Landlord Insurance vs Homeowners Insurance: Key Differences

Many property owners in Utah don’t realize that landlord insurance and homeowners insurance serve completely different purposes. The difference between landlord insurance and homeowners insurance comes down to who lives in the property and what risks need protection.

At Direct Insurance Services, we help property owners understand which policy actually fits their situation. Choosing the wrong type of coverage can leave you exposed to significant financial losses.

What Landlord Insurance Actually Covers

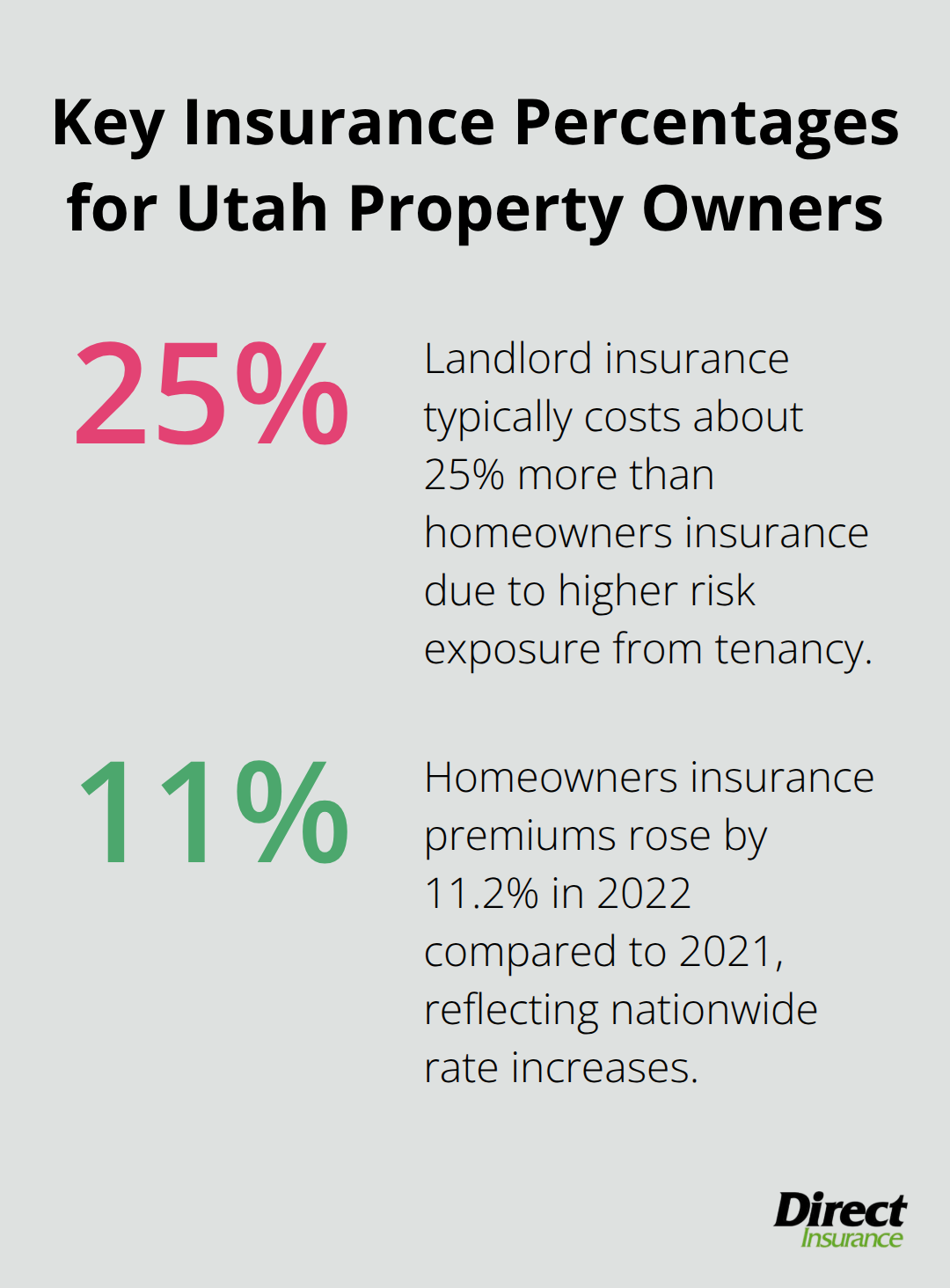

Landlord insurance protects the structure of your rental property and your income from tenants. Unlike homeowners insurance, which covers your personal belongings inside the home, landlord insurance focuses on the building itself, any detached structures like sheds or garages, and liability claims from tenants or their guests. The Insurance Information Institute reports that landlord insurance typically costs about 25% more than homeowners insurance because rental properties carry higher risk exposure. When a tenant causes damage to the property or someone gets injured on the premises, landlord insurance handles the liability protection and medical payments. Loss of rental income coverage replaces your lost monthly income so you can still pay your bills during repairs. If a covered event like fire or windstorm makes the property uninhabitable, this coverage protects your cash flow during a critical period. Most landlords find this component invaluable because rental income often covers mortgage payments, property taxes, and maintenance costs.

Understanding Your Liability Exposure as a Landlord

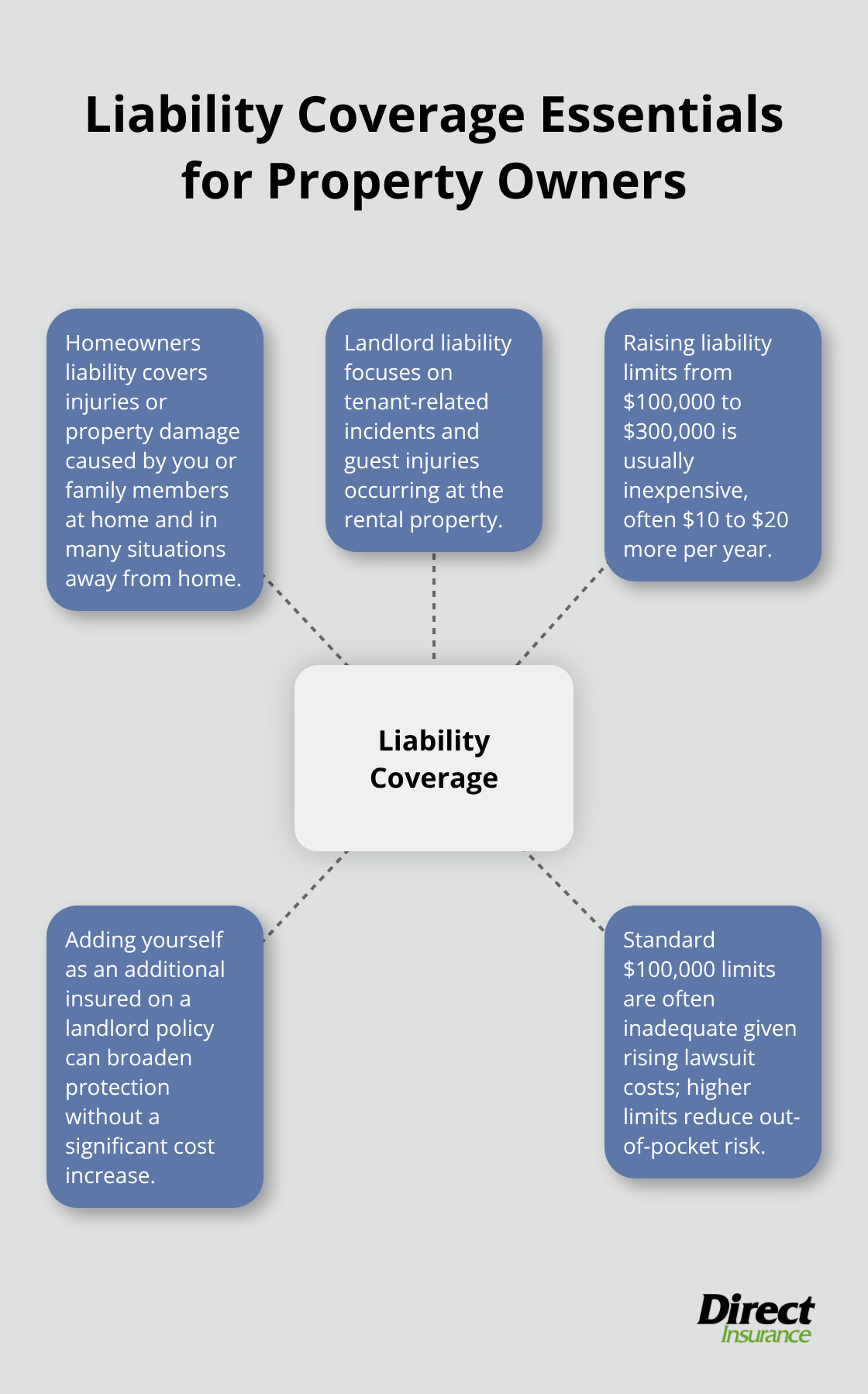

Tenants and their guests create liability risks that homeowners policies don’t address. If someone is injured on your rental property and you’re found liable, landlord insurance covers medical payments and legal defense costs. The coverage typically includes bodily injury and property damage liability, with standard limits around $100,000 to $300,000, though you can increase these limits. Many landlords overlook adding themselves as an additional insured on the policy, which can expand protection without significant cost increases. You should also know that landlord insurance does not cover your tenants’ personal belongings-that’s their responsibility through renters insurance, which most landlords require as a lease condition.

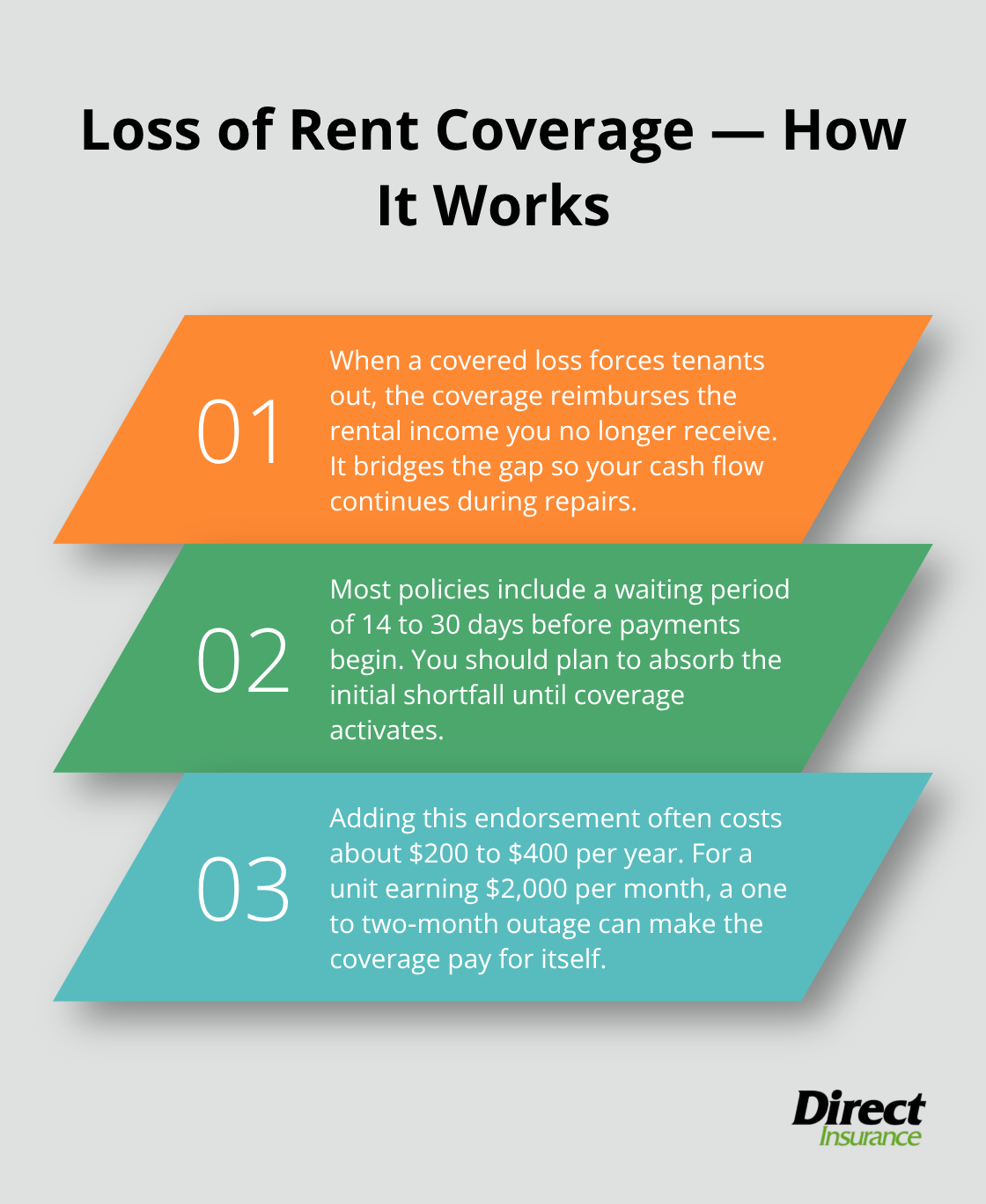

What Loss of Rent Coverage Actually Does

Loss of rent coverage reimburses you when rental income stops due to a covered loss. If a fire damages the rental unit and tenants must move out for three months of repairs, this coverage pays your lost rent. The typical waiting period is 14 to 30 days after the loss occurs, so you absorb initial losses before coverage kicks in.

Based on real quotes, adding loss of rent coverage might increase your annual premium by $200 to $400, depending on your property value and rental income. For a property that generates $2,000 monthly rent, this endorsement pays for itself in just one or two months of lost income, making it a practical investment for most landlords.

How Landlord Insurance Differs from Your Current Homeowners Policy

Your homeowners policy covers your personal belongings and provides loss of use coverage (additional living expenses if you must relocate temporarily). Landlord insurance replaces that with loss of rent coverage instead, since you won’t be living in the property. The dwelling coverage works similarly in both policies, but the liability exposure differs significantly. Rental properties attract more foot traffic and longer occupancy periods, which increases injury risk and property damage claims. This higher risk exposure explains the 25% premium increase that landlords typically face compared to homeowners insurance rates.

Taking the Next Step with Your Coverage

Understanding what landlord insurance covers is the first step toward protecting your rental investment. The specific coverage limits, deductibles, and endorsements you select will depend on your property’s value, location, and rental income. Utah property owners should compare quotes from multiple carriers to find the right balance between protection and cost. Your next decision involves determining which specific coverage options-particularly loss of rent protection-matter most for your financial situation.

What Homeowners Insurance Protects

Homeowners insurance covers your owner-occupied home, the structures attached to it, and your personal belongings inside. Unlike landlord insurance, which protects rental income and tenant-related risks, homeowners insurance focuses on protecting your family’s assets and your own liability exposure. According to the Insurance Information Institute, the average homeowners policy costs around $1,754 per year, though Utah rates vary based on location, home age, and construction type. The policy covers the dwelling structure itself, detached structures like garages or sheds, and your personal property up to a certain limit-typically 50% to 70% of your home’s value for items stored outside the house. If a fire, windstorm, or other covered peril damages your home, the insurance pays for repairs or rebuilding. Your belongings inside the home receive coverage up to your policy limits, which means you need to select limits that actually reflect what you own. Most homeowners underestimate their possessions and choose limits too low, leaving themselves short when they file a claim. The liability portion protects you and your family members if someone is injured on your property or if you accidentally damage someone else’s property-coverage that applies both at home and away from home in certain situations.

Personal Property Coverage Protects Your Belongings

Your homeowners policy covers personal property coverage including furniture, electronics, clothing, and other belongings you own inside the home. The coverage limit matters more than most people realize because replacement costs have climbed significantly. A typical living room setup with a sofa, entertainment system, and furniture can easily exceed $10,000, and that’s before adding bedrooms, kitchens, and outdoor equipment. If you own high-value items like jewelry, art, or collectibles, standard homeowners coverage has sublimits-often $1,500 to $2,500 for jewelry alone. You can add scheduled personal property endorsements to cover these items at full replacement value, though this costs extra. The deductible you choose affects your premium directly; raising it from $500 to $1,000 can save around $200 to $300 annually, but you must be prepared to pay that amount out of pocket when you file a claim. Utah homeowners should inventory their belongings and photograph valuable items, which makes the claims process faster and helps you select appropriate coverage limits. Loss of use coverage included in your policy pays for temporary housing, meals, and other expenses if a covered loss makes your home uninhabitable during repairs-a protection that renters and landlords do not receive.

Liability Coverage Protects You From Lawsuits

Your homeowners policy includes liability coverage that protects you if someone is injured at your home or if you accidentally injure someone or damage their property elsewhere. Standard policies typically offer $100,000 to $300,000 in liability coverage, though you can increase these limits for a modest premium increase. If a guest slips on your icy driveway and breaks their leg, or if your dog bites a neighbor, liability coverage pays their medical bills and legal costs if they sue. Medical payments coverage, separate from liability, pays up to $5,000 (or your chosen limit) for injuries to others without a lawsuit-a practical feature that often resolves disputes quickly. Many Utah homeowners do not realize that liability coverage extends beyond the home to activities away from your property, covering incidents involving your family members. If your teenager accidentally damages a neighbor’s fence or a family member injures someone at a park, the policy typically covers those situations. Increasing your liability limits from $100,000 to $300,000 costs only $10 to $20 more per year, making it a smart investment for minimal expense. You should review your coverage limits every few years because property values and lawsuit costs have increased, and your existing limits may no longer provide adequate protection.

How Homeowners Coverage Differs From Landlord Insurance

The key distinction between these two policies lies in occupancy and income protection. Homeowners insurance covers loss of use (additional living expenses if you must relocate), while landlord insurance covers loss of rent (your lost income from tenants). Your homeowners policy protects your personal belongings inside the home, whereas landlord insurance does not cover tenant possessions at all. Both policies cover the dwelling structure and detached buildings, but the liability exposure differs significantly. Homeowners policies protect you and your family members, while landlord policies protect you against tenant-related claims and injuries on the rental property. The cost difference reflects these distinct protections: landlord insurance typically runs about 25% more than homeowners insurance due to higher risk exposure from tenancy. Understanding which policy matches your situation prevents costly coverage gaps and unnecessary premium expenses.

Which Policy Matches Your Situation

The decision between landlord and homeowners insurance hinges on one question: will you live in the property or rent it out? This occupancy distinction determines everything from coverage types to premium costs. If you rent the entire property to tenants for most of the year, landlord insurance is not optional-it is mandatory. Your homeowners policy explicitly excludes coverage for rental activity, which means you have zero protection if you ignore this requirement. According to the Insurance Information Institute, homeowners insurance premiums rose by 11.2 percent in 2022 from 2021. A property that generates $2,000 monthly rental income cannot afford coverage gaps. The premium difference exists because rental properties present measurable higher risks: longer occupancy periods cause more wear and tear, increased foot traffic creates liability exposure, and tenant disputes can escalate into costly claims.

Converting Your Primary Residence to a Rental

Utah landlords who convert a primary residence into a rental property face a critical decision point. You must notify your insurance carrier immediately and switch policies before tenants move in. Continuing a homeowners policy while renting violates your policy terms and voids coverage when you need it most. If a tenant is injured or causes property damage, the insurer can deny your claim entirely, leaving you personally liable for thousands of dollars in medical bills or repairs.

Understanding Coverage Limits and Personal Property Differences

The coverage limits and specific protections differ dramatically between these policies. Homeowners insurance includes personal property coverage for your belongings inside the home-furniture, electronics, clothing-up to 50% to 70% of your dwelling value for off-premises items. Landlord insurance excludes tenant belongings entirely because those items belong to the renter, not you. This means tenants must carry renters insurance to protect their possessions, which most landlords require in the lease. Loss of use coverage in homeowners policies pays your temporary living expenses if a fire makes your home uninhabitable during repairs, but landlord policies replace this with loss of rent coverage that reimburses your lost income instead. For a Utah landlord with a $1,200 monthly rental income, losing three months of rent during repairs costs $3,600 in lost cash flow. Adding loss of rent coverage typically increases your premium by $200 to $400 annually, yet it protects income that far exceeds that cost in just one month of lost rent. Real quotes show this endorsement pays for itself immediately when a covered loss occurs.

Liability Coverage Scope and Application

Both policy types cover the dwelling structure and detached buildings like garages or sheds, but liability coverage differs significantly in scope and application. Homeowners liability protects you and your family members for injuries or property damage they cause both at home and away from home. Landlord liability specifically protects you against tenant-related claims and guest injuries on the rental property.

Standard liability limits of $100,000 prove inadequate in today’s lawsuit environment; increasing to $300,000 costs only $10 to $20 more annually, making this upgrade a practical necessity for both policy types. Utah property owners operating rental properties should add themselves as additional insureds on their landlord policy, expanding protection without significant cost increases.

Shopping Quotes and Finding the Right Coverage

Comparing actual quotes reveals the true cost difference: a homeowners policy might run $1,400 annually while the same property as a rental could cost $1,750 to $1,900 depending on the carrier and coverage selections. Shopping multiple quotes matters because insurance companies price risk differently, and a property that costs $1,800 with one carrier might cost $1,400 with another. An independent insurance broker can compare multiple carriers simultaneously, saving you time and often uncovering discounts you would miss shopping alone. Direct Insurance Services, as a locally trusted independent agency throughout Utah, works with top-rated carriers to help you access the best coverage options without pressure. Our experienced team provides clear guidance on which policy matches your situation and helps you compare options that fit both your needs and budget.

Final Thoughts

The difference between landlord insurance and homeowners insurance comes down to how you use your property and what financial risks you face. Homeowners insurance protects owner-occupied homes and your personal belongings inside, while landlord insurance protects rental properties and your lost income when tenants cannot occupy the space. Choosing the wrong policy leaves you exposed to denied claims and personal liability that can cost tens of thousands of dollars.

Utah property owners who rent out their homes cannot simply keep their homeowners policy in place. Rental activity voids homeowners coverage, which means you have zero protection if a tenant is injured or causes damage. The 25% premium increase for landlord insurance reflects real risk differences, not arbitrary pricing, because a tenant living in your property for twelve months creates more wear, more liability exposure, and more potential for costly disputes than a homeowner living in their own residence.

Direct Insurance Services helps Utah property owners navigate these decisions without confusion or pressure. We work with top-rated carriers to compare actual quotes and coverage options that fit your situation and budget. Contact us today to discuss which policy protects your property and income properly.