Does Your Landlord Insurance Cover Tenant Evictions?

As landlords, protecting your investment is paramount. At Direct Insurance Services, we often hear the question: “Does landlord insurance cover eviction?” It’s a critical concern for property owners facing the challenging process of removing problematic tenants.

Let’s explore the intricacies of landlord insurance and how it relates to eviction coverage, ensuring you’re well-informed to safeguard your rental property.

What Does Landlord Insurance Actually Cover?

Property Protection

Standard landlord insurance policies typically include two different types of coverage: property and liability protection. The property protection covers the physical structure of your rental property against perils like fire, wind, hail, and vandalism. This protection extends to permanent fixtures and fittings, such as built-in appliances and carpeting. However, it’s important to note that flood and earthquake damage usually require separate policies.

Liability Coverage

Another key component is liability protection. This covers legal expenses and medical costs if a tenant or visitor sustains an injury on your property due to negligence. For example, if someone slips on an icy walkway you failed to salt, your policy could cover the resulting lawsuit.

Loss of Rental Income

Many landlords overlook this vital aspect. If your property becomes uninhabitable due to a covered event (like a fire), your policy may reimburse you for lost rent during repairs. This can provide a financial safety net, especially for those who rely on rental income to cover mortgage payments.

What’s Not Covered

It’s equally important to understand what standard policies don’t cover. Eviction costs, for instance, are typically excluded.

According to the National Apartment Association, the average eviction can cost between $3,500 and $10,000 (accounting for legal fees, lost rent, and property turnover expenses).

Tenant’s personal property is also not covered under your policy. We recommend that you encourage your renters to obtain their own renters insurance to protect their belongings.

The Importance of Policy Review

Insurance needs can change as your property portfolio grows or local regulations evolve. An annual review of your policy will ensure it still meets your needs. This proactive approach can prevent costly coverage gaps.

For example, if you’ve recently upgraded your rental with high-end appliances or added a pool, your current coverage limits may no longer suffice. Similarly, if you’ve started offering short-term rentals, your policy may need adjustments to maintain proper protection.

As we move forward, it’s essential to consider how landlord insurance addresses specific scenarios, such as tenant evictions. Let’s explore this topic in more detail in the next section.

Does Landlord Insurance Cover Eviction Costs?

Eviction presents a challenging and often costly process for landlords. While standard landlord insurance policies typically don’t cover eviction expenses, options exist to protect yourself financially during this difficult situation.

Legal Expenses Coverage

Some insurers offer legal expenses coverage as an add-on to your landlord policy. This can help offset the costs associated with eviction proceedings, including attorney fees and court costs. The low-end average cost of eviction in legal fees is $500. Legal expenses coverage can significantly reduce this financial burden.

We’ve observed an increasing number of landlords opt for this additional protection. Coverage limits typically range from $5,000 to $25,000, so it’s important to assess your potential needs when choosing a policy.

Loss of Rent Coverage

Landlords often face a loss of rental income while evictions progress. Some specialized landlord policies offer coverage for lost rent during the eviction process. However, this is not standard and usually comes with strict conditions.

For instance, many policies only cover lost rent if the eviction results from property damage that makes the unit uninhabitable. Evictions due to non-payment or lease violations may not receive coverage. It’s important to carefully review policy terms and discuss your specific needs with your insurance provider.

Additional Coverage Options

Landlords should consider additional coverage options to protect against eviction-related damages. These may include:

- Malicious damage coverage: This protects against intentional damage caused by tenants (unfortunately common during evictions).

- Vandalism protection: Some policies extend coverage to include damage caused by vandals during the eviction process.

- Clean-up costs: Certain insurers offer coverage for cleaning and debris removal after an eviction, which can be substantial if the property was left in poor condition.

When selecting additional coverage, it’s important to weigh the cost against the potential risks.

Every landlord’s situation is unique. We recommend working closely with your insurance provider to assess your specific risks and identify appropriate coverage options. Tailoring your insurance package to include eviction-related protections can significantly reduce the financial impact of this challenging process.

The best defense against eviction costs remains prevention. Thorough tenant screening, clear lease agreements, and prompt communication can help minimize the likelihood of evictions. However, the right insurance coverage provides an essential safety net when prevention isn’t enough.

As we move forward, it’s important to understand how various factors can affect your eviction coverage. Let’s explore these elements in the next section to ensure you have a comprehensive understanding of your policy’s protections.

What Impacts Your Eviction Coverage?

State and Local Eviction Laws

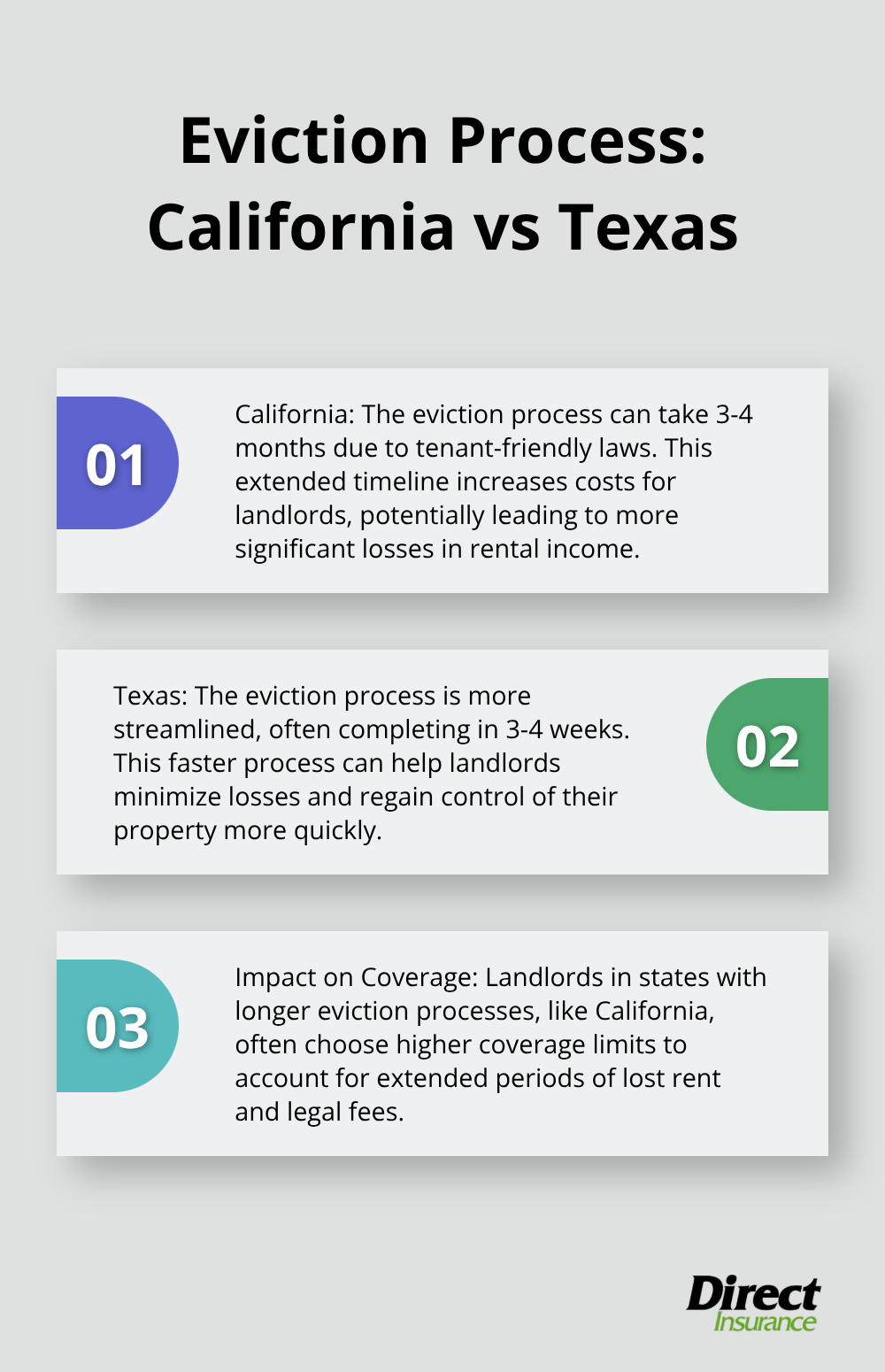

Eviction laws differ across states and local jurisdictions. These laws affect both the eviction process and your insurance coverage. In California, the eviction process can take 3-4 months due to tenant-friendly laws, which increases costs for landlords. Texas, however, has a more streamlined process, often completing evictions in 3-4 weeks.

Landlords in states with longer eviction processes often choose higher coverage limits to account for extended periods of lost rent and legal fees. You should familiarize yourself with your local laws and adjust your coverage accordingly.

Lease Agreement Specifics

Your lease agreement determines the strength of your eviction case and, consequently, your insurance coverage. A well-drafted lease outlines grounds for eviction clearly, which makes it easier to prove your case in court and potentially reduces legal costs.

Work with a legal professional to craft a comprehensive lease agreement. Include specific clauses about rent payment deadlines, property maintenance expectations, and prohibited activities. This clarity can streamline the eviction process if needed and may impact your insurance premiums favorably.

Reasons for Eviction

The reason behind an eviction affects your insurance coverage. Most policies distinguish between evictions due to non-payment of rent and those resulting from property damage or illegal activities.

Evictions due to non-payment are often not covered under standard policies. However, if you evict a tenant for causing significant property damage, your policy may cover both the eviction costs and the repairs needed.

Some insurers offer specialized coverage for high-risk scenarios. If you operate in an area with a history of problematic tenants, discuss additional protection options with your insurance provider.

Tenant Screening Processes

Implementing thorough tenant screening processes can significantly reduce the likelihood of evictions. Use comprehensive background checks and credit reports to vet potential tenants. This proactive approach can help you avoid problematic tenants and potentially lower your insurance premiums.

Policy Limits and Deductibles

Your policy limits and deductibles play a significant role in your eviction coverage. Higher limits provide more protection but come with higher premiums. Lower deductibles mean you pay less out-of-pocket during a claim, but they typically result in higher monthly costs.

Review your policy limits and deductibles annually to ensure they align with your current needs and risk tolerance. Consider factors such as the value of your property, local eviction laws, and your financial situation when setting these amounts.

Some landlord insurance policies may also cover lost rental income if your property becomes uninhabitable, providing additional financial protection during challenging times.

Final Thoughts

Landlord insurance policies do not automatically cover eviction costs. You must review your current policy and identify protection gaps. Add-ons like legal expenses coverage or loss of rent protection during evictions can provide essential financial safeguards.

Strong preventive measures minimize eviction risks. Conduct thorough tenant screenings, maintain clear communication, and create comprehensive lease agreements. Even with the best precautions, evictions can still occur, making proper insurance coverage vital.

We at Direct Insurance Services understand the unique challenges landlords face. Our experienced team can help you navigate landlord insurance intricacies (including eviction coverage). We offer tailored solutions that fit your specific needs and budget, ensuring your rental property investments remain protected.