How Much Auto Insurance Do You Really Need?

Most drivers ask themselves “How much auto insurance do I need?” when shopping for coverage. The answer depends on your specific situation, not just state requirements.

We at Direct Insurance Services see many people either overpaying for unnecessary coverage or leaving themselves financially vulnerable with too little protection.

This guide breaks down the key factors that determine your ideal coverage levels and helps you make an informed decision.

What Does Utah Require for Auto Insurance

Utah mandates specific minimum coverage amounts that every driver must carry, but these state minimums often fall short of real-world protection needs. The current requirements include $25,000 for bodily injury per person, $65,000 for bodily injury per accident, and $15,000 for property damage. Personal injury protection coverage of $3,000 is also mandatory, along with uninsured motorist coverage that matches your liability limits.

State Minimums vs Real Protection Needs

These minimum amounts might seem adequate until you face an actual claim. The average bodily injury liability claim reached $26,501 in 2023, which already exceeds Utah’s per-person minimum. Property damage costs for newer vehicles easily surpass the $15,000 minimum requirement. Medical expenses from serious accidents can reach six figures, which makes the $3,000 PIP requirement insufficient for major injuries.

Financial Responsibility Beyond Minimums

Utah’s financial responsibility law allows alternatives to traditional insurance, such as depositing $160,000 with the state treasurer or obtaining a surety bond. However, most drivers find standard insurance more practical and cost-effective. The state monitors compliance through electronic verification systems, and violations result in license suspension, registration revocation, and reinstatement fees that exceed $600.

Coverage Gaps Create Financial Risk

Smart drivers recognize that meeting minimum requirements protects against legal penalties but leaves significant financial gaps when accidents occur. Your personal assets become vulnerable when damages exceed your policy limits. A single accident can wipe out savings, threaten home ownership, and impact future earnings through wage garnishment (if you’re found liable for damages beyond your coverage).

Understanding these limitations helps you evaluate what additional protection makes sense for your specific situation and asset level.

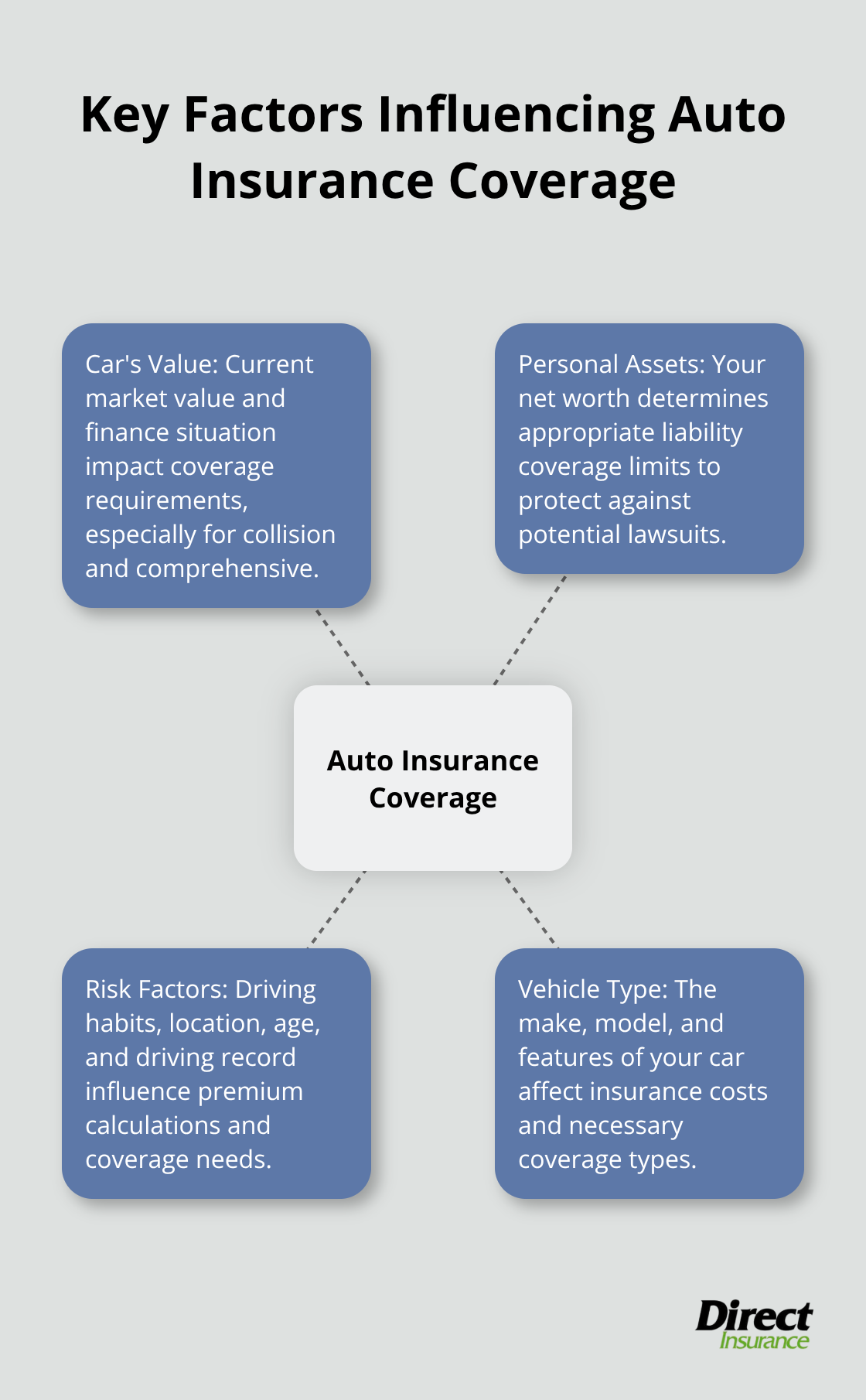

What Factors Should Drive Your Coverage Decisions

Your car’s current value and finance situation directly impact coverage requirements. Lenders typically demand collision and comprehensive coverage until you pay off the loan, which protects their investment in your vehicle. Once you own the car outright, evaluate whether these coverages make financial sense based on the vehicle’s market value. A car worth $5,000 might not justify $1,200 in annual comprehensive and collision premiums with a $500 deductible.

Your Assets Determine Liability Limits

Calculate your net worth (home equity, retirement accounts, and savings included) to determine appropriate liability coverage. If you own assets worth $250,000, Utah’s $25,000 minimum per-person coverage leaves $225,000 exposed to lawsuits. Umbrella policies provide additional liability protection that starts at $1 million increments for roughly $200-400 annually. High earners face greater lawsuit risk since attorneys target defendants with deeper pockets and future income potential.

Risk Factors Shape Premium Calculations

Insurance companies analyze your driving habits and personal risk factors when they set rates. Urban drivers pay more due to higher accident frequencies and theft rates compared to rural areas. Your record over the past three to five years heavily influences prices, with at-fault accidents and violations that increase premiums by 20-40% or more. Age demographics also matter – drivers under 25 and over 65 typically face higher rates due to statistically higher claim frequencies.

Vehicle Type Affects Coverage Costs

Sports cars, luxury vehicles, and trucks with high repair costs command higher premiums than economy models. Theft-prone vehicles also cost more to insure comprehensively. Safety features like anti-lock brakes, airbags, and electronic stability control can reduce rates through available discounts.

These coverage factors work together to create your unique insurance profile, which leads directly into the specific types of protection you should consider beyond basic liability coverage.

Which Coverage Types Protect You Best

Collision coverage pays for your vehicle’s damage when you hit another car or object, regardless of fault. This protection becomes worthless when your car’s value drops below the annual premium cost plus deductible. Drop collision coverage when your vehicle’s market value falls under $4,000, since a total loss payout minus your deductible rarely justifies the expense.

Comprehensive Coverage for Non-Collision Damage

Comprehensive coverage handles theft, vandalism, weather damage, and animal strikes. This coverage makes sense for vehicles parked outdoors or in high-crime areas, but skip it for older cars stored in garages where replacement costs exceed coverage benefits. Weather-related claims account for roughly 76% of comprehensive losses, with hail damage alone costing insurers billions annually.

Uninsured Motorist Coverage Fills Critical Gaps

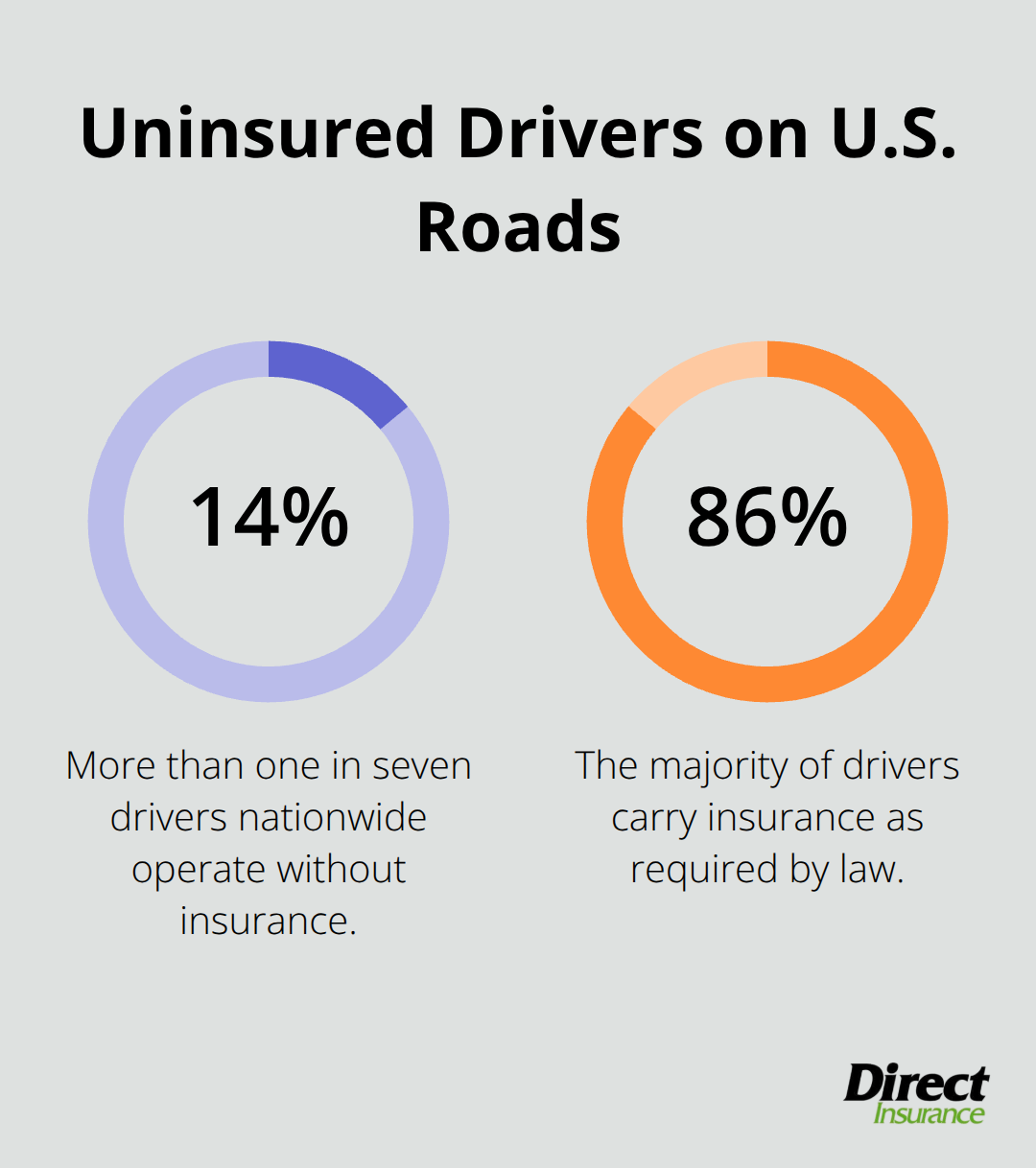

Uninsured and underinsured motorist protection covers your medical bills and vehicle damage when the at-fault driver lacks adequate insurance. Utah requires this coverage to match your liability limits, which creates a safety net when accidents involve drivers with insufficient protection. The Insurance Research Council reports that more than one in seven drivers nationwide operates without insurance, making this coverage essential rather than optional. Underinsured motorist coverage activates when the other driver’s limits fall short of your damages.

Medical Coverage Reduces Out-of-Pocket Expenses

Personal injury protection covers medical expenses, lost wages, and essential services regardless of fault in the accident. Utah’s $3,000 minimum PIP requirement covers basic emergency room visits but falls short for serious injuries that require surgery or extended treatment. Medical payments coverage works similarly but excludes lost wages and typically costs less than PIP. Choose higher PIP limits if your health insurance carries high deductibles or copays, since PIP pays primary and reduces your medical expenses immediately after accidents.

Gap Insurance Protects Against Depreciation

Gap insurance pays the difference between your car’s actual cash value and your loan balance when your vehicle gets totaled. New cars lose 20% of their value within the first year, which creates a coverage gap that standard policies won’t fill. This protection matters most for drivers who finance vehicles with small down payments or lease agreements.

Final Thoughts

The question “How much auto insurance do I need?” requires you to balance adequate protection with affordable premiums. Start with coverage that protects your assets, then adjust based on your vehicle’s value and financial situation. Most Utah drivers benefit from liability limits well above state minimums, especially when serious accidents generate costs far exceeding $25,000 per person.

An independent agent simplifies this complex decision process for you. We at Direct Insurance Services work with multiple top-rated carriers to find coverage that fits your specific needs and budget. Our personalized approach means you receive tailored solutions rather than generic policies that might leave gaps in protection or waste money on unnecessary coverage.

Review your policy annually or after major life changes (like home purchases, marriage, or loan payoffs). Your insurance needs evolve as your financial situation changes, and regular reviews help you maintain optimal coverage levels while you control costs. The right coverage protects your financial future without it breaks your budget today.