Landlord Insurance for Rentals: Protecting Your Investment

Rental property owners face real financial risks every day. Tenants cause damage, guests get injured, and unexpected vacancies drain your income. Landlord insurance for rentals protects against these specific threats that standard homeowners policies won’t cover.

We at Direct Insurance Services help property owners understand exactly what coverage they need and why it matters.

What Landlord Insurance Actually Covers

Rental property owners face distinct risks that standard homeowners policies refuse to cover. Insurance companies treat rental properties as higher risk, and the numbers prove them right-loss of rental income accounts for a significant portion of landlord insurance claims. This reveals why you need a completely different policy. Your homeowners insurance will not pay if a tenant causes damage, if someone gets injured on the property during a lease, or if the building becomes uninhabitable and you lose monthly rent. We see landlords every year who assumed their existing homeowners policy covered their rental unit, only to discover during a claim that they have zero protection.

How Landlord Insurance Differs from Homeowners Coverage

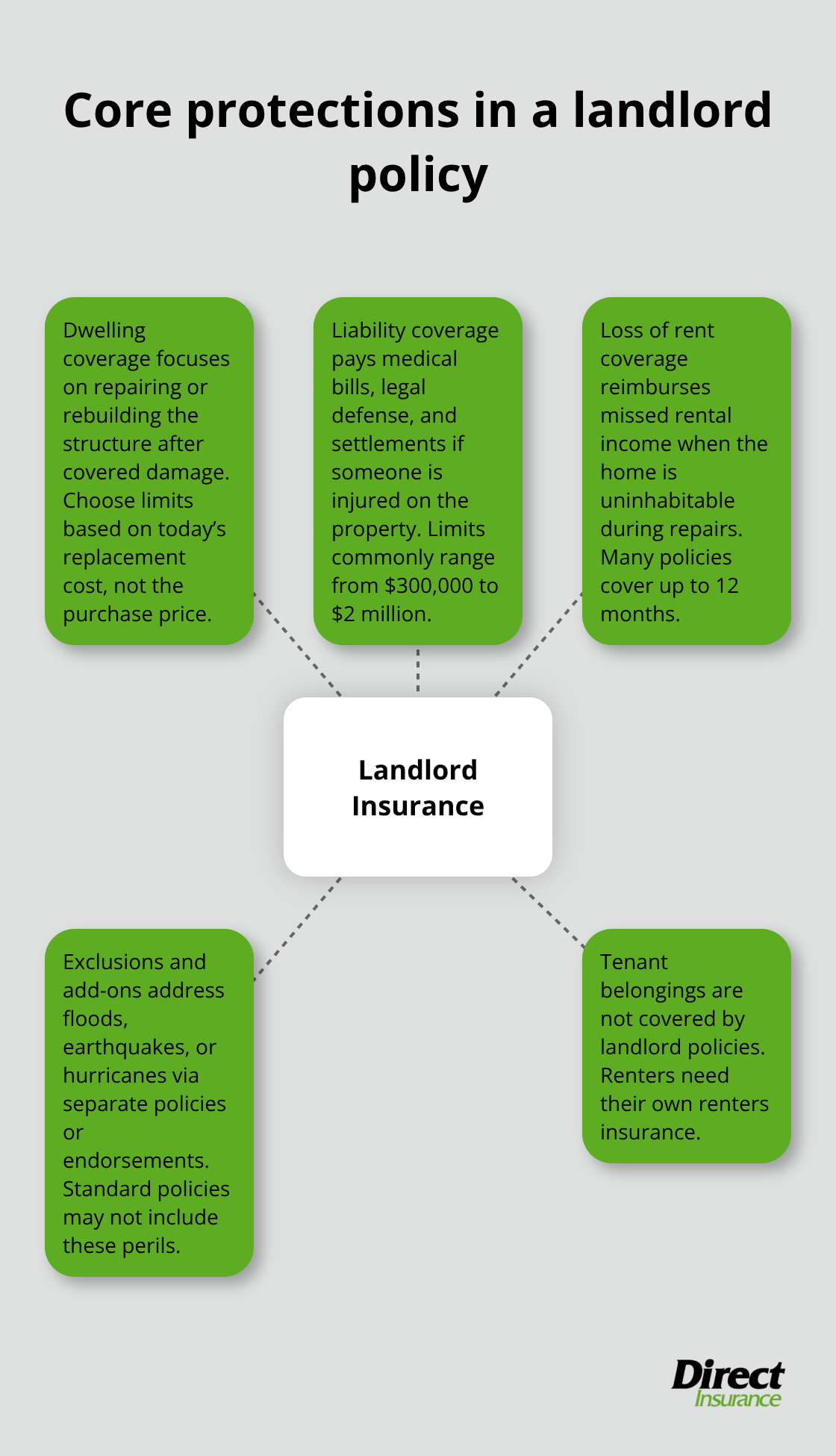

The core difference is straightforward: homeowners insurance protects you and your family in a primary residence. Landlord insurance protects your income and your property when strangers occupy it. Homeowners policies cover tenant belongings, which landlord policies explicitly do not. If a tenant’s furniture burns in a fire, that’s their loss-they need renters insurance to cover it. Landlord policies instead focus on what matters to your bottom line: the structure itself, liability if someone gets hurt on your property, and the rent you’d lose if the building becomes unlivable. Dwelling coverage typically ranges from $100,000 to $500,000 depending on replacement costs, and liability coverage usually sits between $1 million and $2 million. Many landlords underestimate dwelling coverage because they anchor to the purchase price rather than current replacement costs, which have risen significantly due to inflation and supply chain disruptions.

Why Liability Protection Matters Most

A guest slips on your stairs, a tenant’s friend gets injured in the pool, or someone claims the roof collapse was due to your negligence. These scenarios cost money-sometimes substantial amounts. Liability coverage pays medical bills, legal defense costs, and settlements. This protection is why landlord insurance exists in the first place. Without it, you remain personally responsible for every injury claim, which can easily exceed $100,000 when attorney fees and medical costs combine. Steadily, a landlord insurance specialist, includes $300,000 to $2 million in liability coverage across all policies nationwide, recognizing that this is the protection landlords actually need. Your mortgage lender requires proof of landlord insurance before approving a rental property loan, and liability coverage is a major reason why-lenders know that without it, you’re one accident away from financial catastrophe.

What Happens When You Lose Rental Income

The property sustains fire damage, a pipe bursts and floods the unit, or a severe storm makes the building uninhabitable. Your tenant moves out, and suddenly you have no income while repairs take weeks or months. Loss of rent coverage reimburses you for that lost income during the repair period, protecting your cash flow when you need it most. This coverage typically covers up to 12 months of lost rent, though some policies offer longer periods. Without this protection, you still owe your mortgage, property taxes, and maintenance costs while receiving zero tenant payments. The financial strain can force you to deplete savings or take on debt just to keep the property afloat.

The Real Cost of Being Uninsured

Skipping landlord insurance or underinsuring your property creates exposure that can wipe out years of profit. A liability claim without coverage means your personal assets are at risk-your bank accounts, your home, your future income. Property damage without dwelling coverage means you pay for repairs out of pocket. Lost rent without income protection means you absorb months of expenses with no incoming revenue. These aren’t theoretical risks; they happen to landlords who thought they could save money by cutting corners on insurance. The next chapter explores the specific coverage options available and how to determine the right limits for your situation.

Coverage Options and What They Protect

Dwelling Coverage: Protecting Your Building Structure

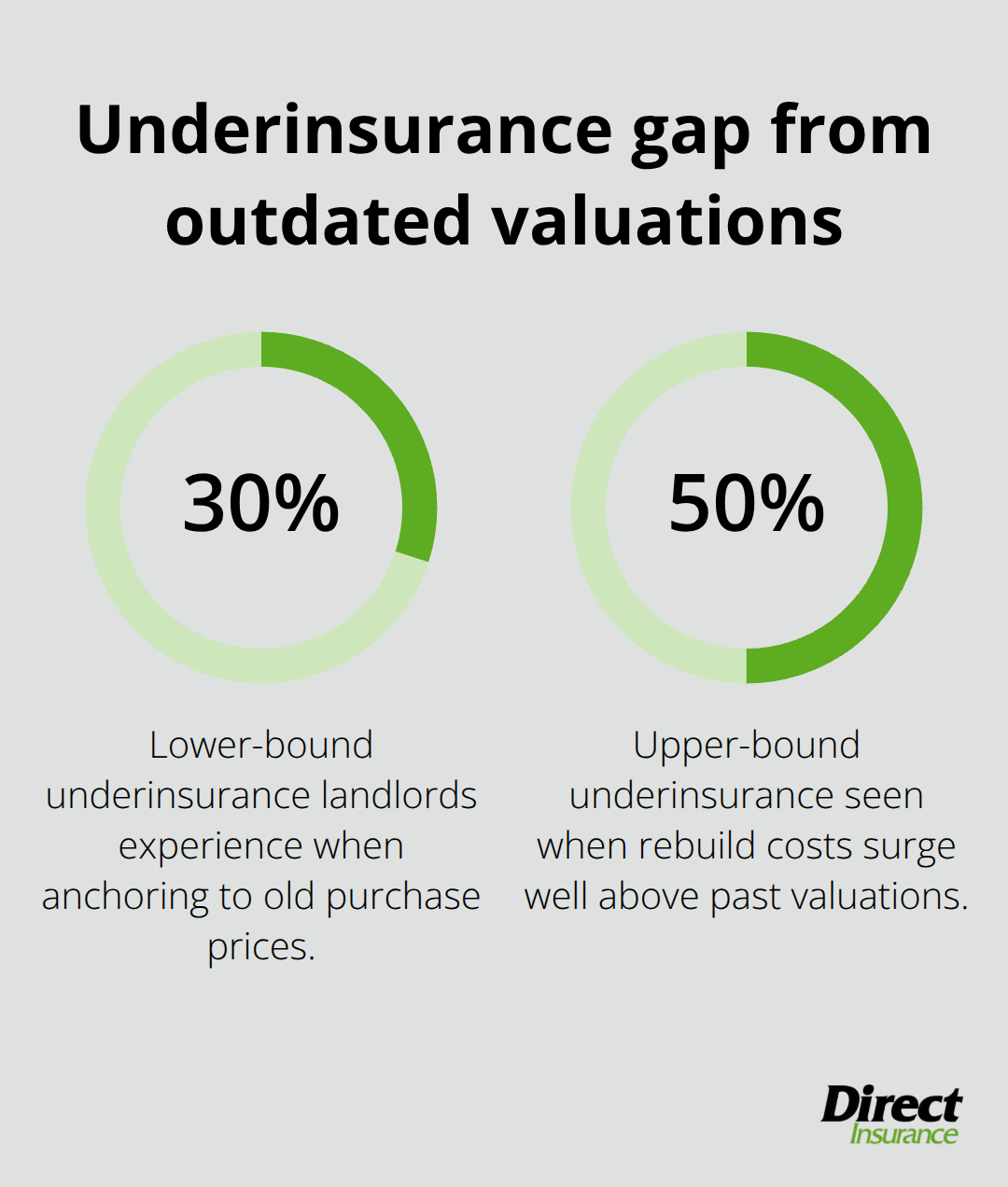

Dwelling coverage protects the physical structure of your rental property, and the number you choose determines whether you recover fully after a loss or face thousands in out-of-pocket repairs. Most landlords make a critical mistake by basing dwelling coverage on their original purchase price rather than current replacement costs. A home purchased for $300,000 ten years ago might now cost $450,000 to rebuild due to inflation and material price increases. Landlords often end up underinsured by 30 to 50 percent because they anchor to outdated valuations.

Your dwelling coverage should reflect what it would actually cost to rebuild the structure today, not what you paid for it. Most policies range from $100,000 to $500,000 depending on property size and location, but the only number that matters is your specific rebuild cost. Request a detailed replacement cost estimate from a contractor or use online rebuild calculators that account for local labor rates and material prices in your area.

If your property sits in a high-risk zone for earthquakes, floods, or hurricanes, standard dwelling coverage may exclude these perils entirely. You’ll need separate policies or endorsements to cover these specific threats. This distinction matters significantly when you live in regions prone to natural disasters.

Loss of Rent Coverage: Your Financial Safety Net

Loss of rent coverage keeps you solvent when the property becomes uninhabitable. A burst pipe, kitchen fire, or roof collapse forces your tenant to leave, and suddenly your mortgage payment, property taxes, and maintenance costs continue while your rental income stops. This coverage typically reimburses you for up to 12 months of lost rent during repairs, though longer periods are sometimes available depending on the carrier.

The protection matters most in properties where repairs take months rather than weeks. If you own a property in a hurricane zone and a storm causes severe structural damage, loss of rent coverage prevents you from draining your savings while contractors rebuild. Without it, a single major loss can force you to liquidate investments or take on debt just to cover basic property expenses.

Liability Coverage: Protecting Your Personal Assets

Liability coverage protects your personal assets when someone gets injured on your property or claims you’re responsible for damages. This coverage pays medical expenses, legal defense costs, and settlements up to your policy limit. A guest falls down exterior stairs, a tenant’s friend drowns in the pool, or a visitor claims the roof collapse caused injury-each scenario triggers liability exposure that can exceed $100,000 when medical bills and attorney fees combine.

Standard liability limits start at $300,000 and extend to $2 million or higher depending on your risk profile and property features. Properties with pools, trampolines, or decks carry significantly higher liability exposure because these features increase injury risk. If your property has a pool, umbrella insurance may be required beyond your base liability limit to handle the additional exposure.

Outdoor features and tenant density directly influence what liability limit you need. A duplex with a pool requires more protection than a single-family home with minimal outdoor amenities. Your mortgage lender mandates that you carry these three coverage types before approving a rental property loan because they address the financial catastrophes that actually destroy landlords. The next chapter examines real-world scenarios where these coverages protect you and shows how claims actually unfold in practice.

Common Claims and Real-World Scenarios

Water Damage Strikes First and Hardest

Water damage strikes without warning and costs landlords more than any other peril. A burst pipe during freezing temperatures, an overflowing bathtub, or a roof leak turns into thousands of dollars in damage within hours. Loss of rent coverage can compensate landlords for lost rental income if their property becomes uninhabitable due to covered events, which means water-related incidents and the resulting vacancy represent the leading reason landlords file claims. A single water event forces your tenant to relocate for weeks while contractors dry walls, replace flooring, and repair structural damage. Without loss of rent coverage, you absorb the full cost of repairs plus lost income simultaneously.

Weather-related losses hit hardest in high-risk regions. Florida landlords face hurricane exposure, Colorado properties deal with hail damage, and properties nationwide experience increasingly severe wind and rain events. Proper coverage can make a significant difference in real-life situations-a single hail storm can destroy a roof that costs $15,000 to $25,000 to replace depending on size and materials. Wind damage from severe storms creates liability exposure when falling debris injures someone on or near your property.

Tenant-Caused Damage and Vandalism

Tenant-caused damage creates a different problem entirely. A tenant punches a hole in drywall, breaks appliances, or causes intentional vandalism beyond normal wear and tear. Your landlord policy covers these sudden, accidental damages to landlord-owned property, but not the tenant’s belongings. The tenant’s renters insurance should cover their items, which is why requiring renters insurance in your lease protects both parties. If a tenant refuses to carry renters insurance and their belongings get damaged in a covered event, that’s their financial problem, not yours.

Liability Claims Escalate Rapidly

Liability claims emerge from the most unexpected situations and escalate faster than property damage claims. A guest trips on a broken step and breaks their leg, requiring surgery and months of physical therapy. Medical bills alone exceed $50,000 before attorney fees and settlement negotiations begin. A tenant’s friend drowns in your pool despite a basic fence, and the family sues for wrongful death, claiming inadequate safety features. These scenarios destroy landlords without liability coverage because courts award damages far beyond medical expenses.

Your liability limit determines whether the insurance company covers the full claim or you pay the excess out of pocket. Properties with pools, trampolines, or elevated decks carry significantly higher liability exposure because these features increase injury risk substantially. A property with an in-ground pool requires a $2 million liability limit instead of the standard $300,000 because pool-related drowning claims routinely exceed $1 million. Umbrella insurance extends beyond typical property-related incidents and can cover claims of libel, slander, or invasion of privacy-additional protections that standard policies often exclude.

Claims Processing Speed and Deductible Strategy

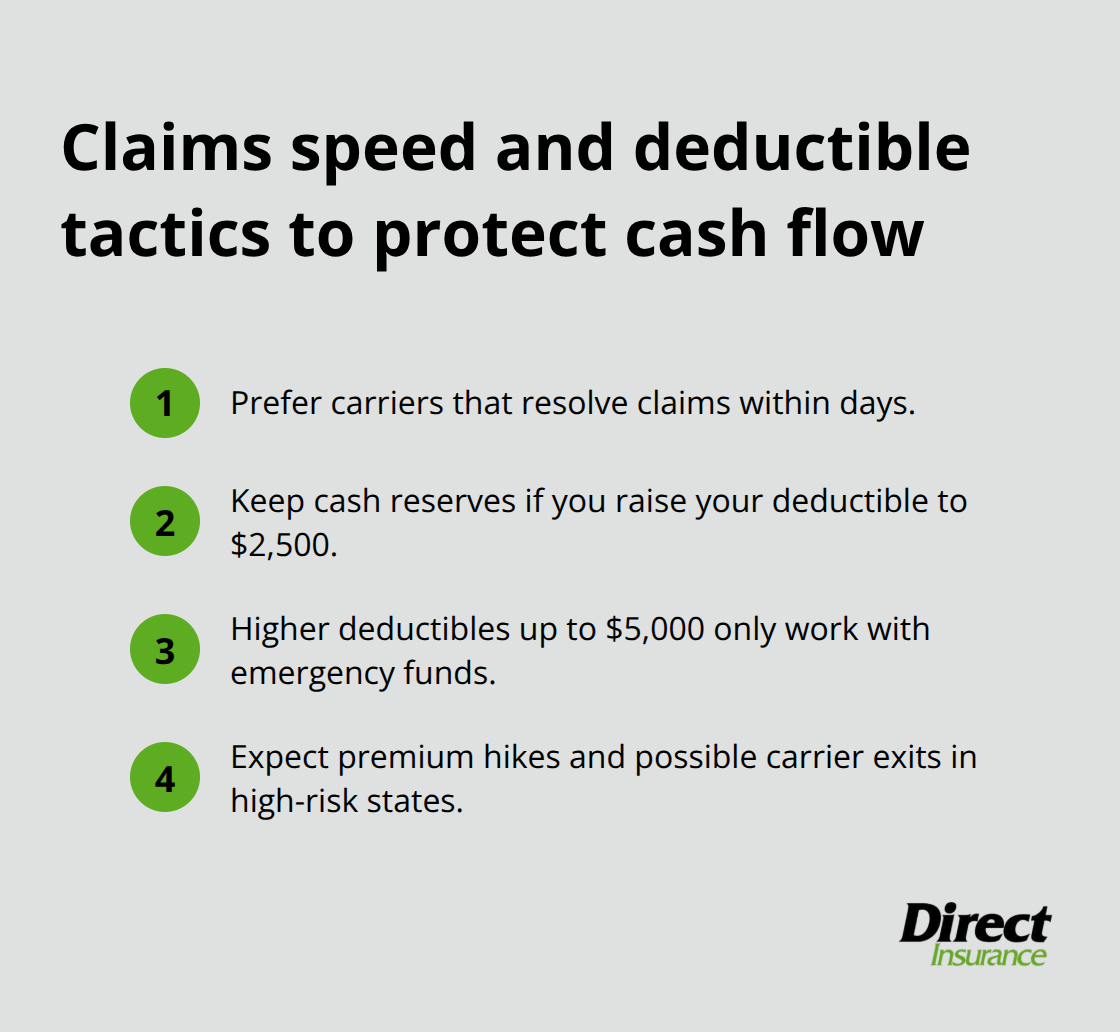

Claims processing speed matters more than most landlords realize. When a pipe bursts and your tenant cannot stay in the property, you need loss of rent coverage activated immediately, not weeks later. Carriers that process claims within days rather than weeks minimize your cash flow disruption. Properties in high-risk markets like Florida, Louisiana, and California face premium increases exceeding 20 percent annually, and some carriers have stopped writing new policies entirely in these regions.

Your deductible choice directly impacts your out-of-pocket costs when claims occur. Raising your deductible from $500 to $2,500 lowers your premium significantly, but you must have cash reserves to cover that deductible when a loss happens. Some landlords have increased deductibles up to $5,000 since 2021 to reduce premiums, but this strategy only works if you have emergency funds available for repairs.

Final Thoughts

Landlord insurance for rentals protects your income, your property, and your personal assets from the financial disasters that destroy unprepared owners. The coverage types we’ve outlined-dwelling protection, loss of rent, and liability-address the specific risks that rental properties create, and a single water damage claim, tenant injury, or extended vacancy can eliminate years of profit without proper protection. Start by calculating your actual replacement cost rather than anchoring to your purchase price, then request quotes from multiple carriers and compare dwelling limits, liability amounts, and loss of rent periods side by side.

Review your current coverage annually because replacement costs rise continuously and your property’s risk profile changes over time. If you’ve added a pool, deck, or other outdoor features, your liability exposure has increased significantly and your policy limits may no longer be adequate. Properties in high-risk regions for hurricanes, hail, or earthquakes need additional endorsements beyond standard coverage to protect your investment fully.

We at Direct Insurance Services help property owners navigate these decisions without pressure or one-size-fits-all solutions. Our team works with top-rated carriers to build customized landlord insurance policies that match your specific property, location, and risk profile, whether you’re protecting a single rental unit or managing a portfolio of properties. Contact Direct Insurance Services today for a personalized review of your rental property protection.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation