Why Did My Home Insurance Go Up This Year?

Your home insurance premium jumped this year, and you’re not alone. Thousands of homeowners are asking why their rates climbed, and the answers often surprise them.

At Direct Insurance Services, we’ve seen firsthand how quickly insurance costs can shift. In this post, we’ll walk you through the main reasons premiums rise and show you concrete steps to bring your costs back down.

What’s Really Driving Your Premium Increase

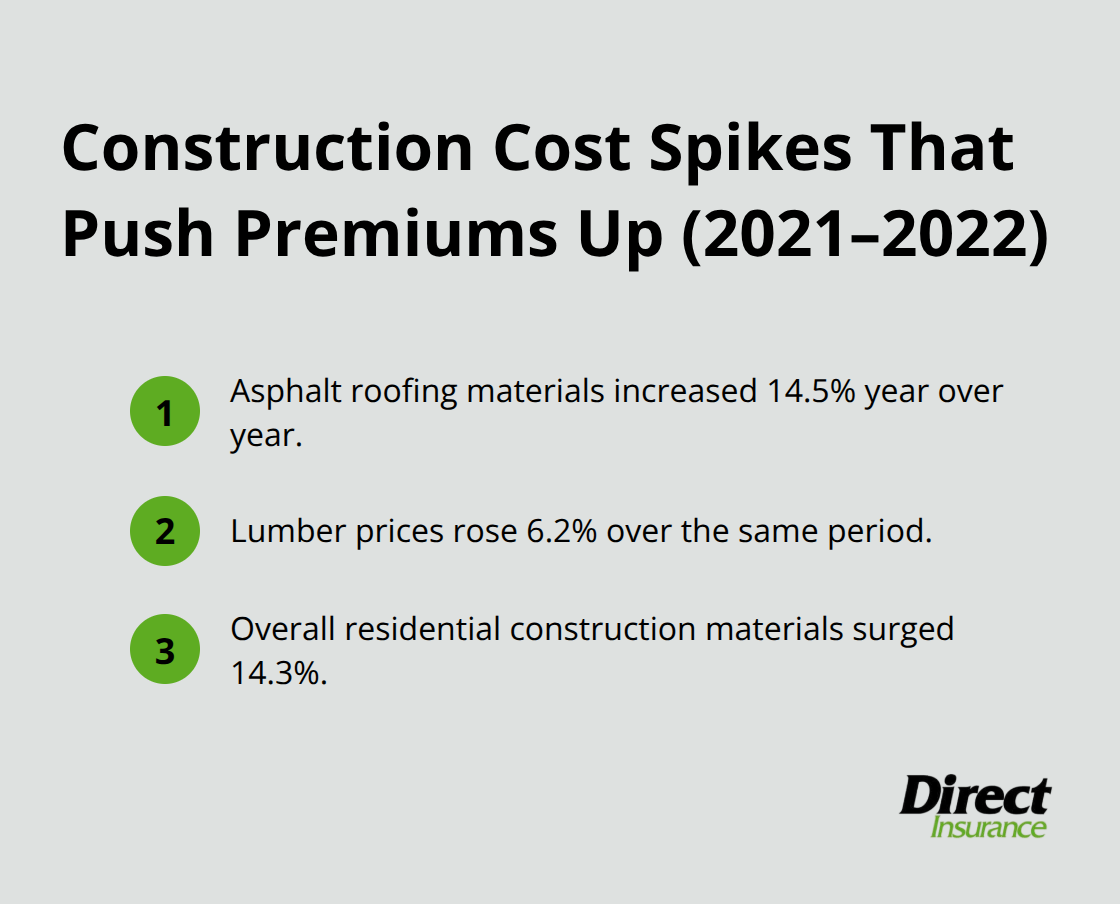

Building materials and labor costs have skyrocketed, and this is the primary reason your premium climbed. From October 2021 to October 2022, asphalt roofing materials jumped 14.5%, lumber rose 6.2%, and overall residential construction materials surged 14.3%, according to the U.S. Bureau of Labor Statistics Producer Price Index. When your home needs repairs after a claim, insurers pay these inflated costs, which means they charge higher premiums upfront to cover future payouts.

A skilled-labor shortage compounds this problem-the construction industry had 423,000 open positions in September 2022, forcing contractors to charge more and take longer on repairs. This directly hits your wallet because insurers factor these extended timelines and wage pressures into their rates.

Natural Disasters Are Hitting Harder and More Often

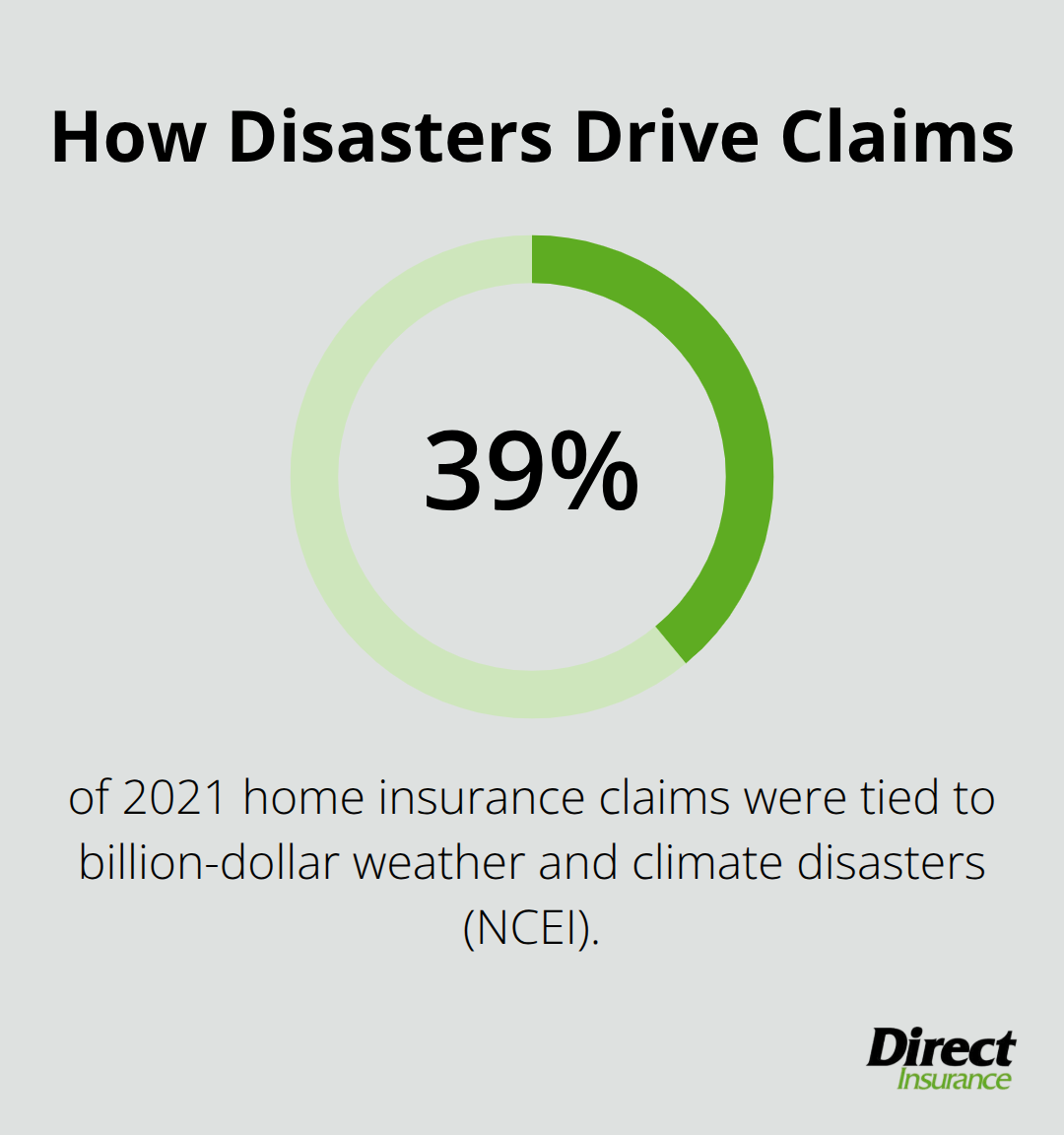

The frequency and severity of catastrophic weather events have accelerated dramatically. In 2024, the U.S. experienced 27 events that exceeded $1 billion in damages each, according to Risk & Insurance in collaboration with Munich Re US. These disasters destroy homes across multiple states simultaneously, forcing insurers to pay billions in claims at once. When this happens, companies raise premiums across entire regions to recover losses. The National Centers for Environmental Information reported that in 2021 alone, there were 18 weather and climate disasters costing over $1 billion, and these events accounted for roughly 39% of all home insurance claims that year. Your premium reflects your area’s exposure to these risks-if you live in a state experiencing more frequent wildfires, hail, or hurricanes, your rates will climb faster than homeowners in lower-risk regions.

Your Home’s Value and Risk Profile Changed

Your home is likely worth more today than when you bought it, and replacement costs have outpaced purchase prices. If you bought your home two years ago for $256,000 but it’s now worth $310,000 or more, your insurer may have adjusted your dwelling coverage upward to reflect current rebuilding costs. A common rebuilding benchmark is approximately $150 per square foot, which often exceeds what you originally paid. Additionally, if you’ve made renovations, added a deck, finished a basement, or upgraded your roof, these improvements increase your home’s replacement cost and your premium. Home improvements that you don’t report to your insurer leave you underinsured, so when you finally tell them about the work, your premium jumps to reflect the actual value you need protected. This isn’t your insurer being unfair-it’s them correcting an imbalance between what you’re paying and what they’d actually owe if your home burned down tomorrow.

Now that you understand why your premium rose, the next section reveals specific actions you can take to lower your costs without sacrificing the protection your home needs.

Factors Specific to Your Policy and Location

Claims History Shapes Your Premium

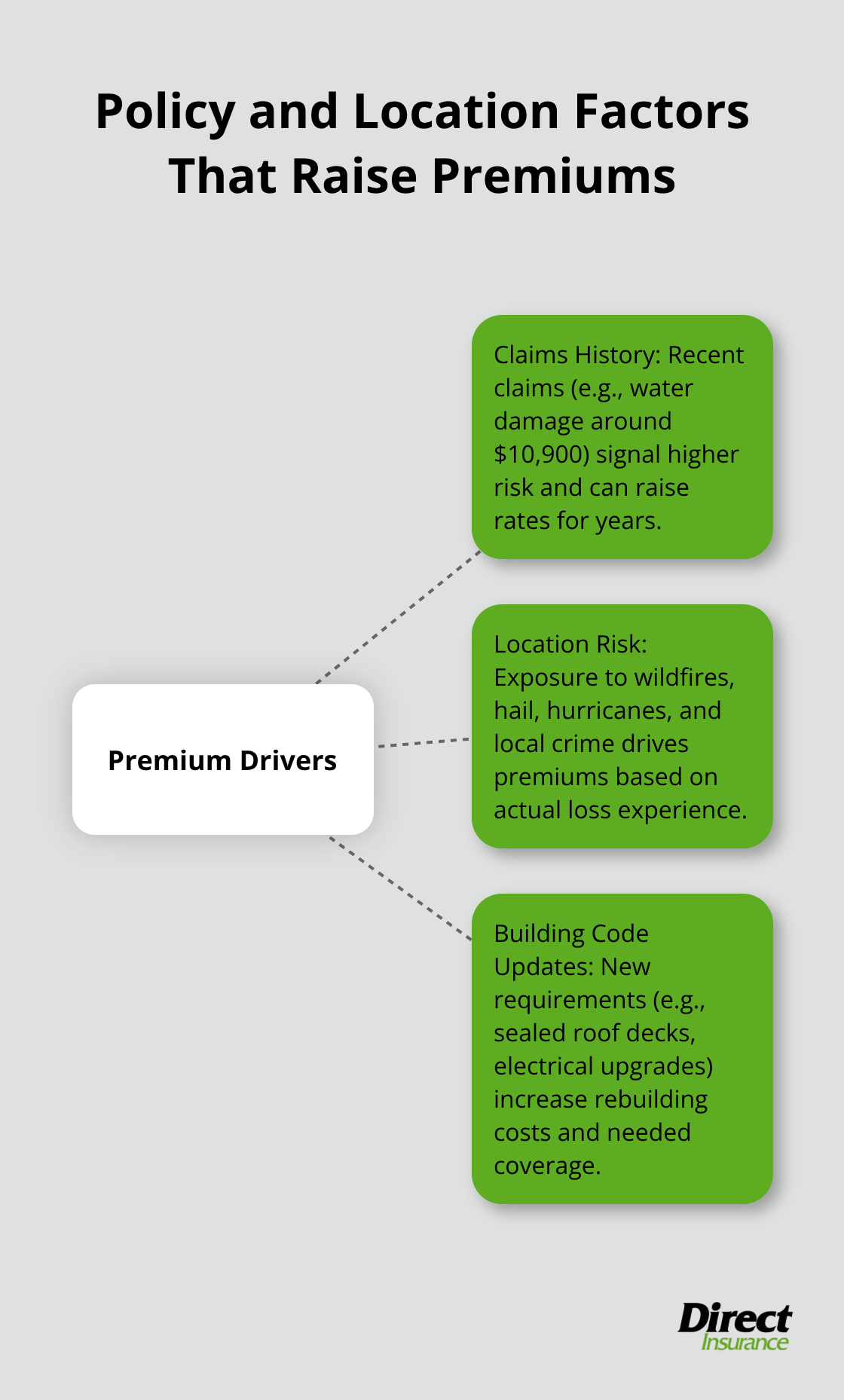

Your past claims determine how insurers price your coverage going forward. If you filed a claim in the last three to five years, your insurer views you as higher risk, and your rates reflect that immediately. A single water damage claim averaging around $10,900 according to the Insurance Information Institute can trigger a premium increase that lasts years. Insurers also track whether you’ve switched policies frequently-constant shopping signals instability to underwriters, and some carriers penalize rate-jumpers.

Location Determines Your Exposure to Risk

Where you live drives your premium more than almost any other factor. If you live in a state experiencing more frequent wildfires, hail, or hurricanes, your premiums climb faster than homeowners in lower-risk regions because your area’s actual loss experience dictates local rates. The National Centers for Environmental Information reported that weather and climate disasters accounted for roughly 39% of all home insurance claims in 2021, so living in a high-exposure area means you pay for the real risk profile of your neighborhood, not just national averages. Your local crime rate also matters-theft and vandalism claims push rates up in specific communities, and this variation explains why two identical homes in different neighborhoods carry vastly different premiums.

Building Code Updates Increase Replacement Costs

When your city or county updates building codes, insurers raise premiums because repairs and rebuilds now cost more to meet new standards. If your area recently required sealed roof decks for wind protection or upgraded electrical standards, your home’s replacement cost automatically rises (particularly in states like Florida and California, where wildfire and hurricane codes have tightened significantly). An insurer won’t rebuild your home to 1990s standards after a loss-they’ll rebuild to current code, which means your dwelling coverage needs to reflect those higher costs upfront. If your coverage limits haven’t been updated to account for code-driven cost increases, you’re underinsured, and when your insurer corrects this gap, your premium jumps. Scheduling a policy review every two to three years matters because building codes evolve, and your coverage should evolve with them. An independent agent who tracks local code changes helps you stay ahead of these adjustments rather than being surprised by them.

Now that you understand how your claims history, location, and local building codes affect your rate, the next section shows you concrete actions to lower your costs without sacrificing protection.

Cut Your Premium Without Cutting Coverage

Shop Around for Better Rates

Shopping around for quotes is the single most effective way to lower your premium, and most homeowners skip this step entirely. Insurance rates vary dramatically between carriers for identical homes in the same neighborhood. A homeowner in Utah might find a $1,200 annual premium at one insurer and an $1,800 premium at another for the same dwelling coverage and deductible. The difference stems from how each carrier prices risk, what claims they’ve paid in your area, and their overall underwriting strategy. Getting three to five quotes takes about an hour and typically saves $300 to $600 annually. Don’t accept the first quote your current insurer sends you when renewal arrives-that’s when they’re most likely to bump your rate aggressively. Request quotes before your renewal date and compare dwelling limits, deductibles, and coverage options side by side to verify you’re evaluating apples to apples.

Raise Your Deductible to Cut Monthly Costs

Increasing your deductible is the second lever that immediately reduces your premium. Moving from a $500 deductible to a higher deductible typically cuts your annual premium by 20 to 25 percent, depending on your insurer and location. If you raise it to $2,500, you could see reductions of 30 to 40 percent. The trade-off is straightforward: you pay more out of pocket if a claim happens, but you pay significantly less every month until it does. This strategy only works if you have emergency savings to cover the deductible you choose. If a $2,500 deductible would wipe out your emergency fund, don’t take it. A $1,000 deductible balances meaningful premium savings with realistic financial protection for most homeowners.

Bundle Policies and Claim Loyalty Discounts

Bundling your homeowners policy with auto, boat, or umbrella coverage unlocks multi-policy discounts that range from 10 to 25 percent depending on your carrier. Some insurers also offer loyalty credits if you stay with them for three, five, or more years, or programs like decreasing deductible credits that reduce your out-of-pocket cost by $100 per year toward your deductible if you remain claim-free. These programs aren’t available everywhere-some states restrict them-but asking your agent about what’s available in your area takes minutes and can save hundreds annually.

Install Protective Devices for Extra Savings

Installing protective devices like smoke detectors, fire alarms, water sensors, or smart home systems qualifies you for additional discounts at many carriers. Water sensors and interior sprinkler systems prove especially valuable in preventing costly water damage claims, which average around $10,900 according to the Insurance Information Institute.

Schedule Regular Policy Reviews

Schedule a policy review with your agent every two to three years to verify your coverage still matches your home’s current value and to catch new discounts you may have become eligible for since your last review. Building codes evolve, home values shift, and new discount programs launch regularly-a periodic conversation with your agent keeps your policy aligned with your actual needs and financial situation.

Final Thoughts

Your home insurance went up this year because construction materials and labor costs have surged, natural disasters are destroying homes at record rates, and your home’s replacement cost has climbed faster than its market value. These pressures affect every homeowner, but understanding why your home insurance went up puts you in a position to act. Shopping around for quotes typically saves $300 to $600 annually, raising your deductible cuts premiums by 20 to 40 percent if you have emergency savings to back it up, and bundling policies unlocks discounts most homeowners never claim.

Start with one action this week: request quotes from two or three other carriers and compare them to your current renewal notice. You will see immediately whether your current insurer is pricing competitively or whether switching saves money. Then tackle your deductible and ask about bundling opportunities.

We at Direct Insurance Services work with top-rated carriers across Utah to find coverage that matches both your needs and your budget. Our independent agency approach means we shop on your behalf and explain exactly why your premium changed. Schedule a policy review with us today to verify your coverage aligns with your home’s current value and to uncover discounts you may have missed.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation