What Is the Average Home Insurance Cost?

Home insurance is one of the biggest expenses homeowners face each year. The average home insurance cost varies dramatically depending on where you live, what your home is worth, and the coverage you choose.

At Direct Insurance Services, we’ve seen firsthand how much premiums can differ from one state to another. This guide breaks down the real numbers and shows you practical ways to reduce what you pay.

What Drives Your Home Insurance Price

Your location is the single biggest factor determining what you pay for home insurance, and it’s not close. If you live in Oklahoma, you’re paying roughly $3,245 per year on average, while someone in Hawaii pays around $610 annually according to Matic data. That’s a five-fold difference for identical coverage levels. The reason is straightforward: some regions face more natural disasters, higher crime rates, and costlier rebuilding expenses.

Geographic Risk and Weather Exposure

Oklahoma City specifically averages $9,770 per year due to severe weather exposure. Meanwhile, San Jose, California sits at just $1,475 annually. Your zip code matters more than almost any other variable, which is why you need quotes from multiple carriers in your specific area. Roof condition has become surprisingly influential over the last few years. The premium gap between a newer roof and one that’s 11 to 15 years old jumped to about $155 in 2025, up from just $49 in 2022.

Roof Age and Claims Costs

Roof claims alone cost roughly $31 billion in 2024, nearly 30 percent higher than in 2022. Insurers now scrutinize roof age heavily during underwriting, and older roofs can disqualify you from standard carriers entirely. This forces you into the more expensive Excess and Surplus market, where coverage costs significantly more and protections are fewer.

How Your Home’s Value Affects Your Quote

The rebuild cost of your home determines your dwelling coverage amount, and this should never equal your purchase price. A home purchased for $256,000 might have a rebuild cost of just $180,000 or substantially more depending on square footage and construction. Using replacement-cost estimates of $150 per square foot gives you a realistic floor. If your policy lists dwelling coverage significantly higher than rebuild cost, you’re paying for protection you don’t need.

Personal Property and Deductible Strategy

Personal property coverage typically runs at 50 to 70 percent of dwelling coverage and should reflect what you actually own, not an inflated estimate. Your deductible directly controls your premium: increasing from $1,000 to $2,500 typically saves around 9 percent annually. However, try a deductible you can actually afford to pay out of pocket when a claim occurs, or you’ll face financial hardship during the worst moment. Understanding these cost drivers positions you to make smarter decisions about coverage levels and deductible amounts.

What You’ll Actually Pay Across America

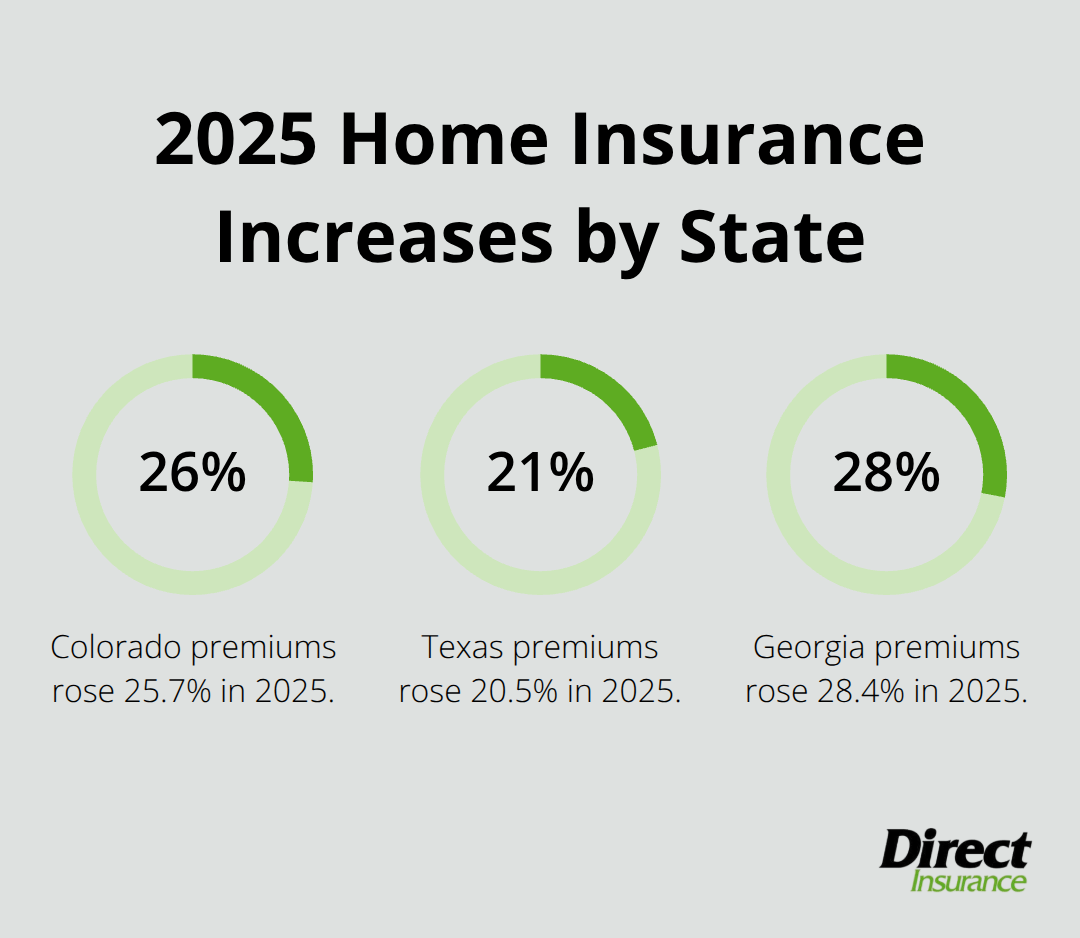

The national average for home insurance sits around $1,952 annually according to Matic data from 2025, but this number masks the reality that your actual cost depends almost entirely on where you live. Oklahoma averages $3,245 per year while Hawaii costs just $610-a spread so wide that it makes the national average nearly meaningless for planning purposes. Colorado saw premiums jump 25.7 percent in 2025 alone, with new policies running about $666 higher than the previous year. Texas experienced a 20.5 percent increase, and Georgia hit 28.4 percent. These aren’t minor adjustments; they represent structural shifts in how insurers price risk.

State-by-State Variation Tells the Real Story

State-by-state variation reveals that your zip code matters far more than national statistics suggest. New York premiums climbed 23 percent in 2025, and Mississippi saw a 19.4 percent jump. Meanwhile, states with lower disaster frequency keep rates substantially lower. The variation isn’t random-it reflects actual loss history and future risk. If you’re comparing quotes from different states or considering a move, expect your premium to swing dramatically based on local climate exposure, building costs, and insurer availability rather than any universal formula.

Urban Areas Often Cost Less Than You’d Expect

Within states, urban and rural areas diverge significantly because urban locations typically have better fire protection services, lower crime rates, and faster emergency response times. San Jose sits at $1,475 annually while nearby rural areas cost considerably more. Oklahoma City residents pay $9,770 per year, roughly three times the state average, due to severe weather exposure and hail risk concentrated in metro areas. This urban advantage disappears entirely in states prone to wildfires or hurricanes, where rural properties sometimes qualify for standard coverage while urban properties get pushed into the expensive Excess and Surplus market.

The Excess and Surplus Market Changes Everything

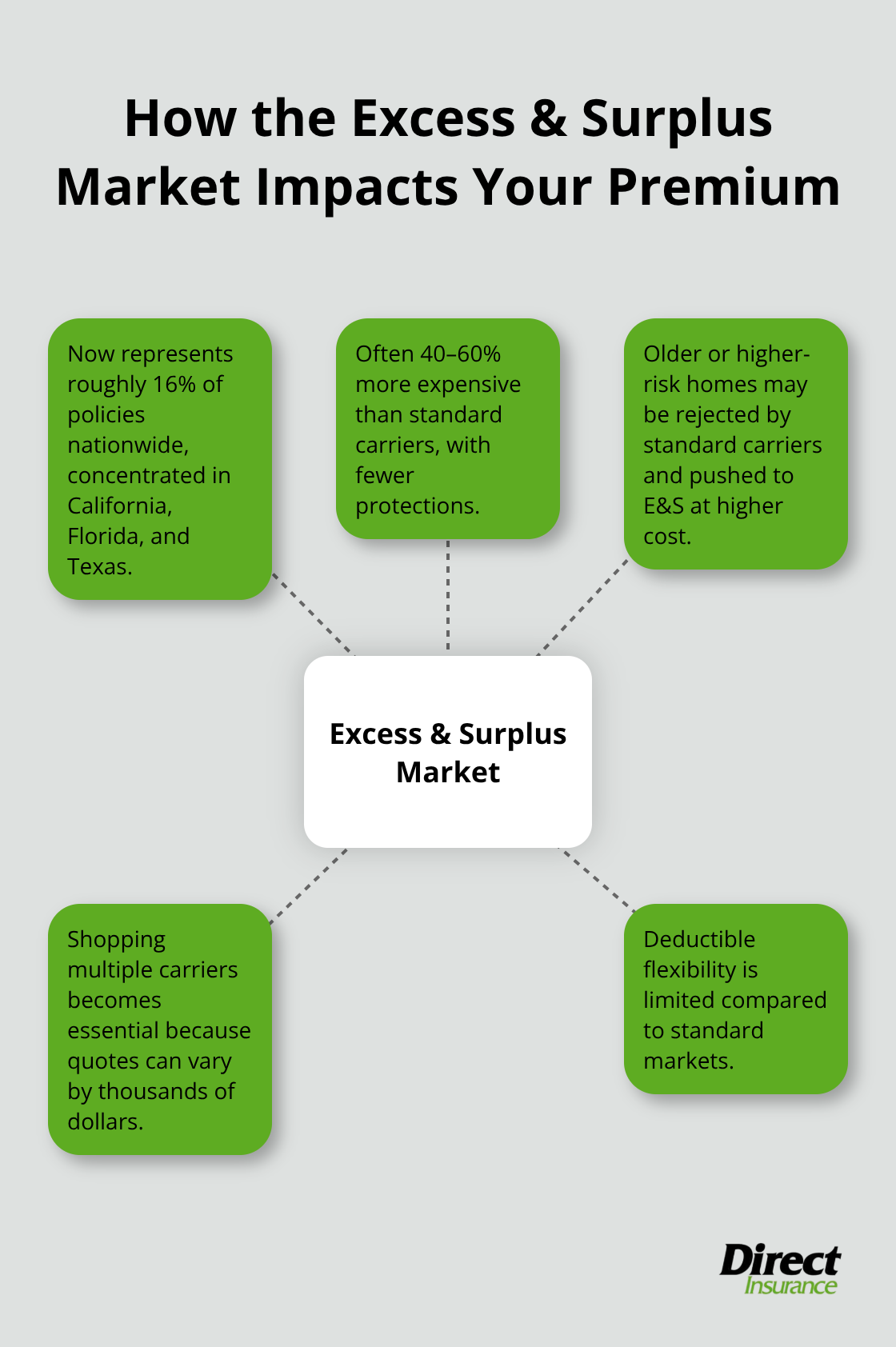

Coverage availability shifted dramatically in 2025, with the Excess and Surplus market now representing roughly 16 percent of policies nationwide, concentrated in California, Florida, and Texas. These non-admitted carriers charge substantially more (sometimes 40 to 60 percent above standard rates) while offering fewer protections and less flexibility on deductibles. If you live in a high-risk state and standard carriers reject your application, you’ll end up paying significantly more with fewer options.

Shopping across multiple carriers becomes mandatory in these states because your premium could differ by thousands of dollars depending on which company takes your risk. Understanding these regional dynamics helps you anticipate what you’ll actually pay and prepares you to shop strategically when rate increases hit your renewal notice.

Cut Your Premium Without Cutting Coverage

Bundle Policies to Unlock Immediate Savings

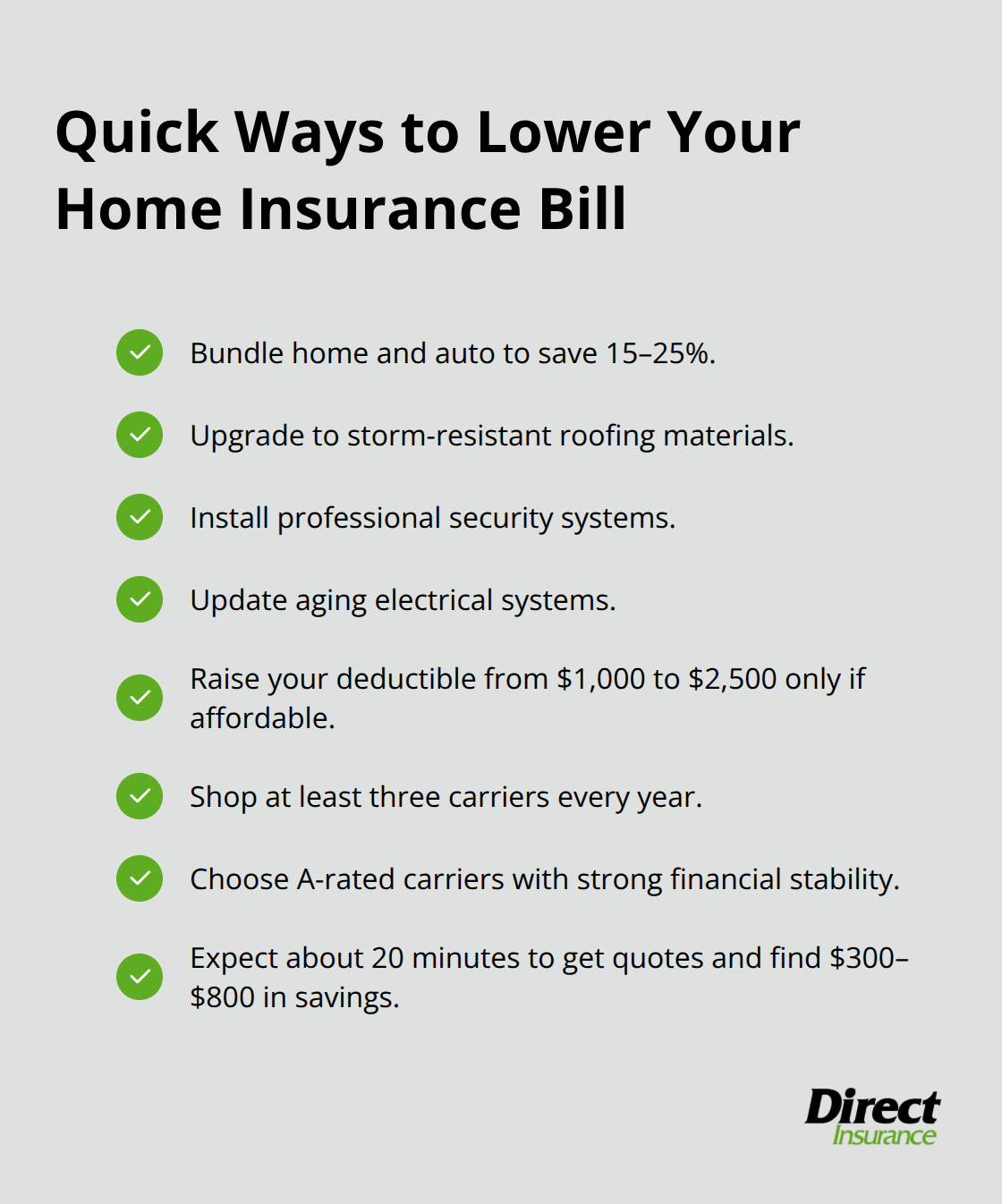

Reducing your home insurance bill doesn’t require accepting worse coverage or taking on unreasonable risk. The most effective strategies focus on what insurers actually reward: lower deductibles paired with other policies, measurable home improvements, and honest assessment of how much coverage you genuinely need. Bundling your home and auto policies typically saves 15 to 25 percent on your combined premium according to industry data, which means a homeowner paying $2,000 annually could save $300 to $500 just by consolidating with one carrier. The math is straightforward: insurers charge less when they manage multiple policies for the same household because the acquisition cost drops and retention improves. More importantly, bundling forces you to shop your entire insurance portfolio at once, which prevents the common mistake of keeping an outdated home policy while updating auto coverage elsewhere.

Invest in Home Improvements That Lower Risk

Beyond bundling, roof condition now dominates underwriting decisions more than almost any other factor. Storm-resistant roofing materials, updated electrical systems, and professional security systems all generate concrete discounts because insurers have loss data showing these improvements reduce claims frequency. These upgrades transform your property into a lower-risk investment from an insurer’s perspective, which translates directly into lower premiums.

Choose a Deductible You Can Actually Afford

Increasing your deductible from $1,000 to $2,500 saves approximately 9 percent annually, but this strategy only works if you can actually cover that deductible from emergency savings without hardship. Too many homeowners raise deductibles to lower premiums, then face financial crisis when a claim occurs because they cannot afford the out-of-pocket cost. The real premium reduction comes from combining all three approaches: bundling policies with one carrier, making genuine home improvements that lower your risk profile, and selecting a deductible level you can comfortably pay.

Shop Multiple Carriers Every Year

Shopping annually across at least three carriers matters more in 2025 than ever before because rate increases hit different companies at different times. Each carrier weights roof age, location risk, and claims history differently, so a quote jump at your current insurer does not mean the entire market raised rates. Coverage availability shifted so dramatically in 2025 that standard carriers now reject applicants who would have qualified two years ago, pushing them into the expensive Excess and Surplus market where premiums run 40 to 60 percent higher. This means if you have not shopped in 12 months, you may not know whether better options exist or whether you have been involuntarily shifted into a riskier market segment. Getting quotes from multiple carriers takes roughly 20 minutes online and typically reveals $300 to $800 in annual savings compared to renewal notices from existing insurers. The carriers you receive quotes from matter less than ensuring they carry A-ratings with strong financial stability, which filters out undercapitalized insurers that might deny claims when you need them most.

Final Thoughts

Your average home insurance cost reflects decisions you control and factors beyond your reach. Location, roof condition, and home value establish your baseline premium, while bundling policies, making home improvements, and selecting the right deductible directly reduce what you pay. Shopping multiple carriers annually prevents overpaying and catches rate increases before they hit your renewal notice.

The most effective strategy combines three actions: bundle your home and auto policies with one carrier to save 15 to 25 percent, invest in measurable home improvements like storm-resistant roofing that insurers reward with concrete discounts, and increase your deductible only if you can afford the out-of-pocket cost. Getting quotes from at least three carriers takes roughly 20 minutes and typically reveals $300 to $800 in annual savings compared to your renewal premium. Do not accept the first quote or assume your current insurer offers the best rate.

Contact Direct Insurance Services to get personalized quotes and expert advice tailored to your situation. Our team works with top-rated carriers to help you find coverage that fits your actual needs and budget without pressure or unnecessary add-ons. Whether you shop for the first time or review a renewal notice that shocked you, we provide clear guidance on coverage levels, deductible options, and bundling opportunities.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation