How to Find Cheap Auto Insurance for New Drivers

New drivers face auto insurance premiums that average 50% higher than experienced drivers. The lack of driving history makes insurers view them as high-risk customers.

We at Direct Insurance Services know finding the cheapest auto insurance for new drivers requires smart strategies and patience. The right approach can save hundreds of dollars annually while maintaining proper coverage.

Why Do New Drivers Pay Double for Insurance

Teen Drivers Face Staggering Accident Statistics

Teen drivers aged 16 to 19 are nearly three times more likely to be involved in fatal accidents per mile driven compared to other age groups, according to the Insurance Institute for Highway Safety. Male teen drivers represent 68% of the teen crash fatality rate, which explains why they pay about $50 more per month than female drivers.

These numbers translate directly to your premium calculations. A 17-year-old male driver pays approximately $4,351 annually while females pay around $3,478 (based on U.S. News research). The difference stems from concrete crash data that insurers track meticulously.

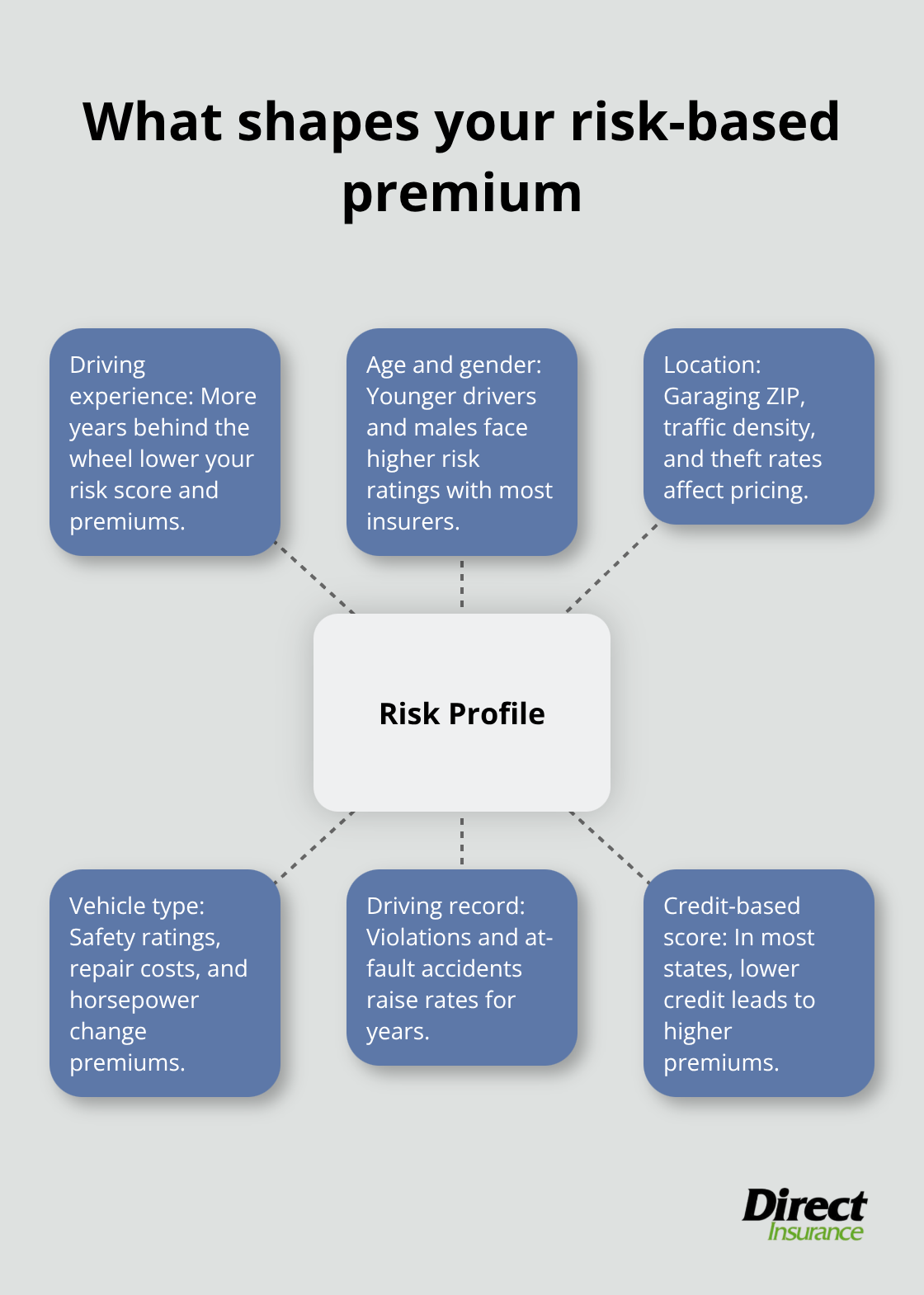

Insurance Companies Use Mathematical Risk Models

Insurers base their rates on decades of claims data that show drivers with less than one year of experience pay approximately 40% more for basic coverage compared to those with five years of experience. Your premium reflects this mathematical reality rather than personal judgment.

The average monthly premium drops from $898 for a 16-year-old to $511 for a 19-year-old, which demonstrates how experience reduces risk assessment scores. Companies like Erie and USAA have developed sophisticated algorithms that factor in age, gender, location, and vehicle type to calculate your exact risk profile.

Experience Reduces Rates Predictably

This data-driven approach means your rates will decrease predictably as you gain experience and maintain a clean record. The mathematical models show consistent patterns across all major insurers (regardless of their specific underwriting guidelines).

Your age alone triggers automatic rate reductions at specific milestones. Most insurers offer significant discounts when you turn 25, assuming you maintain a violation-free record. Understanding these risk factors helps you make informed decisions about coverage options and cost-saving strategies.

How Can New Drivers Cut Insurance Costs in Half

Compare Quotes From Multiple Company Types

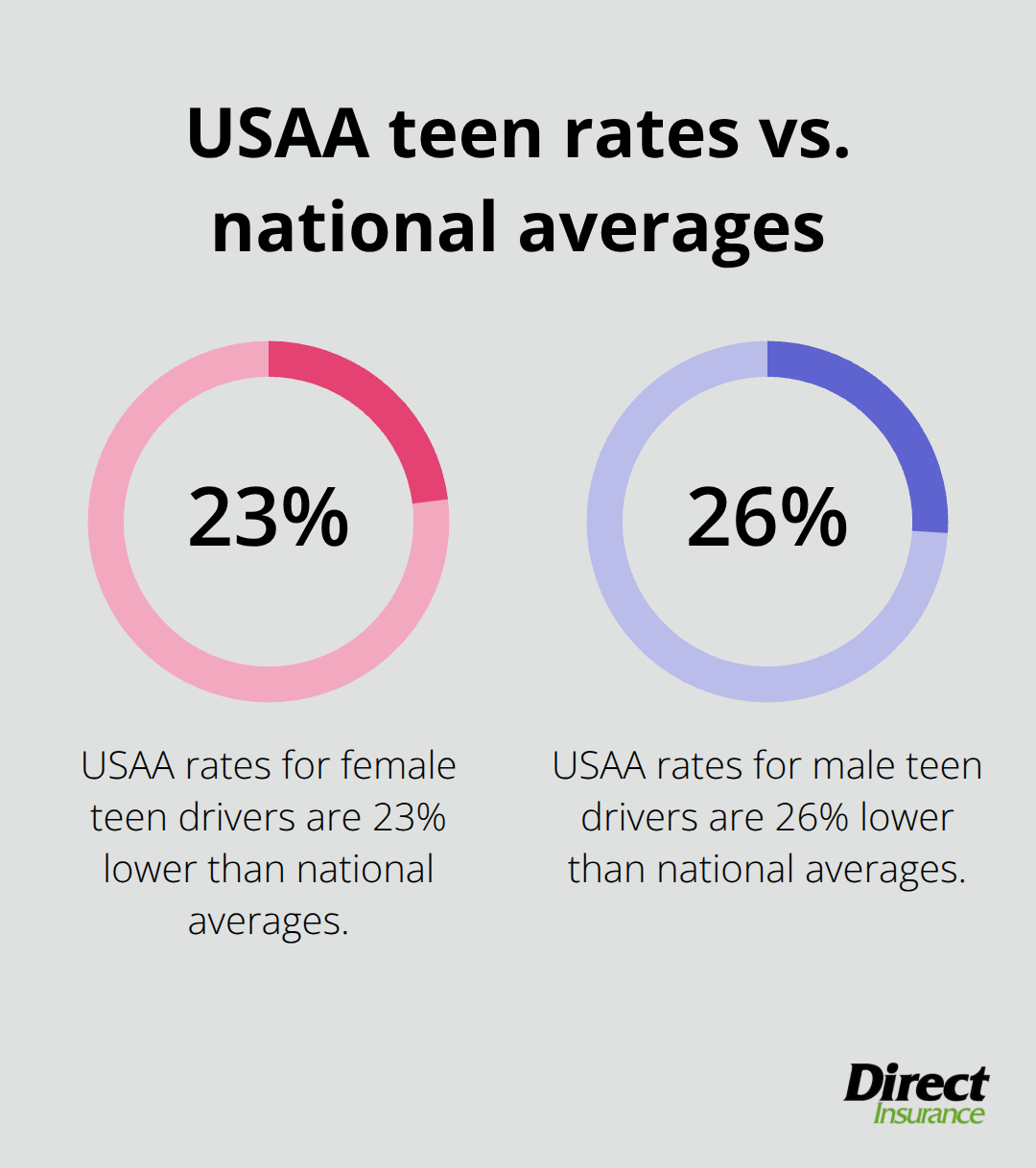

You need quotes from at least five different insurers to save thousands annually. Erie offers the lowest average rates for teen drivers at $3,478 for females and $4,351 for males according to U.S. News research. USAA provides rates 23% lower than national averages for female teens and 26% lower for males. Auto-Owners and Travelers also rank among the cheapest options with monthly premiums that start at $343 and $360 respectively (according to The Zebra data).

Regional carriers often beat national companies by 15-20% because they focus on local risk factors rather than broad statistical models.

Stack Multiple Discounts for Maximum Savings

Good student discounts save families between 10% and 25% on their car insurance premiums when you maintain a 3.0 GPA or higher. Defensive driving courses provide additional reductions of 5-10% according to industry data. Telematics programs like Progressive’s Snapshot and State Farm’s Drive Safe & Save can cut premiums by up to 30% for safe drivers who accept monitoring technology. You save up to 60% when you stay on your parents’ policy compared to individual coverage for drivers under 25. Multi-vehicle discounts, low-mileage programs, and bundled renters insurance create additional savings that compound significantly.

Adjust Deductibles and Coverage Strategically

You reduce premiums by 15-25% when you raise your deductible from $500 to $1,000 without compromising essential protection. However, you should avoid minimum coverage which meets only state liability requirements. The Insurance Information Institute recommends at least 100/300/100 limits for teen drivers to protect against lawsuits. Umbrella coverage costs under $200 annually but provides additional liability protection that makes financial sense for families with young drivers who face higher accident risks.

These immediate cost-reduction strategies work best when you combine them with long-term approaches that build your insurance profile over time.

What Builds Your Insurance Profile Over Time

Your Driving Record Determines Future Premiums

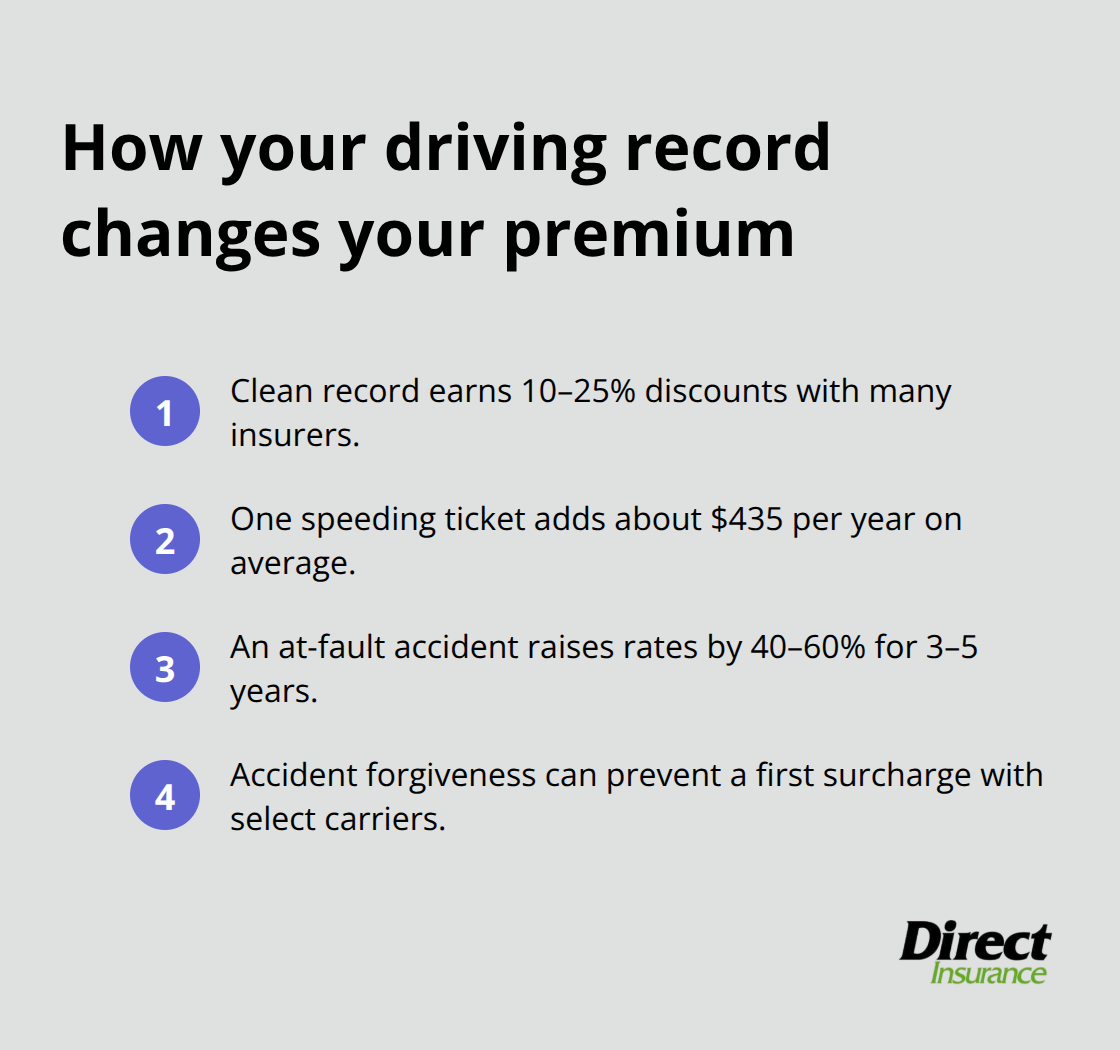

A violation-free record saves you thousands annually as your insurance profile improves. Drivers with clean records receive discounts of 10% to 25% on annual premiums according to industry data. A single speeding ticket increases your premium by an average of $435 per year, while an at-fault accident raises rates by 40-60% for three to five years.

The mathematical impact compounds over time. A 20-year-old with one violation pays approximately $6,500 annually compared to $5,448 for clean drivers. State Farm and other major insurers offer accident forgiveness programs that prevent rate increases after your first at-fault incident.

Credit Scores Control Insurance Costs More Than Most Realize

Your credit score impacts insurance rates as significantly as your driving record in most states. Insurers use credit-based insurance scores to predict claim likelihood, with poor credit increasing premiums by 50-100% compared to excellent credit (in states where this practice is legal).

Young adults should focus on building credit through student credit cards, authorized user status on family accounts, and consistent payment history. Annual premium payments eliminate monthly processing fees and demonstrate financial responsibility to insurers.

Defensive Driving Courses Provide Immediate Benefits

Completing a defensive driving course qualifies you for discounts of 5-15% with most major insurers. These courses teach advanced safety techniques that reduce accident risk and demonstrate your commitment to safe driving practices. Many states require insurers to offer these discounts, making the investment worthwhile for new drivers.

The courses typically cost $25-50 but save hundreds annually on premiums. Online options make completion convenient, and certificates remain valid for multiple years depending on your state’s requirements.

Telematics Programs Reward Safe Habits

Usage-based insurance programs track your driving behavior through smartphone apps or plug-in devices. Progressive’s Snapshot, State Farm’s Drive Safe & Save, and similar programs can reduce premiums by up to 30% for safe drivers who accept monitoring technology.

These programs measure factors like hard braking, rapid acceleration, phone use while driving, and time of day you drive. New drivers who demonstrate consistent safe habits see the largest discounts because they overcome the statistical risk assumptions that drive high initial rates.

Final Thoughts

New drivers can cut insurance costs dramatically when they compare quotes from at least five insurers and stack multiple discounts. Regional carriers often beat national companies by 15-20%, while good student programs and telematics monitoring reduce premiums by up to 30%. The cheapest auto insurance for new drivers combines these immediate strategies with smart coverage choices (like raising deductibles from $500 to $1,000).

Insurance costs drop predictably as you gain experience and maintain a clean record. A single speeding ticket adds $435 annually to your premium, while staying on your parents’ policy saves up to 60% compared to individual coverage. Credit score improvements also reduce rates significantly in most states.

We at Direct Insurance Services help Utah drivers compare options from multiple carriers to find affordable coverage. Our team provides personalized guidance on auto insurance solutions that protect your vehicle without breaking your budget. Contact us today to start saving on your auto insurance premiums.