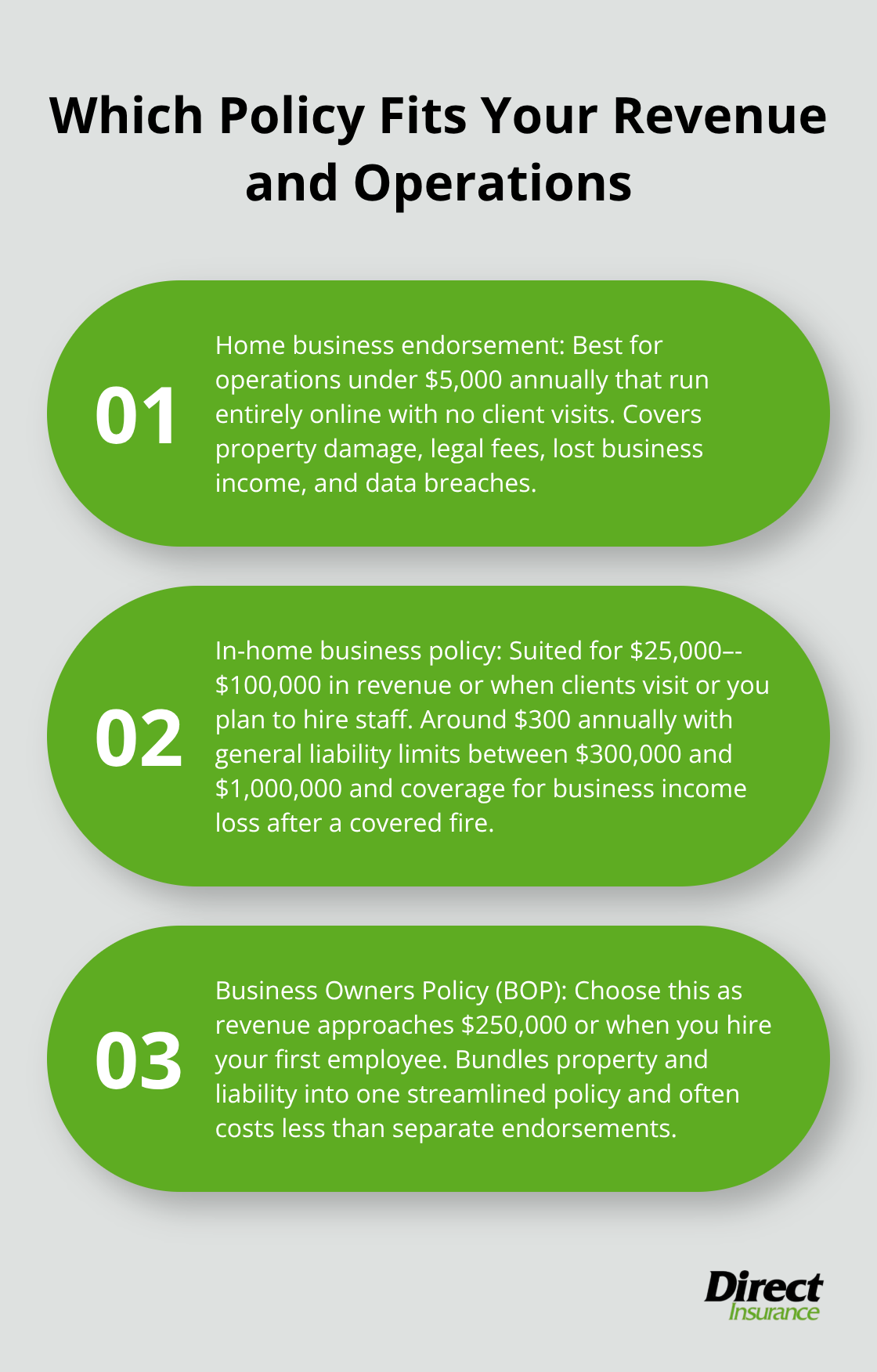

Your business structure determines which policy works best. If your operation generates less than $5,000 annually and operates entirely online with no client visits, a home business insurance endorsement covers property damage, legal fees, lost business income, and data breaches. However, if you earn $25,000 to $100,000 yearly, meet clients at home, or plan to hire staff, a dedicated in-home business policy at roughly $300 annually provides substantially better protection with general liability limits between $300,000 and $1,000,000 and coverage for business income loss if a fire makes your space uninhabitable.

The moment your revenue approaches $250,000 annually or you hire your first employee, a Business Owners Policy becomes the smarter choice because it bundles property and liability coverage into one streamlined policy, simplifying administration and often costing less than purchasing separate endorsements.

Calculate True Protection Value, Not Just Premium Cost

Cost comparisons matter, but comparing only premiums misses the real calculation. An annual cost of $300 to $600 for comprehensive home business coverage is genuinely inexpensive compared to a single liability claim that your homeowners policy won’t cover. Evaluate three specific scenarios for your business: first, what happens if a client injures themselves at your home office; second, what happens if equipment damage or theft disrupts your income for several weeks; and third, whether you could absorb the cost of a data breach if you handle client information. Your answers to these questions determine whether you need general liability, property coverage, cyber insurance, or all three.

Shop Multiple Carriers and Leverage Independent Agents

Request quotes from multiple carriers because premiums vary significantly based on business type and risk profile. An independent agent representing multiple insurers can show you these differences quickly rather than requiring you to contact each carrier separately, and they can identify which endorsements fill specific gaps in your coverage. State regulations affect what’s available in your area, so consulting a licensed professional who understands local requirements prevents purchasing inadequate coverage or discovering mid-claim that something you thought was covered actually isn’t.

Final Thoughts

Home-based business insurance fills a protection gap that standard homeowners policies simply cannot address. A single liability claim from a client injury or a data breach affecting your customers can cost tens of thousands of dollars, and without proper coverage, that financial burden falls entirely on you. The right policy structure depends on your revenue level, whether clients visit your home, and whether you plan to hire employees-an endorsement works for operations under $5,000 annually, an in-home business policy fits the $25,000 to $100,000 range, and a Business Owners Policy makes sense once you approach $250,000 in revenue or bring on staff.

At Direct Insurance Services, we work with multiple carriers to match your actual exposures to the right home-based business insurance policy. Our independent agency approach means we’re not locked into selling one company’s products-we can show you genuine options and explain which gaps matter most for your specific operation. We help clients throughout Utah navigate these decisions with personalized guidance rather than generic recommendations.

Contact Direct Insurance Services today to discuss your home-based business insurance needs and build a protection plan that lets you operate with confidence.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation