Best Auto Insurance Options for New Drivers

Getting your first car is exciting, but picking the right coverage can feel overwhelming. At Direct Insurance Services, we’ve helped thousands of new drivers find policies that actually fit their needs and budgets.

This guide walks you through the best auto insurance options for new drivers, from understanding what each coverage type does to finding discounts that lower your premiums. You’ll learn exactly what to compare when shopping for quotes and how to pick an insurer that won’t leave you hanging when you need them.

Coverage Types That Actually Matter for New Drivers

Why Liability Coverage Sets the Foundation

Liability coverage is non-negotiable, and most states require it by law. This coverage pays for damage or injuries you cause to someone else, and the numbers matter more than you think. Virginia’s minimum requirement sits at 50,000 dollars per person and 100,000 dollars per accident for bodily injury, plus 25,000 dollars for property damage. However, these minimums are dangerously low. A single accident involving multiple people or serious injuries can quickly exceed these limits, leaving you personally responsible for tens of thousands of dollars.

Try higher coverage limits-at least 100,000 dollars per person and 300,000 dollars per accident. Progressive’s quotes show this higher coverage costs roughly 1,037 dollars for six months, compared to 932 dollars for minimum coverage. That 105-dollar difference every six months protects you from financial ruin.

How Your Car Choice Affects Collision and Comprehensive Costs

Collision and comprehensive coverage protect your own vehicle, and here’s where your car choice determines everything. A used Honda Accord costs far less to insure than a new Dodge Challenger because repair bills and replacement costs are lower. If you’re driving a financed or leased vehicle, your lender requires both coverages.

For older cars you own outright, skipping collision and comprehensive saves money, but only if you can afford to replace the vehicle yourself. Many new drivers make the mistake of carrying liability-only coverage on a car they can’t replace, which defeats the purpose of having insurance at all.

The Often-Overlooked Protections That Matter

Additional protections like uninsured motorist coverage and medical payments coverage handle situations where the other driver lacks adequate insurance or injuries require immediate medical care. Uninsured motorist coverage is particularly important because in 2023, 15.4 percent of motorists were uninsured.

Medical payments coverage typically costs just a few dollars monthly and covers hospital bills regardless of fault. These aren’t luxury add-ons-they’re practical shields against scenarios that happen to real drivers every single day. Understanding what each protection does positions you to make smart choices about which ones fit your situation.

How New Drivers Actually Save Money on Insurance

The Real Cost Gap Between Carriers

The gap between what new drivers pay and what they could pay is substantial. As of November 2025, the average annual cost of car insurance is $2,697 for full coverage, but that number drops dramatically with the right strategy. A 17-year-old male pays roughly $7,377 annually on average, yet Erie Insurance quotes the same demographic at just $4,351-a difference of nearly $3,000 per year. This isn’t luck; it’s about knowing where discounts hide and which carriers actually reward safe driving.

Discounts That Stack Up Fast

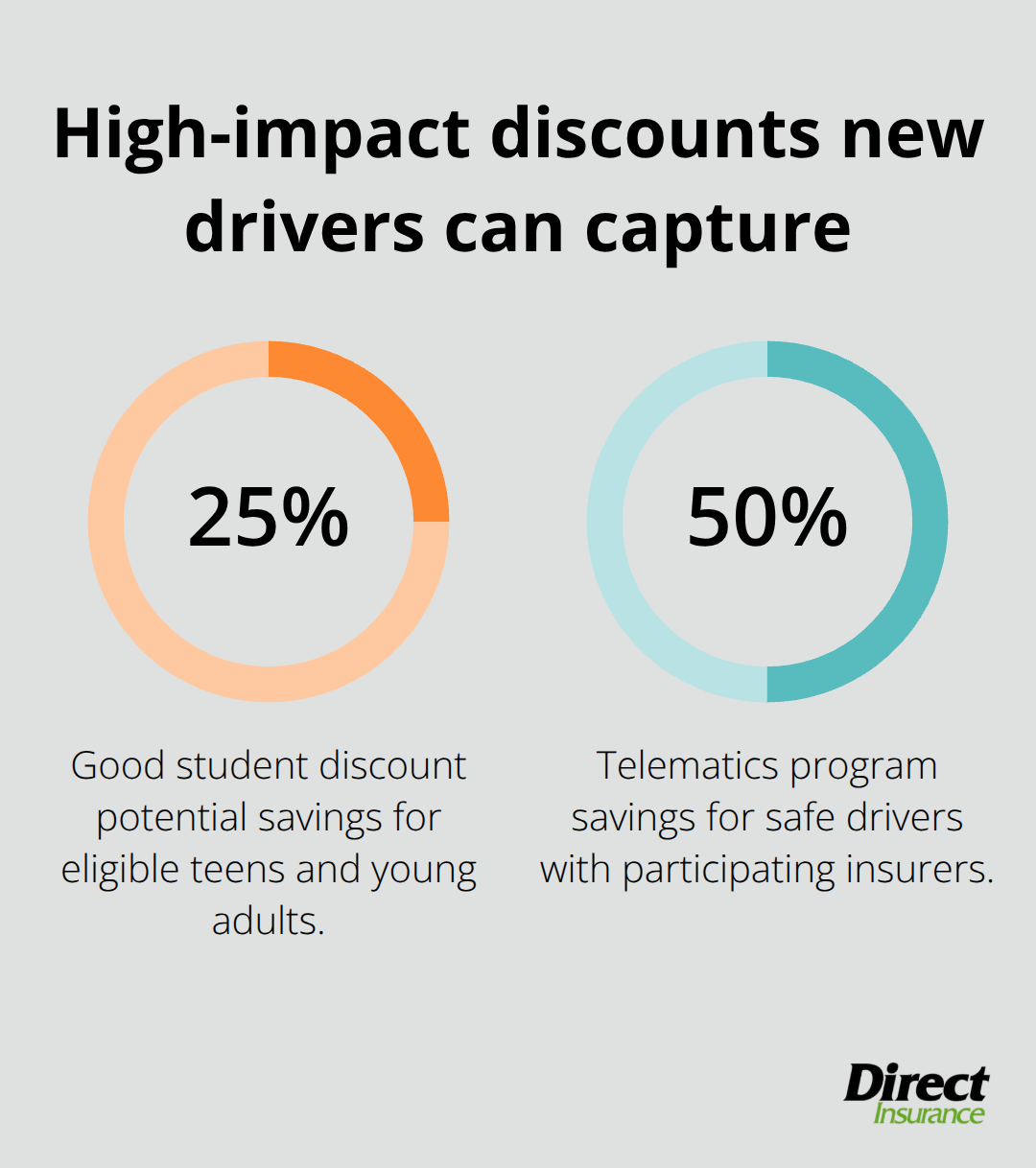

Good student discounts save up to 25 percent for teens maintaining a 3.0 GPA or ranking in the top 20 percent of their class, and this discount extends until age 25. Defensive driving courses unlock additional savings and can remove points from your record. Some insurers offer telematics programs that monitor your actual driving behavior; safe drivers using these programs can reduce premiums by up to 50 percent according to Forbes.

Bundling auto insurance with renters or homeowners coverage creates immediate savings that most new drivers overlook. This approach typically yields multi-policy discounts that reduce your total premium substantially. When comparing quotes, request coverage identical across all carriers so you’re measuring actual price differences rather than coverage variations.

Shopping Strategy That Actually Works

The real power comes from comparing quotes across multiple carriers-USAA charges $1,612 annually for 25-year-old females while Allstate quotes $2,382 for the same profile, showing how dramatically rates vary. Request quotes from at least five insurers including regional carriers, not just national names like Progressive and GEICO, because local insurers sometimes offer better rates for specific geographic areas.

Geographic location matters enormously: a teen male driver in Texas pays roughly $5,397 yearly while the same driver in Ohio pays around $4,008. Your vehicle choice determines everything for collision and comprehensive costs, but it also influences how insurers rate your liability risk. A used Honda Accord qualifies for better rates than a Dodge Challenger because insurers calculate repair costs and replacement value into their models.

Adjusting Coverage to Fit Your Budget

Higher deductibles on collision and comprehensive lower your monthly premium, though you’ll pay more out-of-pocket after a claim. A $1,000 deductible instead of $500 can reduce your premium by 15 to 30 percent depending on your carrier. If you’re staying on a parent’s policy rather than purchasing individual coverage, inform your agent about your learner’s permit and driving status, as this affects rating and ensures proper coverage.

Avoid the temptation to misrepresent your vehicle or driving habits to lower rates-this is illegal and results in denied claims or policy cancellation. Building your long-term strategy means getting multiple quotes now, selecting discounts you actually qualify for, and revisiting your policy annually because rates change and new discounts emerge regularly. Once you’ve locked in your coverage and discounts, the next step involves evaluating which insurance providers actually deliver when you file a claim.

Choosing an Insurer That Actually Delivers When You Need It

Claims Service Separates Good Insurers from Great Ones

State Farm processes approximately 34,000-39,000 claims daily and maintains 24/7/365 service availability, which matters when you file your first claim at midnight after an accident. Their mobile app carries a 4.8/5 rating across over 1 million reviews, making policy management and claims filing genuinely simple. However, State Farm’s strength in claims handling doesn’t automatically make them the cheapest option for your situation. USAA charges just $1,612 annually for 25-year-old females while State Farm may quote considerably higher, depending on your location and driving history. The real decision comes down to this: do you prioritize the lowest premium or responsive claims service?

New drivers often underestimate how much they’ll value fast, hassle-free claims handling when they’re stressed after an accident. If you’re eligible for USAA through military service, comparing their rates against GEICO and Erie Insurance shows exactly where your best value sits. Erie Insurance quotes 17-year-old males at roughly $4,351 annually, substantially below national averages, yet their claims reputation varies by region.

Location Determines Which Insurer Serves You Best

Geographic location determines which insurer actually serves your area well-some carriers maintain strong networks in urban zones while others excel in rural regions where repairer choice and local service quality significantly affect your claims experience. National insurers like Progressive and GEICO offer consistent pricing nationwide, but regional carriers sometimes beat their rates in specific states. A teen male in Ohio pays around $4,008 annually while the same driver in Texas faces $5,397, meaning your state’s preferred insurers matter as much as the carrier itself.

Rural areas present unique challenges: you may need an insurer that allows you to select your repairer rather than forcing you to use expensive or distant shops. Ask each carrier whether they permit repairer choice in your area, as this flexibility protects you from inflated repair costs and long wait times.

What to Ask Before You Commit to a Policy

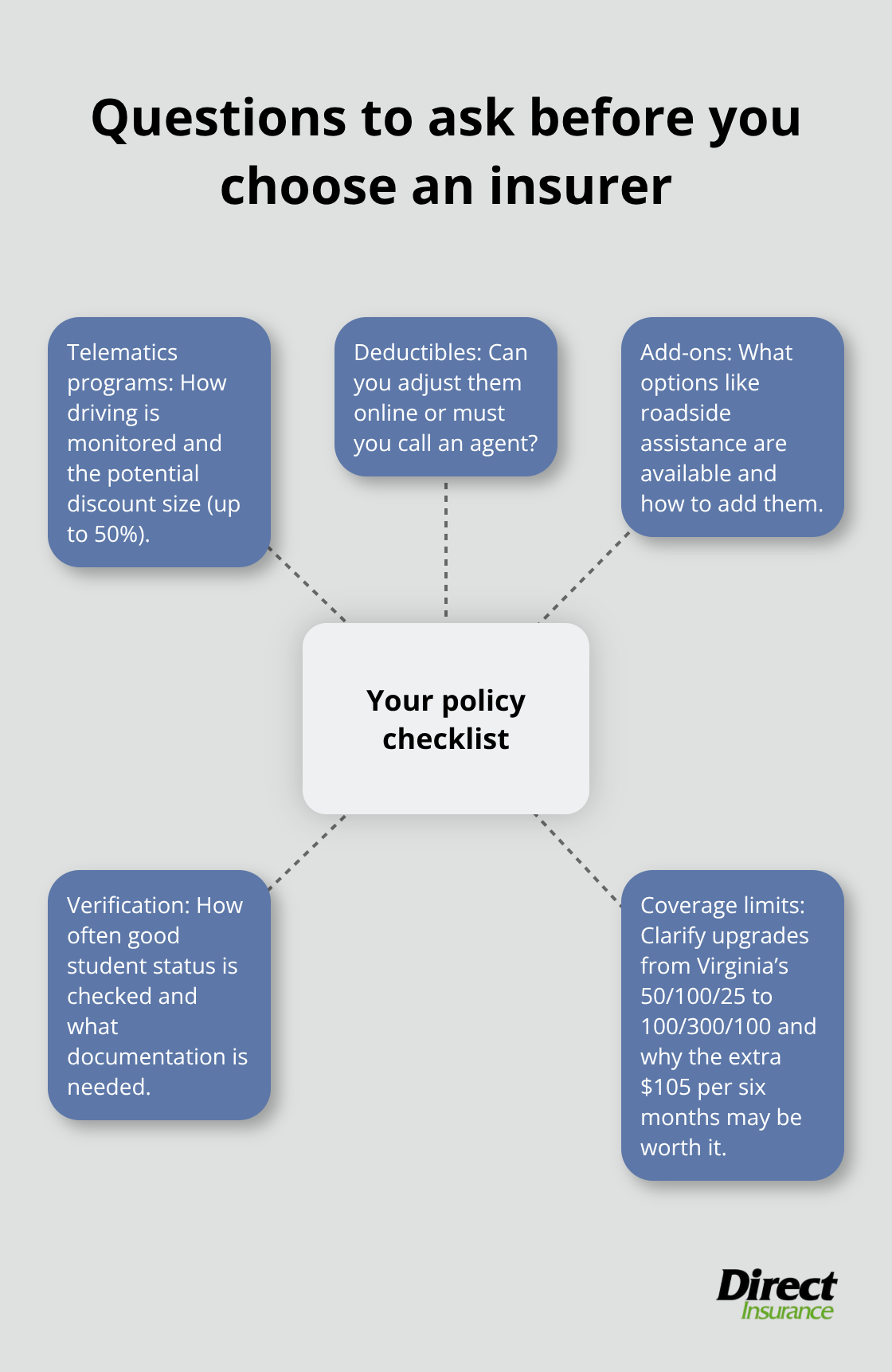

When you’re shopping for auto insurance as a new driver, ask each insurer about their telematics programs, which monitor your actual driving behavior and reward safe drivers with discounts up to 50 percent according to Forbes. Some carriers offer flexibility to customize your policy-can you adjust deductibles without calling an agent, or add coverage for specific needs like roadside assistance? Verify whether your insurer allows policy customization and what that process actually looks like.

Ask specifically about their good student discount verification process, since some insurers require updated transcripts annually while others verify once and extend the discount automatically. Your insurer should explain exactly what their coverage limits mean and help you understand why upgrading from Virginia’s minimum 50,000/100,000/25,000 liability to 100,000/300,000/100,000 costs just $105 extra every six months.

Reading Reviews That Actually Matter

The difference between a responsive insurer and an indifferent one becomes painfully obvious during your first claim, so read recent customer reviews focusing on claims experience rather than premium quotes alone. Look for patterns in how quickly insurers respond to claims, whether they communicate clearly throughout the process, and whether customers felt treated fairly after accidents. Negative reviews mentioning delayed claim payments or poor communication signal red flags, while positive reviews highlighting fast settlements and helpful agents indicate solid claims operations.

Pay attention to reviews from drivers in your specific state or region, since service quality varies by location. An insurer with excellent claims handling in California may operate differently in Utah or Ohio. Check whether reviewers mention their agent’s responsiveness and whether they felt supported when they needed help most.

Final Thoughts

Finding the best auto insurance for new drivers requires you to compare quotes across at least five carriers, select discounts you genuinely qualify for, and pick an insurer whose claims service matches your priorities. The gap between what new drivers pay and what they could pay reaches thousands of dollars annually, but only if you shop strategically rather than accepting the first quote. Gather quotes from USAA, GEICO, Erie Insurance, Progressive, and at least one regional carrier in your state, then request identical coverage across all quotes so you measure actual price differences.

Verify which good student, defensive driving, or telematics discounts apply to your situation, then calculate your true cost after discounts. Check recent customer reviews focusing specifically on claims experience in your geographic area, since service quality varies by region. Once you select your policy, revisit it annually because rates change and new discounts emerge regularly.

As you build your driving record over the next three years, your premiums will drop substantially, especially if you maintain a clean record without accidents or tickets. We at Direct Insurance Services help new drivers navigate these decisions by comparing options from top-rated carriers and finding coverage that actually fits your needs and budget. Contact our team to review your specific situation and lock in the right protection for your first years on the road.